Court Allows Tax Deduction on Unit Trust Transactions, Rejects 'Colourable Devi…

Full News

Court Allows Tax Deduction on Unit Trust Transactions, Rejects 'Colourable Device' Claim

Court Allows Tax Deduction on Unit Trust Transactions, Rejects 'Colourable Device' Claim

This case involves Sundaram Finance Ltd. (the assessee) and the Deputy Commissioner of Income Tax. The dispute centered around the purchase and sale of Unit Trust of India (UTI) units and the resulting tax implications for the assessment year 1992-93. The High Court ruled in favor of the assessee, allowing the claimed tax deduction and rejecting the Revenue's argument that the transactions were a colourable device to avoid tax.

Get the full picture - access the original judgement of the court order here

Case Name:

Sundaram Finance Ltd. Vs Deputy Commissioner of Income Tax (High Court of Madras)

Tax Case (Appeal) No.1211 of 2005

Date: 20th June 2012

Key Takeaways:

1. Section 94 (of Income Tax Act, 1961), which deals with securities transactions, was not applicable to UTI units before April 1, 2002.

2. Legitimate tax planning within the law is not frowned upon by the courts.

3. The court emphasized that taking advantage of beneficial provisions in tax law doesn't automatically make a transaction colourable.

Issue:

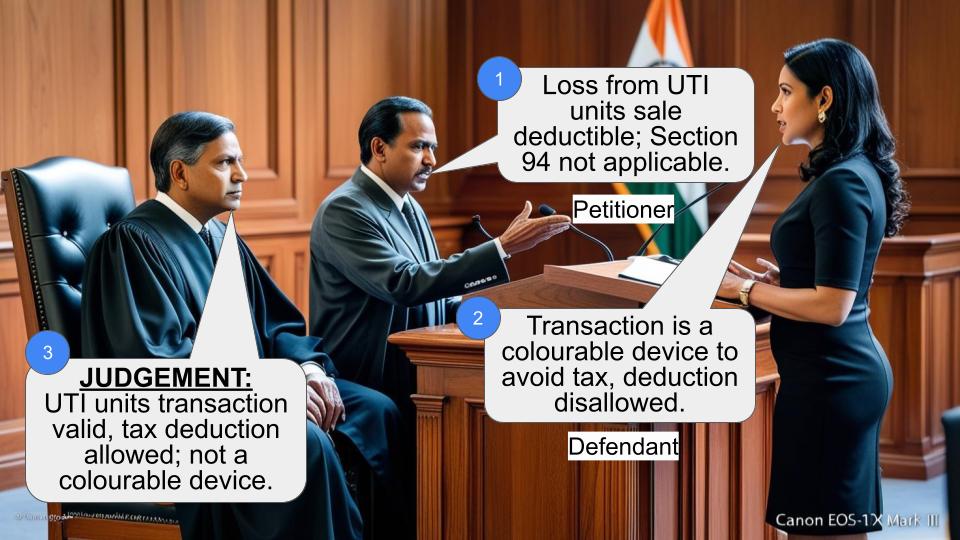

Was the Tribunal correct in holding that the loss arising from the purchase and sale of UTI units is not allowable as the transaction is a colourable device to avoid tax, despite the actual purchase and sale taking place and the appellant incurring a real loss?

Facts:

1. Sundaram Finance Ltd. purchased 85 lakh UTI units from Bank of America on May 31, 1991, for Rs.12,75,00,000.

2. The next day, June 1, 1991, they sold the same units back to Bank of America for Rs. 11,13,79,750.

3. This resulted in a loss of Rs. 1,60,65,000 for the assessee.

4. The assessee received dividends of Rs. 1,65,75,000 on these units.

5. The assessee sought to set off the loss against capital gains and carry forward the remaining loss.

6. The Assessing Officer rejected this claim, citing Section 94 (of Income Tax Act, 1961).

Arguments:

Assessee's Arguments:

1. The transaction was genuine and resulted in an actual loss.

2. Section 94 (of Income Tax Act, 1961) was not applicable to UTI units at the time of the transaction.

3. The assessee was entitled to the benefit of deduction under Section 80M (of Income Tax Act, 1961).

Revenue's Arguments:

1. The transaction was a colourable device to avoid tax.

2. The quick turnaround (purchase and sale within a day) indicated tax avoidance.

3. The units were already in the assessee's name before the purchase, suggesting collusion with Bank of America.

Key Legal Precedents:

1. Commissioner of Income Tax Vs. Walfort Share and Stock Brokers P.Ltd. (2010) 326 ITR 1 (SC): This case clarified that the inclusion of units as securities under Section 94 (of Income Tax Act, 1961) came into effect only from April 1, 2002.

2. McDowell & Co. Ltd. v. CTO (1985) 154 ITR 148 (SC): This case was cited by the Tribunal but later clarified by the High Court.

3. Union of India v. Azadi Bachao Andolan (2003) 263 ITR 706: This case held that tax planning within the law is permissible.

Judgement:

The High Court ruled in favor of the assessee, setting aside the Tribunal's order. Key points of the judgment include:

1. Section 94 (of Income Tax Act, 1961) was not applicable to UTI units for the assessment year in question (1992-93).

2. The transaction was not a colourable device merely because it resulted in a tax benefit.

3. The absence of registration of units in the actual holder's name does not invalidate the transaction.

4. The assessee was entitled to the benefit of deduction under Section 80M (of Income Tax Act, 1961).

FAQs:

1. Q: Why was Section 94 (of Income Tax Act, 1961) not applicable in this case?

A: Section 94 (of Income Tax Act, 1961) only became applicable to UTI units from April 1, 2002, while this case pertained to the assessment year 1992-93.

2. Q: What is a 'colourable device' in tax law?

A: A colourable device refers to a transaction or arrangement designed primarily to avoid tax, often by disguising its true nature.

3. Q: Does this judgment mean all quick buy-and-sell transactions are permissible for tax benefits?

A: Not necessarily. The court emphasized that legitimate tax planning within the law is acceptable, but each case would be judged on its own merits.

4. Q: What was the significance of the units remaining registered in the assessee's name?

A: While the Revenue pointed this out as suspicious, the court held that this alone doesn't make the transaction invalid or colourable.

5. Q: How does this judgment impact the interpretation of Section 80M (of Income Tax Act, 1961) deductions?

A: The judgment reinforces that taxpayers are entitled to take advantage of beneficial provisions like Section 80M (of Income Tax Act, 1961), as long as the transactions are genuine.

1. The assessee is on appeal as against the order of the Tribunal relating to the assessment year 1992-93, raising the following substantial questions of law:-

1. Whether on the facts and in the circumstances of the case, the Tribunal was right in holding that loss arising from purchase and sale of units is not allowable as the transaction is a colourable device to avoid tax despite the fact that the actual purchase and sale has taken place and the appellant has actually incurred the loss ?

2. Whether on the facts and in the circumstances of the case, the Tribunal was right in restoring the order of the Assessing Officer, without appreciating the fact that the assessing officer has ignored the entire transaction by invoking the provisions of section 94 (of Income Tax Act, 1961) which is not applicable to the facts of this case ?"

2. The assessee herein is a non-banking finance company. In respect of the assessment year 1992-93, while completing the assessment, the assessing officer noted that the assessee had purchased 85 lakhs units of the Unit Trust of India from Bank of America on 31.5.1991 for a sum of Rs. 12,75,00,000. On the very next day i.e. 1.6.1991 the assessee sold back the very same units to the same Bank of America for a sum of Rs. 11,13,79,750/-. In that process. the assessee had incurred a loss of Rs. 1,60,65,000/- which included brokerage. It is a matter of record that at the time of purchase of the units, the amount paid by assessee did not include brokerage and commission. It is seen from the facts that the assessee received the dividends in respect of the units held by it amounting to Rs. 1,65,75,000/- which was offered for tax along with other dividends under the head other sources. However, the assessee wanted to set off the loss of Rs.1,60,65,000/- against the income under the head capital gains to the tune of Rs.51,50,698/-. The assessee thereafter sought the balance loss of Rs.1,09,14,302/- to be carried forward as short term capital loss and to be set off against capital gains of later years. The assessing authority pointed out that Unit Trust of India had a record date for those units on 31.5.1991 and for the whole month of June 1991 no transaction of sale or purchase would be recorded and the books stood remained closed. Thus the units transferred upto 31.5.1991 would be entitled to dividend for the year 1990-91.

3. In the background of these facts, the assessing officer noted that the purchase price of the units upto 31.5.1991 would be high. However from 1.6.1991 onwards the price would be low since it is without dividend. The assessing authority pointed out that on enquiry, Bank of America confirmed that the units sold by them on 31.5.1991 were already in the name of the assessee and the Bank had purchased the units from the assessee earlier in two lots on 2.7.1990 and 24.7.1990. The transaction that went through 1990, however, remained in the name of the existing holder, namely, the assessee herein and on the purchase made by the assessee on 31.5.1991 the dividends were released in the name of the assessee only. Subsequently, there was no transfer of the units to the name of the assessee once again after its repurchase on 31.5.1991. The Assessing Authority pointed out that in this regard the Unit Trust of India was addressed and it was confirmed by the Unit Trust of India that the transfers were registered in the name of the assessee from 31.5.1990 till 14.5.1994 and that the assessee received dividends till 1994.

4. In the background of the above said facts, the Assessing Officer issued a proposal to the assessee to show cause as to why the provision of Sections 73 or Section 94 (of Income Tax Act, 1961) should not be applied to the assessee's case. Referring to Explanation under Section 94 (of Income Tax Act, 1961) that securities includes stocks and shares and also interest includes dividend the Assessing Officer held that Section 94(4) (of Income Tax Act, 1961) would be applicable to the facts of the case and thus ignoring the loss of Rs. 1,60,65,000/- on account of the difference between the purchase and sale price as well as the dividend of Rs.1,65,75,000/- the Assessing Officer proceeded to compute the assessee's taxable income. In other words, the assessee was not given set off in respect of capital loss against the capital gain and to carry forward the balance amount as short terms capital loss to be set off against capital gains of later years. The Assessing Officer further held that Bank of America is a foreign company and not a domestic company and the benefit of Section 80 (of Income Tax Act, 1961) M was not available to it and it had paid the tax on the profit earned on the difference between the sale and repurchase price. Quoting Section 94(1) (of Income Tax Act, 1961) which provides the income arising from the transaction of the sale of the securities as income of the owner, the Assessing Authority held that there was an avoidance of tax by the owner Bank of America . Aggrieved by the said view, resulting from the application of Section 94(4) (of Income Tax Act, 1961) to the transaction in question, the assessee went on appeal before the Commissioner of Income Tax (Appeals).

5. A perusal of the order of the Commissioner of Income Tax (Appeals) particularly paragraph 34 shows the discussion on the scope of Section 94 (of Income Tax Act, 1961). Taking the view that the units of the Unit Trust of India could not be considered as having the attributes of the shares, the Commissioner of Income Tax (Appeals) held that Section 94 (of Income Tax Act, 1961) has no relevance at all to the facts of the case. The Commissioner held that the Assessing Officer had ignored the transaction of purchase and sale of units in its entirety by applying the provisions of Section 94(4) (of Income Tax Act, 1961) mainly on the ground that (1) avoidance of tax was seen in the hands of Bank of America ; (2) the units were purchased and sold within a short period of one day ; (3) units were in the name of the assessee even before the purchase date; (4) investment in securities was found to be an organised activity at the hands of the assesseee and (5) similar transactions were done in the preceding year as well as subsequent year thereby the provision of Section 94(3) (of Income Tax Act, 1961) has not been satisfied.

6. The Commissioner of Income Tax (Appeals) held that considering the intention behind the enactment of the provision, a finding as regards the applicability of Section 94(1) (of Income Tax Act, 1961) in the case of Bank of America was absolutely a necessary condition before invoking Section 94(4) (of Income Tax Act, 1961). As regards the view of the Assessing Officer that the transaction was a colourable one, the Commissioner of Income Tax(Appeals) held that in his view the transaction of this nature was neither unreal nor prohibited by the statute. Thus, the Commissioner of Income Tax (Appeals) agreeing with the assessee's contention held that the reliance placed on Section 94 (of Income Tax Act, 1961) was misplaced and the transactions were not colourable one. Aggrieved by the said order, the Revenue went on appeal before the Tribunal.

7. The Tribunal accepted the Revenue's case on different grounds, namely the act of the assessee in purchasing the unit on 31.5.1991 and selling them on 1.6.1991 clearly showed that for the purpose of getting deduction under Section 80M (of Income Tax Act, 1961) alone the transaction was entered into. The Tribunal further pointed out as far as the transfer of units was concerned, the units in fact after the transactions were given physical possession by the assessee to Bank of America and again on its repurchase and resale , there had been in fact physical possession.

8. As far as relevance of Section 94 (of Income Tax Act, 1961) is concerned, the Tribunal had not in any manner spelt out on this aspect, however, it confined its contention only to the issue of colourable transaction. The Tribunal held that the transactions were entered into for the purpose of avoiding tax after getting the benefit of Section 80M (of Income Tax Act, 1961) deduction. Hence transaction not being real transaction the decision of the Apex Court in the case of Mc Dowell & Co., reported in 154 ITR 148 would clearly be applicable to the assessee's case .

9. The Tribunal further pointed out that the units were already in the name of the assessee , even though the real owner was Bank of America. After purchase from the assessee, Bank of America kept the units untransferred to its name. Since the transaction was only for the purpose of getting deduction under Section 80M (of Income Tax Act, 1961), the Bank of America and the assesseee colluded together and made the colourable device to avoid tax. Thus, the Tribunal by applying the decision reported in the case of Mc Dowell & Co., reported in 154 ITR 148 allowed the Revenue's appeal. Aggrieved by the said order the assessee is before us.

10. Learned counsel appearing for the assessee pointed out that admittedly the units of the Unit Trust of India was not included within the definition of securities till the amendment came to sub-section (7) by introduction of Finance Act 2001 with effect from 1.4.2002. In the circumstances, the relevance of Section 94 (of Income Tax Act, 1961) relating to the transaction dealing in securities has to be confined to securities only other than units. He further pointed out that the said provision was also considered by the Apex Court in the decision reported in (2010) 326 ITR 1 (SC) (Commissioner of Income Tax Vs. Walfort Share and Stock Brokers P.Ltd.,) and in respect of a loss arising on account of purchase of securities and sale thereon within three months the scope of Section 94 (of Income Tax Act, 1961) was considered by the Apex Court and in paragraph 20 of the judgment the purpose of introduction of Section 94(7) (of Income Tax Act, 1961) with effect from 1.4.2002 and Section 14A (of Income Tax Act, 1961) inserted with effect from 1.4.1962 was considered by the Apex Court. In the circumstances, when the provision itself came into existence from 1.4.2002, the loss from the transaction relating to the purchase and sale of units cannot be disallowed in the present case it being related to the assessment year 1992-93. Thus, the Revenue committed serious error in placing reliance on Section 94 (of Income Tax Act, 1961). He further pointed out that the theory of tax evasion as propounded by the Assessing Officer is only on the basis of his understanding of Section 94 (of Income Tax Act, 1961) and not on any account. As far as the receipt of dividend on the purchase of units is concerned the assessee pointed out that the same was offered under Section 80M (of Income Tax Act, 1961) and the sale consideration included this amount also which was offered by the Bank of America as income arising out of purchase of units.

11. As regards the non-registration of the units in the respective owners' name in the books of Unit Trust of India, learned counsel for the assessee pointed out that being movable property on the transactions taking place, the units were physically handed over to the purchaser, a fact which has not been disputed by the Revenue too. In the circumstances, when the transaction that had taken place between the parties had not been in any manner questioned, the view of the Tribunal on the claim made by the assessee for deduction under Section 80M (of Income Tax Act, 1961) could not be any manner held as legally correct. The decision of the Apex Court in the case of Mc Dowell & Co., (154 ITR 148) has no relevance to the facts of the case. On going through the records, rightly the Commissioner of Income Tax (Appeals) held that Section 94(4) (of Income Tax Act, 1961) has no relevance to the case of the assessee. Consequently, learned counsel prayed for setting aside the order of the Tribunal.

12. Learned Standing Counsel appearing for the Revenue supported the order of the Tribunal on the reasonings of the Assessing Officer on the applicability of Section 94 (of Income Tax Act, 1961).

13. Heard the learned counsel appearing for the appellant and the learned Standing Counsel appearing for the Revenue and perused the materials available on record.

14. As seen from the preceding paragraphs, it is a matter of record that the assessee purchased the units on 31.5.1991, where the price paid by the assessee included the dividend. As noted in the order of the Assessing Authority the purchase price of the units upto 31.5.1991 is inclusive of dividends entitling the purchaser to the dividends. It is no doubt true that immediately on the next day the assessee sold the units on 1.6.1991 at quoted price, which evidently was not inclusive of dividends. Thus, the difference in the sales price led to the assessee reporting a loss.

15. As far as the absence of entry in the Register of Unit Trust of India is concerned, the assesee never pleaded ignorance or lack of knowledge as to absence of entries in the respective holders name at the relevant point of time. The assessee admits that the Bank of America purchased the units from the assessee earlier in two lots on 2.7.1990 and 24.7.1990 and the transferee viz., Bank of America did nothing to transfer the units to its name. Thus, the units continued to stand in the name of the assessee, even after the transfer in favour of Bank of America and as on 31.5.1991 when the purchase was made by the assessee from Bank of America, the original position before 2.7.1990 remained unaltered in the sense the units continued to be shown in the name of the assessee. The Assessing Authority pointed out that till 14.5.1994 as per the communication from the Unit Trust of India, the units were registered in the name of the assessee alone. These facts were never disputed by the assessee. However, the assessing authority had not quoted this as a circumstance vital to ignore the transactions as colourable transaction. The Assessing Authority did not quote this as a base to apply the decision in the case of Mc Dowell & Co., reported in (154 ITR 148). On the other hand, a reading of the assessment order shows that principally the reasoning of the Assessing Officer rested on Section 94(4) (of Income Tax Act, 1961). As far as the reliance of Section 94 (of Income Tax Act, 1961) is concerned, we do not think that such a reasoning would be justifiable one considering the fact that as held by the Apex Court in the decision reported in (2010) 326 ITR 1 (SC) (Commissioner of Income Tax Vs. Walfort Share and Stock Brokers P.Ltd.,), the inclusion of units as a security for the purpose of applying Section 94 (of Income Tax Act, 1961) comes only with effect from 1.4.2002; thus the provisions under Section 94 (of Income Tax Act, 1961) itself is not applicable to the assessment under consideration. Consequently, the Assessing Authority was not justified in rejecting the transaction as not genuine.

16. As far as the Commissioner's order is concerned, we are in entire agreement with the view expressed by the Commissioner of Income Tax (Appeals), particularly in paragraph 34. When the Explanation to Section 94 (of Income Tax Act, 1961), as it stood at the material time relevant to this case, defined interest to include dividend, the term "securities" to include stocks and shares alone and not units of Unit Trust of India, by necessary implication the units of Unit Trust of India stood excluded from the definition of securities for the limited purpose of section 94 (of Income Tax Act, 1961), which is in line of the reasoning as spelt out by the decision reported reported in (2010) 326 ITR 1 (SC) (Commissioner of Income Tax Vs. Walfort Share and Stock Brokers P.Ltd.,). In the circumstances, we have no hesitation in holding that the assessment made by the Assessing Officer by applying Section 94(4) (of Income Tax Act, 1961) is erroneous in respect of the transaction in question.

17. As far as the Tribunal's reasoning is concerned, it is no doubt true that by purchase, the assessee was entitled to have the benefit of deduction under Section 80M (of Income Tax Act, 1961) and by this we do not think that there is no justifiable ground to hold that the transaction of sale on the next date would make the transaction of purchase and resale a colourable one. The assessee is entitled to have the benefit of deduction under the provisions of the Income Tax Act on any income earning transaction. In taking advantage of such provision, we do not find that the assessee could be charged with the allegation that it has indulged in any colourable transaction. The Apex Court pointed out in the decision reported in (2010) 326 ITR 1 (SC) (Commissioner of Income Tax Vs. Walfort Share and Stock Brokers P.Ltd.,) at paragraph 20 that when the assessee had made use of the beneficial provision available under the Act , as in the case of the present assessee as recognised under Section 10(33) (of Income Tax Act, 1961) such conduct could not be called as abuse of law. The Apex Court observed as follows:-

Even assuming that the transaction was pre-planned there is nothing to impeach the genuineness of the transaction. With regard to the ruling in McDowell and Co., Ltd., V. CTO (1985) 154 ITR 148 (SC), it may be stated that in the later decision of this court in Union of India Vs. Azadi Bachao Andolan (2003) 263 ITR 706 it has been held that a citizen is free to carry on its business within the four corners of the law. That, mere tax planning without any motive to evade taxes through colourable devices is not frowned upon even by the judgment of this court in Mc Dowell and Co., Ltd.,'s case (supra)." Applying the said decision to the facts of the case herein, we have no hesitation in rejecting the reasoning of the Tribunal .

18. It is a matter of record that the Revenue does not dispute the fact that there had been purchase by the Bank of America and later on sale by Bank of America in favour of the assessee and again a resale by the assessee in favour Bank of America. The Revenue does not dispute that the transactions in fact had taken place between the assessee and the Bank of America. The only objection raised by the Revenue is that there was no registration of the units in the actual holder's name. If really the Revenue had questioned the transaction as not legal, and not based on the amendment to Section 94 (of Income Tax Act, 1961), which came into existence only with effect from 1.4.2002, then Section 94 (of Income Tax Act, 1961) would not have come into play in considering the merits of the claim. Thus, on principle, when the Revenue had accepted the transfer, the sole ground on which the transaction was held to be a colourable one could not be sustained. In the circumstances, we have no hesitation in setting aside the order of the Tribunal by allowing the tax case appeal. Accordingly, the tax case appeal is allowed. No costs.

(C.V.,J) (K.R.C.B,.J)

20.06.2012

Index:Yes/No

Internet:Yes/No

To

1. The Income Tax Appellate Tribunal 'C' Bench, Madras

2. The Commissioner of Income -Tax (Appeals-), VII Madras.

3. The Deputy Commissioner of Income Tax, Special Range II Madras 34

CHITRA VENKATARAMAN,J.

and

K.RAVICHANDRABAABU,J.

Dated : 20.06.2012

×

Similar Ripples

Questions

Court Allows Tax Deduction on Unit Trust Transactions, Rejects 'Colourable Device' Claim

Write your CommentSimilar Posts

Generic

- Reportdata/5758.pdf