Court Limits Reassessment Window to 4 Years When Full Disclosure Made

Full News

Court Limits Reassessment Window to 4 Years When Full Disclosure Made

Court Limits Reassessment Window to 4 Years When Full Disclosure Made

This case involves a dispute between the Commissioner of Income Tax, Shimla, and Ruchira Papers Ltd. The main issue was whether the Income Tax Department could issue a reassessment notice after four years when the assessee had fully disclosed all material facts. The High Court ruled in favor of the assessee, limiting the reassessment window to four years in such cases.

Case Name**: Commissioner of Income Tax Shimla VS Ruchira Papers Ltd.

**Key Takeaways**:

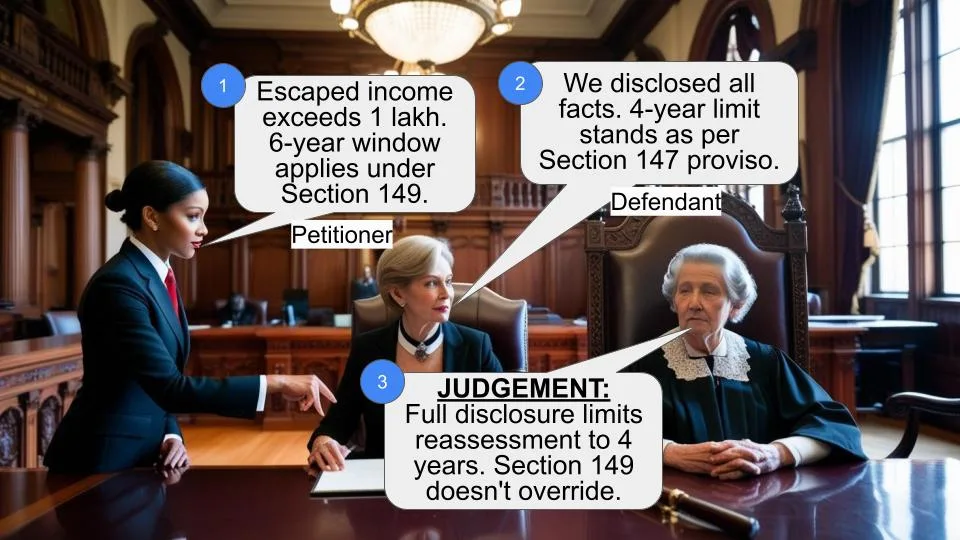

1. When an assessee fully discloses all material facts, the time limit for issuing a reassessment notice is strictly four years.

2. Section 149 (of Income Tax Act, 1961) doesn't override the proviso to Section 147 (of Income Tax Act, 1961) in cases of full disclosure.

3. The court emphasized the need for finality in assessment proceedings.

**Issue**:

Can a notice under Section 148 (of Income Tax Act, 1961) for reassessment be issued after four years, taking benefit of Section 149 (of Income Tax Act, 1961), in a case falling under the proviso to Section 147 (of Income Tax Act, 1961) where there has been true disclosure of all material facts?

**Facts**:

1. Ruchira Papers Ltd. had two units in Himachal Pradesh eligible for tax exemptions under Sections 80 (of Income Tax Act, 1961)-HH and 80-I of the Income Tax Act.

2. The company disclosed losses in one unit and profits in the other but claimed deduction on the entire profits of the profitable unit without adjusting for losses.

3. The Income Tax Department sought to reassess the case after four years, claiming the assessee wasn't entitled to deduction of the entire profits.

**Arguments**:

Revenue's Argument:

- The assessee wrongly claimed deduction, amounting to income escaping assessment.

- Section 149 (of Income Tax Act, 1961) allows for a six-year reassessment window if the escaped income exceeds Rs. 1,00,000.

Assessee's Argument:

- All material facts were fully and truly disclosed during the original assessment.

- The proviso to Section 147 (of Income Tax Act, 1961) limits reassessment to four years in cases of full disclosure.

**Key Legal Precedents**:

1. Vikram Kothari (HUF) vs. State of Uttar Pradesh & Ors., (2011) 242 CTR: This case was cited to support the interpretation of Sections 147 to 149 of the Income Tax Act.

**Judgement**:

The High Court ruled in favor of the assessee, holding that:

1. When there's full, complete, and true disclosure of all material facts, the limitation for reassessment is strictly four years from the end of the assessment year.

2. Section 149 (of Income Tax Act, 1961) governs cases not covered by the proviso to Section 147 (of Income Tax Act, 1961).

3. The four-year limitation in the proviso to Section 147 (of Income Tax Act, 1961) is a specific provision that overrides the general provision in Section 149 (of Income Tax Act, 1961).

**FAQs**:

1. Q: What's the main difference between Section 147 (of Income Tax Act, 1961) and Section 149 (of Income Tax Act, 1961)?

A: Section 147 (of Income Tax Act, 1961) deals with cases where there's full disclosure of facts, while Section 149 (of Income Tax Act, 1961) covers cases where there's non-disclosure or partial disclosure.

2. Q: Does the amount of escaped income matter in cases of full disclosure?

A: No, if there's full disclosure, the four-year limit applies regardless of the amount of escaped income.

3. Q: What's the significance of this judgment for taxpayers?

A: It provides certainty that if they fully disclose all material facts, they won't face reassessment after four years, even if they've claimed a benefit they weren't entitled to.

4. Q: Does this mean the Income Tax Department can never reassess after four years?

A: No, they can still reassess up to six years if there's non-disclosure of facts and the escaped income exceeds Rs. 1,00,000.

5. Q: What's the key takeaway for the Income Tax Department?

A: They need to be more vigilant during the initial assessment, especially in scrutiny cases, as they can't rely on extended time limits if the assessee has made full disclosure.

1. Though this appeal by the Revenue was admitted on a different question of law but in our opinion the following question of law arises in this case:-

Whether in a case falling under proviso to Section 147 (of Income Tax Act, 1961), if there has been true disclosure of all material facts, can notice under Section 148 (of Income Tax Act, 1961) for reassessment be issued after an expiry of period of four years taking benefit of provisions of Section 149 (of Income Tax Act, 1961)?

2. The undisputed fact is that the assessee had two Units within the State of Himachal Pradesh. As per the Industrial Policy and the incentives given, profits in these newly established industrial establishment were entitled for exemption of tax under Sections 80 (of Income Tax Act, 1961)-HH and 80-I of the Income Tax Act, 1961 (hereinafter referred to as the ‘Act’).

3. Before this Court, it has not been disputed that for the purposes of computing profit which was to be exempted under these provisions losses of the Units have also to be taken into consideration and combined together and then the exemption claimed. Admittedly this was not done. However, the assessee did disclose to the Assessing Officer that it had incurred losses in one Unit and made profits in the other Unit. Instead of adjusting the losses o of one Unit against the profits of the other it claimed deduction of the entire profits of the second Unit. It is claimed on behalf of the revenue that the assessee was not entitled to deduction of the entire profits and could have only claimed deduction of the profits after making deduction of the losses of the other Unit of the assessee. The whole dispute revolves around the interpretation to be given to Section 147 (of Income Tax Act, 1961), which reads as follows:-

“147. If the Assessing Officer has reason to believe that any income chargeable to tax has escaped assessment for any assessment year, he may, subject to the provisions of sections 148 to 153, assess or reassess such income and also any other income chargeable to tax which has escaped assessment and which comes to his notice subsequently in the course of the proceedings under this Section, or recomputed the loss or the depreciation allowance or any other allowance, as the case may be, for the assessment year concerned (hereafter in this section and in sections 148 to 153 referred to as the relevant assessment year):

Provided that where an assessment under sub- section (3) of or this section has been made for the relevant assessment year, no action shall be taken under this section after the expiry of four years from the end of the relevant assessment year, unless any income chargeable to tax has escaped assessment for such assessment year by reason of the failure on the part of the assessee to make a return under or in response to a notice issued under sub-section (1) of or to disclose fully and truly all material facts necessary for his assessment, for that assessment year

Explanation 1.- Production before the Assessing Officer of account books or other evidence from which material evidence could with due diligence have been discovered by the Assessing Officer will not necessarily amount to disclosure within the meaning of the foregoing proviso.

Explanation 2. - For the purposes of this section, the following shall also be deemed to be cases where income chargeable to tax has escaped assessment, namely:-

(a) where no return of income has been furnished by the assessee although his total income or the total income of any other person in respect of which he is assessable under this Act during the previous year exceeded the maximum amount which is not chargeable to income-tax;

(b) where a return of income has been furnished by the assessee but no assessment has been made and it is noticed by the Assessing Officer that the assessee has understated the income or has claimed excessive loss, deduction, allowance or relief in the return;

(c) Where an assessment has been made, but-

(i) income chargeable to tax has been under assessed; or

(ii) such income has been assessed at too low a rate; or

(iii) such income has been made the subject of excessive relief under this Act; or

(iv) excessive loss or depreciation allowance or any other allowance under this Act has been computed.”

In addition thereto, reference has been made by Shri Vinay Kuthiala, learned senior standing counsel for the Revenue to the provisions of Section 149 (of Income Tax Act, 1961), which prescribe the time limit for issuance of notice and reads as under:-

“149. (1) No notice under Section 148 (of Income Tax Act, 1961) shall be issued for the relevant assessment year,-

(a) if four years have escaped from the end of the relevant assessment year, unless the case falls under clause (b);

(b) if four years, but not more than six years, have escaped from the end of the relevant assessment year unless the income chargeable to tax which has escaped assessment amounts to or is likely to amount to one lakh rupees or more for that year.

Explanation.- In determining income chargeable to tax which has escaped assessment for the purposes of this sub-section, the provisions of Explanation 2 of Section 147 (of Income Tax Act, 1961) shall apply as they apply for the purposes of that section.

(2) The provisions of sub-section (1) as to the issue of notice shall be subject to the provisions of section 151 (of Income Tax Act, 1961).

(3) If the persons on whom a notice under section 148 (of Income Tax Act, 1961) is to be served is a person treated as the agent of a non-resident under section 163 (of Income Tax Act, 1961) and the assessment, reassessment or recomputation to be made in pursuance of the notice is to be made on him as the agent of such non-resident, the notice shall not be issued after the expiry of a period of two years from the end of the relevant assessment year.”

4. The contention raised on behalf of the Revenue is that in this case though the assessee may have disclosed all facts but it had wrongly claimed the deduction and therefore, it amounts to income escaping from assessment. There can be no dispute with regard to this proposition. In case the assessee has claimed some benefits wrongly then this would definitely be a case of income escaping assessment. The moot point what is the time limit for issuing reassessment notice in such cases.

5. Another admitted fact is that the assessment proceedings in this case were conducted in accordance with the provisions of Section 143 (of Income Tax Act, 1961) i.e. scrutiny proceedings, which definitely entail a greater amount of scrutiny by the Assessing Officer as the term scrutiny itself postulates.

6. It has been contended on behalf of the Revenue that Section 147 (of Income Tax Act, 1961) itself starts with a clause that it is subject to provisions of Sections 148 and 153 of the Act and therefore, must be read subject to Section 149 (of Income Tax Act, 1961). This argument may, at first blush, seem to be attractive but the words of the Statute have to be given a proper interpretation keeping in view the language of all the relevant provisions.

7. When we read Section 147 (of Income Tax Act, 1961), especially the proviso thereto, it clearly postulates that where assessment has been made under sub-section (3) of Section 143 (of Income Tax Act, 1961) no action can be taken after the expiry of four years from the end of the relevant assessment year unless the income chargeable to tax has escaped assessment by reason of or failure on the part of the assessee to either make a return under or in response to a notice or to disclose fully and truly all material facts necessary for the assessment. We are only concerned with the second part of the proviso which deals with disclosing fully and truly all material facts necessary for the assessment. The duty of the assessee is to disclose the facts. It is not his duty to disclose what is the inference to be drawn from the facts. It is not his duty to guide the Income Tax Officer as to whether he is entitled to any exemption or not. This is the role or the duty cast upon the Assessing Officer. If the assessee has placed full and true facts before the Assessing Officer but has taken the benefit of an exemption to which he was not legally entitled to then the Assessing Officer can reopen the assessment only within the period of four years as provided for under this proviso. It is not as if the assessment has become final. It is not as if the mistake cannot be rectified. However, the Legislature has laid down the condition that the limitation for reopening the matter will be four years and no more if there has been full, true and complete disclosure of all the material facts.

8. Finality has to be given to assessment proceedings. These cannot be reopened at the whims and fancy of the Revenue even when mistakes may have taken place. The law provides a procedure and also prescribes the limitation for taking such action. To take benefit of a power, which essentially is very wide power of virtually reopening the assessment, the Revenue must act within the time prescribed by the Act.

9. It has been contended on behalf of the Revenue that Section 149 (of Income Tax Act, 1961) lays down the limitation and since the income, which has escaped assessment in the present case, is more than Rs.1,00,000/- the limitation would be six years and in fact under the un-amended provision of Section 149 (of Income Tax Act, 1961), the limitation would be seven years even in the case where the income escaping assessment was more than Rs.50,000/-.

10. We are of the considered view that Section 149 (of Income Tax Act, 1961) governs that field which is not covered by the proviso to Section 147 (of Income Tax Act, 1961). The proviso to Section 147 (of Income Tax Act, 1961) is a specific provision laying down a special limitation in cases of assessment made on scrutiny where there has been full and complete disclosure of material facts. In such cases, the limitation is four years. Section 149 (of Income Tax Act, 1961) also lays down a limitation of four years even in cases where the income has escaped assessment due to non-disclosure of material facts. However, in case the income escaping assessment is more than Rs.1,00,000/- (Rs.50,000/- earlier) then the limitation would be six years. Therefore, even under Section 149 (of Income Tax Act, 1961), the notice cannot be issued after four years of the end of the relevant assessment year unless the income escaping assessment is more than Rs.1,00,000/- in which case the limitation would be six years. After six years obviously no notice could be issued.

11. It is clear that: (a) when there is full, complete and true disclosure of all material facts, the limitation is only four years from the end of the assessment year concerned; (b) when there is non disclosure of facts the limitation is four years in case the income escaping assessment is less than Rs.1,00,000/-; and (c) in case there is non-disclosure of facts and the income escaping assessment is more than Rs.1,00,000/- the limitation is six years. This is the only interpretation which can be given to Sections 147 to 149.

12. While taking this view we are fortified by the judgment of the Allahabad High Court in Vikram Kothari (HUF) vs. State of Uttar Pradesh & Ors., (2011) 242 CTR Reports, wherein the Allahabad High Court after considering the provisions of Sections 147,148 and 149 of the Act held as follows:-

“13. Thus, on the plain reading of s. 147 and s. 149 legal position in respect of limitation emerges as follows:-

(i) In view of proviso to s. 147 no action can be taken under s.147 beyond the period of four years if the case does not fall within the exception of the proviso mentioned in the proviso itself namely, if there is no case of failure on the part of the assessee to disclose fully and truly all material facts which are necessary for assessment for the year of assessment etc.

(ii) If the case falls under the exception mentioned in the proviso to s. 147, namely there is failure on the part of the assessee to disclose fully and truly all material facts which are necessary for assessment for the year of assessment etc., then action can be taken beyond four years subject to the issue of notice under s. 148 of the Act within the limitation provided under s. 149 of the Act.

(iii) Where case falls under the exception to proviso to s. 147 and escaped income exceed rupees one lac. the notice under s. 148 can be issued beyond the period of 4 years but within 6 years under s. 149(1)(b).

(iv) In case when the escaped income is less than rupees one lac the limitation to issue the notice under s. 148 is only four years, even if the case falls under the exception of proviso to s. 147.”

13. In view of the above discussion, we answer the question in favour of the assessee and against the Revenue and therefore, we find no merit in this appeal, which is accordingly dismissed. No costs.

( Deepak Gupta )

Judge.

( Rajiv Sharma )

Judge.

June 18, 2012

×

Similar Ripples

Questions

Court Limits Reassessment Window to 4 Years When Full Disclosure Made

Write your CommentSimilar Posts

Generic

- Reportdata/5768.pdf