90% deduction under Section 80HHC (of Income Tax Act, 1961) applies to net rece…

Full News

90% deduction under Section 80HHC (of Income Tax Act, 1961) applies to net receipts, not gross

90% deduction under Section 80HHC (of Income Tax Act, 1961) applies to net receipts, not gross

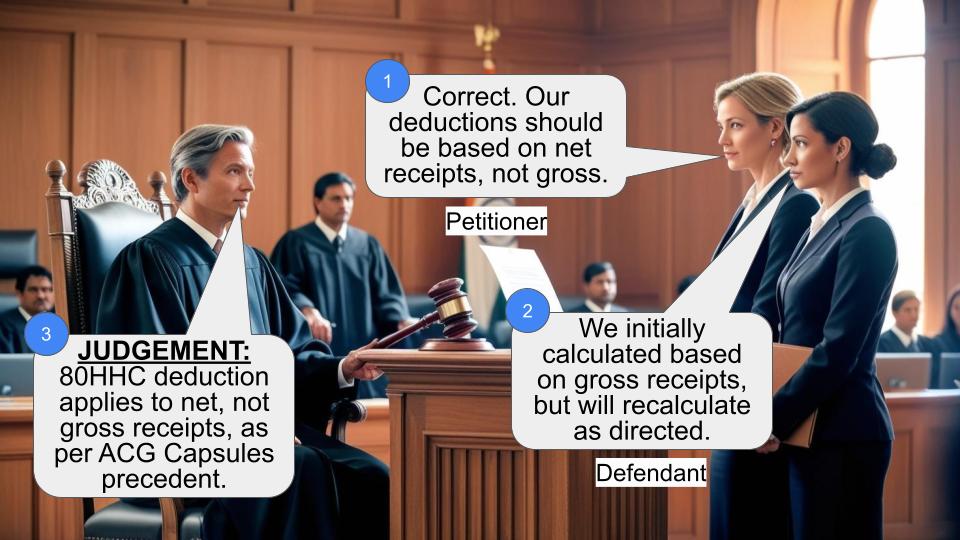

This case involves V.M. Salgaoncar & Brother Private Limited appealing against the Commissioner of Income Tax. The main dispute was about how to calculate deductions under Section 80HHC (of Income Tax Act, 1961). The Supreme Court ruled that deductions should be based on net receipts rather than gross receipts.

Get the full picture - access the original judgement of the court order here

Case Name:

V.M. Salgaoncar & Brother Private Limited vs. Commissioner of Income Tax (High Court of Bombay)

Tax Appeal No.21 of 2011

Key Takeaways:

1. Deductions under Section 80HHC (of Income Tax Act, 1961) should be based on net receipts, not gross receipts.

2. The Supreme Court's decision in ACG Associated Capsules (P) Ltd. vs. Commissioner of Income Tax was applied.

3. The court modified previous orders to align with this interpretation.

4. The revenue department must recalculate assessments based on net receipts.

Issue:

Should the 90% deduction under Clause (baa) of the Explanation to Section 80HHC (of Income Tax Act, 1961) be calculated based on gross receipts or net receipts?

Facts:

1. The case was initially admitted on 26.09.2011 with six substantial questions of law.

2. The appellant, V.M. Salgaoncar & Brother Private Limited, challenged the Tribunal's decision to uphold the Assessing Officer's action.

3. The Assessing Officer had deducted 90% of income from various sources (truck hire charges, barge hire charges, etc.) while computing profits under Section 80HHC (of Income Tax Act, 1961).

4. The dispute centered around whether these deductions should be based on gross or net receipts.

Arguments:

Appellant (V.M. Salgaoncar & Brother Private Limited):

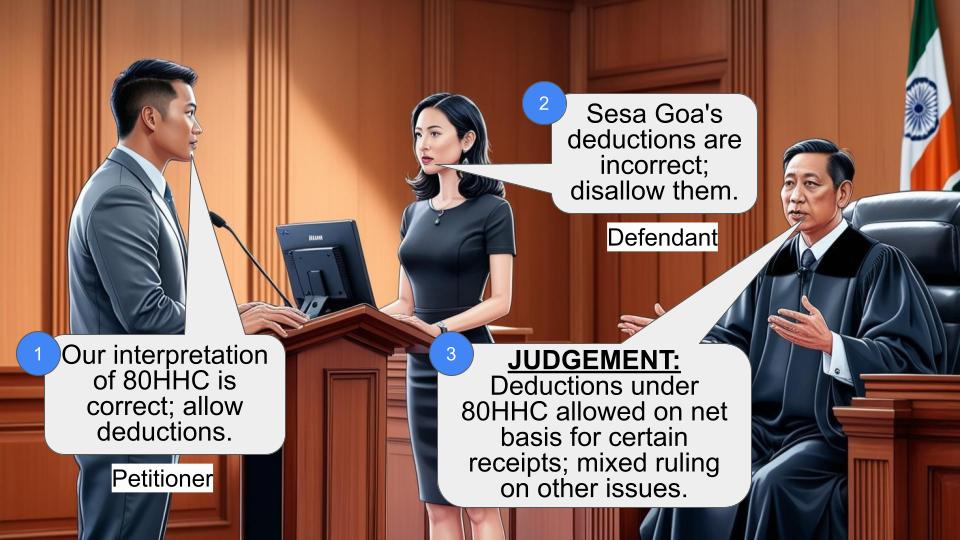

- Argued that deductions should be based on net receipts, not gross receipts.

- Cited the Supreme Court's decision in ACG Associated Capsules (P) Ltd. vs. Commissioner of Income Tax to support their position.

Respondent (Commissioner of Income Tax):

- Defended the impugned order based on the reasoning reflected in it.

- Initially supported the deduction based on gross receipts.

Key Legal Precedents:

1. ACG Associated Capsules (P) Ltd. vs. Commissioner of Income Tax, 2012 18 Taxman.com 137(SC): This Supreme Court decision held that deductions under Section 80HHC (of Income Tax Act, 1961) should be based on net receipts, not gross receipts.

2. CIT vs. Sesa Goa Ltd. Tax Appeal No.81 of 2006 (decided on 07.05.2015): This case took cognizance of the position established in the ACG Associated Capsules case.

3. The Commissioner of Income Tax vs. V. M. Salgaonkar & Brothers Ltd. & anr. in Income Tax Appeal Nos.5, 6 and 7 of 2002 (decided on 27.03.2012): This decision answered a related question in favor of the assessee and against the revenue.

Judgement:

1. The court held that deductions under Section 80HHC (of Income Tax Act, 1961) are permissible, but they should be made on net receipts, not gross receipts.

2. The court modified the impugned orders to align with this interpretation.

3. The revenue department was directed to recalculate the assessment based on net receipts and extend any necessary benefits to the appellant within a reasonable period.

4. The court also answered the question about adding losses from export of trading goods in favor of the assessee, based on a previous decision.

FAQs:

1. Q: What is the main difference between gross receipts and net receipts?

A: Gross receipts represent the total amount received, while net receipts are what remains after deducting allowable expenses.

2. Q: How does this judgment affect taxpayers claiming deductions under Section 80HHC (of Income Tax Act, 1961)?

A: Taxpayers can now claim deductions based on their net receipts, which could potentially result in lower taxable income compared to calculations based on gross receipts.

3. Q: Does this judgment apply retroactively?

A: The judgment doesn't explicitly state retroactive application, but it does require the revenue department to recalculate the assessment for the appellant. Other similar cases might be reviewed on a case-by-case basis.

4. Q: What should businesses do if they've been assessed based on gross receipts in the past?

A: They may want to consult with tax professionals to determine if they can seek a reassessment based on this judgment.

5. Q: Does this judgment apply to all types of income under Section 80HHC (of Income Tax Act, 1961)?

A: The judgment specifically mentions various types of income such as truck hire charges, barge hire charges, and ore processing receipts. It's best to consult a tax professional for specific cases.

1. Heard Mr. A. F. Diniz, learned Counsel for the appellant and Ms. Amira Razaq, learned Standing Counsel for the Department.

2. This appeal was admitted on 26.09.2011 on the following substantial questions of law :

i) Whether on the facts and in law, the Tribunal was right in upholding the exercise of jurisdiction by the Assessing Officer under Section 147 (of Income Tax Act, 1961) ?

ii) Whether on the facts and in law, the Tribunal was right in upholding the action of the Assessing officer of deducting 90% of the income from truck hire charges, barge hire charges, ore processing receipts, trans-shipper loader charges, machinery hire charges and launch hire charges while computing the "profits of the business" in accordance with Clause (baa) of the Explanation below Section 80HHC (of Income Tax Act, 1961) ?

iii) Whether on the facts and in law, the Tribunal was right in not following its earlier Order dated February 26, 2010 in the Appellant's own case for the earlier Assessment year i.e. 1997-1998, where the Tribunal had upheld the Appellant's claim that no part of the income from truck hire charges, barge hire charges, ore processing receipts, trans-shipper loader charges and machinery hire charges was to be reduced while computing the profits of the business for the purpose of deduction under Section 80HHC (of Income Tax Act, 1961) ?

iv) Whether the Tribunal was right in law in holding that Clause (baa) of the Explanation below Section 80HHC (of Income Tax Act, 1961), requires 90 % of the gross receipts instead of net receipts when the only controversy before it was the manner of computation of net receipts?

v) Whether the Tribunal was right in law in holding that Clause (baa) of the Explanation below Section 80HHC (of Income Tax Act, 1961), requires 90% of the gross receipts instead of net receipts, which resulted into enhancing the income of the Appellant ?

vi) Whether on the facts and in law, the Tribunal was right in not permitting adding losses from export of trading goods in respect of disclaimed turnover to the profit eligible for deduction under Section 80HHC (of Income Tax Act, 1961)?

3. Mr. Diniz, learned Counsel for the appellant, at the very outset states that he has instructions not to press the substantial question at (i) above. He also states that the question at (iii) above really does not arise in this matter and, therefore, he has instructions not to press the same as well. Accordingly, there is no necessity to advert the questions at (i) and (iii) above.

4. Mr. Diniz, learned Counsel submits that the substantial question of law at (ii), (iv) and (v) can be taken up for consideration together. He points out that the issues which arise from these questions are no longer res integra. He refers to the decision of the Hon'ble Apex Court in ACG Associated Capsules (P) Ltd. vs. Commissioner of Income Tax, 2012 18 Taxman.com 137(SC). He submits that in this case, the Hon'ble Apex Court has held that the deductions had to be made not on gross rent or gross basis but only on net rent, net interest or net basis. He submits that cognisance was taken on this position in CIT vs. Sesa Goa Ltd. Tax Appeal No.81 of 2006 decided on 07.05.2015. On this basis, Mr. Diniz submits that though this Court may have to hold that deduction as referred to in substantial question of law at (ii) above, may be permissible, the same will have to be made on net basis and not on gross basis.

5. Mr. Diniz, learned Counsel for the appellant, then submits that the substantial question of at law at (vi) above stands fully answered in favour of the appellant and against the revenue by the decision of this Court dated 27.03.2012 in the case of The Commissioner of Income Tax vs. V. M. Salgaonkar & Brothers Ltd. & anr. in Income Tax Appeal Nos.5, 6 and 7 of 2002.

6. Ms. Razaq, the learned Standing Counsel for the respondent defends the impugned order in the present case on the basis of the reasoning reflecting therein and submits that this appeal may be dismissed.

7. Having perused the record, we find that the substantial question of law at (ii), (iv) and (v) above relate to one and the same issue namely, whether the Tribunal in the present case, was right in upholding the action of the Assessing Officer deducting 90% of the income from truck hire charges, barge hire charges, ore processing receipts, trans-shipper loader charges, machinery hire charges and launch hire charges while computing the profits of the business in accordance with Clause (baa) of the Explanation below Section 80HHC (of Income Tax Act, 1961) (IT, Act). Further, if at all, the Tribunal was so justified, then whether the deductions ought to have been made on the basis of gross receipts and not net receipts.

8. In ACG Associated Capsules (P) Ltd. (supra), the Hon'ble Supreme Court, has clearly held that deductions of the nature as are referred to in the substantial question of law at (ii) above, are permissible, such deductions are required to be made not on the gross receipts but on the net receipts. This is clear from the observations in paragraph 12 which read as follows :

“12. If we now apply Explanation (baa) as interpreted by us in this judgment to the facts of the case before us, if the rent or interest is a receipt chargeable as profits and gains of business and chargeable to tax under Section 28 (of Income Tax Act, 1961), and if any quantum of the rent or interest of the assessee is allowable as an expense in accordance with Sections 30 to 44D of the Act and is not to be included in the profits of the business of the assessee as computed under the head “Profits and Gains of Business or Profession”, ninety per cent of such quantum of the receipt of rent or interest will not be deducted under clause (1) of Explanation (baa) to Section 80HHC (of Income Tax Act, 1961). In other words, ninety percent of not the gross rent or gross interest but only the net interest or net rent, which has been included in the profits of business of the assessee as computed under the head “Profits and Gains of Business or Profession”, is to be deducted under clause (1) of Explanation (baa) to Section 80HHC (of Income Tax Act, 1961) for determining the profits of the business.” (Emphasis supplied).

9. From the aforesaid, it is quite clear that the substantial questions of law at (ii), (iv) and (v) will have to be answered by holding that the revenue was quite right in making the deductions referred to in the substantial question of law at (ii). However, such deductions ought to have been made on the basis of net receipts and not gross receipts. The substantial questions of law at (ii), (iv) and (v) are answered accordingly. The revenue will therefore have to rework the assessment on such basis and extend the necessary benefits, if any, to the appellant within a reasonable period. The impugned orders are modified accordingly.

10. Insofar as the substantial question of law at (vi) is concerned, the same stands answered entirely in favour of the assessee and against the revenue in terms of our decision dated 27.03.2012 in the Income Tax Appeal Nos.5, 6 and 7 of 2002. Incidentally, all these appeals were in the case of the present assessee and the ITAT had in fact held in favour of the present assessee. The appeals instituted by the revenue were accordingly dismissed. The substantial question of law at (vi) is consequently answered in favour of the assessee-appellant and against the revenue-respondent. The impugned orders are modified accordingly.

11. The present appeal is disposed off in the aforesaid terms. There shall be no order as to costs.

C. V. BHADANG, J. M. S. SONAK, J.

×

Questions

90% deduction under Section 80HHC (of Income Tax Act, 1961) applies to net receipts, not gross

Write your CommentSimilar Posts

Generic

- Reportdata/5325.pdf