Full News

Court Denies Tax Deduction for Unproven Sub-Agent Payments

Court Denies Tax Deduction for Unproven Sub-Agent Payments

This case involves Raj Kumar Wadhwa (the appellant) challenging an order by the Income Tax Appellate Tribunal. The Tribunal had dismissed the appellant's appeal and confirmed the decision of the Assessing Officer to disallow a claimed deduction for commission payments to sub-agents. The court upheld the Tribunal's decision, finding that the appellant failed to prove the legitimacy of these payments.

Case Name**: RAJ KUMAR WADHWA VS COMMISSIONER OF INCOME TAX

**Key Takeaways**:

1. The burden of proof lies on the assessee to establish the legitimacy of claimed business expenses.

2. Mere existence of bills and payments doesn't automatically entitle an assessee to claim deductions.

3. Failure to provide detailed evidence of services rendered can lead to disallowance of claimed deductions.

4. The court will consider the totality of facts and circumstances when evaluating the validity of claimed expenses.

**Issue**:

Can an assessee claim a deduction under Section 37(1) (of Income Tax Act, 1961) for payments made to sub-agents when they fail to provide sufficient evidence of the services rendered?

**Facts**:

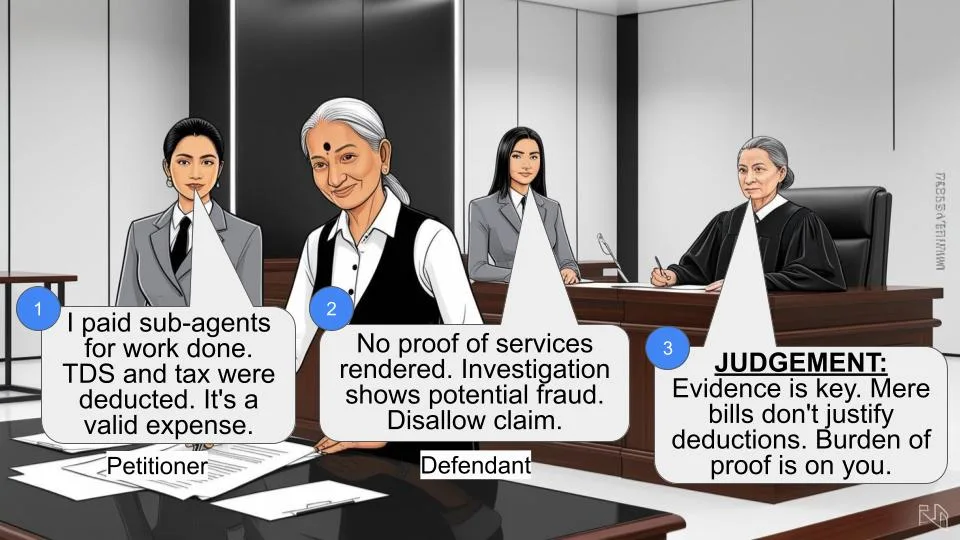

1. Raj Kumar Wadhwa is a cement stockist and sales promoter for M/s J.K. Cement Works.

2. He received a commission of Rs. 55.68 lacs, out of which he claimed to have paid Rs. 41.14 lac as commission to sub-agents for liaison work.

3. The Assessing Officer disallowed this commission payment after a detailed investigation.

4. The appellant appealed to the Commissioner of Income Tax (Appeals), who partially allowed the appeal.

5. Both the appellant and the revenue filed separate appeals to the Income Tax Appellate Tribunal.

6. The Tribunal allowed the revenue's appeal, set aside the CIT (Appeals) order, and rejected the assessee's appeal.

**Arguments**:

Appellant's arguments:

1. The impugned orders would lead to double taxation as similar amounts have already been charged to the recipient assessee.

2. Payments were made out of commercial expediency and business necessity.

3. Payments were made to sub-agents after deducting TDS and service tax.

Revenue's arguments:

1. The appellant failed to establish the bona fides of payments made to sub-agents.

2. The appellant couldn't provide exact details of services rendered, including quantitative details, date-wise and party-wise information.

3. The investigation and statements recorded from the alleged sub-agents didn't justify the commission payments.

**Key Legal Precedents**:

1. Emson Tools Manufacturing Corporation Ltd. Vs. CIT (specific details not provided in the context)

2. Section 37(1) (of Income Tax Act, 1961), which deals with deductions for business expenses.

**Judgement**:

1. The court dismissed the appellant's appeal, upholding the Income Tax Appellate Tribunal's decision.

2. The court found that the appellant failed to prove the bona fides of his claim regarding commission payments.

3. The Tribunal's finding that the entire list of sub-agents was potentially fraudulent was upheld.

4. The court emphasized that merely raising bills and making payments doesn't automatically entitle an assessee to claim deductions.

5. The onus is on the assessee to establish that expenditure was incurred wholly and exclusively for business purposes.

**FAQs**:

Q1: Why was the appellant's claim for deduction rejected?

A1: The claim was rejected because the appellant failed to provide sufficient evidence of the services rendered by the sub-agents and couldn't justify the nature of the commission payments.

Q2: What evidence did the court expect from the appellant?

A2: The court expected detailed evidence including the exact nature of services rendered, quantitative details of services provided date-wise, and party-wise details of supply.

Q3: Does paying TDS and service tax on payments automatically make them deductible?

A3: No, merely deducting TDS and service tax doesn't automatically make payments deductible. The assessee still needs to prove that the expenses were incurred wholly and exclusively for business purposes.

Q4: Can an expense allowed in a previous year be automatically allowed in subsequent years?

A4: No, the acceptance of an expense in a previous year doesn't automatically establish its validity for subsequent years, especially if there's new evidence or investigation results.

Q5: What's the key lesson for businesses from this judgment?

A5: Businesses should maintain detailed records of all expenses, especially payments to sub-agents or contractors, including specific details of services rendered to justify deductions claimed in tax returns.

The appellant challenges order dated 23.2.2010 passed by the Income Tax Appellate Tribunal, Chandigarh Bench-B, Chandigarh, dismissing his appeal thereby confirming order dated 30.4.2009 passed by the CIT (Appeals) and order dated 22.8.2007 passed by the Assessing Officer.

The appellant-assessee is a cement stockiest and sales promoter for M/s J.K.Cement Works. The assessee received commission of Rs.55.68 lacs out of which, he claimed that he had paid Rs.41.14 lac as commission for liaison work to sub-agents. After a detailed appraisal of the entire record, including statements etc., the Assessing Officer disallowed the commission. Aggrieved by this order, the appellant filed an appeal. The Commissioner of Income Tax (Appeals) allowed the appeal in part. The appellant and the revenue filed their separate appeals. The Income Tax Appellate Tribunal, vide impugned order dated 23.2.2010, allowed the appeal, filed by the revenue, set aside the order passed by the CIT (Appeals) and rejected the appeal filed by the assessee.

Counsel for the appellant submits that the impugned orders are illegal as it would lead to double taxation as similar amounts have already been charged in arriving at chargeable income of the recipient assessee. It is further argued that as payments made by the assessee emerge out of commercial expediency and business exigency, the additions made are erroneous as it could not be assessed as chargeable income in the hands of the appellant. We have heard counsel for the appellant and perused the impugned orders. The substantial question of law framed by the appellant reads as follows:-

“ Whether under facts and circumstances of the case, while arriving at the Chargeable Income u/s 29 (of Income Tax Act, 1961), the deduction claimed u/s 37(1) (of Income Tax Act, 1961), can be charged to tax in the hands of payer in spite of the same having been considered as a “Chargeable Income” in hands of the payee?”

The question of law has been raised in the context of a plea that payments made by the assessee emerged out of commercial expediency and business exigency and payment was made to sub-agents, after deducting TDS and service tax. The submission, in our considered opinion, is entirely misconceived as the Income Tax Appellate Tribunal has held, as a matter of fact, that the appellant was unable to establish the bona fides of payments made to sub-agents, in essence, raising an inference that the entire list of sub-agents was a fraud perpetuated with the sole object of evading payment of tax. The Income tax Appellate Tribunal as well as the Assessing Officer have held that the appellant has failed to bring on record the exact nature of services rendered with quantitative details of services provided date-wise, party-wise details of supply etc. and has only furnished consolidated bills at the end of the year.

A perusal of the order passed by the Assessing Officer reveals a detailed analysis of the record and statements recorded before him, before recording his conclusions, which have been affirmed by the Income Tax Appellate Tribunal. A relevant extract from the order passed by the Tribunal reads as follows:

“ ...The basis for disallowing the commission is the investigation carried out by the Assessing Officer and the statement recorded of the various persons to whom the aforesaid commission is claimed to have been paid. In the said statement recorded, none of the parties have been able to justifiably explain the nature and services offered by them entitling them to the receipt of the commission. Even the details of services rendered party-wise on which commission was due could not be forwarded by the said parties. In the entirety of facts and circumstances of the case, where the assessee has failed to explain with evidence the nature of services being rendered by the sub agents, disentitles it to the claim of deduction on account of the service charges. Merely because certain bills have been raised and payments against the same have been released by the assessee, does not entitle the assessee to claim of deduction on account of said expenditure, in the absence of the assessee establishing that the said expenditure had been laid down wholly and exclusively for the purpose of business of the assessee. The said parties had failed to bring on record the exact nature of services rendered and even the quantitative details of the services vis-a-vis, date wise and party wise details to whom supplies were made on behalf of the assessee were not furnished, except for raising a consolidated bill at the end of the year. The acceptance of allowability of the said expenditure in the succeeding year vide intimation issued u/s 143(1) (of Income Tax Act, 1961) as against the evidence and material collected by the Assessing Officer during the year, does not establish the claim of the assessee in respect of the allowability of the said expenditure. Further, we find that the alleged agreement with M/s PEW was entered into by the assessee on 8.4.2005 whereas the assessee was appointed as service agent by M/s SSTPL vide appointment letter dated 18.5.2005. Even the said appointment letter debarred the assessee from assigning the agreement with M/s SSTPL in favour of any other party. In the totality of facts and circumstances, we find no merit in the order of the CIT (A) in allowing the claim of the assessee on the basis of existence of agreement with one of the sub agents and admission of receipts of payments by the parties.”

Upon further consideration of the matter, the Income Tax Appellate Tribunal held as follows:-

“ ...The onus is upon the assessee to establish that it had incurred a particular expenditure for the purpose of carrying on of its business. The second limb of Section 37 (of Income Tax Act, 1961), of incurring the expenditure for the purpose of business, have not been satisfactorily established by the assessee. In view of the evidence collected by the Assessing Officer and the statement recorded of the sub agents, we find no merit in the claim of the assessee in respect of the liaison commission paid by it, which in any case is debarred from vis-a-vis terms of agreement entered between the assessee and its Principal M/s STPL. The said expenditure being allowed in the earlier year, under order passed u/s 143(3) (of Income Tax Act, 1961) does not establish the case of the assessee for the year under consideration as the parties to whom commission was paid for assessment year 2004-05, are completely different and in respect of the parties in assessment year 2003-04 though there was two common parties, but the assessee has failed to furnish on record the evidence in respect of the services rendered in financial year 2003-04 by the said parties for which commission was allowed. We find support from the ratio laid down in Emson Tools Manufacturing Corporation Ltd. Vs. CIT (supra). Accordingly, reversing the order of CIT(A), we confirm the order of Assessing Officer in making an addition of Rs.41,14,518/-. The grounds of appeal raised by the Revenue are thus allowed.”

We find no reason to hold that the Income Tax Appellate Tribunal has committed any error or that the question of law, as framed, arises for consideration. The appellant has not been able to prove the bona fides of his claim that he paid commission and, therefore, the question raised, on the basis of Section 29 (of Income Tax Act, 1961) and 37(1) of the Act, does not arise for consideration. The fraudulent nature of the transactions disentitles the appellant to any relief.

Dismissed.

( RAJIVE BHALLA)

JUDGE

18.7.2013 ( DR. BHARAT BHUSHAN PARSOON)

VK JUDGE

×

Similar Ripples

Questions

Court Denies Tax Deduction for Unproven Sub-Agent Payments

Write your CommentSimilar Posts

Generic

- Reportdata/5661.pdf