Full News

Hit with a GST Cancellation Order? Spot This Theme and Win Your Appeal

Hit with a GST Cancellation Order? Spot This Theme and Win Your Appeal

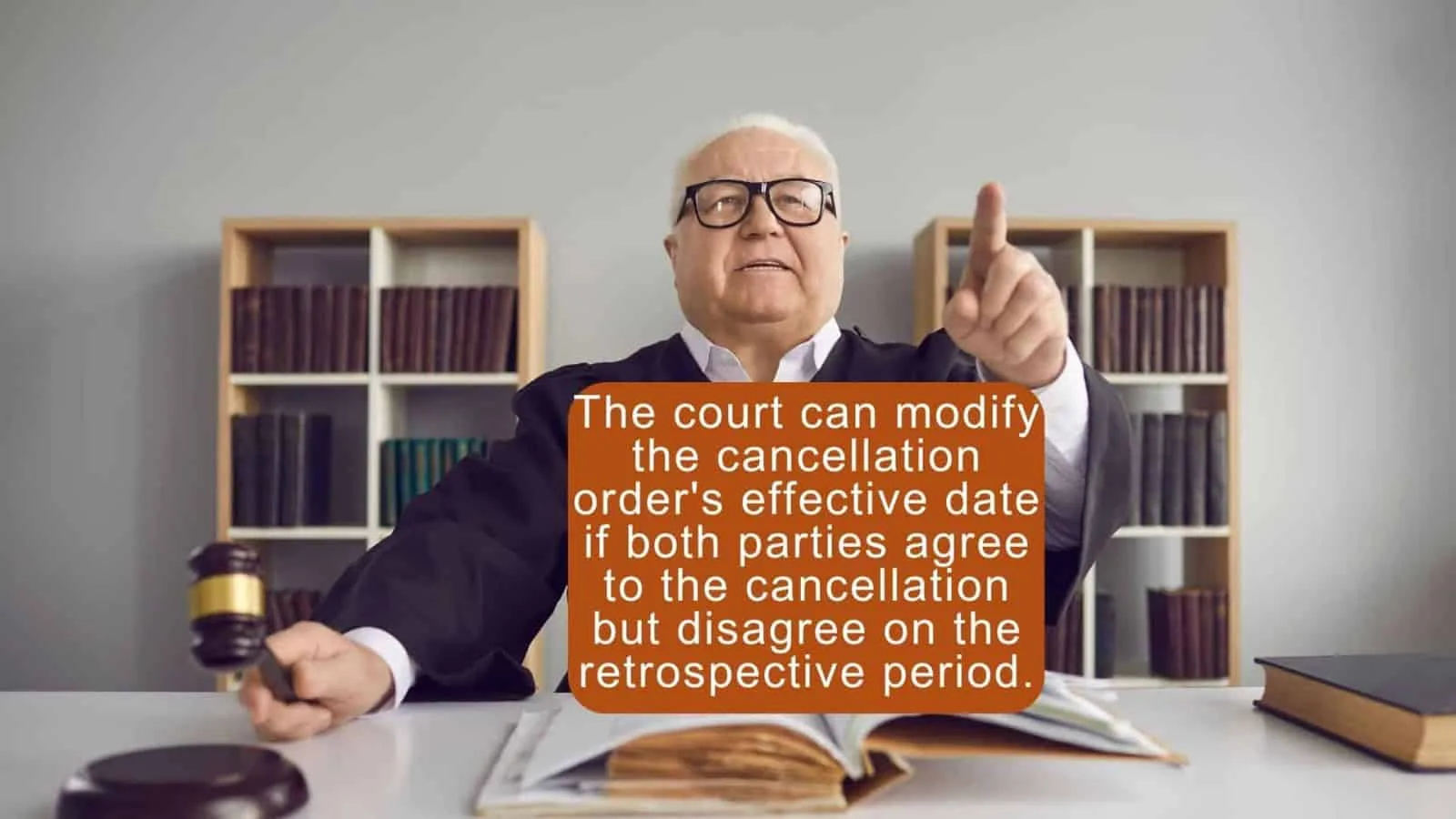

There's one common theme you'll notice in all these 19 court orders quashing GST cancellation orders and Show Cause Notice. You'll notice that all these cancellation orders cancelled GST retrospectively without mentioning retrospective cancellation in SCN. Most of the SCN stated weird cancellation reasons without corroborating them. Another point you'll notice that courts restored GST registration where parties desired to continue whereas if parties wanted to discontinue then courts modified the cancellation date.

A garment manufacturer's GST registration was restored after the court found the cancellation order lacked reasoning and details of alleged invoices issued without supply of goods or services, emphasizing the need for proper justification in such actions. (You'd right click here to read in full)

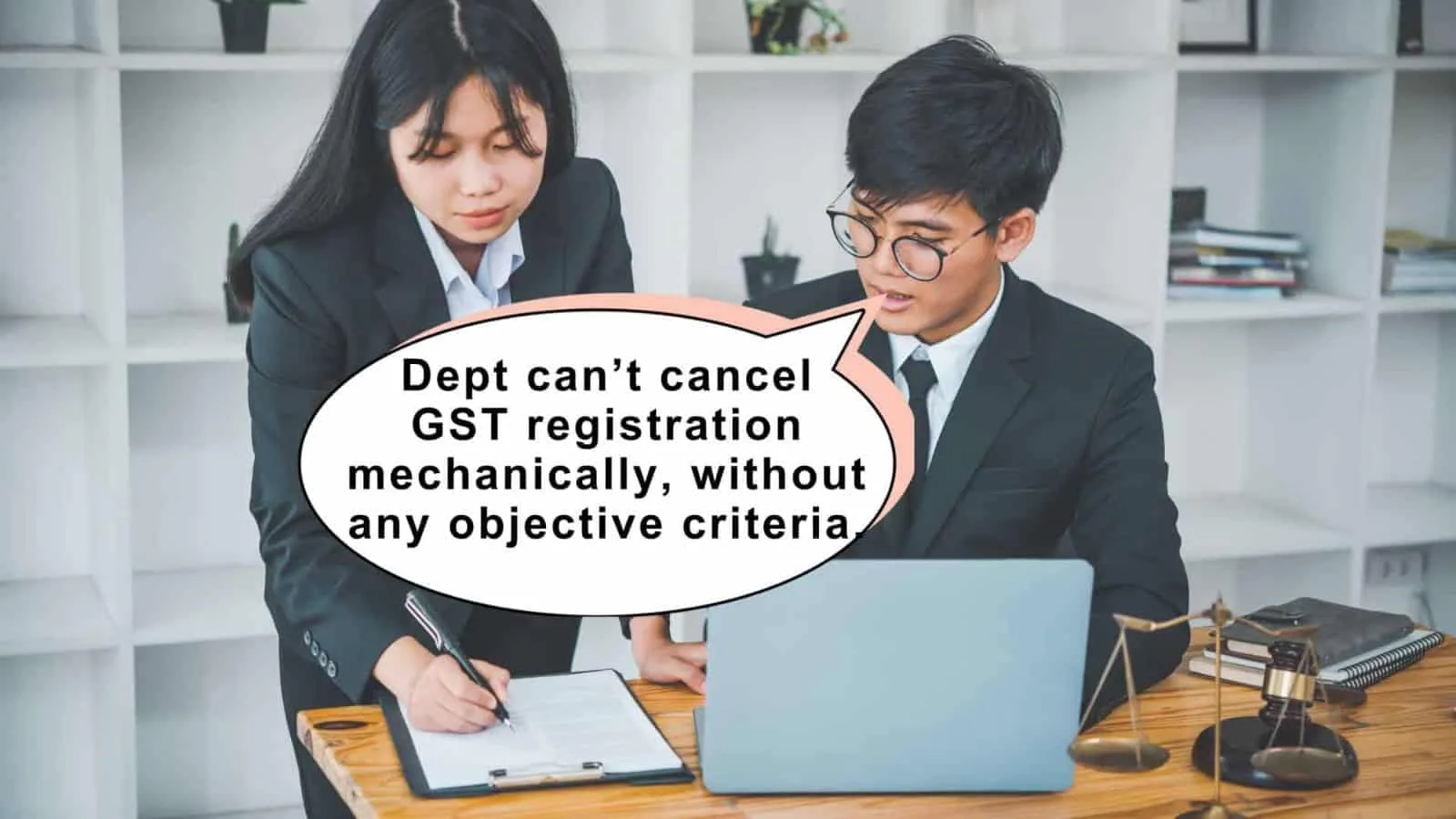

The court modified a retrospective cancellation order, making it effective from the date the taxpayer applied for cancellation, highlighting that the registration cannot be cancelled retrospectively in a mechanical manner without considering the consequences and objective criteria.(You'd right click here to read in full)

The court upheld the principles of natural justice by requiring tax authorities to provide clear reasons for canceling GST registrations and allowing taxpayers to object to retrospective cancellations, while also allowing authorities to recover outstanding taxes.(You'd right click here to read in full)

The court set aside the show cause notice and cancellation order due to lack of reasoning, failure to specify provisions violated, and denying the taxpayer an opportunity to object, upholding principles of natural justice and due process.(You'd right click here to read in full)

The court modified the cancellation order to align with the last period for which the taxpayer filed GST returns, as the show cause notice and order lacked adequate details and reasoning for the retrospective cancellation. (You'd right click here to read in full)

The court modified a cancellation order to operate from the date the taxpayer applied for cancellation, as the show cause notice did not mention the proposed retrospective cancellation, underscoring the need for transparency. (You'd right click here to read in full)

The court modified the cancellation order to take effect from the date of the show cause notice, as the order had contradictory statements, lacked clear reasons, and did not provide details for the retrospective cancellation. (You'd right click here to read in full)

The court modified the cancellation order to align with the date of the show cause notice, as mere non-filing of GST returns for some period is not proper justification for the retrospective cancellation. Further the order didn't consider the consequences, and the taxpayer was not given an opportunity to object.(You'd right click here to read in full)

The court modified the cancellation order to take effect from the date of the show cause notice, as the order lacked details and reasoning for the retrospective cancellation, and the taxpayer intended to close the business.(You'd right click here to read in full)

The court modified the cancellation order to align with the last date the taxpayer filed GST returns, as the show cause notice and order lacked reasoning for the retrospective cancellation, emphasizing the need for objective criteria.(You'd right click here to read in full)

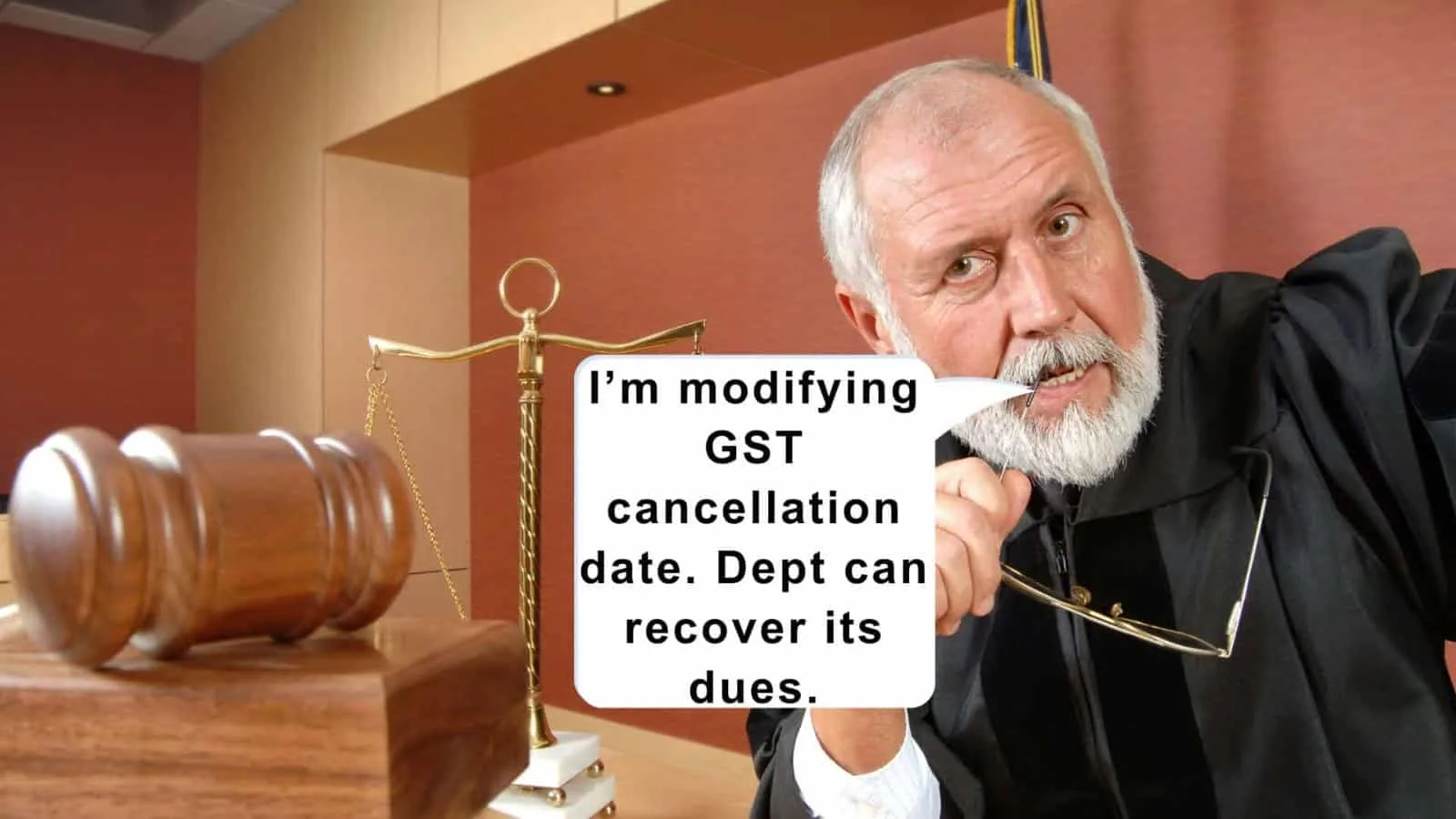

The court balanced the interests of both parties by modifying the cancellation date while allowing further proceedings for recovery of dues. (You'd right click here to read in full)

The court restored the petitioner's GST registration as the show cause notice and order lacked details and reasons for retrospective cancellation, which is required by law. The court ordered the petitioner to file all requisite returns and pay the tax, if any, within a period of 30 days. (You'd right click here to read in full)

The court modified the cancellation order to the limited extent by cancelling the GST registration from Show cause notice's issue date in view of the fact that Petitioner does not seek to carry on business or continue the registration. (You'd right click here to read in full)

The court restored the GST registration by quashing the retrospective cancellation order and show cause notice as neither provided cogent reasons for the retrospective action, nor allowed the taxpayer to object, further emphasizing the importance of proper justification and adherence to natural justice.(You'd right click here to read in full)

The court modified the cancellation order to operate from the date the taxpayer applied for cancellation, as the show cause notice did not mention the proposed retrospective cancellation, underscoring the need for transparency. (You'd right click here to read in full)

The court modified the cancellation order to align with the petitioner's stated business closure date, treating the registration as cancelled from that date onwards, as the show cause notice and order lacked details and reasons for retrospective cancellation.(You'd right click here to read in full)

The court restored petitioner's GST registration and set aside the order cancelling the petitioner's GST registration with retrospective effect, as SCN and order didn't clearly state the grounds and reasons for retrospective cancellation.(You'd right click here to read in full)

The court emphasized that tax authorities cannot cancel GST registration with retrospective effect without providing valid reasons and objective criteria, and that show cause notices must inform the taxpayer about the proposed retrospective cancellation to allow them to object.(You'd right click here to read in full).

The court modified the cancellation order, limiting the retrospective effect to the last date the taxpayer filed GST returns since both parties wanted the registration cancelled. Thus, striking a balance between the authorities' powers and the taxpayer's rights, while allowing for further action as per law. (You'd right click here to read in full)

×