Cash credits dispute: Court upholds tax addition, no substantial question of la…

Full News

Cash credits dispute: Court upholds tax addition, no substantial question of law arises

Cash credits dispute: Court upholds tax addition, no substantial question of law arises

Where a taxpayer (the assessee) is challenging a decision made by the Income Tax Appellate Tribunal (ITAT). The ITAT had upheld an order by the Commissioner of Income Tax (CIT) to add Rs. 3.08 lakhs to the assessee's income as unexplained cash credits. The High Court dismissed the appeal, agreeing with the lower authorities that the assessee's explanation for the credits wasn't satisfactory.

Get the full picture - access the original judgement of the court order here

Case Name:

Mahavir Prasad Vs Income Tax Officer (High Court of Punjab & Haryana)

I.T.A. No. 70 of 2008

Date: 1st February 2008

Key Takeaways:

1. The court emphasized the importance of providing truthful and consistent explanations for cash credits.

2. Assessees can't change their stance about the source of funds after initial claims are proven false.

3. Tax authorities can reject explanations that are contradicted by the assessee's own evidence.

4. The case highlights the significance of Section 68 (of Income Tax Act, 1961) in dealing with unexplained cash credits.

Issue:

The main question here is: Was the ITAT correct in upholding the CIT's order to add Rs.3.08 lakhs to the assessee's income as unexplained cash credits, and does this decision raise any substantial question of law?

Facts:

1. The assessee filed an income tax return for the assessment year 1997-98.

2. Later, it was discovered that the assessee had deposited Rs.4,00,000 with a firm called M/s Om Parkash & Co.

3. The Assessing Officer (AO) initially added Rs.68,000 to the assessee's income.

4. The CIT reviewed the case and found the AO's order erroneous.

5. The assessee claimed the credits came from four individuals, providing confirmations and affidavits.

6. However, it was found that this claim was false, and the money actually came from two different people.

7. The CIT directed the AO to add Rs.3,08,000 to the assessee's income.

8. The ITAT upheld this decision, which the assessee then appealed in the High Court.

Arguments:

The assessee's side:

- Claimed the credits were from four specific individuals.

- Provided confirmations, affidavits, and income statements as evidence.

The tax department's side:

- Showed that the assessee's initial explanation was false.

- Argued that the credits actually came from two different individuals.

- Contended that the assessee's explanation was unsatisfactory and contradictory.

Key Legal Precedents:

While no specific case laws were cited, the judgment refers to Sections 68, 69, and 69-A of the Income Tax Act. These sections deal with unexplained cash credits, investments, and money. The court emphasized that these sections place the initial burden on the assessee to explain the source of credits or investments.

Judgement:

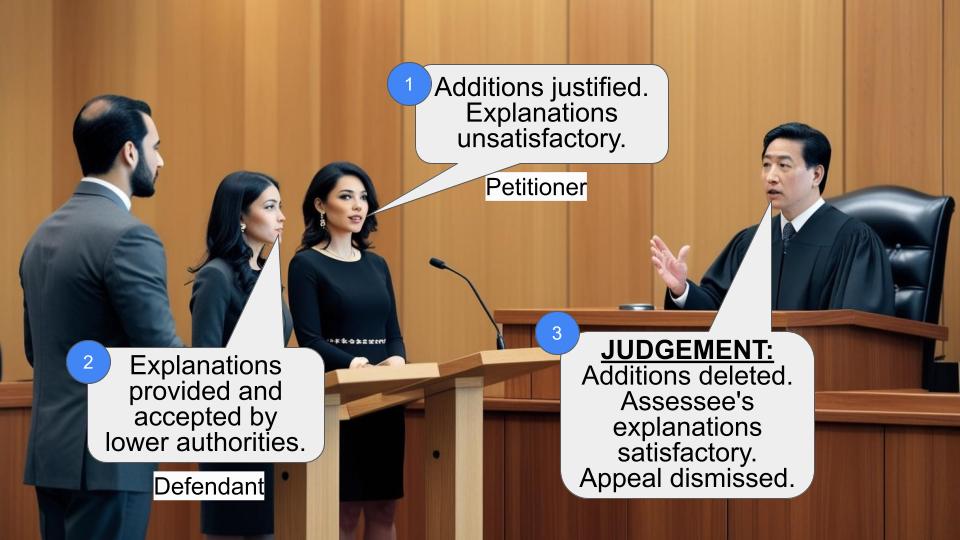

The High Court dismissed the appeal, agreeing with the CIT and ITAT. They found that:

1. The assessee's explanation was not just unsatisfactory but also false.

2. The AO shouldn't have accepted an explanation (about Surinder Sharma and Dinesh Kumar) that contradicted the assessee's own claims.

3. No substantial question of law arose from the ITAT's order.

FAQs:

Q1: What's the main lesson from this case?

A1: Always provide truthful and consistent explanations for cash credits to tax authorities.

Q2: Can tax authorities reject an explanation even if it seems plausible?

A2: Yes, if the explanation contradicts evidence or previous statements made by the assessee.

Q3: What's the significance of Section 68 (of Income Tax Act, 1961)?

A3: It places the burden on the assessee to explain the source of unexplained cash credits.

Q4: Can an assessee change their explanation about the source of funds?

A4: While they can, this case shows that changing explanations, especially when the first is proven false, can be viewed unfavorably.

Q5: What happens if no explanation is provided for cash credits?

A5: The amount can be charged to income tax without further inquiry.

The assessee has filed this Appeal under Section 260 (of Income Tax Act, 1961) A of the Income Tax Act, 1961 (hereinafter referred to as `the Act') against the order dated 26.10.2007, passed by the Income Tax Appellate Tribunal, Bench Delhi, Delhi (hereinafter referred to as `the ITAT'), in ITA No. 2597 (Del.)/ 2005 dated 26.10.2007, pertaining to the assessment of the assessee for the year 1997-98.

In this appeal, the assessee has raised the following substantial questions of law :-

(i) Whether the order is liable to be set aside as it enhances the income of the assessee?

(ii) Whether the order is liable to be set aside as it tends to subject the income to dual taxation?

(iii) Whether the error in the source of income amounts to concealment of income?

(iv) Whether an assessee can be made liable to pay tax on the money which is not the income of the assessee and where the assessee has merely acted as a Post Office?

(v) Whether the income can be presumed beyond the accepted statement of accounts?

(vi) Whether the order is liable to be set aside being in non- appreciation and misreading of the facts?

We have heard learned counsel for the appellant and have gone through the orders, passed by the Assessing Officer, Commissioner of Income Tax, Hisar, as well as the ITAT.

In the present case, the assessee filed his income tax return for the assessment year 1997-98 on 2.9.1997, which was processed under Section 143(1) (of Income Tax Act, 1961) vide order dated 27.2.1998 and a refund of Rs. 1,380/- was granted to him. Later on, on the basis of the information gathered from the file of M/s Om Parkash & Co., Charkhi Dadri, it was revealed that the assessee had deposited a sum of Rs. 4,00,000/- with the said firm by cheque drawn on Oriental Bank of Commerce, Bhiwani and source of such deposit was not verifiable from the return originally filed by the assessee. As such, due to failure on the part of the assessee to disclose fully and truly the facts necessary for the assessment, the proceedings under section 147 (of Income Tax Act, 1961) were initiated and a notice dated 30.3.2001 under Section 148 (of Income Tax Act, 1961) was issued to him. In response to the notice, the assessee filed return showing the same income of Rs. 46,100/-, which was shown in the return originally filed by him. The assessment was completed by the Assessing Officer vide his order dated 28.3.2003 by making an addition of Rs. 68,000/- being the amount deposited in cash in assessee's bank account and thus, the total income of the assessee was taken as Rs. 1,14,100/-. Later on, the Commissioner of Income Tax, Hisar, while taking the view that the order of the Assessing Officer was erroneous and detrimental to the interest of the revenue, issued a notice dated 28.2.2005 to the assessee under Section 263(1) (of Income Tax Act, 1961), requiring him to show cause as to why an appropriate order under Section 263 (of Income Tax Act, 1961) be not passed in respect of the aforesaid credit shown in the account of M/s Om Parkash & Co. The Commissioner, after hearing the assessee, came to the conclusion that before the Assessing Officer, the assessee had taken a categoric stand that four credits were received by him from four different persons, namely Sarvshri Vinod Kumar, Parveen Kumar, Banwari Lal and Sushil Kumar. In support thereof, he placed on record letters of confirmations, affidavits, their statements of income etc. As a matter of fact, it was found by the Assessing Officer that the said stand taken by the assessee was totally wrong, as the said credits did not flow from the aforesaid four persons. However, it was observed that the alleged credits in the hand of the assessee were received to the extent of Rs. 3.08 lakh from Sarvshri Surinder Sharma and Dinesh Kumar and the said money was advanced by the assessee to M/s Om Parkash & Co. along with an amount of Rs. 68,000/-, which was deposited by the assessee in cash. Therefore, on the basis of that reasoning, the Assessing Officer had made addition of Rs.68,000/-. The Commissioner of Income Tax, while considering all these facts, came to the conclusion that the Assessing Officer has wrongly accepted the explanation with regard to an amount of Rs. 3,08,000/- and therefore, vide his order dated 28.3.2005, directed the Assessing Officer to make an addition of Rs. 3,08,000/- being unexplained investment over and above the addition of Rs. 68,000/- already made as income from undisclosed sources and further directed to initiate penalty proceedings under Section 271(1)(c) (of Income Tax Act, 1961) for furnishing inaccurate particulars of income.

Against the aforesaid order of the Commissioner of Income Tax, Hisar, the assessee filed an appeal before the ITAT, which has been partly allowed to the extent of initiation of penalty proceedings under Section 271(1)(c) (of Income Tax Act, 1961), but the remaining part of the order of the Commissioner, Income Tax has been upheld, while observing as under :

“... The case of the assessee before the Assessing Officer was that four credits were received from four persons, namely, S/Shri Vinod Kumar, Parveen Kumar, Banwari Lal and Sushil Kumar. In support thereof, letters of confirmations, affidavits, their statements of income etc. were filed. Sections 68, 69, 69- A etc. place initial burden on the assessee to explain the source of credit, investment, money etc. There could be two situations, namely, that – (i) no explanation is furnished, or (ii) the explanation is furnished. In the first eventuality, the sum can be charged to income-tax without any further enquiry. In the second eventuality, the Assessing Officer has to examine whether the explanation furnished furnished by the assessee was satisfactory or not. There can be any number of possible explanations, but the Assessing Officer has to consider the explanation on record, more so when such explanation is backed by substantial evidence filed by the assessee. This examination has to be conducted on an objective basis and not on subjective basis. Nonetheless, it has to be examined by the Assessing Officer whether the explanation was satisfactory or not. Although the bank informed the Assessing Officer that the credits were received from S/Shri Surinder Sharma and Dinesh Kumar, the explanation of the assessee was not that the amounts were received from these persons. Thus, on the basis of facts available on record of the Assessing Officer, the explanation furnished by the assessee was not merely not satisfactory but was also false. Such an evidence can not be because of oversight or loss of memory because positive action was required on behalf of the assessee and the alleged creditors.

In such a situation, the credits having been received from Shri Surinder Sharma & Dinesh Kumar could not have been accepted to be the explanation of the assessee, explaining the deposits in the bank in a satisfactory manner. Therefore, the theory that the assessee was merely a conduit for transfer of money from Shri Surinder Sharma and Shri Dinesh Kumar could not have been accepted by the Assessing Officer on the facts on record. The fact is that the credits were received from certain persons for which there was no satisfactory explanation furnished by the assessee. Rather, the credits were stated to have been received from totally different persons and evidence, including affidavits was created to show that the credits were received from those persons.”

After hearing counsel for appellant and going through the impugned orders, we are of the opinion that on the basis of material evidence available on the record, the Commissioner of Income Tax has recorded a pure finding of fact and on the basis of said finding of fact, the Assessing Officer was directed to add a sum of Rs. 3.08 lakhs to the income of the assessee in respect of the credits, which according to the version of the assessee is received from four persons and the said stand was found to be false. Both the authorities have categorically found that in the facts and circumstances of the case, the Assessing Officer has wrongly accepted that the said amount was received by the Assessee from Surinder Sharma and Dinesh Kumar, because the said fact is totally contrary to the stand taken by the assessee and the evidence and material produced by the assessee himself to show that the said credit was received by him from those four persons.

Thus, we are of the view that in this appeal, no substantial question of law is arising from the order of the ITAT.

Dismissed.

( SATISH KUMAR MITTAL )

JUDGE

( RAKESH KUMAR GARG )

JUDGE

February 01, 2008

×

Questions

Cash credits dispute: Court upholds tax addition, no substantial question of law arises

Write your CommentSimilar Posts

Generic

- Reportdata/4912.pdf