Court Condones Delay in Tax Return Filing, Orders Refund Consideration

Full News

Court Condones Delay in Tax Return Filing, Orders Refund Consideration

Court Condones Delay in Tax Return Filing, Orders Refund Consideration

This case involves Artist Tree Pvt. Ltd. (the petitioner) challenging a Central Board of Direct Taxes (CBDT) order that refused to condone a delay in filing their income tax return for the 1997-1998 assessment year. The High Court set aside the CBDT's order, condoned the delay, and directed the Income Tax Officer to consider the return and examine the refund claim on its merits.

Get the full picture - access the original judgement of the court order here

Case Name:

Artist Tree Pvt. Ltd. vs. Central Board of Direct Taxes and Others (High Court of Bombay)

Writ Petition No. 3087 of 2006

Date: 3rd December 2016

Key Takeaways:

1. Courts should adopt a liberal approach in matters of condonation of delay.

2. "Genuine hardship" should be interpreted liberally, especially for delay condonation applications.

3. The CBDT has the power to condone delays under Section 119(2)(b) (of Income Tax Act, 1961).

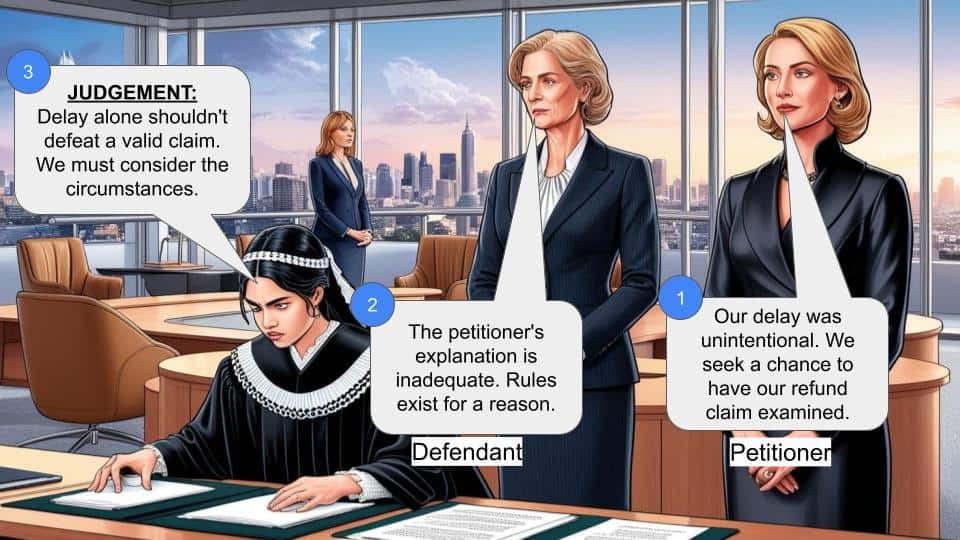

4. Delay alone shouldn't defeat a legitimate refund claim if a reasonable explanation is provided.

Issue:

Should the delay in filing the income tax return for the 1997-1998 assessment year be condoned, allowing the petitioner's refund claim to be considered on its merits?

Facts:

1. Artist Tree Pvt. Ltd. filed its income tax return for 1997-1998 on September 14, 1999, about 22 months late.

2. The company claimed a refund of Rs.6,34,929.

3. The company's office had shifted, allegedly causing TDS certificates to be misplaced.

4. CBDT rejected the company's application for condonation of delay on May 16, 2006.

5. The company had generally filed returns within permissible time limits for other years.

Arguments:

Petitioner (Artist Tree Pvt. Ltd.):

- The delay was due to misplaced TDS certificates during office relocation.

- They have no objection to scrutiny assessment for determining the refund.

- A liberal approach should be adopted in condonation matters.

Revenue (CBDT):

- The petitioner is a "habitual late filer" trying to avoid scrutiny.

- There's no proper explanation for the two-year delay in filing the return.

- No documentary evidence was provided to support the claim of misplaced TDS certificates.

Key Legal Precedents:

1. B.M. Malani vs. Commissioner of Income Tax

2. R. Seshammal vs. Income Tax Officer & anr

3. Sitaldas K. Motwani vs. Director General of Income Tax & anr

4. Bombay Mercantile Cooperative Bank Limited vs. Central Board of Direct Taxes and ors

These cases emphasize the need for a liberal approach in condonation matters and interpreting "genuine hardship" under Section 119(2)(b) (of Income Tax Act, 1961).

Judgement:

The High Court set aside the CBDT's order, finding that:

1. The CBDT adopted an unduly restrictive approach.

2. The petitioner provided an acceptable explanation and demonstrated genuine hardship.

3. The delay wasn't deliberate or due to culpable negligence.

4. The court condoned the delay and directed the Income Tax Officer to consider the return and examine the refund claim on merits within six months.

FAQs:

1. Q: Does condonation of delay automatically grant the refund?

A: No, it only allows the tax authorities to consider the return and examine the refund claim on its merits.

2. Q: What is Section 119(2)(b) (of Income Tax Act, 1961)?

A: It gives CBDT the power to condone delays in filing tax returns or claims when there's genuine hardship.

3. Q: Why did the court criticize CBDT's approach?

A: The court found CBDT's approach unduly restrictive and not in line with the principle of adopting a liberal stance in condonation matters.

4. Q: What does this judgment mean for other taxpayers?

A: It reinforces the principle that courts should adopt a liberal approach in delay condonation matters, especially when there's a reasonable explanation and no deliberate negligence.

5. Q: Does this judgment guarantee the petitioner will get the refund?

A: No, it only ensures that their return will be considered. The tax authorities will still scrutinize the claim and decide based on merits.

1] This petition is directed against the order dated 16 May 2006 passed under Section 119(2)(b) (of Income Tax Act, 1961) (“the said Act”) by the Central Board of Direct Taxes (CBDT). By the impugned order dated 16 May 2006 the petitioner's application dated 7 April 2002 for condonation of delay in filing Return of Income for the Assessment Year 19971998 was rejected, resulting in the claim for refund of Rs.6,34,929/ not being examined on merits.

2] For the Assessment Year 19971998, the petitioner, which is engaged in the business of dealing in Artifacts and finances, filed a Return of Income on 14 September 1999, declaring income of Rs.1,46,000/ and claiming refund of Rs.6,34,929/. The due date for filing the Return of Income was 30 November 1997, but the return was filed on 14 September 1999, i.e., after delay of about 22 months.

3] As there was a delay in filing the Return of Income for Assessment Year 19971998 beyond the period specified under Section 139(1) (of Income Tax Act, 1961) & (4) of the said Act, the Assessing Officer did not act upon the same. On 7 April 2002 the petitioner approached the CBDT under Section 119(2)(b) of the Income Tax Act, 1961 and sought for condonation of delay in filing the Return of Income for the Assessment Year 19971998. In the application dated 7 April 2002, the petitioner stated that at the relevant time, the office of the petitioner company was shifted and certain records including TDS Certificates got misplaced/mislaid and considerable time was spent to retrieve the same resulting in the delay.

4] The CBDT by its communication dated 7 February 2006 required the petitioner to show cause as to why the application dated 7 April 2002 seeking condonation of delay be not rejected upon the following grounds:

(a) That the petitioner was a 'habitual late filer', with a view to avoid scrutiny/enquiry; and

(b) There do not appear to be any genuine reasons for the late filing of the Return of Income.

5] The petitioner through its Chartered Accountant submitted a response dated 21 March 2006 to the notice dated 7 February 2006 elaborating upon the circumstances in which the delay was occasioned in filing of return for the Assessment Year 19971998. In the response, reference was made, inter alia, to CBDT Circulars as well as the decision of this Court in case of Bharatiya Engineering Corporation Private Limited vs. R.G. Deshpande1 , urging that a liberal approach be adopted in matters of condonation of delay.

6] The CBDT, by impugned order dated 16 May 2006 has however, declined to condone the delay, inter alia, on the following grounds:

(a) That audited accounts were prepared by 14 September 1997. However, there is no proper explanation as to why the returns came to be filed only on 14 September 1999. Further there is no explanation as to why the application seeking condonation of delay came to be filed only on 17 April 2002. All this, leads to the inference that delayed return was only to avoid scrutiny;

(b) That no documentary evidence in support of misplacement of TDS Certificate by postal authorities on account of change in address of the petitioner's company or evidencing delay in receipt of duplicate TDS Certificate was produced.

7] Ms Vissanji, learned counsel for the petitioner, submitted that in terms of Section139(1) (of Income Tax Act, 1961), 139(9), (c)(i) of the said Act read with Income Tax Rules, 1962, as in force at the relevant time, a Return of Income is required to be accompanied, inter alia, with proof of the tax, if any, claimed to have been deducted at source. The registered office of the petitioner company, was shifted from Somerset House, Warden Road to Poornima, B.G. Kher Marg, which is evident from change of situation of registered office notice dated 16 June 1997. On account of shifting of office, coupled with the fact that the petitioner company does not have any administrative staff, the TDS Certificate got misplaced/mislaid and considerable time was spent to retrieve the same. Ms Vissanji further submitted that the petitioner company from the date of its incorporation, i.e., 15 February 1995 had always filed its Returns of Income within the time permissible under Section139(4) (of Income Tax Act, 1961) of the said Act. Except for the Assessment Year 19961997, returns filed by the petitioner company were accepted, without any scrutiny. Even for the Assessment Year 19961997, the scrutiny assessment order made on 15 February 1998 would bear out that the returned income was substantially accepted, with some minor dis- allowances. In such circumstances, there was neither any material nor any justification to style the petitioner as an 'habitual late filer'. Besides, the petitioner by its communication dated 23 March 2006 addressed to the CBDT had made it clear that it has no objection whatsoever to scrutiny assessment for the purpose of determining refund and further even the instructions issued by the CBDT contemplated scrutiny in respect of delayed claims of refund. In such circumstances, the charge that the delay in filing of Return was to avoid scrutiny, is completely baseless. Ms Vissanji, relying upon the undermentioned decisions, submitted that a liberal approach is to be adopted in matters of condonation of delay, rather than a pedantic or hyper technical approach, which would defeat the legitimate claims of tax payers.

(1) B.M. Malani vs. Commissioner of Income Tax2 ;

(2) R. Seshammal vs. Income Tax Officer & anr3 ;

(3) Sitaldas K. Motwani vs. Director General of Income Tax & anr.4 and

(4) Bombay Mercantile Cooperative Bank Limited vs. Central Board of Direct Taxes and ors5 .

8] Mr. Pinto, learned counsel for the revenue submitted that the impugned order dated 16 May 2006 is well reasoned and did not warrant any interference. The accounts for the Assessment Year 19971998 had been duly audited by 14 September 1997. In such circumstances, there is no explanation for delay of almost two years in filing the Return of Income. The petitioner could have always filed the return within time, and thereafter invoked the provisions of Section 154 of the Income Tax Act, 1961 to rectify the order passed by furnishing TDS Certificates, if indeed the same had been misplaced or mislaid. The shifting of office, as per the documentary evidence produced by the petitioner itself took place on 16 June 1997. The so called misplacement of documents, on account of shifting did not prove any hindrance in the matter of audit of accounts which was completed by 14 September 1997. There is no material produced by the petitioner with regard to claim of misplacement of TDS Certificates or the efforts made by the petitioner to retrieve the same, including by way of obtaining duplicates. In such circumstances, the CBDT was justified in drawing the inference that the delay in filing of returns was to avoid scrutiny. Mr. Pinto submitted that the petitioner had failed to make out any case of genuine hardship and there was no explanation for the delay of almost two years in filing the Return of Income. Besides it is submitted that there is no explanation for a delay of about two years in filing an application for condonation of delay with the CBDT from 14 September 1999, when the Return of Income was filed. In such circumstances, the impugned order ought not to be interfered with by this Court in exercise of its extra ordinary jurisdiction under Article 226 of the Constitution of India.

9] The rival contentions, which now fall for our determination have to be examined in the context of Section 119(2)(b) of the Income Tax Act, 1961 which reads as under:

“Section 119(2)(b) (of Income Tax Act, 1961) The Board may, if it considers it desirable or expedient so to do for avoiding genuine hardship in any case or class of cases, by general or special order, authorize [any incometax authority, not being a Commissioner (Appeals)] to admit an application or claim for any exemption, deduction, refund or any other relief under this Act after the expiry of the period specified by or under this Act for making such application or claim and deal with the same on merits in accordance with law;”

10] The CBDT, in terms of Section 119(2)(b) of the Income Tax Act, 1961 is vested with powers to admit an application or claim for any exemption, deduction, refund or any other relief under the said Act after the expiry of period specified by or under said Act for making such application or claim and deal with the same on merits in accordance with law, where the CBDT considers it desirable or expedient so to do for avoiding genuine hardship in any case or class of cases. From time to time, the CBDT has been issuing instructions to effectuate exercise of powers under Section 119(2)(b) of the Income Tax Act, 1961, which includes inter alia instruction No.12/2003 dated 30 October 2003. Instruction No.12/2003, inter alia, provides that cases where delayed claims of refunds are being considered would be taken up for scrutiny. This as to ensure that income declared and refund claimed are correct and genuine and also that the case is of genuine hardship on merits. Support for the above is also found in similar instruction No.13/2006, inter alia, provides that no interest will be admissible on the belated refund claims and for ascertaining the correctness of the claim could direct the Assessing Officer to examine the same albeit issued after the impugned order.

11] The expression 'genuine hardship' came up for consideration of the Supreme Court in case of B.M. Malani (supra), wherein, by reference to New Collins Concise English Dictionary, the Supreme Court accepted the position that 'genuine' means not fake or counterfeit, real, not pretending (not bogus or merely a ruse). Further, a genuine hardship would, inter alia, mean a genuine difficulty. The ingredients of genuine hardship must be determined keeping in view the dictionary meaning thereof and legal conspectus attending thereto. For the said purpose another well known principle, namely, that a person cannot take advantage of his own wrong, may also have to be borne in mind. Compulsion to pay any unjust dues per se would cause hardship. But a question as to whether the default in payment of the amount was due to circumstances beyond the control of assessee, also bears consideration.

12] In case of R. Seshammal (supra), the Madras High Court was pleased to observe as under:

“This is hardly the manner in which the State is expected to deal with the citizens, who in their anxiety to comply with all the requirements of the Act pay monies as advance tax to the State, even though the monies were not actually required to be paid by them and thereafter seek refund of the monies so paid by mistake after the proceedings under the Act are dropped by the authorities concerned. The State is not entitled to plead the hypertechnical plea of limitation in such a situation to avoid return of the amounts. Section 119 (of Income Tax Act, 1961) vests ample power in the Board to render justice in such a situation. The Board has acted arbitrarily in rejecting the petitioner's request for refund”.

(emphasis supplied)

13] In case of Sitaldas Motwani (supra), this Court has held that the expression 'genuine hardship' used in Section 119(2)(b) of the Income Tax Act, 1961 should be construed liberally, particularly in matters of entertaining of applications seeking condonation of delay. This Court was pleased to observe as under:

“The phrase “genuine hardship” used in section 119(2)(b) (of Income Tax Act, 1961) should have been construed liberally even when the petitioner has complied with all the conditions mentioned in Circular dated October 12,1993. The Legislature has conferred the power to condone delay to enable the authorities to do substantive justice to the parties by disposing of the matters on the merits. The expression “genuine” has received a liberal meaning in view of the law laid down by the apex court referred to hereinabove and while considering this aspect, the authorities are expected to bear in mind that ordinarily the applicant, applying for condonation of delay does not stand to benefit by lodging its claim late. Refusing to condone delay can result in a meritorious matter being thrown out at the very threshold an cause of justice being defeated. As against this, when delay is condoned the highest that can happen is that a cause would be decided on the merits after hearing the parties. When substantial justice and technical considerations are pitted against each other, the cause of substantial justice deserves to be preferred for the other side cannot claim to have a vested right in injustice being done because of a non- deliberate delay. There is no presumption that delay is occasioned deliberately, or on account of culpable negligence, or on account of mala fides. A litigant does not stand to benefit by resorting to delay. In fact he runs a serious risk. The approach of the authorities should be justice oriented so as to advance the cause of justice. If refund is legitimately due to the applicant, mere delay should not defeat the claim for refund.”

(emphasis supplied)

14] In case of Bombay Mercantile Cooperative Bank Limited (supra), this Court again observed that it is well settled that in matters of condonation of delay highly pedantic approach should be eschewed and a justiceoriented should be adopted. It also observed that a party should not be made to suffer on account of technicalities.

15] Applying the aforesaid principles to the facts and circumstances of the present case, we are of the opinion, that the CBDT, in passing the impugned order, has adopted an unduly technical or pedantic approach.

16] The petitioner, at ExhibitP to the petition has furnished the following details with regard to filing of returns from the date of its incorporation, i.e., 15 February 1995.

M/S.ARTIST TREE PVT. LTD.

DETAILS OF RETURNS FILED

DATE OF INCORPORATION : 15.02.1995 ASST.YEAR DATE OF FILING INTIMATION ISSUED 199596 31.03.97 15.05.97 SERVED ON 01.12.2000 199697 17.09.97 06.10.97 SERVED ON 25.03.1998 (SCRUTINY ASSESSMENT ORDER ALSO PASSED ON 15.02.97) 199798 14.09.99 NO INTIMATION ISSUED 199899 14.09.99 INTIMATION ISSUED ON 20.01.2000 SERVED ON 22.06.2000 199900 13.03.00 NOT INTIMATION RECEIVED ONLY ITNS150A RECD. ON 18.12.02. 200001 29.03.01 NO INTIMATION RECEIVED 200102 08.04.02 NO INTIMATION RECEIVED

17] From the aforesaid, though it may be true that the returns may not have been filed within the period specified under Section 139(1) of the Income Tax Act, 1961, nevertheless, the returns came to be filed in respect of all assessment years (except Assessment Year 19971998) within the time allowable under Section 139(4) of the Income Tax Act, 1961. Further in all cases, except for the Assessment Year 19961997, the Return of Income came to be accepted. For the Assessment Year 19961997, the petitioner's case was taken up for scrutiny, however, the return was substantially accepted with only some minor disallowances. In light of such facts, the CBDT was obviously not right in condemning the petitioner as 'habitual late filer'.

18] Further, there is no material to sustain the inference that late filing of returns was to avoid scrutiny. The petitioner, by its communication dated 23 March 2006, had already made it clear that it had no objection to scrutiny assessment for the purposes of determining refund for the Assessment Year 19971998. The CBDT instructions, to which reference has been made earlier also provide that cases where delayed claims for refunds are being considered would be taken up for scrutiny. Besides, even the provisions of Section 119(2)(b) of the Income Tax Act, 1961 make it clear that the CBDT can authorise any Income Tax Authorities to admit an application or claim for any exemption, deduction, refund or any other relief under the said Act after the expiry of period specified by or under the said Act for making such application or claim and to deal with the same on merits in accordance with law. The expression 'deal with the same on merits in accordance with law' makes it clear that the CBDT, even where it authorises an ITO to admit an application or claim made belatedly, would obviously direct its consideration on merits and in accordance with law. In such circumstances, the contention of Mr.Pinto, learned counsel for the revenue that the effect of an order condoning delay in filing the returns, leave the ITO with no choice but to grant the refund as claimed, has no substance. Obviously, it would be well within the jurisdiction of such authority to deal with the claim on merits and in accordance with law. This Court in case of Sitaldas (supra) has explained the position in the following words:

“Whether the refund claim is correct and genuine, the authority must satisfy itself that the applicant has a prima facie correct and genuine claim, does not mean that the authority should examine the merits of the refund claim closely and come to a conclusion that the applicant's claim is bound to succeed. This would amount to prejudging the case on the merits. All that the authority has to see is that on the face of it the person applying for refund after condonation of delay has a case which needs consideration and which is not bound to fail by virtue of some apparent defect. At this stage, the authority is not expected to go deep into the niceties of law. While determining whether a refund claim is correct and genuine, the relevant consideration is whether on the evidence led, it was possible to arrive at the conclusion in question and not whether that was the only conclusion which could be arrived at on that evidence.”

19] The circumstance that the accounts were duly audited way back on 14 September 1997, is not a circumstance that can be held against the petitioner. This circumstance, on the contrary adds force to the explanation furnished by the petitioner that the delay in filing of returns was only on account of misplacement or the TDS Certificates, which the petitioner was advised, has to be necessarily filed alongwith the Return of Income in view of the provisions contained in Section 139 of the Income Tax Act, 1961 read alongwith Income Tax Rules, 1962 and in particular the report in the prescribed Forms of Return of Income then in vogue which required an assessee to attach the TDS Certificates for the refund being claimed. The explanation furnished is that on account of shifting of registered office, it is possible that TDS Certificates which may have been addressed to the earlier office, got misplaced. There is nothing counterfeit or bogus in the explanation offered. It cannot be said that the petitioner has obtained any undue advantage out of delay in filing of Income Tax Returns. As observed in case of Sitaldas (supra), there is no presumption that delay is occasioned deliberately or on account of culpable negligence or on account of mala fides. It cannot be said that in this case the petitioner has benefited by resorting to delay. In any case when substantial justice and technical consideration are pitted against each other, the cause of substantial justice deserves to prevail without in any manner doing violence to the language of the Act.

20] Mr. Pinto submitted that inordinate delay of two years in filing the Return of Income lands the petitioner in the arena of laches and therefore, no relief should be granted to the petitioner. The principle on which the relief is denied to the party on grounds of delay or laches is that the rights which have accrued to others by reason of the delay in filing the petition should not be allowed to be disturbed unless there is a reasonable explanation for the delay. The real test to determine delay in such cases is that the petitioner should come to the Court before a parallel right is created and that the lapse of time is not attributable to any laches or negligence. The test is not to physical running of time6 . This does not mean or imply that the applicant seeking condonation of delay is absolved of the requirement to establish genuine hardship and sufficient cause. Similarly, the length of delay is not invariably the crucial factor. What is really important is the acceptability of the explanation offered. In every case of delay, there may be some lapse on the part of the party concerned. That by itself is not ordinarily sufficient to turn down the plea or to shut the doors against him. If the explanation offered does not smack of mala fides or it is not put forth as a part of dilatory strategy, the Court is expected to show utmost consideration to the applicant, particularly because refusal to condone delay would result in foreclosing an applicant from even putting forth his cause. Once the Court accepts the explanation as sufficient, it is the result of positive exercise of discretion and normally the superior Court should not disturb such exercise, unless the same was on wholly untenable grounds or arbitrary or perverse. But it is a different matter when Court or Authority of the first instance refuses to condone the delay. In such a case, the superior Court would be free to consider the cause shown for the delay afresh and come to its own finding7 . 6 M/s.Dehri Rohtas Light Railway Company Ltd. vs. District Bord, Bhojpur & ors – (1992) 2 SCC 598 7 N.Balakrishnan vs. M. Krishnamurthy – (1998) 7 SCC 123

21] We find that the impugned order dated 16 May 2006 of the CBDT also seeks to reject the the application for condonation of delay on account of delay from the date of filing the Return of Income, i.e., 14 September 1999 upto 30 April 2002. This was not the ground mentioned in notice dated 7 February 2006 given to the petitioner by the CBDT for rejecting the application for condonation of delay. Thus the petitioner had no occasion to meet the same. It appears to be an afterthought. However, as pointed out in paragraph 20 hereinabove, the delay in filing of an application if not coupled with some rights being created in favour of others, should not by itself lead to rejection of the application. This is ofcourse upon the Court being satisfied that there were good and sufficient reasons for the delay on the part of the applicant.

22] Mr. Pinto then submitted that the decision in case of Seshammal (supra) is distinguishable, inasmuch as the Madras High Court, in the said case was concerned with a widow seeking refund of a paltry amount of Rs.43,808/. Whereas, the present case concerns a company dealing in Artifacts and finances, which has the benefit of services of professionals and auditors. This is no manner to distinguish a decision. Seshammal (supra) is basically an authority for the proposition that in matters of condonation of delay, a liberal approach needs to be adopted and further the State should not ordinarily plead hyper technical plea of limitation to avoid return of amounts due to an assessee. This Court, in case of Sitaldas (supra) has understood Seshammal (supra) accordingly.

23] In light of the aforesaid discussion, we are of the opinion that an acceptable explanation was offered by the petitioner and a case of genuine hardship was made out. The refusal by the CBDT to condone the delay was a result of adoption of an unduly restrictive approach. The CBDT appears to have proceeded on the basis that the delay was deliberate, when from explanation offered by the petitioner, it is clear that the delay was neither deliberate, nor on account of culpable negligence or any mala fides. Therefore, the impugned order dated 16 May 2006 made by the CBDT refusing to condone the delay in filing the Return of Income for the Assessment Year 19971998 is liable to be set aside. Consistent with the provisions of Section 119(2)(b) of the Income Tax Act, 1961, the concerned I.T.O. or the Assessing Officer would have to consider the Return of Income and deal with the same on merits and in accordance with law.

24] We make it clear that we have not examined the issue of whether the petitioner is indeed entitled to any refund or not, as in our opinion that is a matter for the concerned I.T.O. or the Assessing Officer to decide in accordance with law after subjecting the Return of Income to scrutiny assessments.

25] Accordingly, the impugned order dated 16 May 2006 made by the CBDT is set aside. The delay in filing the Return of Income for the Assessment Year 19971998 is condoned and Return of Income is directed to be admitted for consideration. The jurisdictional I.T.O./Assessing Officer is directed to scrutinize the Return of Income and examine the claim for refund on merits in accordance with law and grant refund, if the petitioner is entitled to the same, in accordance with law within a period of six months from today.

26] Rule is made absolute to the aforesaid extent. There shall be no order as to costs.

(M.S.SONAK, J.) (M. S. SANKLECHA, J.)

×

Similar Ripples

Questions

Court Condones Delay in Tax Return Filing, Orders Refund Consideration

Write your CommentSimilar Posts

Generic

- Reportdata/4275.pdf