Full News

Court Orders Review of Tax Assessment, Halts Demand Notices for Manufacturing Firm

Court Orders Review of Tax Assessment, Halts Demand Notices for Manufacturing Firm

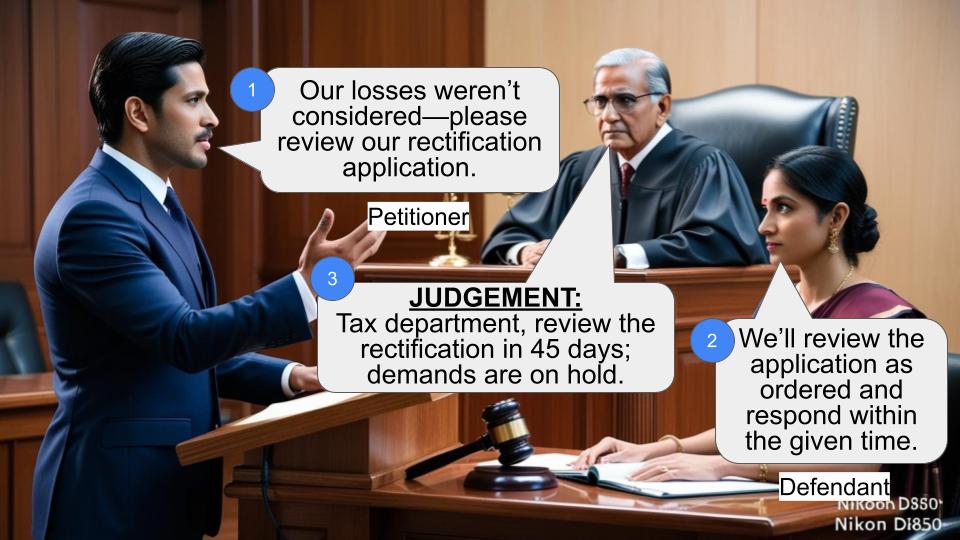

This case involves a manufacturing company (the petitioner) challenging ex-party assessment orders for the tax years 2012-13 and 2013-14. The company filed for rectification of errors in tax calculations, particularly regarding brought forward losses. The court directed the Income Tax Officer to review the rectification application within 45 days and suspended the demand notices in the meantime.

Get the full picture - access the original judgement of the court order here

Case Name:

Paiva Manufacturing Co. Vs Income Tax Officer & Ors. (High Court of Kerala)

WP(C).No.10972 OF 2020(V)

Date: 4th June 2020

Key Takeaways:

1. The court recognized the importance of addressing rectification applications promptly.

2. Ex-parte assessment orders can be challenged if errors are evident.

3. The court provided temporary relief by suspending demand notices pending review.

4. The judgment emphasizes the need for proper consideration of brought forward losses in tax assessments.

Issue:

Should the ex-parte assessment orders for the tax years 2012-13 and 2013-14 be quashed due to errors in calculating brought forward losses?

Facts:

1. The petitioner, a manufacturing company operating as a partnership firm, filed nil income tax returns for 2012-13.

2. The return was processed under Section 143(1) (of Income Tax Act, 1961).

3. The company noticed that brought forward losses of Rs.22,94,096/- were not considered, and a profit of Rs.21,05,953/- was incorrectly set off.

4. The petitioner filed a rectification application under Section 154 (of Income Tax Act, 1961) on 5th June 2013.

5. For the 2013-14 assessment year, the company claimed brought forward losses of Rs.1,88,143/-, but only Rs.1,01,633/- was considered.

6. The department raised demand notices of Rs.7,37,950/- and Rs.38,530/- for 2012-13 and 2013-14 respectively.

Arguments:

Petitioner's Arguments:

1. The assessment orders contained errors in calculating brought forward losses.

2. The company filed timely rectification applications that were not addressed.

3. Despite submitting a detailed reply, no opportunity was given for a hearing.

Income Tax Department's Arguments:

The counsel for the Income Tax Department stated they had not received a copy of the petition and were unable to provide instructions or assistance to the court.

Key Legal Precedents:

The judgment doesn't explicitly mention any legal precedents. However, it references several sections of the Income Tax Act:

1. Section 143(1) (of Income Tax Act, 1961) - Processing of returns

2. Section 154 (of Income Tax Act, 1961) - Rectification of mistakes

3. Section 139 (of Income Tax Act, 1961) - Return of income

Judgement:

1. The court directed the first respondent (Income Tax Officer) to decide on the rectification application within 45 days of receiving the order copy.

2. The demand notices (Exts.P5 and P7) were ordered to be kept in abeyance until the decision on the rectification application.

3. The petitioner was granted liberty to challenge the outcome of the rectification decision if desired.

4. The writ petition was disposed of with these directions.

FAQs:

1. Q: What was the main issue in this case?

A: The main issue was the incorrect calculation of brought forward losses in the petitioner's tax assessments for 2012-13 and 2013-14.

2. Q: Did the court quash the assessment orders?

A: No, the court didn't quash the orders. Instead, it directed the Income Tax Officer to review the rectification application.

3. Q: What immediate relief did the petitioner get?

A: The court ordered that the demand notices be kept in abeyance until the rectification application is decided.

4. Q: How long does the Income Tax Officer have to decide on the rectification application?

A: The officer has 45 days from the receipt of the court order to decide on the application.

5. Q: Can the petitioner challenge the decision on the rectification application?

A: Yes, the court explicitly stated that the petitioner has the liberty to challenge the outcome if they choose to do so.

6. Q: What happens if the information in the writ petition is found to be false?

A: The court granted liberty to the Income Tax Authority to move an appropriate application if the averments in the writ petition are found to be false or incorrect.

This breakdown should help you understand the key aspects of the judgment. Remember, while this analysis provides insights into the case, it's not a substitute for professional legal advice.

1. The petitioner, a manufacturing company, carrying on the business of a partnership firm in the year 2008 has approached this court for quashing of the ex-parte assessment orders Exts.P2 and P4 for the assessment years

2012-13 and 2013-14. The skeleton facts of the case are that the petitioner filed income tax return for the year 2012-13 as Nil. They were uploaded the income tax file through electronic system, which is evidenced from Ext.P1.

Return was processed under Section 143(1) (of Income Tax Act, 1961). Accordingly, an order was issued by the department ie., the Central Processing Centre, (CPC of the Income Tax Department at Bangalore) on 9th May 2013. Upon receipt of the order, it was noticed that the brought

forward losses to the extent of Rs.22,94,096/- was not considered and profit of Rs.21,05,953/- for the same assessment year had been set off against the brought forward losses, w reflected in the Annexure to the return submitted by the petitioner. All these facts are evidenced from the order dated 9th May 2013, Ext.P2.

2. On acquiring the knowledge, the petitioner

availed the remedy of Section 154 (of Income Tax Act, 1961), by

submitting a rectification application dated 5th June 2013,

Ext.P4. However for the next assessment year ie., 2013-

14 filed the return, under Section 139 (of Income Tax Act, 1961) within the

time and claimed the brought forward losses to the extent

of Rs.1,88,143/-. A sum of Rs.11,88,143/- was adjusted

against the proper assessment year 2013-14. But the

petitioner was astonished to notice the intimation under

Section 143(1) (of Income Tax Act, 1961), whereby the adjustment of brought forward

losses to the extent of Rs.1,01,633/- was not considered.

3. Learned counsel appearing on behalf of the

petitioner submits that the aforementioned mistake is

evidenced by Ext.P4. The department, vide Ext.P5, raised

the demand of Rs.7,37,950/- and Rs.38,530/- for the

assessment years 2012-13 and 2013-14 respectively.

Petitioner filed a detailed reply dated 18th March 2019,

Ext.P6 but no opportunity had been given and despite the

receipt of the reply again a similar notice dated 11th

February 2020, Ext.P7 reiterating the demand indicated in

Ext.P5 was issued by the respondent. He submitted that as

per the information downloaded from the income tax site on

18th February 2020, the rectification application is

forwarded to the Jurisdictional Assessing Officer but no

action has been taken.

4. Learned counsel appearing on behalf of the

Income Tax Department submits that he has not received

the copy of the petition and therefore he is unable to obtain

the instructions or rendered assistance to this Court.

5. Having heard the learned counsel for the parties,

appraised the paper book and noticing the fact which are

not in dispute particularly, Ext.P9 dated 18th February 2020,

which reveals the pendency of the rectification application

which stands transferred to the Jurisdictional Assessing

Officer. The grievance of the petitioner can be vindicated

by issuing directions to the first respondent to takes a call

on the rectification application and to decide the same

within a period of 45 days from the date of receipt of the

copy of the order. Till then, the demand raised vide notices

Exts.P5 and P7 is ordered to be kept in abeyance. However,

it is made clear that the petitioner is at liberty to assail the

outcome of the decision of the rectification petition, if he so

chooses, in accordance with law.

The writ petition stands disposed of. Liberty is

granted to the Income Tax Authority to move appropriate

application in case the averments of the writ petition are

found to be false or incorrect.

Sd/-

AMIT RAWAL

JUDGE

×

Similar Ripples

Questions

Court Orders Review of Tax Assessment, Halts Demand Notices for Manufacturing Firm

Write your CommentSimilar Posts

Generic

- Reportdata/6243.pdf