Chartered Accountant Penalized for Misconduct in Fund Arrangement Case

Full News

Chartered Accountant Penalized for Misconduct in Fund Arrangement Case

Chartered Accountant Penalized for Misconduct in Fund Arrangement Case

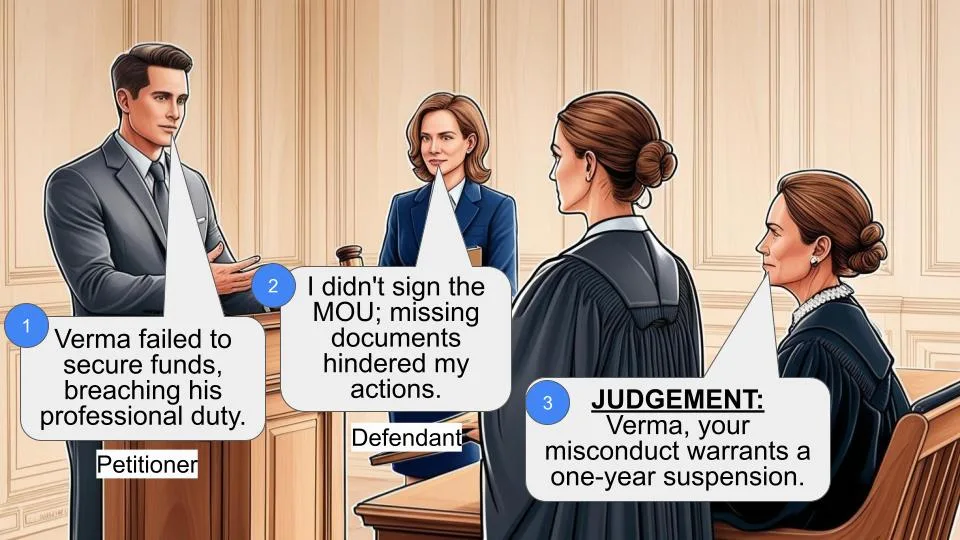

In the case involving the Council of the Institute of Chartered Accountants of India and Rakesh Verma, the court found Verma guilty of professional misconduct. The dispute centered around Verma’s failure to secure funds as promised in a Memorandum of Understanding (MOU) with M/s Sanvijay Rolling and Engineering Ltd. The court decided to suspend Verma from the Register of Members for one year due to his actions.

Get the full picture - access the original judgement of the court order here

Case Name

Council of the Institute of Chartered Accountants of India vs. Rakesh Verma (High Court of Delhi)

CHAT.A.REF.5/2011

Date: 8th August 2016

Key Takeaways

- Misconduct Identified: Rakesh Verma, a Chartered Accountant, was found guilty of misconduct for failing to fulfill his obligations under an MOU to secure funds.

- Disciplinary Action: The court upheld the recommendation to suspend Verma from the Register of Members for one year.

- Legal Principles: The case underscores the importance of due diligence and accountability in professional conduct, particularly for Chartered Accountants.

Issue

Did Rakesh Verma commit professional misconduct by failing to secure funds as per the MOU with M/s Sanvijay Rolling and Engineering Ltd.?

Facts

- Parties Involved: The case involved the Council of the Institute of Chartered Accountants of India and Rakesh Verma, a Chartered Accountant.

- Dispute Origin: Verma entered into an MOU with M/s Sanvijay Rolling and Engineering Ltd. to secure funds, taking an advance fee of `2.5 lacs.

- Failure to Act: Verma did not secure the funds and instead went on a foreign trip, failing to take necessary steps or produce documents to justify his actions.

Arguments

- Petitioner’s Argument: The Council argued that Verma failed to fulfill his professional duties and misled the company by not securing the promised funds.

- Respondent’s Defense: Verma claimed he did not sign the MOU and blamed the lack of necessary documents from Mr. Sanjay Aggarwal for his inability to secure funds.

Key Legal Precedents

- Chartered Accountants Act, 1949: Sections 21 and 22 were cited, which pertain to the misconduct of Chartered Accountants and the disciplinary actions that can be taken.

Judgement

The court found Rakesh Verma guilty of professional misconduct. It agreed with the Disciplinary Committee’s findings that Verma had cheated M/s Sanvijay Rolling and Engineering Ltd. The court ordered the suspension of Verma’s name from the Register of Members for one year, emphasizing the need for accountability and due diligence in professional conduct.

FAQs

Q: What was the main reason for Rakesh Verma’s suspension?

A: Verma was suspended for failing to secure funds as promised in an MOU and for not taking necessary steps to fulfill his professional obligations.

Q: What sections of the law were applied in this case?

A: The case referenced Sections 21 and 22 of the Chartered Accountants Act, 1949, which deal with professional misconduct and disciplinary actions.

Q: What does this case mean for Chartered Accountants?

A: It highlights the importance of adhering to professional standards and the consequences of failing to meet obligations, reinforcing the need for due diligence and accountability.

1. Ms. Isha Jha, Advocate who appears for respondent Rakesh Verma has shown to us a letter as per which the respondent No.1 Mr.Rakesh Verma has taken back the file from learned counsel; undertaking to appear in the matter himself.

2. It was the duty of Mr.Rakesh Verma to ensure that he appears himself or through a counsel today. We have accordingly heard learned counsel for the Institute of Chartered Accountants of India and have perused the record.

3. The respondent No.1 is a Member of the Institute of Chartered Accountants and is amenable to the disciplinary control as per the Chartered Accountants Act, 1949.

4. The report of the Committee would bring out that on November 17, 2002 a Memorandum of Understanding was arrived at, as per which the respondent offered his services as a Chartered Accountant to obtain funds and took `2.5 lacs as advance fee. The signatory to the Memorandum of Understanding was one Mr.Sanjay Aggarwal. The respondent did nothing except to proceed on a foreign trip. He secured no loan as per the MOU.

5. The complaint was made by M/s Sanvijay Rolling and Engineering Ltd., Nagpur. The defence of the respondent was that he had not signed any MOU with the company.

6. The disciplinary Committee of the Council has found that the cheque in sum of `2.5 lacs received by the respondent was issued by the company and thus the respondent was aware that the funds which he had to obtain were for the benefit of M/s Sanvijay Rolling and Engineering Ltd., Nagpur. An inference with which we agree.

7. That apart, the respondent does not claim to have taken any steps to arrange for any funds for Mr.Sanjay Aggarwal. If his case was that he had to arrange funds for Mr.Sanjay Aggarwal he had to establish having taken steps to arrange the funds.

8. The stand taken by the respondent that since Mr.Sanjay Aggarwal failed to provide him with the necessary documents he could not arrange for the funds, has been dealt with by the Disciplinary Committee of the Council. It has been held that the respondent produced no document to show that he ever asked Mr.Sanjay Aggarwal to provide him any document. The respondent admits having travelled to London and Oslo to secure the funds contemplated by MOU.

9. Now, the respondent is a Chartered Accountant. We fail to understand as to how come he proceeded to London and Norway if he had no documents with him concerning either Mr.Sanjay Aggarwal or M/s Sanvijay Rolling and Engineering Ltd., for obtaining funds.

10. As a Chartered Accountant he ought to know that a person would advance a credit to an individual or a company after satisfying itself with the credit worthiness of the individual or the company. All documents required for a due diligence ought to have been taken by the respondent.

11. It is a clear case where the respondent No.1 has cheated M/s Sanvijay Rolling and Engineering Ltd., Nagpur. Indeed, we concur that the respondent No.1 has committed misconduct as per Section 21 (of Income Tax Act, 1961) and 22 of the Chartered Accountants Act, 1949. The recommendation is to remove the name of the respondent from the Register of Members for a period of one year.

12. The conduct of the respondent justifies the proposed penalty.

13. We answer the Reference in the affirmative holding that the respondent is guilty of misconduct and we impose the penalty of suspension of the name of the respondent No.1 Rakesh Verma from the Register of Members for a period of one year.

14. No costs.

(PRADEEP NANDRAJOG)

JUDGE

(PRATIBHA RANI)

JUDGE

AUGUST 08, 2016

×

Questions

Chartered Accountant Penalized for Misconduct in Fund Arrangement Case

Write your CommentSimilar Posts

Generic

- Reportdata/HC-Delhi-5-2011.pdf