Court Clarifies "Previous Year" in IT Act, Overturns Outdated Credit Assessment

Full News

Court Clarifies "Previous Year" in IT Act, Overturns Outdated Credit Assessment

Court Clarifies "Previous Year" in IT Act, Overturns Outdated Credit Assessment

This case involves Ivan Singh (the appellant-assessee) challenging the Income Tax Department's (respondent-Revenue) assessment for the year 2009-10. The main dispute centered around the interpretation of "previous year" in the Income Tax Act and the addition of unexplained credits from an earlier financial year. The High Court ruled partially in favor of the assessee, overturning the addition of old credits but upholding the disallowance of certain labor charges.

Get the full picture - access the original judgement of the court order here

Case Name:

Ivan Singh vs Assistant Commissioner of Income Tax & Anr. (High Court of Bombay)

Tax Appeal No. 29 of 2013

Date: 14th February 2020

Key Takeaways:

1. The court clarified that "previous year" in the IT Act means the financial year immediately preceding the assessment year.

2. Unexplained credits can only be taxed in the year they appear, not in subsequent years.

3. The court upheld the principle that disallowances should not be based on mere suspicion but on reasonable grounds.

4. The judgment emphasizes the importance of proper timing in tax assessments.

Issue:

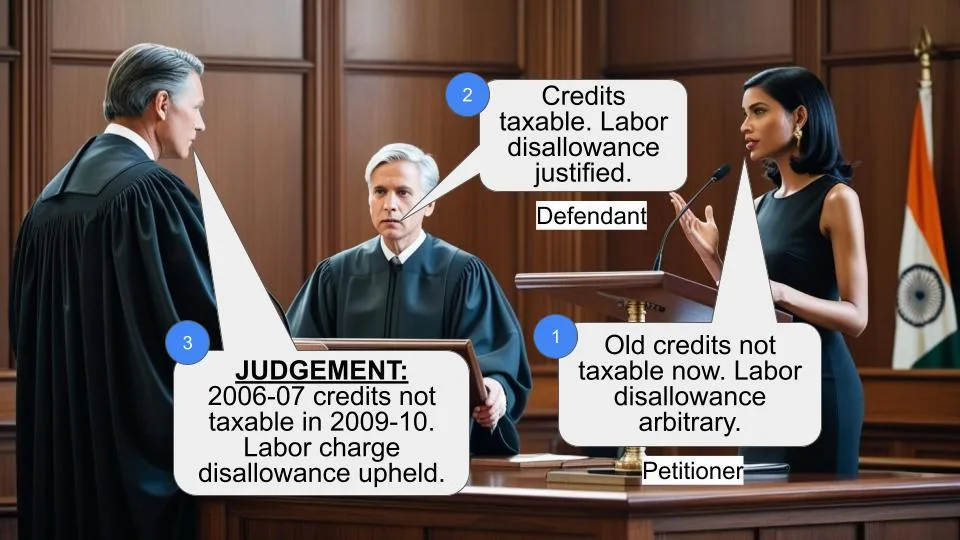

Can unexplained credits from the financial year 2006-07 be added to the assessee's income for the assessment year 2009-10 under Section 68 (of Income Tax Act, 1961)?

Facts:

1. The case relates to the assessment year 2009-10 (previous year 2008-09).

2. The Assessing Officer found unexplained credits in the assessee's books for the financial year 2006-07.

3. These credits, amounting to Rs. 62,24,163, were added to the assessee's income for the assessment year 2009-10.

4. Additionally, the Assessing Officer disallowed Rs. 26,54,158 out of labor charges on an ad hoc basis.

5. The assessee appealed these decisions through various stages, ultimately reaching the High Court.

Arguments:

Assessee's Arguments:

1. Section 68 (of Income Tax Act, 1961) only allows taxation of unexplained credits in the year they appear, not in subsequent years.

2. The disallowance of labor charges was based on mere suspicion without substantial evidence.

Revenue's Arguments:

1. The assessee didn't raise the "previous year" argument in earlier proceedings.

2. The assessee was given an opportunity to explain the cash payments for labor charges.

3. The disallowance was reasonable, considering the assessee's failure to contest a similar disallowance in the preceding year.

Key Legal Precedents:

1. Commissioner of Income-Tax, Poona Vs. Bhaichand H. Gandhi, 141 ITR 67

2. Commissioner of Income-Tax, Rajasthan Vs. Lakshman Swaroop Gupta & Brothers, 100 ITR 222

3. M/s Bhor Industries Limited Vs. Commissioner of Income Tax, Bombay, AIR 1961 SC 1100

4. Abdul Qayume Vs. Commissioner of Income-Tax, 184 ITR 404

5. Laxmi Engineering Industries Vs. Income-Tax Officer, [2008] 298 ITR 203 (Raj)

6. J.K. Woollen Manufacturers Vs. Commissioner of Income-Tax, U.P., 72 ITR 612

These cases supported the interpretation of "previous year" and the principle that disallowances should not be based on mere suspicion.

Judgement:

1. The court ruled in favor of the assessee on the first question, stating that unexplained credits from 2006-07 cannot be added to the income for the assessment year 2009-10.

2. The court upheld the disallowance of labor charges, finding that it was not based on mere suspicion and that the assessee was given an opportunity to explain.

3. The court ordered the Assessing Officer to modify the assessment in accordance with this judgment.

FAQs:

1. Q: What does "previous year" mean in the Income Tax Act?

A: As per Section 3 (of Income Tax Act, 1961), "previous year" means the financial year immediately preceding the assessment year.

2. Q: Can the Income Tax Department add unexplained credits from past years to current assessments?

A: No, unexplained credits can only be taxed in the year they appear in the books of accounts.

3. Q: On what basis can the Income Tax Department disallow expenses?

A: Disallowances should not be based on mere suspicion but on reasonable grounds and after giving the assessee an opportunity to explain.

4. Q: Does failing to contest a disallowance in one year affect future assessments?

A: While it may be considered, it's not the sole basis for disallowance. Each year's assessment should be based on its own merits.

5. Q: What's the significance of this judgment for taxpayers?

A: It emphasizes the importance of timing in tax assessments and reinforces the principle that unexplained credits should be assessed in the year they appear.

Heard Dr. Daniel with Ms. Y. Mandrekar, the learned Counsel for the appellant-assessee and Ms. Susan Linhares, the learned Standing Counsel for the respondent-Revenue.

2. On 02.12.2013, this Appeal came to be Admitted on the following substantial questions of law:

(I) On the facts and in the circumstances of the case and in law, whether the Tribunal was right in sustaining the additions made of old outstanding sundry credit balances amounting to Rs.62,24,163/- under Section 68 of the Income Tax Act, 1961 ?

(II) On the facts and in the circumstances of the case and in law, whether the Tribunal was right in sustaining the allowance made of Rs.26,54,158/- out of labour charges on an adhoc basis ?

(III) On the facts and in the circumstances of the case and in law, whether the I.T.A.T. had any material to confirm the adhoc disallowance of labour charges of Rs.26,54,158/- on an assumption that the same are not genuine ?

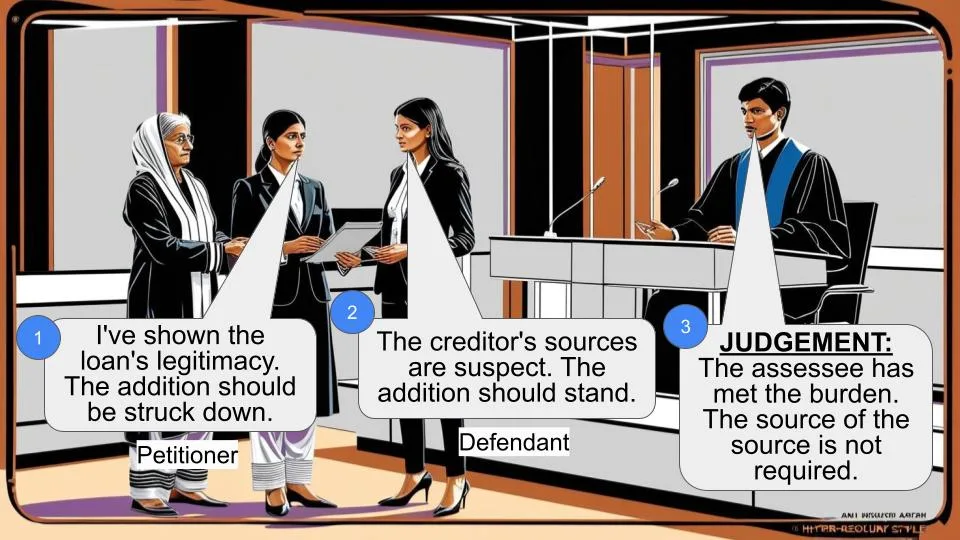

3. Insofar as the first substantial question of law is concerned, Dr. Daniel has pointed out that Section 68 (of Income Tax Act, 1961) (IT Act), is very clear in providing that where any sum is found to be credited in the books of the assessee for the previous year and the assessee offers no explanation about the nature and source thereof or the explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, the sum so credited may be charged to the income tax as the income of the assessee of that previous year. Relying upon several decisions, Dr. Daniel submits that since, it is the case of Revenue that some amounts were found credited in the books of account for the financial year 2006-07, there was no question of taking cognizance of such amounts for the assessment year 2009-10 and the corresponding previous year 2008-09. He submits that on this short ground, the first substantial question of law, is liable to be answered in favour of the appellant-assessee and against the respondent-Revenue.

4. Insofar as the second and third substantial questions of law are concerned, Dr. Daniel is quite correct in pointing out that both these substantial questions of law relate to one and the same issue of adhoc disallowance of labour charges to the extent of 26,54,158/-. ₹ He submits that in the present case, disallowance is only on the basis of some suspicion, which is backed by no material as such. He submits that the disallowance is also based upon the failure on the part of the appellant-assessee to challenge the similar disallowance for the preceding year 2008-09. He submits that in such matters, principles of estoppel or acquiescence cannot be applied and therefore, the substantial questions of law are liable to be answered in favour of the appellant-assessee and against the respondent-Revenue. Dr. Daniel referred to certain decisions in support of his contentions.

5. Ms. Linhares, the learned Standing Counsel for the respondent-Revenue supports the impugned judgments and orders made by the ITAT, on the basis of the reasoning reflected therein. She pointed out that the contentions based upon the definition of the “previous year” and the provisions of the IT Act were never raised and therefore, are not reflected in the order of the ITAT. She pointed out that there are concurrent findings of facts in relation to disallowance of labour charges. She pointed out that opportunity was granted to the appellant-assessee to explain the cash payment against vouchers amounting to 2.65 crores in respect of labour charges. For these ₹ reasons, she submits that the substantial questions of law may be decided against the appellant-assessee and in favour of the respondent- Revenue.

6. Rival contentions now fall for our determination.

7. Insofar as the first substantial question of law is concerned, reference at the outset is necessary to the definition of the expression “previous year” as defined in Section 3 (of Income Tax Act, 1961). This definition provides that for the purposes of the IT Act, “previous year” means the financial year immediately preceding the assessment year.

8. Thereafter, reference is necessary to the provisions of Section 68 (of Income Tax Act, 1961), which read as follows:

Cash credits.

68. Where any sum is found credited in the books of an assessee maintained for any previous year, and the assessee offers no explanation about the nature and source thereof or the explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, the sum so credited may be charged to income-tax as the income of the assessee of that previous year:

Provided that where the assessee is a company (not being a company in which the public are substantially interested), and the sum so credited consists of share application money, share capital, share premium or any such amount by whatever name called, any explanation offered by such assessee-company shall be deemed to be not satisfactory, unless—

(a) the person, being a resident in whose name such credit is recorded in the books of such company also offers an explanation about the nature and source of such sum so credited; and

(b) such explanation in the opinion of the Assessing Officer aforesaid has been found to be satisfactory:

Provided further that nothing contained in the first proviso shall apply if the person, in whose name the sum referred to therein is recorded, is a venture capital fund or a venture capital company as referred to in clause (23FB) of section 10 (of Income Tax Act, 1961).

9. From the plain reading of the provisions of Section 68 (of Income Tax Act, 1961), it does appear that where any sum is found to be credited in the books of Account maintained for any previous year and there is no proper explanation for such credit, the sum so credited can be charged to the income tax as the income of the assessee of “that previous year”.

10. In the present case, the material on record indicates that the Assessing Officer has relied upon the credits for the financial year 2006-07. However, the sum so credited, in terms of such credit, is sought to be brought to tax as the income of the appellant-assessee, for the assessment year 2009-10, which means for the previous year 2008- 09, in terms of the definition under Section 3 (of Income Tax Act, 1961). Dr. Daniel is justified in submitting that this is not permissible.

11. The view taken by this Court in Commissioner of Income-Tax, Poona Vs. Bhaichand H. Gandhi, 141 ITR 67 and by Rajasthan High Court in Commissioner of Income-Tax, Rajasthan Vs. Lakshman Swaroop Gupta & Brothers, 100 ITR 222, supports the contentions raised by Dr. Daniel. Similarly, we find that in M/s Bhor Industries Limited Vs. Commissioner of Income Tax, Bombay, AIR 1961 SC 1100, the Hon'ble Apex Court in the context of provisions of the Merged States (Taxation Concessions) Order (1949) has interpreted the expression “any previous year” to mean as not referring to all the previous years, but, the previous year in relation to the assessment year concerned. Again, this decisions also, to some extent, supports the contentions of Dr. Daniel.

12. The crucial phrase in Section 68 (of Income Tax Act, 1961), which provides that the sum so credited in the books and which is not sufficiently explained, may be charged to the income tax as income of the assessee of “that previous year” also lends support to the contentions of Dr. Daniel.

13. For all the aforesaid reasons, we answer the first substantial question of law in favour of the appellant-assessee and against the respondent-Revenue.

14. Insofar as the second and third substantial questions of law are concerned, we find that the Assessing Officer, the Commissioner (Appeals) as well as the ITAT have recorded concurrent findings of facts. The contention that no opportunity was afforded to the assessee is not correct. The order of the Assessing Officer clearly indicates that opportunity to explain the cash payments to the tune of 2.65 crores ₹ was afforded to the assessee. It is only after taking into consideration the explanation offered and further, looking to the position of the preceding year, which was not even contested, the Assessing Officer has made disallowance only to the extent of 10% of 2.65 crores. In these ₹ circumstances, we do not think that the substantial questions of law, as framed, on this issue of disallowance are required to be answered in favour of the appellant-assessee.

15. In Abdul Qayume Vs. Commissioner of Income-Tax, 184 ITR 404, the Allahabad High Court has no doubt held that an admission or an acquiescence cannot be the foundation for an assessment, where the income is returned under an erroneous impression or misconception of law. In the present case, the foundation of the assessment order cannot be said to be an admission or an acquiescence on the part of the assessee. The circumstance that in the preceding year that the appellant has not allowed disallowance, is only one of the considerations taken into account by the Assessing Officer.

16. In Laxmi Engineering Industries Vs. Income-Tax Officer, [2008] 298 ITR 203 (Raj) and J.K. Woollen Manufacturers Vs. Commissioner of Income-Tax, U.P., 72 ITR 612, it is held that disallowance should not be on the basis of mere suspicion and further, on applying test of commercial expediency, the reasonableness of the expenditure must be judged from the point of view of the businessman and not on the Income Tax Department. To the similar effect are certain observations in Principal Commissioner of Income-Tax, Mumbai Vs. Chawla Interbild Construction Co. (P) Ltd., [2019] 104 taxmann.com 402 (Bombay).

17. On perusing the impugned judgment made by the Assessing Officer, Commissioner (Appeals) and the ITAT, we are satisfied that all these Authorities have in fact, followed the principles laid down in the aforesaid decisions. This is not a matter where the disallowance is based on mere suspicion. Further, it is only accepting the principle that commercial expediency has to be judged from the view of businessman, that these Authorities have made disallowance of only 10%, in the present case. There is neither any unreasonability nor any perversity in the approach or the findings of these authorities so as to warrant interference.

18. For all these reasons, the second and the third substantial questions of law are required to be answered against the appellant- assessee and in favour of the respondent-Revenue.

19. The Appeal is accordingly disposed off in the aforesaid terms. The modification in terms of this judgment and order to be carried out by the concerned Assessing Officer, within a reasonable period.

20. The Appeal is disposed off, without there being any order as to costs.

SMT. M. S. JAWALKAR, J. M. S. SONAK, J.

×

Questions

Court Clarifies "Previous Year" in IT Act, Overturns Outdated Credit Assessment

Write your CommentSimilar Posts

Generic

- Reportdata/6044.pdf