Court Limits AO's Power in Fresh Assessment After Set Aside

Full News

Court Limits AO's Power in Fresh Assessment After Set Aside

Court Limits AO's Power in Fresh Assessment After Set Aside

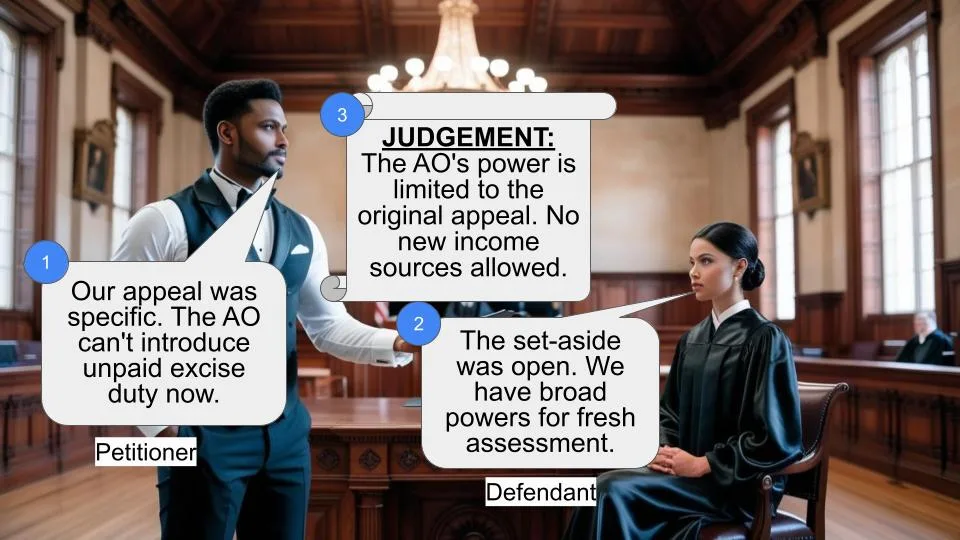

This case involves Saheli Synthetics (P) Ltd. and the Commissioner of Income Tax. The main dispute was about whether an Assessing Officer (AO) could introduce a new source of income during a fresh assessment after the original assessment was set aside by the Commissioner of Income Tax (Appeals) [CIT(A)]. The High Court ruled in favor of the assessee, limiting the AO's power in such situations.

Get the full picture - access the original judgement of the court order here

Case Name:

Saheli Synthetics (P) Ltd. vs Commissioner of Income Tax (High Court of Gujarat)

Income Tax Reference No.116 of 1996

Date: 18 February 2008

Key Takeaways:

1. An AO cannot introduce new sources of income in a fresh assessment following a set-aside order, unless specifically directed.

2. The scope of fresh assessment is limited to the subject matter of the original appeal.

3. The court emphasized the importance of reading appellate orders in context.

4. This decision clarifies the limits of an AO's powers in reassessment cases.

Issue:

Can an Assessing Officer introduce a new source of income during a fresh assessment after the original assessment was set aside by the CIT(A), when the new source was not part of the original assessment or appeal?

Facts:

- The case pertains to the Assessment Year 1987-88.

- Saheli Synthetics (P) Ltd. declared a total income of Rs. 1,08,320.

- The AO initially assessed the taxable income at Rs. 17,57,329.

- The assessee appealed against six items of additions and interest levied.

- The CIT(A) set aside the assessment order on 05.02.1992 for fresh assessment.

- In the fresh assessment, the AO introduced a new item - unpaid excise duty of Rs.81,62,006 under section 43B (of Income Tax Act, 1961).

- This new item was not part of the original assessment or appeal.

Arguments:

Assessee:

- The set-aside order should be read in context of the points in appeal.

- The AO cannot process a new source of income that the CIT(A) itself couldn't have done.

- The AO's powers are limited to the subject matter of the original appeal.

Revenue:

- The set-aside was an "open" set-aside, allowing the AO to reassess all aspects.

- Section 251 (of Income Tax Act, 1961) gives broad powers for fresh assessment.

Key Legal Precedents:

1. CIT vs. Rai Bahadur Hardutroy Motilal Chamaria (1967) 66 ITR 443 (SC): Established that appellate authorities cannot assess new sources of income not processed by the AO.

2. CIT vs. D.N. Dosani (2006) 280 ITR 275: Discussed the scheme of the Act and the specific powers granted to different authorities.

Judgement:

The High Court ruled in favor of the assessee, stating that:

- The AO could not introduce a new source of income (unpaid excise duty) in the fresh assessment.

- The set-aside order by CIT(A) was specific to the items under appeal and couldn't be interpreted as an "open" set-aside.

- The AO's powers in fresh assessment are limited to the subject matter of the original appeal.

FAQs:

Q1: What does this judgment mean for taxpayers?

A1: It provides protection against AOs introducing new sources of income during reassessments unless specifically directed by appellate authorities.

Q2: Does this mean AOs can never assess new sources of income?

A2: No, AOs can still assess new sources through other provisions like sections 147 or 263 of the Income Tax Act, if applicable conditions are met.

Q3: How does this affect the powers of CIT(A)?

A3: It reinforces that CIT(A)'s powers are limited to the subject matter of the appeal, unless they follow specific procedures for enhancement.

Q4: What's the significance of the "open set-aside" concept?

A4: The court rejected the notion of an "open set-aside," emphasizing that all set-aside orders must be read in context of the original appeal.

Q5: How does this judgment impact the interpretation of section 251 (of Income Tax Act, 1961)?

A5: It clarifies that the powers under section 251 (of Income Tax Act, 1961) are not unlimited and must be exercised within the context of the original assessment and appeal.

1. The Income Tax Appellate Tribunal, Ahmedabad Bench 'C' has referred three questions at the instance of the assessee u/s. 256(1) (of Income Tax Act, 1961) (the Act) as against 12 questions proposed by the assessee :

“(1) Whether, on the facts and in the circumstances of the case, the Tribunal was right in law in interpreting the order of the CIT (A) dated 5-2-1992 as open set aside i.e. setting aside the assessment order in toto and accordingly the A.O. was justified bringing to tax a new source of income while framing the de novo assessment?

(2) Whether, on the facts and in the circumstances of the case, the Tribunal was right in law in holding that the Excise Duty collected by the assessee on grey fabrics was in the nature of trading receipts and hence disallowable u/s. 43B (of Income Tax Act, 1961) ?

(3)Whether, on the facts and in the circumstances of the case, the Tribunal was right in law in holding that the bank guarantee furnished by the assessee which was taken by the assessee by depositing certain amount in bank fixed deposit as margin money did not tantamount to actual payment and so section 43B (of Income Tax Act, 1961) is applicable?”

2 The Assessment Year is 1987-88 and the relevant accounting period is year ended on 08.07.1986 (Ashadh Sud Bij). The assessee, a Private Limited Company declared total income of Rs.1,08,320/-. The Assessing Officer framed assessment at a total taxable income of Rs. 17,57,329/- u/s.143(3) (of Income Tax Act, 1961) vide assessment order dated 30.03.1990. In the course of framing the assessment order additions were made in relation to six different items referred to in paragraph Nos. 2 to 7 of the assessment order totaling to Rs.21,75,688/-. The assessee carried the matter in Appeal before the Commissioner (Appeals) challenging the aforesaid six items of additions and also objected to interest levied under sections 139 (of Income Tax Act, 1961) and 217 (of Income Tax Act, 1961).

3 After hearing the representative of the assessee vide order dated 05.02.1992 the Commissioner (Appeals) passed the following order :

“4. I have considered the facts and the appellant's submissions. It is the appellant company's contention that considering the facts which can be verified, no addition or disallowance on any count can be made in the appellant's case. It is the appellant's contention that the assessing officer has made the impugned additions and disallowances in an arbitrary manner without adducing any material in support of his action. It is the appellant's contention that the impugned additions/disallowances have been made without considering the relevant material and without giving to the appellant a proper opportunity of being heard and of explaining its stand with the help of necessary supporting evidence. It may be pointed out that the assessing officer officer is quasi judicial authority and therefore, as a quasi judicial authority, he is supposed to give to the assessee a reasonable opportunity of being heard and of adducing necessary evidence in support of its claim. It may also be mentioned that the doctrine of 'audi alteran parton' is the basic ingredient of natural justice. Besides, it is held that the applicant's contention discussed in detail supra deserve proper examination and consideration by the assessing officer. Considering the totality of the facts and the appellant's submissions and in the interest of justice, the impugned assessment order is set aside with the direction to the assessing officer to reframe the assessment afresh as per law after giving to the appellant a reasonable opportunity of being heard in the matter”.

4 Subsequent thereto the Assessing Officer framed fresh assessment order on 29.03.1994 making additions of four items totaling to Rs.5,08,360/- comprised of following items

“Add : Additions made.

1. Addition on account of stores account relating to previous year as discussed in para 5 above 0,36,040

2. Addition on account of coal as discussed in para 6 above 42,660

3. Addition on account of empty drums and waste materials as discussed in para 6 above 25,000

4. Addition on account of work in process as discussed in para 8 above. 4,04,660

5,08,360”.

However, in the body of the assessment order detailed discussion has been made in relation to unpaid excise duty amounting to Rs.81,62,006/- by holding that same was not allowable u/s. 43B (of Income Tax Act, 1961). This addition is reflected in the order made u/s. 154 (of Income Tax Act, 1961) on 08.04.1994. As the order u/s. 154 (of Income Tax Act, 1961) was not available on record, the learned Advocate for the assessee was permitted to place the same on record with the consent of the other side.

5. The assessee carried the matter in Appeal before the Commissioner (Appeals) and one of the principal ground of challenge was regarding jurisdiction of the Assessing Officer to bring to tax an amount of excise duty collected but not paid by invoking provisions of section 43B (of Income Tax Act, 1961). The Commissioner (Appeals) vide order dated 25.01.1995 rejected the contention regarding absence of jurisdiction in so far as the Assessing Officer is concerned by holding that there was no specific direction and the assessment was set aside to be reframed afresh in totality.

6. The assessee carried the matter in Second Appeal before the Tribunal once again raising the issue relating to jurisdiction of the Assessing Officer. The Tribunal vide order dated 19.10.1995 upheld the order of Commissioner (Appeals) by holding that the entire assessment was set aside and the entire assessment stood open before the Assessing Officer.

That the Assessing Officer was not only free but required by law to probe into the case afresh on all aspects and arrive at a judicially correct conclusion. According to the Tribunal the scope of fresh assessment following the appellate order depended on the subject-matter of the appeal and the appellate order read as a whole in its proper context. Thus, in effect the Tribunal upheld the jurisdiction of the Assessing Officer to make addition of Rs.81,62,006/- being unpaid excise duty u/s. 43B (of Income Tax Act, 1961).

7. At the hearing of the Reference both sides are in agreement that question Nos. 2 and 3 are required to be gone into only provided the first question is answered in favour the Revenue upholding the view expressed by the Tribunal.

8. On behalf of the applicant-assessee Mr. J.P. Shah, learned Advocate contended that the order of the Appellate Authority has to be read as a whole and with reference to context. The last paragraph of the order of the Appellate Authority viz. order dated 05.02.1992 has to be read in context of the points in Appeal. That even if the said order of the Appellate Authority has to be read as a total set aside it is not open to the Assessing Officer to process a new source of income which the Appellate Authority itself could not have done. It was further submitted that in a case where an item is taxed in the assessment order and the assessee does not challenge the same in Appeal, if it was not possible for the assessee to reagitate the said issue on a set aside by the Appellate Authority, on the same reasoning the Assessing Officer cannot be permitted to bring to tax a new source of income. In support of the submissions made reliance has been placed on :

[1] Relevant extract from Vol.II of The Law and Practice of Income Tax by Kanga, Palkhivala and Vyas at page No. 1760 & 1761 :

[2] Katihar Jute Mills (P.) Ltd. Vs. CIT (Cal.) (1979) 120 ITR 861

[3] CIT Vs. Late Jawaharlal Nagpal (1988) 171 ITR 136 (M.P. High Court – Indore Bench)

[4] CIT Vs. S.V. Divakar (1993) 201 ITR 914

[5] CIT Vs. Mahindra And Company (1995) 215 ITR 922- (Raj.H.C. Jaipur Bench)

[6] CIT Vs. D.N. Dosani, (2006) 280 ITR 275

[7] CIT Vs. Rai Bahadur Hardutroy Motilal Chamaria, (1967) 66 ITR 443.

9. Mr. M.R.Bhatt, learned Senior Standing Counsel appearing on behalf of respondent supported the order of the Tribunal by referring to provisions of section 251 (of Income Tax Act, 1961) which deals with powers of the appellate authority to point out that there was no dispute that Commissioner (Appeals) was entitled to set aside the assessment order and refer the case back to the Assessing Officer for making a fresh assessment in accordance with the directions given by Commissioner (Appeals). That in absence of any directions being given by Commissioner (Appeals) the Assessing Officer was entitled to reframe the assessment afresh in totality considering that the set aside was an open set aside and not a conditional or a limited set aside. That the latter part of section 251(1)(a) (of Income Tax Act, 1961) provided that the Assessing Officer was duty bound to proceed to make such fresh assessment and determine the tax payable on the basis of such fresh assessment and therefore bearing in mind the scheme of the Act, with special reference to Sections 4 and 14 of the Act no interference was called for. In support of the submissions reliance was placed on the following decisions :

(1) CIT Vs. McMillan & Co. (1958) 33 ITR 182 (SC).

(2) CIT Vs. Seth Manicklal Fomra (By L.Rs.) (1975) 99 ITR 470.

(3) CIT Vs. T.T. Krishnamachari And Co.(1997) 223 ITR 224.

(4) Smt. Vijaykunverba Vs. CIT (1994) 208 ITR 312 (Guj.)

(5) State of Andhra Pradesh Vs. Hyderabad Asbestos Cement Production Ltd. (1994) 119 CTR 240 (SC).

10. It was further submitted that when the Courts have consistently come to the conclusion that it is open to the Appellate Authority to process a new source of income the same power would be available to the Assessing Officer in case of an open set aside and that once a dispute as to taxability under a particular head was at large before the Appellate Authority, and the assessment was set aside, the powers of the Assessing Officer cannot be restricted only to those particular items under the head of Profits and Gains of Business or Profession but must be available to assess the real income under the said head.

11. Section 251 (of Income Tax Act, 1961) reads as under : “Powers of the Appellate Assistant Commissioner [or, as the case may be, the Commissioner (Appeals)].

251.(1) In disposing of an appeal, the Appellate Assistant Commissioner [or, as the case may be, the Commissioner (Appeals)] shall have the following powers -

(a) in an appeal against an order of assessment, he may confirm, reduce, enhance or annul the assessment; or he may set aside the assessment and refer the case back to the Income-tax Officer for making a fresh assessment in accordance with the directions given by the Appellate Assistant Commissioner [or, as the case may be, the Commissioner (Appeals)] and after making such further inquiry as may be necessary, and the Income-tax Officer shall thereupon proceed to make such fresh assessment and determine, where necessary, the amount of tax payable on the basis of such fresh assessment;

(b) in an appeal against an order imposing a penalty, he may confirm or cancel such order or vary it so as either to enhance or to reduce the penalty;

(c) in any other case, he may pass such orders in the appeal as he thinks fit.

(2). The Appellate Assistant Commissioner [or, as the case may be, the Commissioner (Appeals)] shall not enhance an assessment or a penalty or reduce the amount of refund unless the appellant has had a reasonable opportunity of showing cause against such enhancement or reduction.

Explanation : In disposing of an appeal, the Appellate Assistant Commissioner [or, as the case may be, the Commissioner (Appeals) may consider and decide any matter arising out of the proceedings in which the order appealed against was passed, notwithstanding that such matter was not raised before the Appellate Assistant Commissioner [or, as the case may be, the Commissioner (Appeals)] by the appellant”.

12 On a plain reading of the aforesaid provisions it becomes apparent that the Appellate Authority is entitled to either confirm, reduce, enhance or annul the assessment; or the Appellate Authority may set aside the assessment and refer the case back to the Assessing Officer for making a fresh assessment in accordance with the directions given by the Appellate Authority after making such further inquiry as may be necessary, and the Assessing Officer shall thereupon proceed to make such fresh assessment and determine, where necessary, the amount of tax payable on the basis of such fresh assessment. Thus, the section, or more specifically the clause stipulates confirmation, reduction, enhancement or annulment of the assessment. Alternatively, the section envisages setting aside of assessment and referring the case back to the Assessing Officer for making a fresh assessment in accordance with the directions given, and such fresh assessment may either result in some tax becoming payable or there may be a situation where tax may not be payable on the basis of such fresh assessment. However, the material words in provisions are : “make such fresh assessment”, viz. the word “such” qualifies the assessment to be made afresh in context of the directions given by the Appellate Authority. Therefore, it is not possible to define a set aside assessment as either open set aside or a conditional set aside or a limited set aside. The set aside of assessment made by the Appellate Authority is always in accordance with the directions given by the Appellate Authority for making a fresh assessment. But, the most material part of the provision is the opening portion which stipulates “In an appeal against an order of assessment”. In other words, the entire gamut of powers which are available to the Appellate Authority is governed within the four corners of the subject matter of appeal. The subject matter of appeal is the assessment of income which forms part of the order of assessment in light of the return of income filed by an assessee. There is a subtle, fine distinction between assessment simplicitor, namely assessment of income, and the assessment order. In practice and in effect an assessment order may contain number of assessments of incomes under one head, depending upon the source of income, and/or under more than one head. Even in case where, an Appellate Authority wants to exercise powers of enhancement, under sub-section (2) of section 251 (of Income Tax Act, 1961) such powers have to be exercised after giving a notice for enhancement providing for a reasonable opportunity of showing cause and not in absence of such a notice. This provision itself gives an indication that even if the Appellate Authority wants to process a new source of income which forms part of either return of income or the order of assessment, but was not in challenge in appeal before the Appellate Authority, the Appellate Authority has to give a reasonable opportunity of hearing before processing such a source of income and enhancing the assessment.

13 A fortiori if it is not open to the Appellate Authority to enhance an assessment of income without issuing show cause notice one can never contemplate that the Appellate Authority can set aside an assessment so as to enable the Assessing Officer to exercise powers of enhancement vested in the Appellate Authority without the Appellate Authority discharging the statutory obligation cast on the Appellate Authority by virtue of provisions of section 251(2) (of Income Tax Act, 1961).

14 Similarly even where an assessment is set aside simplicitor, without any enhancement proposal, it is always in context of the appeal against an order of assessment and cannot be read to mean that the Appellate Authority granted powers to the Assessing Officer in relation to items of assessment which were never forming part of Appeal before the Appellate Authority. At the cost of repetition it is required to be noted that processing a new source of income which was on the record before the Assessing Officer but is not forming part of subject matter of appeal before the Appellate Authority can be undertaken by the Appellate Authority only in the course of enhancement of the assessment and therefore any set aside, which does not involve a proposal for enhancement, cannot be used for the purpose of expanding the scope of the powers available to the Assessing Officer while making fresh assessment pursuant to a set aside.

15. Consistently the Courts have held that the powers available to an Appellate Authority are co- extensive and co-terminus with that of the assessing authority and though such powers are plenary powers, yet the Appellate Authority has no power to enhance the assessment by discovering a new source of income not mentioned in the return of income filed by the assessee or considered by the Assessing Officer in the assessment order. In other words, the Appellate Authority cannot travel outside the record. In the case of CIT Vs. Rai Bahadur Hardutroy Motilal Chamaria (supra) the Supreme Court has stated thus :

“The principle that emerges as a result of the authorities of this court is that the Appellate Assistant Commissioner has no jurisdiction, under section 31(3) (of Income Tax Act, 1961), to assess a source of income which has not been processed by the Income-tax Officer and which is not disclosed either in the return filed by the assessee or in the assessment order, and therefore the Appellate Assistant Commissioner cannot travel beyond the subject-matter of the assessment. In other words, the power of enhancement under section 31(3) (of Income Tax Act, 1961) is restricted to the subject-matter of assessment or the source of income which have been considered expressly or by clear implication by the Income-tax Officer from the point of view of the taxability of the assessee. It was argued by Mr. Viswanatha Iyer on behalf of the appellant that, by applying the principle to the present case, the Appellate Assistant Commissioner had jurisdiction to enhance the quantum of income of the assessee. It was pointed out that the fact of the alleged transfer of Rs.5,85,000 to Forbesganj branch was noted by the Income-tax Officer and also the fact that it did not reach Forbesganj on the same day. So, it was argued that in the appeal the Appellate Assistant Commissioner had jurisdiction to deal with the question of the taxability of the amount of Rs.5,85,000 and to hold that it was taxable as undisclosed profits in the hands of the assessee. We are unable to accept the argument put forward on behalf of the appellant as correct. It is true that the Income-tax Officer has referred to the remittance of Rs.5,85,000 from the Calcutta branch; but the Income-tax Officer considered the despatch of this amount only with a view to test the genuineness of the entries relating to Rs.4,30,000 in the books of the Forbesganj branch. It is manifest that the Income-tax Officer did not consider the remittance of Rs.5,85,000 in the process of assessment from the point of view of its taxability. It is also manifest that the Appellate Assistant Commissioner has considered the amount of remittance of Rs.5,85,000 from a different aspect, namely, the point of view of its taxability. But since the Income-tax Officer has not applied his mind to the question of taxability or non-taxability of the amount of Rs.5,85,000 the Appellate Assistant Commissioner had no jurisdiction in the circumstances of the present case to enhance the taxable income of the assessee on the basis of this amount of Rs.5,85,000 or of any portion thereof. As we have already stated, it is not open to the Appellate Assistant Commissioner to travel outside the record, i.e., the return made by the assessee or the assessment order of the Income-tax Officer with a view to find out new sources of income and the power of enhancement under section 31(3) (of Income Tax Act, 1961) is restricted to the source of income which have been the subject-matter of consideration by the Income-tax Officer from the point of view of taxability. In this context “consideration” does not mean “incidental” or “collateral” examination of any matter by the Income-tax Officer in the process of assessment. There must be something in the assessment order to show that the Income-tax Officer applied his mind to the particular subject-matter or the particular source of income with a view to its taxability or to its non-taxability and not to any incidental connection. In the present case, it is manifest that the Income-tax Officer has not considered the entry of Rs.5,85,000 from the point view of its taxability and, therefore, the Appellate Assistant Commissioner had no jurisdiction, in an appeal under section 31 (of Income Tax Act, 1961), to enhance the assessment”.

16. Considering the issue from a slightly different angle one cannot lose sight of the scheme of the Act wherein different provisions have been incorporated for the purpose of disturbing a finalised assessment in light of the fact that the Revenue does not have any power of Appeal against an order of assessment. Though in a slightly different context, this Court has stated thus in relation to the legislative scheme in the case of CIT Vs. D.N. Dosani (supra)”The scheme of the Act has provided different powers to different authorities and these are required to be exercised after satisfying the pre-requisite conditions and jurisdictional facts. The Assessing Officer can disturb/reopen a finalised assessment by invoking his powers either under section 154 (of Income Tax Act, 1961) or under section 147 (of Income Tax Act, 1961), provided he can show that the necessary requirements are fulfilled. If, what the Revenue contends today is accepted, these and other such provisions which empower different authorities to exercise jurisdiction at different points of time in distinct settings would be rendered otiose and that can never be the legislative intent. It is almost akin to providing separate keys for separate locked doors and the person wanting to open a particular door is required to apply the correct key which matches the concerned lock. Therefore, in proceedings to give effect to an order under section 263 (of Income Tax Act, 1961), the Assessing Officer cannot be permitted to undertake an exercise not warranted by the legislative scheme”.

17. Similarly the position in law is well settled that an assessment which is reopened u/s. 147 (of Income Tax Act, 1961) for bringing to tax an escaped income cannot be converted by an assessee into an entirely fresh assessment by making claims which were not originally made. The principle in law is, that every particular provision operates within the limited sphere for which the provision is enacted and hence powers u/s. 251 (of Income Tax Act, 1961) granted to an Appellate Authority cannot be used to render other provisions of the Act like sections 154, 147, 263 and 264 of the Act otiose or redundant.

18. Applying the aforesaid tests to the facts on hand it becomes apparent that when the assessment order was originally framed the Assessing Officer had not considered the issue as regards taxability or non taxability of excise duty collected in context of provisions of section 43B (of Income Tax Act, 1961). The assessment order was silent in this regard. The assessee had only challenged six items of additions before Commissioner (Appeals) along with charging of interest under sections 139 (of Income Tax Act, 1961) & 217 (of Income Tax Act, 1961).

Therefore, when Commissioner (Appeals) framed the order on 05.02.1992 the set aside that was envisaged was in context of the additions or disallowances which were in appeal. The grievance voiced on behalf of the assessee before Commissioner (Appeals) was that considering the facts which could be verified no addition or disallowance was called for, the additions and disallowance were made in an arbitrary manner without adducing any evidence in support of such additions or disallowance, the same have been made without considering the relevant material and without giving an opportunity to the assessee to explain the stand of the assessee. In light of the aforesaid submissions after referring to the doctrine of audi alteram partem, Commissioner (Appeals) held that : “it is held that the appellant's contention discussed in detail supra deserve proper examination and consideration by the assessing officer. Considering the totality of the facts and the appellant's submissions and in the interest of justice, the impugned assessment order is set aside with the direction to the assessing officer to reframe the assessment afresh as per law after giving to the appellant a reasonable opportunity of being heard in the matter”. Hence, even on facts the set aside is with specific directions only, i.e. directions issued by Commissioner (Appeals) in relation to and in context of the grounds of appeal raised before Commissioner (Appeals) ventilating the grievances of the assessee. The aforesaid finding by Commissioner (Appeals) cannot be read to mean that the items of assessment which were not under challenge like depreciation, travelling expenditure under rule 6(D) (of Income Tax Rules, 1962) etc. deserve to be disturbed. If such items could not be disturbed by referring to the order of set aside made by Commissioner (Appeals) the Assessing Officer could not have processed a new source of income which did not form subject matter of assessment in the first round, and thus not a subject matter of appeal before the Appellate Authority. Even the assessee is not permitted to seek deduction/allowance of an item which was not originally claimed, or after being claimed has been disallowed, if the same was not challenged by way of an Appeal. The only remedy that an assessee would have in such circumstances is seeking relief u/s. 264 (of Income Tax Act, 1961) in accordance with law.

19. In the aforesaid set of facts and circumstances and in light of what is stated hereinbefore it becomes apparent that if the Appellate Authority could not have processed the item relating to unpaid excise duty the order of set aside in relation to six items of additions alongwith interest charged could not have been read by the Assessing Officer to expand jurisdiction of the Assessing Officer in the course of fresh assessment made in pursuance of directions issued by Commissioner (Appeals) on 05.02.1992. Hence, the Tribunal was in error in upholding the view expressed by Commissioner (Appeals) in the second round vide order dated 25.01.1995. Question No.1 referred for the opinion of this Court is therefore answered in the Negative i.e. in favour of the assessee and against the Revenue.

20. In light of the answer to question No.1 it is not necessary to answer question Nos. 2 and 3 and the same are left unanswered. Reference stands disposed of accordingly with no order as to costs.

Sd/-

(D.A. Mehta, J.)

Sd/-

(Z.K. Saiyed, J.)

×

Questions

Court Limits AO's Power in Fresh Assessment After Set Aside

Write your CommentSimilar Posts

Generic

- Reportdata/4805.pdf