Full News

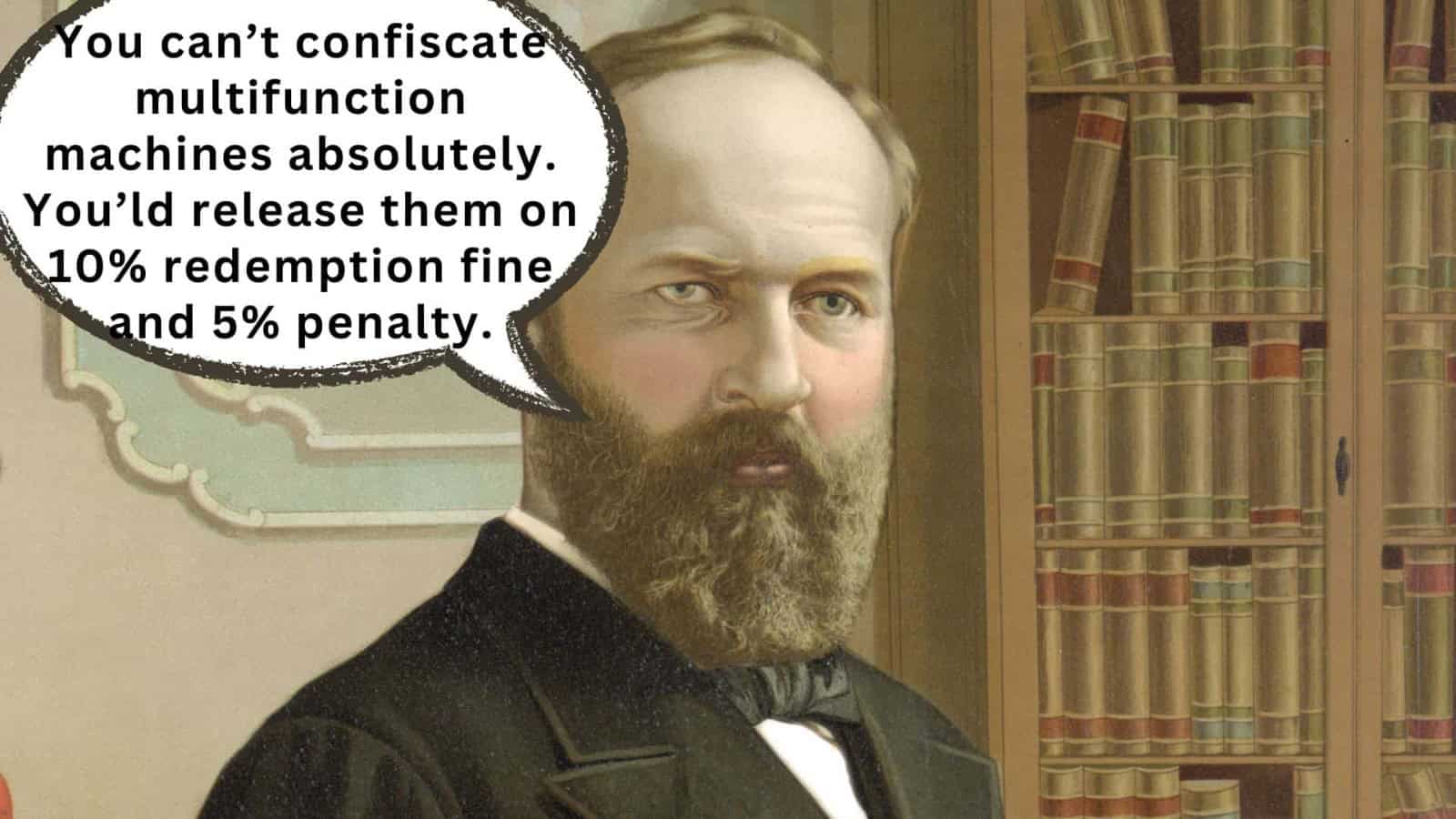

Customs Tribunal reduces redemption fine and penalty for import of used multifunction machines.

Customs Tribunal reduces redemption fine and penalty for import of used multifunction machines.

The case involves the import of 244 units of used multifunction machines by J J Graphics from Chennai. The customs authorities alleged violation of various provisions and ordered absolute confiscation of the goods along with a penalty equal to the value of the goods. The appellant challenged the order, and the matter reached the Customs, Excise and Service Tax Appellate Tribunal (CESTAT), Bangalore.

Case Name:

J J Graphics Vs Commissioner of Customs (CESTAT Bangalore)

Key Takeaways:

- The Tribunal held that the goods are not liable for absolute confiscation and should be released on payment of an appropriate redemption fine.

- The Tribunal reduced the redemption fine to 10% and the penalty to 5% of the enhanced assessable value of the imported goods.

- The decision follows the precedent set by the Kerala High Court in the case of Commissioner of Customs, Cochin vs. Office Devices.

Issue:

Should the imported used multifunction machines be absolutely confiscated, and what should be the appropriate redemption fine and penalty?

Facts:

- J J Graphics imported 244 units of used multifunction machines and filed a Bill of Entry declaring the value as USD.51,575 (equivalent to Rs.34,00,286).

- The goods were examined by a DGFT-approved Chartered Engineer, who assessed the value at Rs.42,49,780.

- The Adjudication Authority ordered absolute confiscation of the goods and imposed a penalty of Rs.42,49,780 under Section 112(a)(i) of the Customs Act, 1962.

- The Commissioner (Appeals) held that the goods are not liable for absolute confiscation but should be released on payment of an appropriate redemption fine. The penalty was upheld.

Arguments:

The appellant argued that the issue of confiscation was settled by the Supreme Court in the case of Commissioner of Customs vs. M/s Atul Automation Pvt Ltd, and the goods are liable for confiscation. However, the redemption fine and penalty should be reduced to 10% and 5% of the enhanced assessable value, respectively, following the Tribunal’s decisions in similar cases.

The Revenue argued that the remand order by the Commissioner (Appeals) was proper and sustainable, citing the Tribunal’s decision in the case of M/s S.R. Enterprises & M/s Digital Enterprise, where the matter was remanded to determine the market value and quantify the redemption fine.

Key Legal Precedents:

- Commissioner of Customs vs. M/s Atul Automation Pvt Ltd (Supreme Court)

- Commissioner of Customs, Cochin vs. Office Devices - 2009 (240) E.L.T. 336 (Ker.) (Kerala High Court)

- M/s S.R. Enterprises & M/s Digital Enterprise (CESTAT, Bangalore)

- M/s Photofax Systems vs. CC, Bangalore (CESTAT, Bangalore)

- M/s City Office Equipment vs. CC, Bangalore (CESTAT, Bangalore)

Judgment:

The Tribunal partially allowed the appeal and reduced the redemption fine to 10% and the penalty to 5% of the enhanced assessable value of the imported goods. The Tribunal followed the precedent set by the Kerala High Court in the case of Commissioner of Customs, Cochin vs. Office Devices and its own decisions in similar cases involving the import of used multifunction machines.

FAQs:

Q1: What was the main issue in this case?

A1: The main issue was whether the imported used multifunction machines should be absolutely confiscated, and what should be the appropriate redemption fine and penalty.

Q2: Why did the Tribunal reduce the redemption fine and penalty?

A2: The Tribunal reduced the redemption fine and penalty based on its own precedents and the judgment of the Kerala High Court in a similar case involving the import of used multifunction machines.

Q3: What was the rationale behind the Tribunal’s decision?

A3: The Tribunal considered that the goods were not liable for absolute confiscation and took a lenient view by releasing the goods on payment of a reduced redemption fine and penalty, following the precedents in similar cases.

Q4: What was the impact of the Tribunal’s decision?

A4: The Tribunal’s decision provided relief to the importer by reducing the redemption fine and penalty, allowing them to redeem the goods for home consumption on payment of the reduced amounts.

Q5: What was the significance of the legal precedents cited in the case?

A5: The legal precedents, particularly the Supreme Court and High Court judgments, played a crucial role in guiding the Tribunal’s decision. The Tribunal followed the precedents set by higher courts and its own decisions in similar cases involving the import of used multifunction machines.

The appellant had imported 244 units of used Multifunction machines and filed Bill of Entry No. 2749299 dt.07.08.2017 declaring the value as USD 51575 equivalent to Rs.34,00,286/-. Goods were subjected to examination by DGFT approved Chartered Engineer and vide report dated 26.09.2017, the Charted Engineer assessed the value of the goods as Rs.42,49,780/-. Alleging violation of various provisions of law, a show cause notice dated 03.12.2018 was issued. Thereafter, the Adjudication Authority issued the order on 23.08.2019, whereby ordered absolute confiscation of the goods. For the alleged violation, the Adjudication Authority imposed penalty of Rs.42,49,780/- under section 112(a)(i) of the Customs Act, 1962. Aggrieved by the said order, the appellant filed an appeal before the Commissioner (Appeals). The Commissioner (Appeals) vide order dated 11.11.2021 after considering the various judgments of the Hon’ble Supreme Court and this Tribunal in similar cases, held that goods are not liable for absolute confiscation and remanded the matter by allowing redemption of goods on payment of appropriate redemption fine. Penalty imposed by the adjudication authority is upheld. Aggrieved by the said order, the appellant filed present appeal.

2. The learned counsel appearing on behalf of the appellant submitted that the import of used digital multifunction machines were subject matter in large number of cases including the case law referred by the Appellate Authority. Since the issue regarding confiscation of the goods is settled by the judgment of the Supreme Court in the case of Commissioner of Customs vs M/s Atul Automation Pvt Ltd dated 24.01.2019, goods are liable for confiscation. Regarding quantum of fine and penalty, learned counsel draws our attention to various decisions of this Tribunal in similar case and held that in the absence of any finding regarding the market value of the goods, in similar cases, the goods are being released subject to payment of redemption fine of 10% and penalty of 5% on enhanced assessable value. It is further submitted that, in view of the findings given by the Appellate Authority and this Tribunal in similar cases, the impugned order of remand made by the learned Commissioner (Appeals) is illegal and unsustainable. Further submitted that inspite of specific finding from various appellate forums, there was undue delay of more than 06 years in releasing the goods. Hence appellant also prays for issuing a direction for waiver of detention/demurrage charge.

3. The learned A.R. for the Revenue produced the copy of the Final Order No. 21308-21309/2019 dated 20 December, 2019 of this Tribunal in the matter of M/s S.R. Enterprises & M/s Digital Enterprise where the issue was considered by this Tribunal. Though the order of absolute confiscation was found unsustainable, the matter was remanded to Lower Authorities on the ground that the economic advantage of import even in the absence of license mandated for restricted goods must be neutralized with reference to the market price of the goods that are imported against such license. It is the negation of this windfall that is the intent of determining the quantum of redemption fine.

Considering the said finding, the learned A.R. submitted that the remand order is proper and sustainable.

4. In response to the submission on remanding the issue for ascertaining the market value and to determine the redemption fine, Learned counsel for the appellant submitted that in the ibid matter of M/s S.R. Enterprises (supra), issue was related to import of very same goods against Bill of Entry No. 4620026 dated 30.12.2017 and the present appeal is related to very same goods imported on August 2017. The learned counsel further submits that when this Tribunal remanded the matter for denovo adjudication directing adjudication authority to find out the market value of the goods and to quantify the redemption fine and penalty, aggrieved by the said order, the respondent filed appeal before the Hon’ble High Court of Karnataka and only on dismissal of the departmental appeal, Adjudication Authority considered the issue for denovo adjudication. Though this Tribunal had issued specific direction to find out the market value of the goods, the Adjudication Authority issue an order imposing redemption fine equivalent to the value of the goods on the ground that the market value of such goods is not readily available and considered the re-determined assessable value of the market price of such goods. The appeal filed before the Commissioner (Appeals) was also dismissed and importer was forced to file appeal before this Tribunal by filing Customs Appeal No. 20350 of 2021. This Tribunal vide Final Order No. 20762-20763/2021 dated 23.09.2021 considered the appeal on merits and following the decision of the Tribunal in similar cases, allowed the appellant to redeem the goods on payment of redemption fine of 10% on the enhanced value and penalty also reduced to 5% of the enhanced value. The learned counsel further submits that the issue attained finality only after more than 06 years and the importer had suffered huge losses due to undue delay in clearing the goods due to such remand order. Learned counsel further submits that in the absence of any finding regarding market value of the goods in the impugned order, the ratio of the judgment of the Hon’ble High Court of Kerala in the matter of Commissioner of Customs, Cochin Vs Office Devices - 2009 (240) E.L.T. 336 (Ker.) is squarely applicable in this case.

5. The learned counsel also submitted that on very same issue, in the matters of M/s Photofax Systems vs. CC, Bangalore vide Final Order No. 20728/2023 dt. 24.07.2023 and M/s City Office Equipment vs. CC, Bangalore vide Final Order No. 20729/2023 dt. 24.07.2023, this Tribunal partially allowed the appeal and reduced the fine and penalty to 10% and 5% enhanced assessable value.

6. We have gone through the facts and circumstances made by the appellant and the Revenue. The Original Authority had redetermined the value of the 244 units of used Digital Multifunction Printing and Copying Machine (MFDs) at value of Rs.42,49,780/-.

He held that goods were liable for absolute confiscation and imposed 100% penalty equivalent to the value of the goods on the imported goods. The Commissioner (Appeals) in the impugned order had held that the goods are not liable for absolute confiscation but are to be released on payment of redemption fine. He further upheld 100% penalty equivalent to the value of the imported goods. The appellant now is in appeal only to the extent of redemption fine and penalty since he has accepted the enhanced value as per the Chartered Engineer’s certificate.

7. It is seen from the records that there have been number of orders issued by this Tribunal and various High Courts accepting the fact that the impugned MFDs are not liable for absolute confiscation. Hence have taken a lenient view and released these goods on payment of redemption fine of 10% & penalty of 5%. From the Final Order No. 20844/2020 dated 15.12.2020 in the case of M/s Accord Digitech Vs C.C. Bangalore passed by this Tribunal, it is clearly evident that the used Digital Multifunction Printing and Copying Machine were released on payment of redemption fine of 10% and penalty of 5% of the enhanced value of the imported goods. This was also followed by this Bench in the case of M/s S.R. Enterprises Vs Commissioner of Customs, Bangalore vide Final Order No. 20762-20763/2021 dated 23.09.2021 wherein the redemption fine and penalty was 10% and 5% respectively. The ratio of the judgment of the Hon’ble High Court of Kerala in the matter of Commissioner of Customs, Cochin Vs Office Devices (Supra) is also squarely applicable in this case.

8. Keeping in view of the above decisions and considering the fact that the Department has also accepted the same in the case of M/s Accord Digitech Vs C.C. Bangalore (Supra), we are of the opinion that in the interest of justice since 06 years have already been lapsed, the present appeal is partially allowed by reducing the redemption fine and penalty by 10% and 5% respectively of the enhanced value.

9. Keeping in view the above decisions the present appeal is partially allowed by reducing the redemption fine to 10% of the enhanced value and penalty to 5% of the enhanced value. Appellant is allowed to redeem the goods for home consumption inabove terms.

(Order pronounced in the court on 09.08.2023)

(P. A. AUGUSTIAN)

MEMBER (JUDICIAL)

(R. BHAGYA DEVI)

MEMBER (TECHNICAL)

×