Court Blocks Tax Reassessment, Upholds Full Disclosure Rule in 4-Year Limit Cas…

Full News

Court Blocks Tax Reassessment, Upholds Full Disclosure Rule in 4-Year Limit Cases

Court Blocks Tax Reassessment, Upholds Full Disclosure Rule in 4-Year Limit Cases

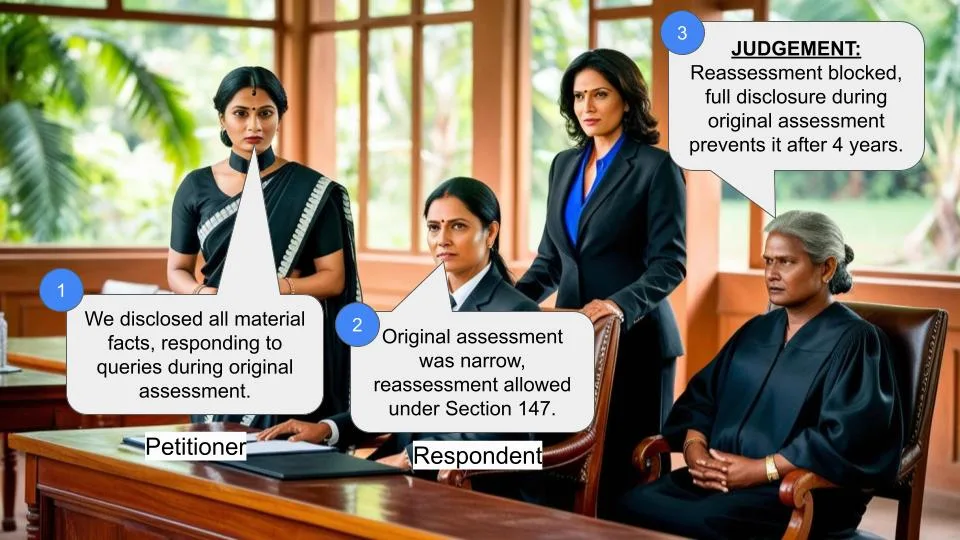

The High Court dismissed an appeal by the Commissioner of Income Tax against Hindustan Latex Ltd., affirming that reassessment after four years is only permissible if the assessee failed to disclose all material facts during the original assessment.

To delve deeper, you can read the original judgement of the court order here.

Case Name:

Commissioner of Income Tax Vs Hindustan Latex Ltd.(High Court of Kerala)

ITA.No. 92 of 2010

Key Takeaways

1. Reassessment after four years requires proof of non-disclosure by the assessee.

2. The Tribunal's factual findings on disclosure are crucial and rarely overturned.

3. Full response to queries and production of requested documents during original assessment prevents later reassessment.

Issue

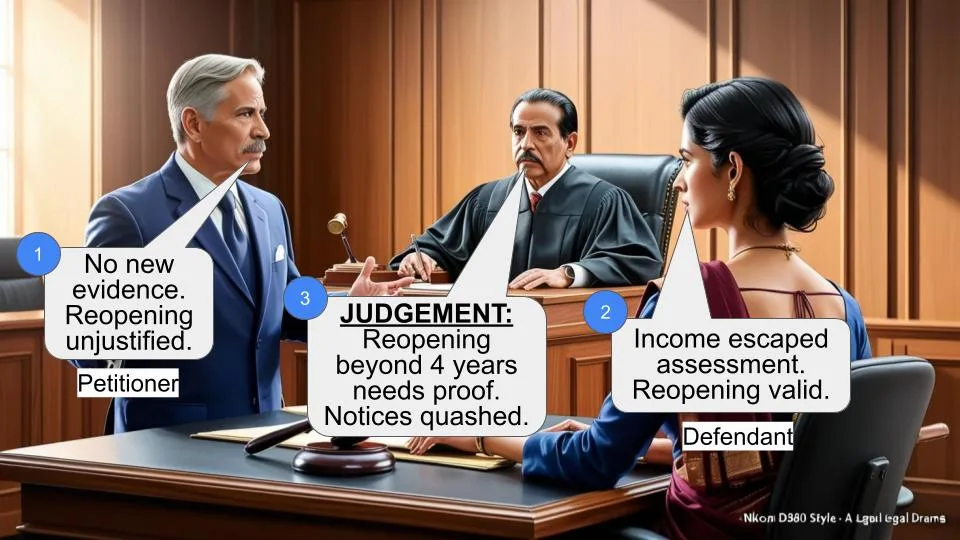

Was the assessing authority entitled to invoke Section 147 (of Income Tax Act, 1961) for reassessment of deductions under Sections 80HH (of Income Tax Act, 1961) and 80I (of Income Tax Act, 1961) after four years from the original assessment?

Facts

1. The original assessment under Section 143(3) (of Income Tax Act, 1961) was completed on 24.03.1995.

2. The assessee had claimed deductions under Sections 80HH (of Income Tax Act, 1961) and 80I (of Income Tax Act, 1961).

3. The assessing officer had raised queries and the assessee had responded with clarifications and documents.

4. The Department attempted reassessment after four years from the end of the relevant assessment year.

Arguments

Department's Argument:

- The original assessment was done within the narrow confines of Section 143(1)(a) (of Income Tax Act, 1961), allowing for reassessment under Section 147 (of Income Tax Act, 1961).

Assessee's Argument:

- All material facts were disclosed during the original assessment, preventing reassessment after four years as per the first proviso to Section 147 (of Income Tax Act, 1961).

Key Legal Precedents

1. Sowdagar Ahmed Khan (deceased) (By His Legal Representatives) v. Income Tax Officer, Nellore [70 ITR 79]

- The Department cited this case to argue for the applicability of Section 147 (of Income Tax Act, 1961).

Judgement

The High Court dismissed the appeal, holding that:

1. The Tribunal was justified in concluding that reassessment proceedings were impermissible under the first proviso to Section 147 (of Income Tax Act, 1961).

2. The assessee had responded to all queries and produced all necessary materials during the original assessment.

3. The Tribunal's factual findings showed that the assessee had fully disclosed all material facts, preventing reassessment after four years.

FAQs

Q1: What is the key condition for reassessment after four years?

A1: The income must have escaped assessment due to the assessee's failure to disclose fully and truly all material facts necessary for the assessment.

Q2: Can the High Court easily overturn the Tribunal's factual findings?

A2: No, the Tribunal is considered the final authority on facts, and its findings are rarely overturned unless perverse.

Q3: What was the significance of the assessee's responses during the original assessment?

A3: The assessee's full responses and production of requested documents during the original assessment prevented later reassessment, as it showed full disclosure of material facts.

Q4: How did the court interpret Section 147 (of Income Tax Act, 1961)?

A4: The court strictly interpreted the first proviso to Section 147 (of Income Tax Act, 1961), emphasizing that reassessment after four years is only permissible if the assessee failed to disclose all material facts during the original assessment.

Q5: What was the impact of this judgment on tax reassessment practices?

A5: This judgment reinforces the importance of full disclosure by assessees during original assessments and limits the tax department's ability to reassess cases after four years without clear evidence of non-disclosure.

1.This income tax appeal by the Department stands admitted on 30.09.2013 formulating the following as the substantial questions of law, for consideration:

(1) “Whether on the facts and circumstances of the case, the Tribunal was right in holding that the reassessment proceedings in the case of the assessee is not valid under law in light of the fact that there has been no full and true disclosure of material necessary for assessment during the original assessment proceedings?

(2) Whether on the facts and circumstances of the case, the Tribunal is right in holding that the Assessing Officer had verified the claim of deduction at the stage of proceedings u/s.143(1) (of Income Tax Act, 1961) (a) and also in the related proceedings u/s.154 (of Income Tax Act, 1961), when in fact the Assessing Officer had only considered the allowability of the deduction in toto under the above proceedings and not the eligibility of the assessee to claim the deductions, since there was no opportunity for the Assessing Officer to verify the previous assessment records of the assessee to detect the wrongful claim as he is constrained under law from going into the past records under the provisions of Section 143(1)(a) (of Income Tax Act, 1961)?

(3) Whether on the facts and circumstances of the case, the finding of the Tribunal is perverse in nature as the same is based on wrong appreciation of facts?”

2.We have heard the learned counsel for the Department and the learned counsel for the respondent/assessee, which is a Government Company.

3. Learned counsel for the respondent pointed out that no question of law much less any substantial question of law, including those mentioned hereinabove, arises for decision in this appeal, going by the order of the Income Tax Appellate Tribunal as also the order of the subordinate authority, which the Tribunal considered.

4. Learned Senior Standing Counsel for the Department argued that the Tribunal exceeded its jurisdiction in setting aside the action taken by the assessing authority to determine and assess income which, according to the assessing authority, had escaped assessment. He pithily pointed out that the Tribunal erred in law in holding that the materials were insufficient for the assessing authority to proceed under Section 147 (of Income Tax Act, 1961), the 'Act', for short. Specific reference was made to the decision in Sowdagar Ahmed Khan (deceased) (By His Legal Representatives) v. Income Tax Officer, Nellore [70 ITR 79] to state that when the original assessment order showed that the cash credits in question were not duly considered, proceedings under Section 147 of the Income Tax Act, 1961 would be applicable, going by the ratio of that decision rendered in terms of the corresponding provisions of the 1922 Act.

5.The dispute between the Department and the assessee, is as to whether the assessing authority was entitled to invoke Section 147 (of Income Tax Act, 1961) as regards the deductions granted by the assessing authority at the first instance through the assessment order allowing deductions under Sections 80HH (of Income Tax Act, 1961) and 80I (of Income Tax Act, 1961) during the regular assessment proceedings against the assessee. The argument advanced by the learned counsel for the Department on the basis of the pleadings of the Department in the appeal is that the said issue was considered by the assessing authority through the original assessment order within the narrow confines of Section 143(1)(a) (of Income Tax Act, 1961), and therefore, it was permissible under Section 147 (of Income Tax Act, 1961) to re-open the assessment.

6.The Tribunal through the impugned order noted that the re- assessment was attempted to be made after the period of four years from the end of the relevant assessment year. Specific reference was made to Sub-section (3) of Section 147 (of Income Tax Act, 1961) and the effect of the provisos.

7.We may now note certain factual details, which have been culled out from the relevant paper books and materials by the Appellate Tribunal, which is the last authority on facts, after noticing that the assessment under Section 143(3) (of Income Tax Act, 1961) was done on 24.03.1995. We quote the relevant facts from the order of the Appellate Tribunal as follows:

In the assessee's paper book Pg.No.3 (internal page No.2) shows the deductions under section 80HH (of Income Tax Act, 1961) and 80I (6th year claim) made by the Assessing Officer under the Head revised computation of total income. The assessee's paper book pg.No.6 shows the intimation under Section 143(1)(a) (of Income Tax Act, 1961) dated 16.07.1993 wherein the Assessing Officer has not allowed deduction under section 80I (of Income Tax Act, 1961) as separate accounts have not been kept for new industrial undertaking as required by section 80I (of Income Tax Act, 1961). In assessee's paper book, pg.No.7, in reply to the intimation under section 143(1)(a) (of Income Tax Act, 1961), the assessee vide letter dated 10th July 1993 stated that Section 80-I (of Income Tax Act, 1961) does not insist on keeping separate accounts for the new industrial undertaking. The profit arising out of the operations of the new plants can be reasonably estimated as a proportion to the production since the items produced at all the plants are same. Hence, the basis on which the deduction is allowed under section 80HH (of Income Tax Act, 1961) can be applied for this section also. Therefore since deduction was allowed under section 80HH (of Income Tax Act, 1961), the deduction claimed under section 80-I (of Income Tax Act, 1961) must also be allowed on the same basis. Then in assessee's paper book pg.No.9, the Deputy Commissioner of Income Tax (Asst.), Special Range vide letter dated 10.08.1993 invited the assessee's attention to section 80I(6) (of Income Tax Act, 1961). He pointed out that in section 80HH (of Income Tax Act, 1961) there was no parallel sub-section. The Deputy Commissioner, however, submitted that if any case laws are available in assessee's favour, he may be informed of the same. Further, the Deputy Commissioner asked the assessee to clarify why this deduction was claimed at 5% only. The assessee vide his letter dated 19th August 1993 furnished the necessary clarifications in first para itself which is available in assessee's paper book pg.No.10. It was also accepted by the ld. Counsel for the assessee in assessee's paper book in pg.11 that it appears by mistake he has claimed only 5% instead of 25%. Since it was mistake apparent on record, he requested the Department to allow the eligible 25% deduction. The assessee's paper book pg.No.12 particularly para 2 sub-para (a) relates to the Department's rectification order under section 154 (of Income Tax Act, 1961) wherein the assessee vide letter dated 30.07.1993 pointed out that the Department has accepted that this is a debatable issue which cannot be covered under section 143(1)(a) (of Income Tax Act, 1961) and allow the deductions claimed. The Department allowed the request of the assessee to fully deduct 25% since this was within the scope of section 143(1)(a) (of Income Tax Act, 1961). The rectified deduction of income under Section 80I (of Income Tax Act, 1961) is given in assessee's paper book pg.No.13. The assessee has furnished the information called for by the Department in detail which is available in assessee's paper book, pg.Nos.14 and 15 particularly pg.15 and pg.No.16 mentions about the schedule of sundry creditors.”

8.On the basis of the aforesaid materials, the Appellate Tribunal was satisfied that the assessing officer, in the first round, while making the original assessment order, had actually considered the materials, after requiring the relevant materials to be produced. The assessee-Company had produced those materials and the Tribunal also dilated on the question as to whether the claims were debatable or not.

With the aforesaid in mind, we revert to the first proviso to Section 147 (of Income Tax Act, 1961). It has to be pointedly noted here that action under the first proviso to Section 147 (of Income Tax Act, 1961), that is to say, for a period after the expiry of four years, can be generated only if the income chargeable to tax has escaped assessment by reason of the failure on the part of the assessee to make a return under section 139 (of Income Tax Act, 1961) or in response to a notice issued under Section 142(1) (of Income Tax Act, 1961) or Section 148 (of Income Tax Act, 1961) or to disclose fully and truly all material facts necessary for the assessment. As is clearly discernible from what we have quoted above out of the order of the Tribunal, it was crystal clear for the Tribunal that the assessee had responded to the queries raised by the assessing officer in the original assessment proceedings and during the course of such proceedings had produced all material facts as were called for and were relevant and necessary for completing the assessment for the year. Under such circumstances, we are of the view that the Tribunal was abundantly justified in the facts and in the circumstances of the case in hand to have concluded that this is a case where proceedings were impermissible in view of the embargo under the first proviso to Section 147 (of Income Tax Act, 1961). Having held so, we cannot but to affirm the decision of the Tribunal and thereby answer the questions raised by the Revenue against it. The income tax appeal is dismissed answering the questions formulated, against the Revenue.

(THOTTATHIL B.RADHAKRISHNAN, JUDGE)

(DEVAN RAMACHANDRAN, JUDGE)

×

Similar Ripples

Questions

Court Blocks Tax Reassessment, Upholds Full Disclosure Rule in 4-Year Limit Cases

Write your CommentSimilar Posts

Generic

- Reportdata/11464-kerela-HC.pdf