Tax Deduction Dispute: Court Upholds Tribunal’s Decision on Contractor Status

Full News

Tax Deduction Dispute: Court Upholds Tribunal’s Decision on Contractor Status

Tax Deduction Dispute: Court Upholds Tribunal’s Decision on Contractor Status

A business owner (let’s call them the appellant) is challenging a decision made by the Income Tax Appellate Tribunal. The main issue? Whether a guy named Suresh should be considered an employee or a sub-contractor. This distinction is crucial because it affects the tax deductions the business owner was supposed to make. Long story short, the court sided with the tax authorities and dismissed the appeal.

Get the full picture - access the original judgement of the court order here

Case Name:

Prasanna Radha Krishnan Vs Income Tax Officer (High Court of Kerala)

I.T.A. No. 28 of 2015

Date: 18th July 2016

Key Takeaways:

- The court upheld the Tribunal’s factual finding that Suresh was a sub-contractor, not an employee.

- This classification triggered the requirement for tax deduction under Section 194C (of Income Tax Act, 1961).

- Failure to make these deductions resulted in disallowance under Section 40(a)(ia) (of Income Tax Act, 1961).

- The court emphasized that factual findings by the Tribunal are generally not interfered with in appeals under Section 260A (of Income Tax Act, 1961).

Issue:

The main question here is: Should the appellant (the business owner) have been required to deduct tax under Section 194C (of Income Tax Act, 1961) for payments made to Suresh, and consequently, was the disallowance under Section 40(a)(ia) (of Income Tax Act, 1961) justified?

Facts:

- This all went down during the 2009-2010 assessment year.

- The appellant is a distributor for Hindustan Petroleum Corporation Limited, dealing with Liquefied Petroleum Gas.

- The appellant made payments to a guy named Suresh for transportation services.

- The tax authorities said, “Hey, you should have deducted tax from these payments under Section 194C (of Income Tax Act, 1961) because Suresh is a sub-contractor.”

- The appellant disagreed, saying, “No way, Suresh is just an employee, not a sub-contractor.”

- This disagreement led to a disallowance of the payments under Section 40(a)(ia) (of Income Tax Act, 1961).

- The case went through various stages - from the Assessing Officer to the Commissioner (Appeals) to the Income Tax Appellate Tribunal, and finally to this High Court.

Arguments:

From the appellant’s side:

- “Look, Suresh is just an employee. We shouldn’t have to deduct tax under Section 194C (of Income Tax Act, 1961) for payments to employees.”

From the tax authorities’ side:

- “Nope, Suresh is clearly a sub-contractor. The appellant should have deducted tax under Section 194C (of Income Tax Act, 1961).”

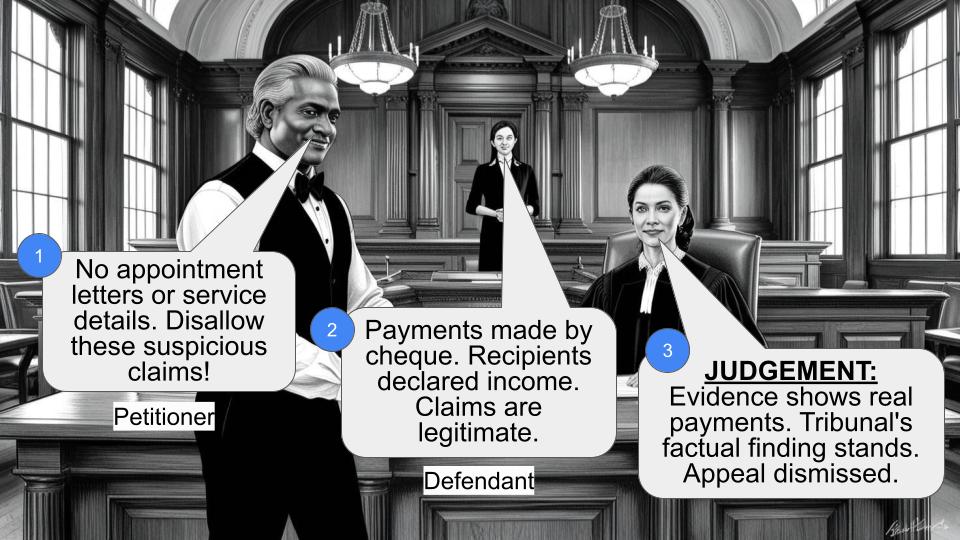

- They pointed out that lump sum payments were made to Suresh, and he was entirely responsible for transportation without accounting for expenses to the appellant.

- They also noted that if Suresh was an employee, he would have provided details like truck numbers, names of truck owners and drivers, etc., which he didn’t.

Key Legal Precedents:

Interestingly, this judgment doesn’t cite any specific legal precedents. Instead, it focuses on the application of specific sections of the Income Tax Act to the facts of the case.

Judgement:

The court basically said, “Sorry, appellant, but we’re siding with the tax folks on this one.” Here’s why:

- They agreed with the Tribunal’s finding that Suresh was indeed a sub-contractor, not an employee.

- They said this factual finding wasn’t “perverse” (lawyer-speak for “obviously wrong”), so they wouldn’t mess with it.

- Given that Suresh was a sub-contractor, Section 194C (of Income Tax Act, 1961) applied, meaning tax should have been deducted.

- Since the appellant didn’t deduct this tax, the disallowance under Section 40(a)(ia) (of Income Tax Act, 1961) was justified.

- The appeal was dismissed, with the court answering the question of law in favor of the Revenue (tax authorities) and against the appellant.

FAQs:

Q: What’s the big deal about Suresh being a sub-contractor instead of an employee?

A: It’s all about taxes! If Suresh is a sub-contractor, the business has to deduct tax from payments to him. If he’s an employee, they don’t.

Q: Why didn’t the court change the Tribunal’s decision?

A: Courts generally don’t mess with factual findings made by lower courts or tribunals unless they’re clearly wrong. In this case, they thought the Tribunal’s reasoning made sense.

Q: What’s this Section 194C (of Income Tax Act, 1961) everyone keeps talking about?

A: It’s a part of the Income Tax Act that says you need to deduct tax at source when you’re paying contractors or sub-contractors.

Q: What happens now that the appeal was dismissed?

A: The appellant will have to accept the disallowance under Section 40(a)(ia) (of Income Tax Act, 1961) and pay the additional tax resulting from this disallowance.

Q: Could this case affect other businesses?

A: Absolutely! It’s a reminder for businesses to be clear about the status of their workers (employee vs. contractor) and to make sure they’re following the right tax deduction rules.

1. This appeal is filed by the assessee challenging the order passed by the Income Tax Appellate Tribunal, Cochin Bench in I.T.A.No.153/14. During the assessment year 2009-2010, on the ground of non compliance of Section 194C (of Income Tax Act, 1961) in respect of the payments made by the assessee to one Suresh, who was found to be a sub-contractor, the amounts paid were disallowed under Section 40(a)(ia) (of Income Tax Act, 1961). The assessee filed appeal and the Commissioner (Appeals) considered the contention of the assessee that Sri. Suresh was only an employee and not a sub-contractor for transportation of the Liquefied Petroleum Gas manufactured and marketed by Hindustan Petroleum Corporation Limited whose distributor is the assessee.

2. In his order, the Commissioner came to the factual finding that Sri.Suresh is a Sub Contractor of the assessee and that from out of the payments made to such a sub-contractor, deduction under Section 194C (of Income Tax Act, 1961) should have been made. The Commissioner, accordingly, found that since the assessee has not made deduction under Section 194C (of Income Tax Act, 1961), disallowance under Section 40(a)(ia) (of Income Tax Act, 1961) is legal. This order was again challenged by the assessee before the Income Tax Appellate Tribunal by filing I.T.A.No. 153/14 and by the impugned order, the Tribunal dismissed the appeal. It is this order, which is under challenge before us.

3. We heard the counsel for the appellant and the learned Senior Standing Counsel appearing for the Revenue.

4. The question of law that is framed for our consideration is whether the Tribunal ought to have held that the appellant is not liable to deduct tax under Section 194C (of Income Tax Act, 1961) and whether the Tribunal should have deleted the addition of income on account of disallowance under Section 40(a)(ia) (of Income Tax Act, 1961). Although the contention that Sri.Suresh being only an employee of the assessee and that, therefore, Section 194C (of Income Tax Act, 1961) is not attracted, is reiterated before us, we find that, on facts, the Tribunal came to a finding that Sri.Suresh is a sub-contractor of the assessee. This factual finding of the Tribunal is based on its findings that lump sum payments were made by the assessee to Suresh and that Suresh was entirely responsible for transportation without even accounting to the assessee the expenses incurred by him for discharge of the transportation work. Tribunal further found that if Suresh was her employee as contended by the assessee, Suresh would have furnished to the assessee the truck numbers, names and addresses of the truck owners, drivers and the payments made by him to each of the trucks engaged by him. Tribunal found that none of these details were furnished by the assessee at any stage of the proceedings either before the Assessing Officer or the 1st Appellate Authority or the Tribunal. Such a finding of fact arrived at by the Tribunal that Sri.Suresh was a sub-contractor, is not perverse to be interfered in an appeal under Section 260A (of Income Tax Act, 1961). Once we accept the status of Sri.Suresh as a sub- contractor, the liability under Section 194C (of Income Tax Act, 1961) is automatically attracted. Admittedly, the assessee has not effected deduction under the said Section. Consequence thereof is disallowance under Section 40(a)(ia) (of Income Tax Act, 1961).

5. In such circumstances, the order passed by the Tribunal dismissing the appeal of the assessee does not merit interference. Therefore, answering the question of law framed in favour of the Revenue and against the assessee, this appeal is dismissed.

SD/-

ANTONY DOMINIC

JUDGE

SD/-

DAMA SESHADRI NAIDU

JUDGE

×