Tribunal upholds commission deduction claim after AO fails to follow remand dir…

Full News

Tribunal upholds commission deduction claim after AO fails to follow remand directions

Tribunal upholds commission deduction claim after AO fails to follow remand directions

The Income Tax Department (the revenue) is challenging a company's claim for deduction of commission payments. The Income Tax Appellate Tribunal (ITAT) sided with the company, allowing the deduction. The revenue wasn't happy with this and took it to the High Court, but the court dismissed their appeal, agreeing with the ITAT's decision.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Official Liuidator (High Court of Madras)

Tax Case (Appeal) No.79 of 2004

Date: 22nd October 2007

Key Takeaways:

1. When a higher authority (like the ITAT) gives specific directions on remand, lower authorities (like the Assessing Officer) must follow them.

2. If directions aren't followed, the higher authority can uphold the assessee's claim.

3. Consistency in tax treatment across assessment years is important.

4. Courts value proper investigation and verification of evidence.

Issue:

Was the Income Tax Appellate Tribunal correct in allowing the assessee's deduction for commission payments, despite the National Rayon Corporation stating no middlemen were involved?

Facts:

- We're looking at the assessment year 1975-76.

- The company (now under liquidation) claimed a deduction of Rs. 3,00,034 for commission paid to P.M. Traders.

- This commission was supposedly for selling wood pulp and buying caustic soda from National Rayon Corporation Limited.

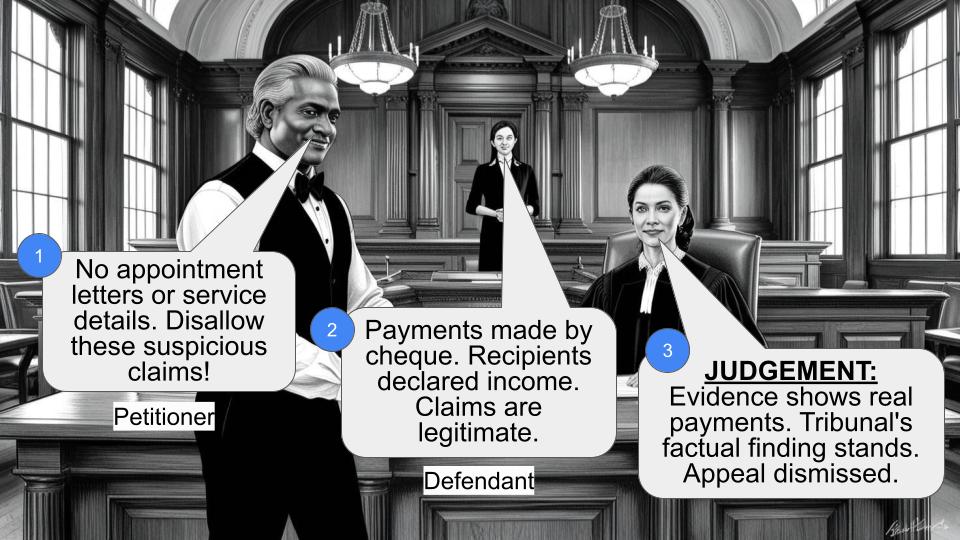

- The Assessing Officer (AO) initially disallowed this, calling it bogus.

- The case went through multiple rounds of appeals and revisions.

- The ITAT eventually allowed the deduction, which the revenue challenged in the High Court.

Arguments:

Revenue's side:

- The AO's reasons for disallowing the deduction were solid.

- National Rayon Corporation said they didn't use any middlemen, proving the claim was fake.

Company's side:

- The ITAT considered P.M. Traders' statement accepting the commission.

- The AO didn't follow the ITAT's earlier directions to investigate P.M. Traders.

- Similar deductions were allowed in subsequent years without the department challenging them.

Key Legal Precedents:

Interestingly, this case doesn't cite specific legal precedents. However, it relies on the principle that lower authorities must follow directions given by higher authorities on remand. The court also emphasizes the importance of consistent treatment across assessment years.

Judgement:

The High Court dismissed the revenue's appeal, agreeing with the ITAT. Here's why:

1. The AO didn't follow the ITAT's earlier directions to verify P.M. Traders' letter.

2. The revenue accepted similar deductions in subsequent years.

3. The court found no irregularity in the ITAT's order.

FAQs:

1. Q: Why did the court side with the company?

A: The court felt the AO didn't follow proper procedure by ignoring the ITAT's directions and failing to verify crucial evidence.

2. Q: Does this mean all commission claims will be allowed now?

A: Not necessarily. Each case is unique, but this judgment emphasizes the importance of following proper investigation procedures.

3. Q: What's the significance of subsequent years' treatment?

A: It shows that consistency in tax treatment is important. If the department accepted similar claims in later years, it weakens their case for the current year.

4. Q: Could the revenue have won this case?

A: Possibly, if they had evidence that the AO followed the ITAT's directions or if they had challenged similar deductions in subsequent years.

5. Q: What's the main lesson for tax authorities from this case?

A: Always follow directions given by higher authorities on remand, and conduct thorough investigations as instructed.

1. The assessee's assessment order in respect of the assessment year 1975-76 has been revised more than once in order to give effect to the order of the Commissioner of Income-tax (Appeals) and Appellate Tribunal and also further modified on rectification of the mistakes. The amount claimed as a deduction in a sum of rs.3,00,034/- on account of commission paid to one P.M.Traders was rejected. The assessee claimed that the commissions were paid for sale of wood pulp and purchase of caustic soda from National Rayon Corporation Limited. The Assessing Officer verified the assessment records of both recipients of the commission and also made enquiries through National Rayon Corporation Limited, who denied having any middle man to the business. The assessing officer accordingly disallowed the payment of commission treating it as bogus. On appeal, the Commissioner of Income-tax (Appeals) upheld disallowance with respect to the payment to P.M.Traders. The assessee filed an appeal against the order of the Commissioner of Income-tax (Appeals) to the Income-tax Appellate Tribunal. The Tribunal has allowed the appeal on the ground that the receipt of commission has been accepted by the recipient by its letter and in the absence of any method to discard the admission the deduction should have been granted. Aggrieved by the said order of the Appellate Tribunal, the revenue filed this appeal and the appeal was admitted on the following substantial questions of law:

"1. Whether on the facts and in the circumstances of the case, the Appellate Tribunal was right in law in allowing deduction of the commission payment by the assessee on the ground that the commission agents were not examined, in spite of the fact that National Rayon Corporation had clearly said that no middlemen were engaged in the transaction?

2. Whether on the facts and in the circumstances of the case, the Appellate Tribunal was right in law in allowing deduction of the commission payment by the assessee, when it was clearly a colourable device to fund extra commercial considerations?

2. The learned counsel appearing for the revenue vehemently contended that the reasoning given by the assessing officer, which is confirmed by the Commissioner of Income-tax (Appeals) are unassailable reasons. The other fact that the National Rayon Corporation has given a statement that no middle men were engaged by them in the transaction would also go to prove the bogus claim of the assessee that finding would not have been reversed by the Tribunal.

3. On the contrary, the learned counsel appearing for the respondent Company, which is under liquidation, has submitted that the Tribunal has passed an order after taking note of the statement given by the person to whom the commission has been given. The Tribunal further taken into consideration of the fact that earlier the Tribunal has passed an order of remittal with a direction to the assessing officer to enquire the person i.e., P.M.Traders to whom the commission has been paid. That direction has not been complied with by the assessing officer. On the contrary, the assessing officer has enquired some of the officers of the National Rayon Corporation, which is not a direction given by the Tribunal. He further contended that in respect of the subsequent assessment years, the Tribunal has taken the same view as taken in the present case, which has not been agitated by the Department, rather it is accepted by the Department. When that being the position, for the present assessment year, they cannot take a different view.

4. We heard the argument of the learned counsel on either side and perused the materials on record.

5. The learned counsel appearing for the revenue has fairly submitted that in respect of the subsequent assessment years, he is not in a position to place before this Court any material as to whether the matters have been taken on appeal, as he was also not sure whether appeals have been filed or not. However, the learned counsel appearing for the Company under liquidation submits that till date, no notice has been received by the Company under liquidation in any case in respect of the subsequent assessment years. From that, it is clear that for the subsequent assessment years, the revenue has accepted the finding arrived at by the Tribunal.

6. In addition to that, one more factor needs to be stated is that in respect of the assessment year, when the matter was originally carried to the Income-tax Appellate Tribunal, the Tribunal after taking into consideration of the submission formed an opinion that the matter requires fresh investigation on the ground that as per the records, the partnership deed of the P.M.Traders executed in April 1986 was to take effect from 1.1.1984, which was not taken into account by the Income Tax Officer, who had seen the document. In addition to that, the assessing officer has not considered the letter dated 31.12.1975 submitted by the P.M.Traders to the effect that they did receive the commission from the assessee and verified the same with the P.M.Traders. The assessing officer also failed to verify whether the partnership was for the purpose of exploiting the agreement with the assessee for the purpose of business. The Tribunal ultimately set aside all orders of the authorities below and remitted the matter to the Income-tax Officer for making fresh assessment after a proper investigation by examining the agent the P.M.Traders after giving the assessee an opportunity of being heard.

7. On remittal also, from the records, it could be seen that the assessing officer has not even taken the pain of verifying the letter dated 31.12.1975 issued by P.M.Traders accepting the receipt of the commission from the assessee. However, the assessing officer thought it fit enough to inquire with one of the Officers of the National Rayon Corporation. The assessing officer on the basis of the statement recorded from one of the officers of the National Rayon Commission has rejected the claim for payment of commission to P.M.Traders.

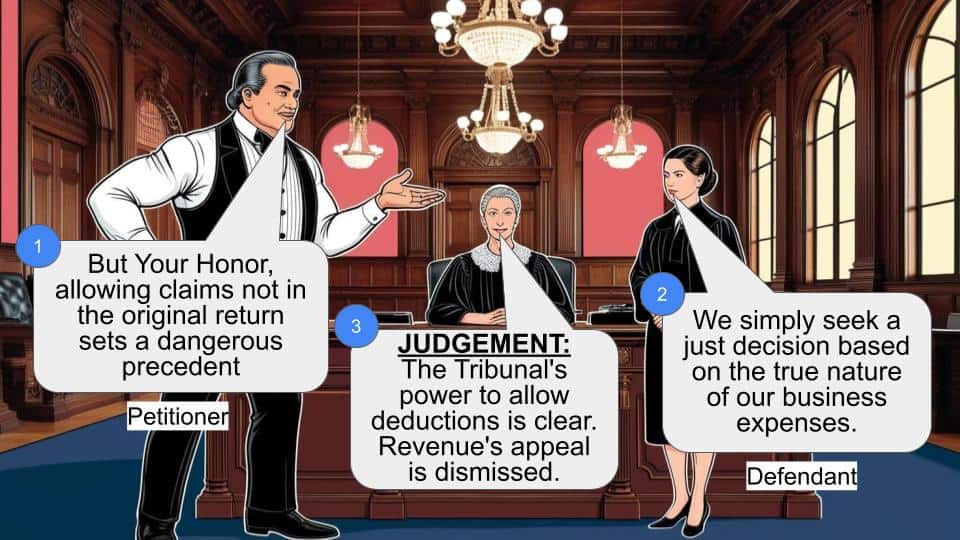

8. It is well established legal principle that in the hierarchy of the statutory authorities, when the higher fact finding authority remitted the matter with a direction to the lower authority to follow certain procedure, so as to be within the statutory provision, the lower authority has to make that exercise as directed by the Tribunal. In this case, as rightly pointed out by the counsel for the assessee as well as in the order of the Tribunal, the Income-tax Officer has totally flouted the direction to verify with the letter dated 31.12.1975 by which the P.M.Traders has accepted that they did receive the commission from the assessee. On the other hand, much reliance has been placed by the authorities below on the statement given by one of the officers of the National Rayon Commission.

9. Having regard to the totality of the circumstances of the case, and with particular reference to the Tribunal Order, which has extracted the orders made by the Tribunal in respect of the assessee's case in the subsequent years to the effect that the claim of the assessee in regard to payment of commission to P.M.Traders deserves to be upheld, the further factual position as to the non-verification of the letter dated 13.12.1975 issued by P.M.Traders, who by that letter accepted the receipt of commission, we do not find any irregularity in the order of the Tribunal.

10. After perusal of the records, we are of the view that the order of the Tribunal requires no modification and the questions of law framed were answered in affirmative against the revenue and the appeal is dismissed.

To

1. The Asst.Registrar Income tax Appellate Tribunal Chennai.

2. The Commissioner of Income tax Coimbatore.

3. The Inspecting Asst.Commissioner of Incometax (Assessment) Range I Coimbatore.

4. The Commissioner of Income tax (Appeals) Coimbatore.

5. The Deputy Commissioner Special Range I Coimbatore.

×

Similar Ripples

Questions

Tribunal upholds commission deduction claim after AO fails to follow remand directions

Write your CommentSimilar Posts

Generic

- Reportdata/5258.pdf