Court Clarifies Scope of Section 153A (of Income Tax Act, 1961) in Income Tax S…

Full News

Court Clarifies Scope of Section 153A (of Income Tax Act, 1961) in Income Tax Searches

Court Clarifies Scope of Section 153A (of Income Tax Act, 1961) in Income Tax Searches

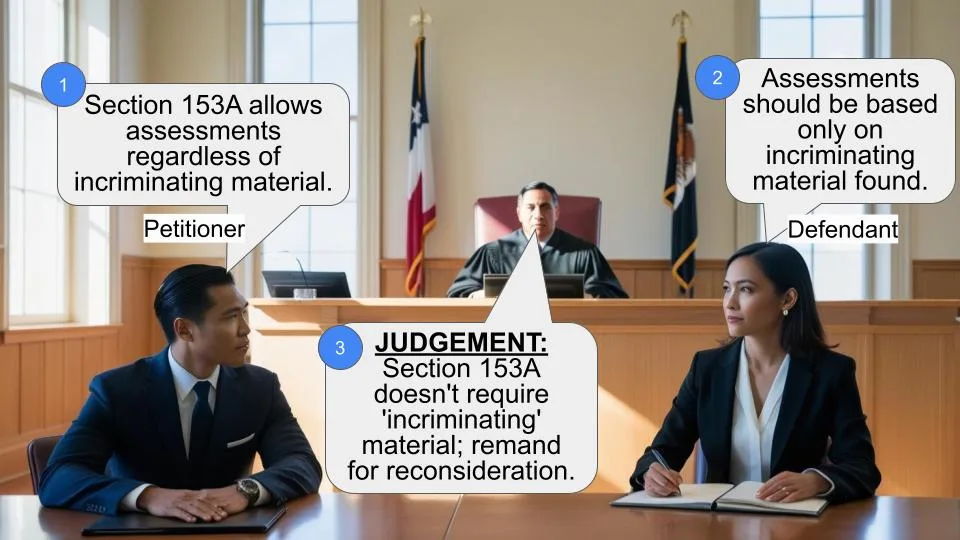

This case involves the Revenue and several assessees, primarily partnership firms engaged in chit and money lending businesses. The central issue was whether additions under Section 153A (of Income Tax Act, 1961) could be made only if incriminating material was found during a search. The court ultimately decided in favor of the Revenue, remanding the case back to the Tribunal for reconsideration, emphasizing that Section 153A (of Income Tax Act, 1961) does not require incriminating material to proceed with assessments.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs. St. Francis Clay Decor Tiles (High Court of Kerala)

ITA. No. 169 of 2015

Date: 22nd March 2016

Key Takeaways:

- Section 153A (of Income Tax Act, 1961) allows the Assessing Officer to assess or reassess income for six years prior to the year of search, regardless of whether incriminating material is found.

- The court clarified that the term “incriminating” is not used in Section 153A (of Income Tax Act, 1961), and any material unearthed during a search can be used as evidence.

- The Tribunal’s reliance on the Special Bench decision in All Cargo Logistics Ltd was deemed inappropriate without considering the specific facts of the case.

Issue:

Can additions under Section 153A (of Income Tax Act, 1961) be made only if incriminating material is found during a search, especially when regular assessment proceedings are abated?

Facts:

- The assessees are partnership firms involved in chit and money lending businesses.

- A search under Section 132 (of Income Tax Act, 1961) was conducted on March 26, 2008, at the premises of the firms and their partners.

- Notices under Section 153A (of Income Tax Act, 1961) were issued for assessment years 2002-2003 to 2007-2008.

- The assessees argued that assessments for years 2002-2003 to 2005-2006 should be based only on incriminating materials found during the search.

Arguments:

- Revenue: Argued that Section 153A (of Income Tax Act, 1961) does not require incriminating material to proceed with assessments. The Assessing Officer is empowered to assess or reassess income for six prior years, regardless of the presence of incriminating material.

- Assessees: Contended that assessments should be based only on incriminating materials found during the search, especially for years where assessments were already concluded.

Key Legal Precedents:

- All Cargo Logistics Ltd [137 ITD 287 (Mum)]: The Tribunal relied on this case, which held that assessments under Section 153A (of Income Tax Act, 1961) should be based on incriminating material.

- Commissioner of Income-Tax v. Continental Warehousing Corporation and All Cargo Global Logistics Ltd [2015] 374 ITR 645: Discussed the application of Section 153A (of Income Tax Act, 1961) in pending and concluded proceedings.

- Commissioner of Income Tax v. Kabul Chawla [(2016) 380 ITR 573 (Delhi)]: Addressed the requirement of incriminating material for Section 153A (of Income Tax Act, 1961) assessments.

Judgement:

The court set aside the Tribunal’s decision and remanded the case for fresh consideration, emphasizing that Section 153A (of Income Tax Act, 1961) does not require incriminating material to proceed with assessments. The court instructed the Tribunal to consider the principles laid down in relevant judgments and decide on the merits.

FAQs:

What is Section 153A (of Income Tax Act, 1961)?

Section 153A (of Income Tax Act, 1961) allows the Assessing Officer to assess or reassess income for six years prior to the year of search, regardless of whether incriminating material is found.

Does Section 153A (of Income Tax Act, 1961) require incriminating material to proceed with assessments?

No, the court clarified that the term “incriminating” is not used in Section 153A (of Income Tax Act, 1961), and any material unearthed during a search can be used as evidence.

What was the outcome of this case?

The court remanded the case back to the Tribunal for reconsideration, emphasizing that Section 153A (of Income Tax Act, 1961) does not require incriminating material to proceed with assessments.

Why was the Tribunal’s decision set aside?

The Tribunal’s decision was set aside because it relied on the Special Bench decision in All Cargo Logistics Ltd without considering the specific facts of the case.

1. The captioned appeals are filed by the Revenue challenging Annexure F order of the Income Tax Appellate Tribunal, Cochin Bench dated 10.10.2014. By a common order, 84 connected appeals filed by the Revenue were dismissed by the Tribunal and it is accordingly the captioned appeals along with other appeals were filed by the Revenue before this court.

2. In all the 84 appeals, one question was common and in the above 21 appeals, out of the 84 appeals, apart from the common question involved, yet another question of law was involved. While arguing the common question involved in all the 84 appeals, ITA No.84/2015 was taken as the main case and only the common question involved in the 84 appeals alone was considered and judgement was rendered answering the question against the Revenue and thus dismissing all appeals.

3. The second common question in 21 cases due to inadvertence was not brought to our notice and therefore, the said question could not be considered by us and in such circumstances Revenue filed review petitions in the above appeals, the review petitions were allowed and it is thus the above 21 appeals are coming before us to consider the common question involved therein. The common question raised in the above appeals are enumerated as follows:

"1.(a) Whether on the facts and in the circumstances of the case, is not the Tribunal erroneous in holding that addition in pursuance to notice issued under Section 153A (of Income Tax Act, 1961) can be made only if incriminating material is found and seized in case where there is also abatement of regular assessment proceedings, and are not, such an approach and the resultant conclusion perverse and uncalled for ?

(b) Whether on the facts and in the circumstances of the case and when the Assessing Officer is empowered to assess and reassess income for six prior period assessment years notwithstanding the provisions in sections 139, 147, 148, 149, 151 and 153 is not the above approach of the Tribunal one putting an artificial cap on section 153A (of Income Tax Act, 1961) ?”

4. The facts required for the disposal of the above appeals are common in nature and they are as follows: 5. The parties are hereinafter referred to as Revenue and assessee for convenience. The assesses are partnership firms which are carrying on Chit business and money lending business by way of gold loans and pro-note loans. Head office of the firms is at Palayamparambu with three branches at Chalakudy, Annamanada and Mala. The firms are belonging to E.T. Devassy Group. A search under Section 132 (of Income Tax Act, 1961) was conducted on 26.3.2008 at the premises of some of the firms and residence of Partners. A search under Section 132 (of Income Tax Act, 1961) was also conducted at the business premises of M/s.New Kerala Investments, Palayamparambu.P.O., Thrissur. Consequent to search the Assessing Officer issued notice under Section 153A (of Income Tax Act, 1961) for A.Ys. 2002 - 2003 to 2007-2008 and issued notice under Section 142(1) (of Income Tax Act, 1961) for A.Y. 2008-2009. The assessees filed returns of income and the Assessing Officer completed assessment under Section 153A (of Income Tax Act, 1961) vide order dated 29.12.2009 in respect of A.Ys. 2002-2003 to 2007-2008 and under Section 143(3) (of Income Tax Act, 1961) in respect of A.Y.2008-2009. The assessees have raised a legal issue before the Commissioner of Income Tax (Appeals) that the assessment under Section 153A (of Income Tax Act, 1961) for A.Ys.2002-2003 to 2006-2007 are to be made only on the basis of incriminating materials found/seized during the course of search. The CIT(Appeals) by its order dated 4.6.2013, held in favour of the assessee on this issue by following the decisions of the Special Bench of the Tribunal in the case of All Cargo Logistics Ltd [137 ITD 287 (Mum) (Single Bench)] and in the case of DCIT v. Matha Enterprises (ITA 269 to 275/COCH/2010).

6. Aggrieved by the order of the CIT (Appeals), Revenue preferred appeals before the Income Tax Appellate Tribunal but however, the Tribunal did not find any infirmity in the order passed by the CIT(Appeals) and accordingly the grounds raised by the Revenue regarding the same were rejected. It is thus challenging Annexure F common order of the Income Tax Appellate Tribunal, the above appeals are preferred.

7. Heard learned Senior Counsel for the Revenue and learned Senior Counsel appearing for the assessee.

8. The main contention advanced by the learned Senior Counsel for the Revenue is that, the Tribunal erred in holding that the addition in pursuance to notice issued under Section 153A (of Income Tax Act, 1961) can be made only if incriminating material is found and seized in case where there is also abatement of regular assessment proceedings. That apart it is contended that such a restriction to Section 153A (of Income Tax Act, 1961) is artificial in nature since the Assessing Officer under law is vested with power to assess or re-assess income for six prior period assessment years notwithstanding the provisions of Sections 139, 147, 148, 149, 151 and 153. Learned Senior Counsel also contended that the view taken by the ITAT is against the settled principles of interpretation of statutes and hence perverse. Therefore, learned Senior Counsel contended that the findings rendered by the Appellate Tribunal with respect to the scope of Section 153A (of Income Tax Act, 1961) cannot be sustained under law. Learned counsel has also invited our attention to Section 153A (of Income Tax Act, 1961) and contended that the word “incriminating” is not used anywhere in the said provision and therefore by incorporating such a provision the Tribunal was expanding the scope of the said provision. It is also contended by the learned Senior Counsel that Section 153A (of Income Tax Act, 1961) can be invoked by the Assessing Officer if and when the search is initiated under Section 132 (of Income Tax Act, 1961) or books of account, other documents or any assets are requisitioned under Section 132A (of Income Tax Act, 1961). In that event, learned Senior Counsel contends that the Assessing Officer is vested with powers to issue notice to such person requiring him to furnish within such period as may be specified in the notice, the return of income in respect of each assessment year falling within six assessment years referred to in Clause (b), in the prescribed form and verified in the prescribed manner and setting forth such other particulars as may be prescribed and the provisions of the Income Tax Act shall, so far as may be, apply accordingly as if such return were a return required to be furnished under section 139 (of Income Tax Act, 1961).

9. It is also contended that as per Section 153A(1)(b) (of Income Tax Act, 1961) when such a procedure is adopted by the Assessing Officer, the Assessing Officer can assess or re-assess the total income of six assessment years immediately preceding the assessment year relevant to the previous year in which such search is conducted or requisition is made, that the proviso further provides that the Assessing Officer shall assess or re-assess the total income in respect of each assessment year falling within such six assessment years. That apart, it is contended that the second proviso to the said section says that assessment or re-assessment, if any, relating to any assessment year falling within the period of six assessment years referred to in this sub-section pending on the date of initiation of the search under Section 132 (of Income Tax Act, 1961) or making of requisition under Section 132A (of Income Tax Act, 1961), as the case may be, shall abate. Therefore, it is contended that whenever there is a search, the Assessing Officer is bound under law to re-open the assessment by resorting to Section 153A (of Income Tax Act, 1961), and after complying with the statutory requirement provided thereunder, the assessment shall be done by taking into account the materials produced by the assessee, recovered in search and all other materials that is received by the Assessing Officer in the proceedings under Section 132 (of Income Tax Act, 1961). It is also contended by the learned Senior Counsel that the first proviso to Section 153A (of Income Tax Act, 1961) vests ample power with the Assessing Officer to assess or re-assess the total income in respect of each assessment years falling within such six assessment years.

10. It is therefore contended that the Tribunal went wrong in holding that in order to proceed under Section 153A (of Income Tax Act, 1961) incriminating materials should be recovered. Learned Senior Counsel contends that such findings of the Tribunal cannot be sustained under law since under Section 153A (of Income Tax Act, 1961) nowhere it is stated that the materials recovered while conducting search under Section 153A (of Income Tax Act, 1961) should be incriminating in nature. It is also contended that whatever materials unearthed during the search operations under Section 132 (of Income Tax Act, 1961) is sufficient to proceed under Section 153A (of Income Tax Act, 1961). That being the situation, the Tribunal went wrong in holding that there are no incriminating materials before the Assessing Officer to proceed against the assessee. It is also contended by the learned Senior Counsel for the Revenue that during the search operations the Managing Partner of the firms involved in the above 21 appeals has conceded that an amount of Rs.2.75 Crores was not disclosed by him while submitting the returns. It is also contended by the learned Senior Counsel for the revenue that in the remand report the Assessing Officer has stated that there are documents unearthed in the form of day book and ledger relating to assessment years 2006 - 2007 to 2008 - 2009 and seized from the business premises of the assessee firms. It is further contended in that regard by the Revenue that since materials belonging to the assessee firms were found and seized in the course of a search and seizure operation conducted under Section 132 (of Income Tax Act, 1961), the Assessing Officer was bound to issue notices to the assessee firms to furnish return for each assessment year falling within the six assessment years immediately preceding the assessment year relating to the previous year in which the search was made. Thus according to the Revenue, under the provisions of law notice under Section 153A (of Income Tax Act, 1961) are to be issued for all the six assessment years irrespective of whether materials relating to all these assessment years were found or seized during the course of the search. That apart it is contended by the Revenue that under the current scheme of search, the Assessing Officer was empowered to assess or re-assess the total income of all the six assessment years, notwithstanding that the income tax assessments for certain years were concluded as on the date of search. Therefore, according to the Revenue, the objection of the assessee regarding initiation of assessment proceedings for the assessment years 2002- 2003 to 2005 - 2006 was not legally valid.

11. Learned Senior Counsel for the Revenue has also invited our attention to judgement of the Apex Court in Salem Co-operative Central Bank Ltd. v. Commissioner of Income-Tax [(1993) 201 ITR 697] to canvass the proposition that if and when there is any error which is manifested in the contention of both sides before the Tribunal this court has jurisdiction to correct the error in the order of the Tribunal so long as the point arose out of its order, whoever be the author of the mistake or error in taking up a particular contention. With the above said proposition learned counsel has contended that merely because the Assessing Officer has submitted certain incorrect facts before the 1st Appellate Authority, that will not in any manner affect the case of the Revenue and such errors are liable to be corrected by the Tribunal. So also learned Senior Counsel invited our attention to the judgement of the Apex Court in Income Tax Officer, Special Investigation Cirlcle "B", Meerut v. Seth Brothers and others [(1969) 74 ITR 836] to contend that as per Section 132 (of Income Tax Act, 1961), the warrant of authorisation do not require to specify the particulars of documents and books of accounts but it contemplates only the general authorisation to search for and seize documents and books of account relevant to or useful for any proceeding to comply with the requirements of the Act and the Rules, that it is for the officer making the search to exercise his judgement and seize or not seize any documents or books of account. An error committed by the officer in seizing documents which may ultimately be found not to be useful for or relevant to the proceeding under the Act will not by itself vitiate the search, nor will it entitle the aggrieved person to an omnibus order releasing all documents seized. That apart it is also contended that any irregularity in the course of entry, search and seizure committed by an officer acting in pursuance of the authorisation will not be sufficient to vitiate the action taken, provided the officer has, in executing the authorisation, acted bonafide. Learned Senior Counsel also invited our attention to the judgement of this court in V. Kunhambu and sons v. Commissioner of Income-Tax [(1996) 219 ITR 235] to explain the nature of Section 132(4) (of Income Tax Act, 1961) wherein it is provided that the authorised officer may, during the course of search or seizure, examine on oath any person who is found to be in possession or control of any books of account, documents, money, bullion, jewellery or other valuable article or thing and any statement made by such person during such examination may thereafter be used in evidence in any proceeding under the Indian Income Tax Act, 1922 (11 of 1922), or under this Act. Further the explanation contained thereunder reads thus:

"Explanation.- For the removal of doubts, it is hereby declared that the examination of any person under this sub-section may be not merely in respect of any books of account, other documents or assets found as a result of the search, but also in respect of all matters relevant for the purposes of any investigation connected with any proceeding under the Indian Income- tax Act, 1922 (11 of 1922), or under this Act.”

12. So also our attention was invited to the judgement of a Division Bench of this court in Commissioner of Income-Tax v. Hotel Meriya reported in [(2011) 332 ITR 537] with respect to the validity of the search operations contained under Section 132 (of Income Tax Act, 1961) vis-a-vis Section 158BB (of Income Tax Act, 1961). In the said judgement it was held that the statement made by a partner of a firm is evidence as contemplated under Section 3 of the Evidence Act and therefore, such evidence is a valid material to proceed under Section 158BB (of Income Tax Act, 1961).

13. Therefore, learned Senior Counsel contends that if and when a search is conducted as provided under Section 132 (of Income Tax Act, 1961), the Assessing Officer is bound to initiate action under Section 153A (of Income Tax Act, 1961) and proceed in terms of the said provision. The thrust of the contention made by the learned Senior Counsel is that, when under a search any material as provided under Section 132 (of Income Tax Act, 1961) is unearthed or statement of a responsible person is taken out by the Assessing Officer, that by itself is a material to proceed under Section 153A (of Income Tax Act, 1961).

Therefore, the Senior Counsel contends that there is no provision at all either under Section 132 (of Income Tax Act, 1961) or under Section 153A (of Income Tax Act, 1961), that in order to proceed under Section 153A (of Income Tax Act, 1961) an incriminating material shall be unearthed. Thus it is contended by the counsel that the finding of the Tribunal that there are no incriminating materials before it so as to justify the action of the Assessing Officer is not a legal and valid finding and thus he seeks interference of this court in these appeals.

14. On the other hand learned Senior Counsel for the assessee contended that in order to assess under Section 153A (of Income Tax Act, 1961), the materials that are unearthed can alone be applied against the relevant assessment years in question as contemplated under Section 153(1)(b) (of Income Tax Act, 1961) and therefore, the Tribunal was right in holding that there was no incriminating materials received during the search operations in order to proceed under Section 153A (of Income Tax Act, 1961). It is also contended that Section 153A (of Income Tax Act, 1961) can be invoked only if materials are procured during the search operations under Section 132 (of Income Tax Act, 1961) and a mere statement made by the Managing Partner, which was retracted by him at the appellate stage, cannot be taken into account to proceed with the assessment under Section 153A (of Income Tax Act, 1961). In order to substantiate the said contention, learned Senior Counsel has invited our attention to the common judgement of the Bombay High Court in Commissioner of Income-Tax v. Continental Warehousing Corporation and All Cargo Global Logistics Ltd. reported in [2015]374 ITR 645] and the judgement of the Delhi High Court in Commissioner of Income Tax v. Kabul Chawla reported in [(2016) 380 ITR 573 (Delhi)]. Learned Senior Counsel contended that in both the judgements the respective courts were considering the question of incriminating materials unearthed during the search operations in order to invoke power under Section 153A (of Income Tax Act, 1961) vis-a-vis its application to pending proceedings, its abatement and concluded proceedings.

15. The issue that was raised by the assessee before the 1st Appellate Authority as well as the Tribunal with regard to the initiation of proceedings under Section 153A (of Income Tax Act, 1961) was that since the assessment for the years 2002 - 2003 to 2005 -2006 were concluded as on the date of the search and no proceedings were pending, the scope of assessment under Section 153A (of Income Tax Act, 1961) for these assessment years was restricted to the incriminating materials relating to those years recovered during the course of search. The assessee further contended that since no incriminating materials relating to these years were found or seized during the course of search the Assessing Officer had no jurisdiction to initiate proceedings under Section 153A (of Income Tax Act, 1961) for the aforesaid years.

16. However, the learned Senior Counsel for the assessee contended that the scope of assessment under Section 153A (of Income Tax Act, 1961) was settled by the Special Bench decision of the ITAT in the case of All Cargo Logistics Ltd (supra). Thus according to the learned Senior Counsel for the assessee, the assessment proceedings which are already terminated are not liable for abatement and only pending assessments as on the date of search shall abate.

Therefore, taking into account such circumstances, Senior Counsel contended that, so far as the assessment with respect to A.Ys. 2002 - 2003 to 2005 - 2006, the assessments are completed as on the date of search and the same can be re-opened only on the basis of specific incriminating documents/transactions/seized assets. It is also contended that as per the scheme of Section 153A (of Income Tax Act, 1961) such assessments which are pending as on the date of search are liable to abate and the assessments which are not pending i.e. completed assessments as on the date of search would hold their base and would not abate. It is also contended by the learned Senior Counsel for the assessee that the scope of assessment under Section 153A (of Income Tax Act, 1961) in the case of assessment that are abated and in the case of assessments that have attained finality as on the date of search, which has been settled by the decision of the Special Bench of the Tribunal referred supra wherein it is held that in case assessment has abated, the Assessing Officer retains the original jurisdiction as well as jurisdiction under Section 153A (of Income Tax Act, 1961) for which assessment shall be made for each assessment separately. Thus according to the learned Senior Counsel, in that circumstances, the Assessing Officer can make additions in the assessment, even if no incriminating material has been found. Therefore, according to the learned Senior Counsel, it thus means that, the assessment under Section 153A (of Income Tax Act, 1961) will be made on the basis of incriminating material, which in the context of relevant provisions means books of account and other documents found in the course of search but not produced in the course of original assessment and undisclosed income or property found during the course of search. Learned counsel also contended that going by the first proviso to Section 153A (of Income Tax Act, 1961) it is categoric and clear that an assessment under Section 153A (of Income Tax Act, 1961) can be made only on unearthed materials to the relevant assessment years. According to the counsel, in such circumstances, the Tribunal was right in dismissing the appeals on the said ground also.

17. After considering the rival submissions and appreciating and perusing the pleadings and documents produced by the Revenue and the written submissions made by the learned counsel for the assessee, we find that the Tribunal without taking any efforts to find out the facts and circumstances involved in the cases on hand has relied on the decision of the Special Bench of the ITAT in All Cargo Logistics Ltd (supra) and has held that there was no need to interfere with the order passed by the Appellate Tribunal. In order to consider the issue, we think it is profitable to extract Section 132(1) (of Income Tax Act, 1961) and clause (a) and sub-section (4).

"132. Search and seizure

(1) Where the Director General or Director or the Chief Commissioner or Commissioner or Additional Director or Additional Commissioner or Joint Director or Joint Commissioner in consequence of information in his possession, has reason to believe that ---

(a) any person to whom a summons under sub-section (1) of section 37 of the Indian Income-tax Act, 1922 (11 of 1922), or under sub-section (1) of Section 131 of the Income Tax Act, 1961, or a notice under sub-section (4) of section 22 of the Indian Income-tax Act, 1922 (11 of 1922), or under sub-section (1) of section 142 of the Income Tax Act, 1961 was issued to produce, or cause to be produced, any books of account or other documents has omitted or failed to produce, or cause to be produced, such books of account or other documents as required by such summons or notice, or etc. etc.

Sub-section (4): The authorised officer may, during the course of the search or seizure examine on oath any person who is found to be in possession or control of any books of account, documents, money, bullion, jewellery or other valuable article or thing and any statement made by such person during such examination may thereafter be used in evidence in any proceeding under the Indian Income-tax Act, 1922 (11 of 1922), or under this Act."

18. On going through Section 132 (of Income Tax Act, 1961), what we find is that if the authority specified therein has reason to believe that any person to whom a summons under sub-section (1) of section 37 of the Indian Income-tax Act, 1922 (11 of 1922), or under sub-section (1) of section 131 of the Income Tax Act, 1961, or a notice under sub-section (4) of section 22 of the Indian Income-tax Act, 1922 (11 of 1922), or under sub-section (1) of section 142 of the Income Tax Act, 1961 was issued to produce, or cause to be produced, any books of account or other documents has omitted or failed to produce, or cause to be produced, such books of account or other documents as required by such summons or notice etc. etc., can authorise the officers referred therein to enter and search any building etc. etc. Such authorised officer under sub-section (4) of Section 132 (of Income Tax Act, 1961) may during the course of search or seizure examine on oath any person who is found to be in possession or control of any books of account, document, money, bullion, jewellery or other valuable article or thing and any statement made by such person during such examination may thereafter be used in evidence in any proceeding under the Indian Income-tax Act, 1922 or under the Act 1961. Therefore, going by the said provision not only the books, documents etc. etc. that are unearthed during the course of search but a statement made by such person during such examination can also be used in evidence in any proceeding under the Income Tax Act, 1961. Thus viewing the provision in such manner, it is an admitted fact that the Managing Partner of the firms in question has given a voluntary statement to the Assessing Officer that there is a undisclosed income of Rs.2.75 Crores, which according to the learned counsel, was retracted by the Managing Partner subsequently. Thus it can be seen that even according to the assessee, there was a disclosure made by giving a statement during the course of search and therefore, the Assessing Officer, by virtue of the power conferred on him under section 153A (of Income Tax Act, 1961) was competent to issue notice under the said provision and require the assessee firms to furnish the returns as provided thereunder. Neither under section 132 (of Income Tax Act, 1961) or under section 153A (of Income Tax Act, 1961), the phraseology “incriminating” is used by the Parliament. Therefore, any material which was unearthed during search operations or any statement made during the course of search by the assessee is a valuable piece of evidence in order to invoke section 153A (of Income Tax Act, 1961).

19. In order to appreciate the provisions of Section 153A (of Income Tax Act, 1961) in a proper manner, it is appropriate to extract the said provision, which reads thus:

153A. [(1)] Notwithstanding anything contained in section 139 (of Income Tax Act, 1961), section 147 (of Income Tax Act, 1961), section 149 (of Income Tax Act, 1961), section 151 (of Income Tax Act, 1961) and section 153 (of Income Tax Act, 1961), in the case of the person where a search is initiated under section 132 (of Income Tax Act, 1961) or books of account, other documents or any assets are requisitioned under section 132A (of Income Tax Act, 1961) after the 31st day of May, 2003, the Assessing Officer shall--

(a) issue notice to such person requiring him to furnish within such period, as may be specified in the notice, in return of income in respect of each assessment year falling within six assessment years referred to in clause (b), in the prescribed form and verified in the prescribed manner and setting forth such other particulars as may be prescribed and the provisions of this Act shall, so far as may be, apply accordingly as if such return were a return required to be furnished under section 139 (of Income Tax Act, 1961);

(b) assess or reassess the total income of six assessment years immediately preceding the assessment year relevant to the previous year in which such search is conducted or requisition is made.

Provided that the Assessing Officer shall assess or reassess the total income in respect of each assessment year falling within such six assessment years:

Provided further that assessment or reassessment, if any, relating to any assessment year falling within the period of six assessment years referred to in this sub-section pending on the date of initiation of the search under section 132 (of Income Tax Act, 1961) or making of requisition under section 132A (of Income Tax Act, 1961), as the case may be, shall abate.

Provided also that the Central Government may by rules made by it and published in the Official Gazette (except in cases where any assessment or reassessment has abated under the second proviso), specify the class or classes of cases in which the Assessing Officer shall not be required to issue notice for assessing or reassessing the total income for six assessment years immediately preceding the assessment year relevant to the previous year in which search is conducted or requisition is made.

[(2)] If any proceeding initiated or any order of assessment or reassessment made under sub- section (1) has been annulled in appeal or any other legal proceeding, then, notwithstanding anything contained in sub-section (1) or section 153 (of Income Tax Act, 1961), the assessment or reassessment relating to any assessment year which has abated under the second proviso to sub-section (1), shall stand revived with effect from the date of receipt of the order of such annulment by the Commissioner. Provided that such revival shall cease to have effect, if such order of annulment is set aside. Explanation.-- For the removal of doubts, it is hereby declared that.--

(i) save as otherwise provided in this section, section 153B (of Income Tax Act, 1961) and section 153C (of Income Tax Act, 1961), all other provisions of this Act shall apply to the assessment made under this section.

(ii) in an assessment or reassessment made in respect of an assessment year under this section, the tax shall be chargeable at the rate or rates as applicable to such assessment year." 20. On a plain reading of Section 153A (of Income Tax Act, 1961), it is clear that once search is initiated under Section 132 (of Income Tax Act, 1961) or a requisition is made under Section 132A (of Income Tax Act, 1961) after the 31st day of May 2003, the Assessing Officer is empowered to issue notice to such person requiring him to furnish return of income in respect of each assessment year following within six assessment years referred to in clause (b). It further treats the returns so filed as if such return were a return required to be furnished under Section 139 (of Income Tax Act, 1961). So that on a reading of Section 153A(1) (of Income Tax Act, 1961) it is categoric and clear that once a notice is issued and the Assessing Officer has required the assessee to furnish return for a period of six assessment years as contemplated under clause (b) then the assessee has to furnish all details with respect to each assessment year since the same is treated as a return filed under section 139 (of Income Tax Act, 1961). It is true that as per the first proviso, the Assessing Officer is bound to assess or reassess the total income with respect to each assessment year following the six assessment years specified in sub-clauses (a) and (b) of Section 153A (of Income Tax Act, 1961). However, even if no documents are unearthed or any statement made by the assessee during the course of search under section 132 (of Income Tax Act, 1961) and no materials are received for the aforespecified period of six years, the assessee is bound to file a return, is the scheme of the provision. Even though the second proviso to Section 153A (of Income Tax Act, 1961) speaks of abatement of assessment or reassessment pending on the date of the initiation of search within the period of six assessment years specified under the provision that will also not absolve the assessee from his liability to submit returns as provided under Section 153A(1)(a) (of Income Tax Act, 1961). This being the scheme of the provisions of the Act, the Appellate Tribunal ought to have considered the issue with specific reference to the facts involved in the case and as provided under Section 153A (of Income Tax Act, 1961).

21. However, we find that the Tribunal without appreciating the facts and circumstances has proceeded purely on the basis that the cases at hand were covered under the Special Bench decision in All Cargo Logistics Ltd. (supra). In our view the course adopted by the Tribunal was not the proper one to decide the question with regard to the sustainability of the order passed by the First Appellate Authority. Therefore, we are of the considered opinion that the Tribunal has not adopted the right method to decide the issue with regard to the question framed in these appeals and therefore, it is only necessary to remand the matter to the Tribunal for fresh consideration.

22. Therefore, we set aside the order passed by the Tribunal in the above appeals and remand the cases to the Tribunal to re-consider the question raised in these appeals by taking into account the principles laid down in the judgement cited by the Revenue as well as the assessee or any other principles of law laid down by competent courts of law and take a decision on merits in accordance with law. The question thus framed is answered in favour of revenue to the extent indicated above. However we make it clear that the common question with regard to the power of the Appellate Authority with respect to receipt of evidence in appeal and its application, concluded by the Tribunal in 84 cases and upheld by this court, will remain undisturbed.

The appeals are disposed of accordingly.

Sd/-

ANTONY DOMINIC

JUDGE

Sd/-

SHAJI P. CHALY

JUDGE

×

Similar Ripples

Questions

Court Clarifies Scope of Section 153A (of Income Tax Act, 1961) in Income Tax Searches

Write your CommentSimilar Posts

Generic

- Reportdata/2979.pdf