Court Orders Timely Decision on Tax Exemption, Halts Demand Notice

Full News

Court Orders Timely Decision on Tax Exemption, Halts Demand Notice

Court Orders Timely Decision on Tax Exemption, Halts Demand Notice

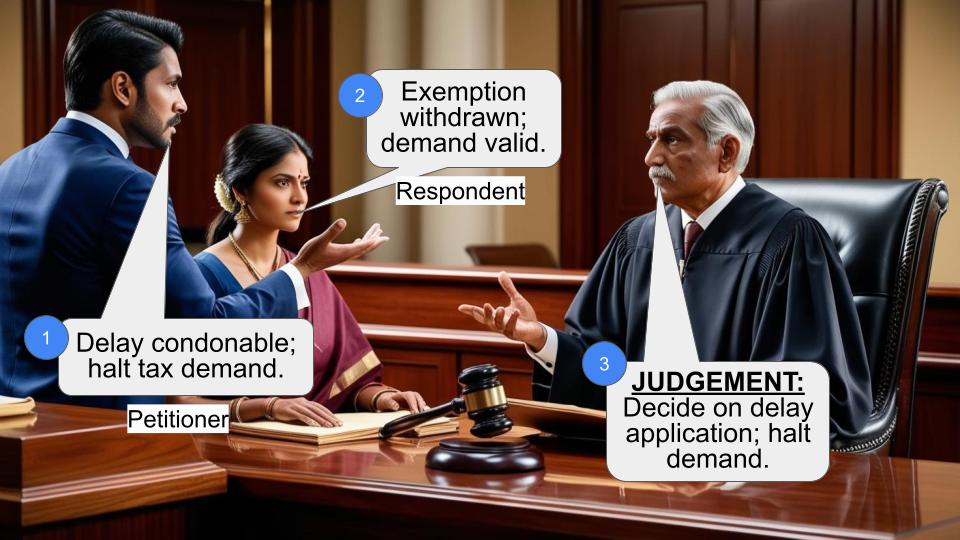

This case involves a dispute between Sree Narayana Educational and Charitable Society (the petitioner) and the Commissioner of Income Tax (Exemptions) (the respondent). The society filed a writ petition seeking a mandamus to direct the respondent to dispose of their application for condonation of delay in filing tax returns and to keep the tax demand in abeyance until then. The court ultimately ruled in favor of the petitioner, directing the respondent to decide on the application within two months and suspending the tax demand until then.

Get the full picture - access the original judgement of the court order here

Case Name:

Sree Narayana Educational and Charitable Society vs Commissioner of Income Tax (Exemptions) and Anr. (High Court of Kerala)

WP(C).No.8890 of 2020(I)

Date: 1st June 2020

Key Takeaways:

1. The court recognized the importance of timely adjudication of tax-related applications.

2. The judgment highlights the potential for condonation of delay in filing tax returns under specific circumstances.

3. The court's decision to suspend the tax demand pending the application's resolution demonstrates a balanced approach to taxpayer rights and tax collection.

Issue:

Should the Income Tax Department be directed to decide on the petitioner's application for condonation of delay in filing tax returns before enforcing a tax demand?

Facts:

1. The petitioner is an educational and charitable society with a certificate under Section 12AA (of Income Tax Act, 1961) .

2. The society failed to file its income tax return for the assessment year 2017-18 within the extended deadline of 07/11/2017 .

3. A notice under section 142(1) (of Income Tax Act, 1961) was issued, granting time until 07/04/2018, but the return was filed on 04/05/2018 .

4. The Income Tax Department denied exemption under Section 11 (of Income Tax Act, 1961) and issued an assessment order on 27/02/2019, assessing the income as Rs.1,11,20,325/- .

5. The petitioner filed an application (Ext.P3) on 30.01.2020 seeking condonation of delay based on a circular allowing such relief .

6. While the application was pending, a demand notice (Ext.P4) for Rs.50,101,576/- was issued on 09.03.2020.

Arguments:

Petitioner's Arguments:

1. Internal disputes among members caused the delay in filing returns .

2. Section 119 (of Income Tax Act, 1961) 2(B) of the Income Tax Act and Circular F.No. 197/55/2018 – ITA-1 dated 22/05/2019 allow for condonation of delay in filing Form 10B Audit Report.

3. The application for condonation (Ext.P3) is still pending, while a demand notice has been issued.

Respondent's Arguments:

1. The exemption under Section 11 (of Income Tax Act, 1961) had to be withdrawn due to non-filing of returns within the usual and extended periods .

2. The demand notice was issued as a result of the withdrawn exemption .

Key Legal Precedents:

The judgment doesn't explicitly mention any specific legal precedents. However, it refers to:

1. Section 12AA (of Income Tax Act, 1961)

2. Section 11 (of Income Tax Act, 1961)

3. Section 143(3) (of Income Tax Act, 1961)

4. Section 119 (of Income Tax Act, 1961) 2(B) of the Income Tax Act

5. Circular F.No. 197/55/2018 – ITA-1 dated 22/05/2019

Judgement:

1. The court directed the 1st respondent to decide on the application (Ext.P3) within 2 months, after giving the petitioner an opportunity to be heard .

2. The demand raised in Exts.P1, P2, and P4 is to be kept in abeyance until the application is disposed of .

3. The interim order is only valid until the disposal of the application (Ext.P3).

FAQs:

1. Q: What was the main issue in this case?

A: The main issue was whether the Income Tax Department should decide on the petitioner's application for condonation of delay before enforcing a tax demand.

2. Q: Why did the court issue an interim order?

A: The court issued an interim order to ensure fair treatment of the petitioner by allowing their application to be heard before enforcing the tax demand.

3. Q: Does this judgment mean the petitioner won't have to pay the tax?

A: Not necessarily. The judgment only suspends the tax demand until the application for condonation of delay is decided. The final tax liability will depend on the outcome of that decision.

4. Q: What is the significance of Circular F. No. 197/55/2018 – ITA-1 in this case?

A: This circular provides guidelines for condonation of delay in filing Form 10B Audit Report, which the petitioner relied on for their application.

5. Q: How long does the Income Tax Department have to decide on the petitioner's application?

A: The court directed the department to decide on the application within 2 months.

1. The petitioner is an Educational and charitable Society, who in the instant Writ Petition, sought the indulgence of this Court to issue a writ in the nature of mandamus, directing the 1st respondent to dispose of Ext.P3, at the earliest and until such time, the demand in terms of Ext.P4 may be ordered to be kept in abeyance. As per the facts which emanate from the pleadings, petitioner Society has been issued a certificate under Section 12AA (of Income Tax Act, 1961) for the assessment year 2017-18, to be filed the Return of income. The Income Tax Return was to be filed on before 07/11/2017 in view of the extension granted by the Central Board of Direct Taxes. However, the Return could not be filed.

2. On account of non-filing of the Return by the petitioner, the petitioner was received notice under section 142(1) (of Income Tax Act, 1961) to file the Return on or before 07/04/2018, but the same could not be filed within the time granted and in fact, it was filed on 04/05/2018. It is in this backdrop of the matter, exemption under Section 11 (of Income Tax Act, 1961) was denied by the 2nd respondent and assessed the Tax by invoking the provisions of Section 143(3) (of Income Tax Act, 1961), resulting into an assessment order dated 27/02/2019, Ext.P1 and the Demand Notice of even date Ext.P2 whereby the income was assessed as Rs.1,11,20,325/- by denying the benefit of exemption under Section 11 (of Income Tax Act, 1961). Mr.Sajan Varghese K, the learned counsel appearing on behalf of the petitioner submits that there were certain disputes among the members and on account of that, the Return could not be filed and there was a delay. Under the provisions of Section 119 (of Income Tax Act, 1961) 2(B) of the Income Tax and the Circular F.No. 197/55/2018 – ITA-1 dated 22/05/2019 the guidelines of the Board, the delay in filing of Form 10B Audit Report for assessment years 2016-17 and 2017-18 could be condoned. It is in this background of the matter, an application, Ext.P3 dated 30.01.2020 was filed. But it is still pending and in the meantime, the Demand, Ext.P4 dated 09.03.2020 calling upon the petitioner to pay a sum of Rs.50,101,576/- has been issued. The petitioner is thus left in lurch in the absence of any adjudication on Ext.P3.

3. Mr.Christopher Abraham accepts notice on behalf of the respondents and submits that on account of non-filing of Return within the usual period and extended period, the exemption under Section 11 (of Income Tax Act, 1961) had to be withdrawn/cancelled. The benefit of exemption had not been granted resulting into issuance of demand and urges this Court for dismissal of this Writ Petition.

4. Heard the learned counsel for parties and perused the paper book. The facts narrated above are not in dispute. Once the circular provides the opportunity to assessees having issued a Registration under Section 12AA (of Income Tax Act, 1961), to seek to recall of the denied exemption in Form 10B and to seek condonation of delay which as noticed above has already been filed in January 2020 vide Ext.P1, but there is no adjudication so far and during its pendency, the impugned Demand Notice of March 2020, Ext.P4 has been issued.

5. Without expressing anything on the merit of the matter, particularly contents of Ext.P3, I dispose of this Writ petition by issuing directions to the 1st respondent and take a call on the application, Ext.P3 filed under Form 10B of the Circular ibid in accordance with law, after affording an opportunity of hearing to the petitioner as expeditiously as possible within a period of 2 months. Until such time, the demand raised in Exts.P1, P2 and P4 is also to be kept in abeyance. It is made clear that the interim order is only till the disposal of the application, Ext.P3 and not thereafter.

This writ petition stands disposed of in the aforementioned directions.

Sd/-

AMIT RAWAL JUDGE

APPENDIX

PETITIONER'S/S EXHIBITS:

EXHIBIT P1 TRUE COPY OF THE ASSESSMENT ORDER DATED

27.12.2019 PASSED BY THE 2ND RESPONDENT.

EXHIBIT P2 TRUE COPY OF THE NOTICE OF DEMAND DATED

27.12.2019 ISSUED BY THE 2ND RESPONDENT.

EXHIBIT P3 TRUE COPY OF THE PETITION DATED 30.01.2020 SUBMITTED BEFORE THE FIRST RESPONDENT SEEKING CONDONATION OF DELAY.

EXHIBIT P4 TRUE COPY OF THE DEMAND NOTICE DATED 09.03.2020 ISSUED BY THE 2ND RESPONDENT.

×

Similar Ripples

Questions

Court Orders Timely Decision on Tax Exemption, Halts Demand Notice

Write your CommentSimilar Posts

Generic

- Reportdata/6244.pdf