Full News

When and How to Apply for Compounding of offence under Income Tax Act?

When and How to Apply for Compounding of offence under Income Tax Act?

Have you ever wondered what happens if you accidentally run afoul of the Income-tax Act? The concept of 'compounding' offers a way to rectify such mistakes without going through lengthy legal battles. Here's a straightforward guide designed to help you understand and act with confidence, providing a detailed overview of how to approach the compounding of offences under the Income-tax Act, including application timelines, fees, and other critical considerations.

Filing of Application

The process begins with the filing of an application for compounding to the competent authority, detailed as follows:

Application Details

Form: Must be submitted in the prescribed format outlined in Annexure-I, on a ₹100 stamp paper.

Time Limit: Can be filed at any time post-offence but has implications on the compounding charges.

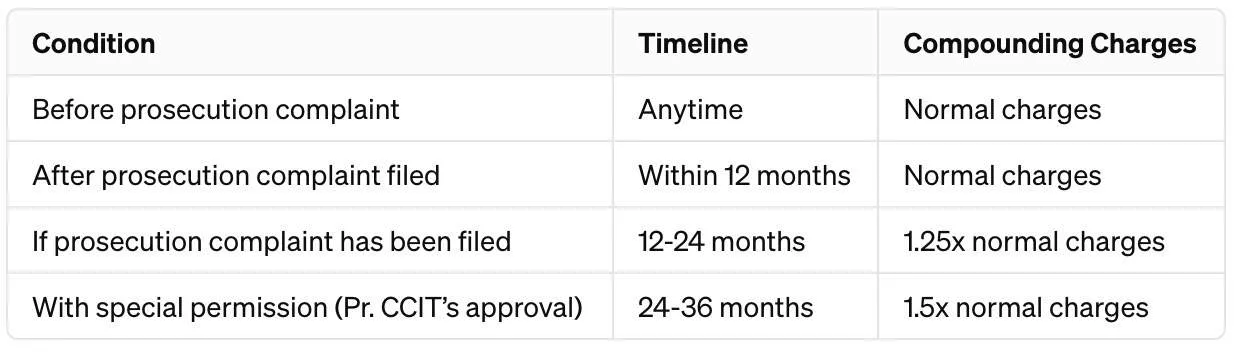

Timeline for Filing

Important Notes:

Relaxation of Time Limit: Applications can be filed after 12 months but within 36 months under special circumstances, subject to increased compounding charges.

Payment of Outstanding Dues

Requirement: All due taxes, interest, penalties, and other sums related to the offence must be cleared before the application.

Procedure: If any outstanding amount is discovered, it must be paid within 30 days of notification.

Compounding Charges

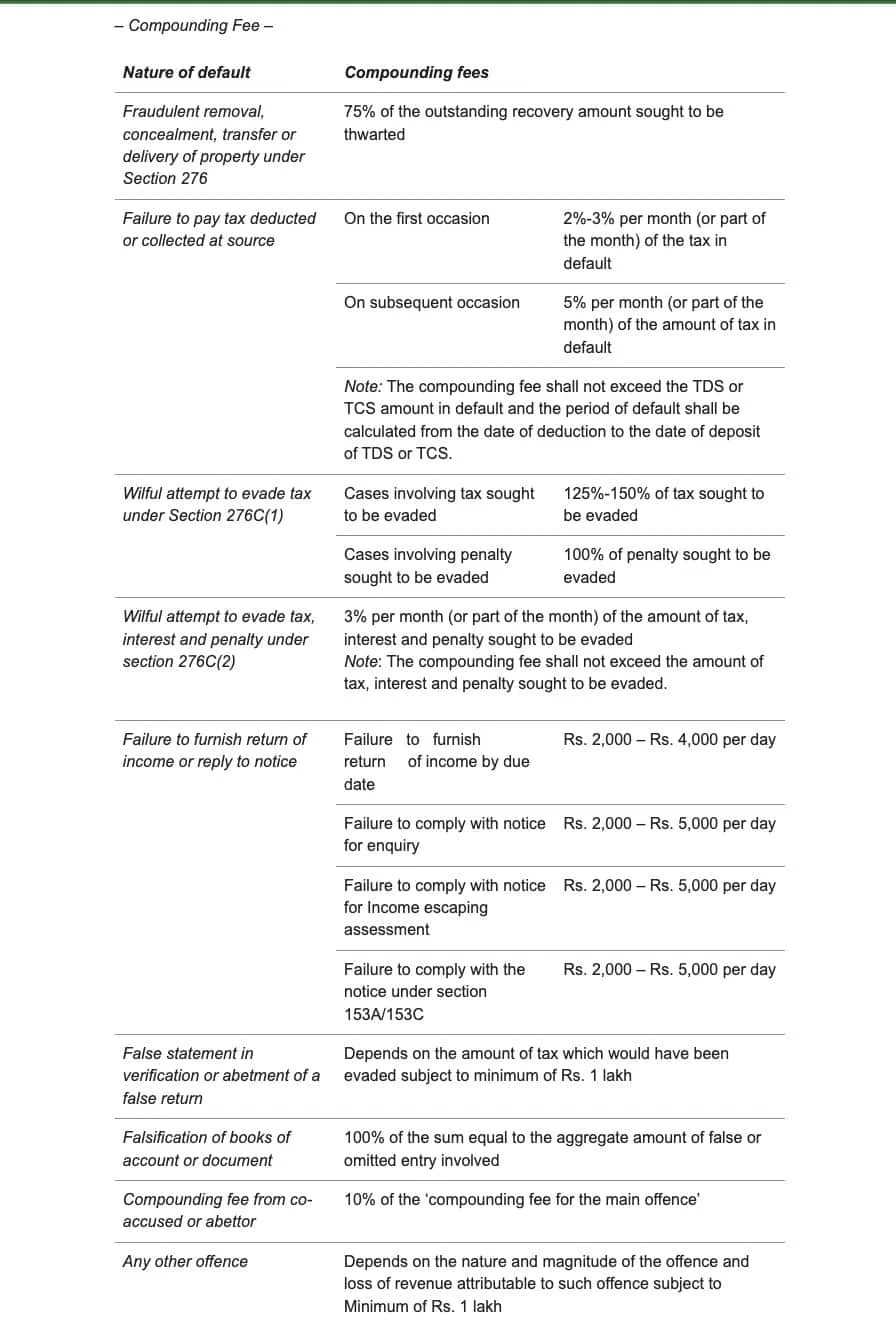

The charges vary based on the nature of the default and the timing of the application.

Detailed Charges

Additional Charges

Prosecution Establishment Expenses: 10% of the compounding fees, minimum ₹25,000.

Interest for Delayed Payment: Charged if the compounding charge payment is delayed beyond one month from the notification date.

Other Key Conditions

Withdrawal of Appeal: Applicants must withdraw any appeals related to the offence being compounded.

Disclosure: Full disclosure of all defaults related to the offence is required for compounding.

Authority and Jurisdiction

The Principal Chief Commissioner or Chief Commissioner has the authority to compound an offence.

In cases involving multiple jurisdictions, the application should be filed with the commissioner in charge of the region where the applicant's PAN is registered.

Conclusion of Procedure

Review and Decision: Upon receiving the application, the competent authority reviews it, considering reports from the assessing officer, and then issues a decision.

Practical Scenario

Imagine a business owner who inadvertently failed to pay taxes due. Realizing the mistake, the owner decides to apply for compounding within 10 months, ensuring all related dues are cleared. By doing so within the stipulated time, the owner is subject to normal compounding charges, thereby avoiding further legal complications.

×