Court Allows Tax Settlement Applications for Undisclosed Foreign Income Filed B…

Full News

Court Allows Tax Settlement Applications for Undisclosed Foreign Income Filed Before Black Money Act

Court Allows Tax Settlement Applications for Undisclosed Foreign Income Filed Before Black Money Act

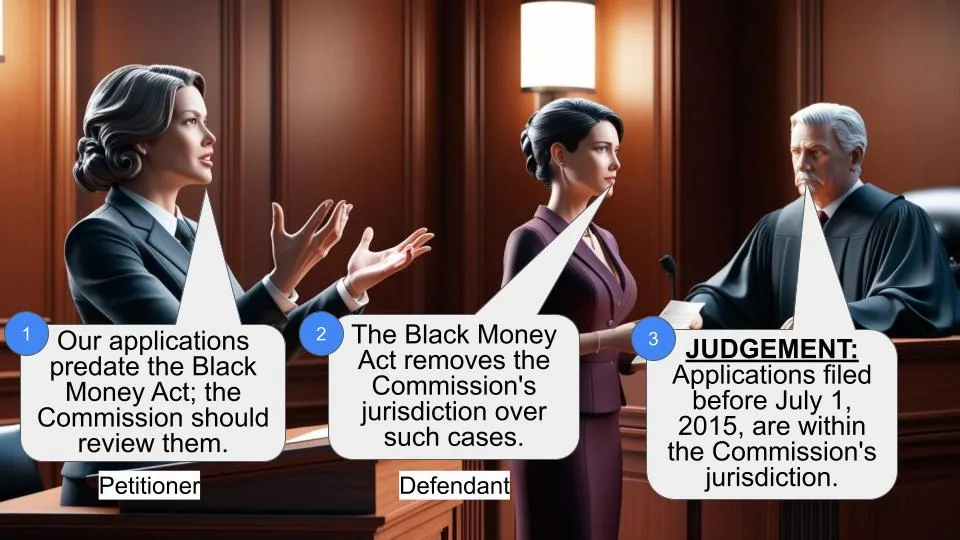

This case involves petitioners who filed applications before the Income Tax Settlement Commission for assessment years 2005-2006 to 2014-2015. The Commission initially rejected these applications, citing lack of jurisdiction due to the new Black Money Act. However, the High Court overturned this decision, allowing the petitioners to file their applications with the Commission.

Get the full picture - access the original judgement of the court order here

Case Name

Arun Mammen Vs Union of India (High Court of Madras)

W.P.Nos.22216 to 22219 of 2015 and M.P.Nos.1 to 1 and 2 to 2 of 2015

Date: 21st June 2016

Key Takeaways

- The Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 came into effect on July 1, 2015.

- Applications filed before this date are still eligible for consideration by the Income Tax Settlement Commission.

- The court’s decision clarifies the jurisdiction of the Settlement Commission in cases of undisclosed foreign income filed before the new act’s implementation.

Issue

Does the Income Tax Settlement Commission have jurisdiction to entertain applications for undisclosed foreign income and assets filed before the implementation of the Black Money Act, 2015?

Facts

- The petitioners filed tax returns on May 21, 2015.

- They received a notice under Section 148 (of Income Tax Act, 1961) on May 29, 2015.

- Both these events happened before July 1, 2015, when the Black Money Act came into effect.

- The petitioners then filed applications with the Income Tax Settlement Commission for assessment years 2005-2006 to 2014-2015.

- On June 30, 2015, the Commission rejected these applications, saying they didn’t have jurisdiction.

- The petitioners tried again on July 10, 2015, but were rejected once more on July 15, 2015.

- Frustrated, they took their case to the High Court.

Arguments

Petitioners’ side:

“We filed our returns and got the notice before this new Black Money Act came into play. The Settlement Commission should look at our case under the old rules.”

Commission’s side (initially):

“This new Black Money Act means we can’t touch cases about undisclosed foreign income anymore. We don’t have the power to do that now.”

Key Legal Precedents

In this case, the court didn’t rely on previous case laws. Instead, they focused on a recent circular from the tax department. Specifically, they mentioned:

- Circular No. 12 of 2015

- Explanatory note dated July 2, 2015

These documents clarified when the Black Money Act would start applying.

Judgement

- They said, “Look, based on that explanatory note from July 2, 2015, the Black Money Act only kicked in from July 1, 2015.”

- They pointed out that the petitioners filed their returns and got their notice before this date.

- Therefore, the court ruled that the Settlement Commission should indeed look at these applications.

- They told the petitioners, “Go ahead and file your applications with the Income Tax Settlement Commission again.”

- The court also said, “Commission, you need to consider these applications according to the law.”

FAQs

Q: What’s this Black Money Act everyone’s talking about?

A: It’s the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015. It’s a law designed to deal with undisclosed foreign income and assets.

Q: Why did the Settlement Commission initially reject the applications?

A: They thought the new Black Money Act took away their power to handle cases about undisclosed foreign income.

Q: What changed the court’s mind?

A: The court looked at a circular (No. 12 of 2015) and an explanatory note that clarified when the Black Money Act started applying.

Q: Does this mean anyone can now approach the Settlement Commission for undisclosed foreign income?

A: Not exactly. This ruling applies to cases where the tax returns were filed and notices were issued before July 1, 2015, when the Black Money Act came into effect.

Q: What happens next for the petitioners?

A: They need to file their applications again with the Income Tax Settlement Commission, which will then consider their case under the applicable laws.

1. Heard Mr. V.T. Gopalan, learned Senior Counsel assisted by Mr. Suhrith Parthasarathy, learned counsel for the petitioner and Mr. T. Promod Kumar Chopda, learned Standing Counsel appearing for the respondents.

2.In the light of the stand taken by the respondents in their counter affidavit, it may not be necessary to go into the factual averments nor test the correctness of the impugned proceedings on the merits of the case. It would suffice to take note of the following facts for the purpose of disposal of the writ petitions.

3.The petitioners have filed these four writ petitions challenging the orders passed by the Income Tax Settlement Commission, Additional Bench, Chennai dated 30.06.2015 and 15.07.2015. The petitioners have filed applications before the Settlement Commission in respect of the assessment years 2005 - 2006 to 2014 - 2015. The applications came to be rejected, by order dated 30.06.2015, on the following ground:

"11.10 Therefore after going though the applications, the arguments by the A.R. and papers filed during the course of hearing, we are of the view that the Commission does not have jurisdiction to entertain these applications offering undisclosed foreign income and assets. Since the Commission does not have the jurisdiction, we have not gone into the further question as to whether the Applicants have fulfilled the conditions u/s.245C (of Income Tax Act, 1961). The order was pronounced in the court on 30.06.2015.

11.11 For the reasons discussed above, we do not allow the above Settlement Applications to be proceeded with and reject the same."

4.Thereafter, the petitioners filed another application on 10.07.2015 for the same assessment years requesting the Commission to take up the matter and consider the same and this application was rejected by order dated 15.07.2015 and the Commission has stated that the petitioners have re-submitted their applications along with circulars issued by the CBDT. The Commission after considering the submissions made by the petitioners by order dated 15.07.2015 rejected the applications for the following reasons:

"14.7 After going through the Applications, the arguments by the A.R. and papers filed during the course of hearing, we find no reason to interfere in our earlier order dated 30.06.2015 in respect of the above two Applicants and we reiterate our findings given in the said order dated 30.06.2015 that since a resident's total undisclosed foreign income and asset will be dealt under the provisions of the New Act and not under the existing Income Tax Act (which will deal with disclosed foreign income of a resident which is part of the total Income Tax Act), the New Act imposes an implied repeal of the provisions of the Income Tax Act conferring such rights to such assessees to approach the Income Tax Settlement Commission.

14.8 Therefore, we are of the view that the Commission does not have jurisdiction to entertain these Applications offering undisclosed foreign income and assets. Since the Commission does not have the jurisdiction, we have not gone into the further question as to whether the Applicants have fulfilled the conditions u/s.245C (of Income Tax Act, 1961). 14.9 For the reasons discussed above, we do not allow the above Settlement Applications to be proceeded with and reject the same."

5.Challenging these orders, the writ petitions have been filed.

6.In the counter affidavit filed in all these four writ petitions, the respondents have taken the following stand:

"The First Respondent by order dated 01.07.2015 followed by Explanatory notes dated 2.07.2015 issued in Circular No.12 of 2015 have clarified that the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 comes into effect from 1.07.2015. It is submitted that the Petitioner had filed Return of Income on 21.05.2015. Notice u/s.148 (of Income Tax Act, 1961) was issued by the Assessing Officer on 29.05.2015 which is, before coming into effect the provisions of The Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015."

7.In the light of the above stand taken which is based on the Explanatory note dated 02.07.2015 issued in Circular No.12 of 2015, as the Black Money (Undisclosed Foreign Income Tax and Assets) and Imposition of Tax Act, 2015 comes into effect from 01.07.2015 and the petitioners had filed their Return of Income on 21.05.2015 and notice was issued under Section 148 (of Income Tax Act, 1961) by the Assessing Officer on 29.05.2015 which is before coming into effect of the provisions of the Black Money Act, 2015, the applications submitted by the petitioners before the Commission are maintainable.

8.Accordingly, the Writ Petitions are allowed and the impugned orders are set aside and the petitioners are directed to file an application before the Income Tax Settlement Commission, which shall be considered by the Commission in accordance with the provisions of the Act. No costs.

Consequently, connected Miscellaneous Petitions are closed.

21.06.2016

×

Questions

Court Allows Tax Settlement Applications for Undisclosed Foreign Income Filed Before Black Money Act

Write your CommentSimilar Posts

Generic

- Reportdata/2742.pdf