Court Quashes Income Tax Reassessment Notice, Citing Lack of Jurisdiction

Full News

Court Quashes Income Tax Reassessment Notice, Citing Lack of Jurisdiction

Court Quashes Income Tax Reassessment Notice, Citing Lack of Jurisdiction

This case involves a partnership firm (the petitioner) challenging a notice issued by the Income Tax Department (the respondent) to reopen an assessment for the 1996-97 assessment year. The High Court ruled in favor of the petitioner, quashing the reassessment notice due to lack of jurisdiction and failure to meet statutory requirements.

Case Name**: V.B. INVESTMENTS VS DEPUTY COMMISSIONER OF INCOME TAX

**Key Takeaways**:

1. Reassessment notices issued after four years from the end of the relevant assessment year require specific conditions to be met.

2. The Assessing Officer must have reason to believe income has escaped assessment due to the assessee's failure to disclose material facts fully and truly.

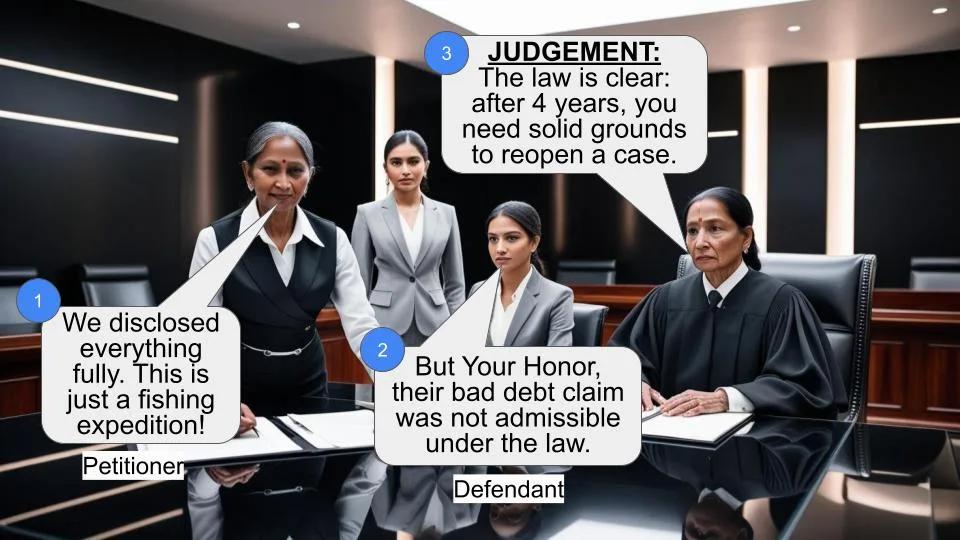

3. Fishing inquiries are not valid grounds for reopening assessments under section 147 (of Income Tax Act, 1961).

4. Change of opinion alone is not sufficient for reopening an assessment.

**Issue**:

Did the Income Tax Department have jurisdiction to reopen the assessment for the 1996-97 assessment year after the expiry of four years from the end of the relevant assessment year?

**Facts**:

1. The petitioner, a partnership firm, filed its return for the 1996-97 assessment year on 30.8.96, declaring a total loss of Rs.3,68,090.

2. The case was selected for scrutiny, and the assessment was framed under section 143(3) (of Income Tax Act, 1961).

3. On 27th February 2003, the respondent issued a notice under section 148 (of Income Tax Act, 1961) to reopen the assessment.

4. The reopening was initiated to scrutinize the petitioner's claim for bad debts of Rs.9,59,423/- due to embezzlement by an accountant.

**Arguments**:

Petitioner's Arguments:

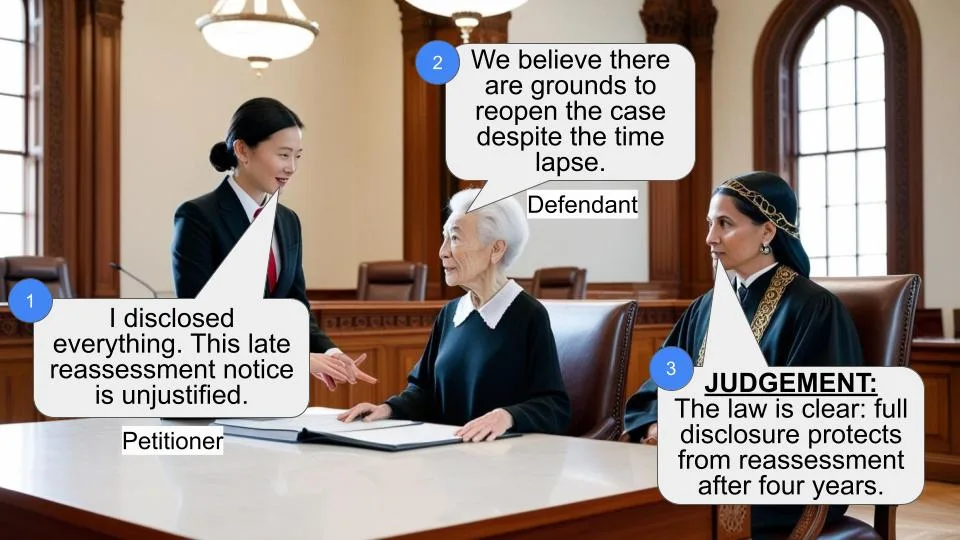

1. The notice was issued after four years from the end of the relevant assessment year, requiring specific conditions to be met.

2. There was no allegation of failure to disclose material facts fully and truly.

3. The reopening was based on a mere change of opinion.

4. All necessary particulars were furnished during the original assessment.

Respondent's Arguments:

1. The claim for bad debts was not admissible in law based on Supreme Court decisions.

2. The claim was erroneously allowed by the Assessing Officer at the relevant time.

**Key Legal Precedents**:

1. Associated Banking Corporation of India Limited v. C.I.T. 56 ITR 1 (SC)

2. C.I.T. v. Navneet Lal Bank Ltd., 56 ITR 707 (SC)

These cases were cited by the respondent regarding the admissibility of bad debt claims. However, the court noted that these decisions were from 1965 and should have been known to the Assessing Officer during the original assessment.

**Judgement**:

The High Court ruled in favor of the petitioner and quashed the reassessment notice. Key points of the judgment include:

1. The Assessing Officer failed to satisfy the conditions of the proviso to section 147 (of Income Tax Act, 1961) for reopening assessments after four years.

2. There was no allegation of failure on the petitioner's part to disclose material facts fully and truly.

3. The reopening appeared to be a fishing inquiry, which is not permissible under section 147 (of Income Tax Act, 1961).

4. The court found that all necessary particulars had been furnished by the petitioner during the original assessment under section 143(3) (of Income Tax Act, 1961).

**FAQs**:

1. Q: What is the significance of the four-year period mentioned in the case?

A: After four years from the end of the relevant assessment year, specific conditions must be met to reopen an assessment, including the assessee's failure to disclose material facts fully and truly.

2. Q: Can an assessment be reopened based on a change of opinion?

A: No, a mere change of opinion is not sufficient grounds for reopening an assessment under section 147 (of Income Tax Act, 1961).

3. Q: What is a "fishing inquiry" in the context of this case?

A: A fishing inquiry refers to reopening an assessment without a firm belief that income has escaped assessment, but rather to investigate whether such an escape has occurred. This is not permitted under section 147 (of Income Tax Act, 1961).

4. Q: How did the court view the Supreme Court decisions cited by the respondent?

A: The court noted that these decisions were from 1965 and should have been known to the Assessing Officer during the original assessment. Their relevance was limited due to the procedural issues in reopening the assessment.

5. Q: What lesson can tax authorities learn from this case?

A: Tax authorities must ensure they meet all statutory requirements, especially when reopening assessments after four years. They should have a clear reason to believe income has escaped assessment due to the assessee's failure to disclose material facts fully and truly.

1. This petition challenges notice dated 27th February 2003 issued by the respondent under section 148 (of Income Tax Act, 1961) (hereinafter referred to as 'the Act') seeking to reopen assessment of the petitioner for the assessment year 1996-97.

2. The petitioner, a partnership firm, filed its return of income for assessment year 199697 on 30.8.96 declaring total loss of Rs.3,68,090. The case of the petitioner was selected for scrutiny assessment and the assessment came to be framed at a total loss of Rs.3,68,090/ under section 143(3) (of Income Tax Act, 1961). Subsequently, the impugned notice came to be issued to the petitioner seeking to reopen the assessment for the said assessment year.

3. Mr. M. J. Dawawala, learned advocate for the petitioner, submitted that the assessment year is 199697 whereas the impugned notice has been issued on 27th February 2003 after the expiry of a period of four years from the end of the relevant assessment year and as such in the absence of any allegation to the effect that there is any failure on the part of the petitioner to disclose fully and truly all material facts necessary for his assessment for the assessment year under consideration, the assumption of jurisdiction on the part of the Assessing Officer under section 147 (of Income Tax Act, 1961) is bad in law.

3.1 Referring to the reasons recorded by the Assessing Officer for reopening the assessment, it was submitted that there is nothing whatsoever stated therein to indicate that there was any failure on the part of the petitioner to disclose material facts. It was pointed out that the reason for reopening is that the Assessing Officer wants to scrutinize the assessee's claim for bad debts of Rs.9,59,423/. Under the circumstances, it is not even the case of the Assessing Officer the any income chargeable to tax has escaped assessment, but that the Assessing Officer wants to make a fishing inquiry upon scrutiny of the material on record to examine as to whether any income chargeable to tax has escaped assessment.

3.2 Next it was contended that the reopening of assessment is also bad on the count that it is based upon a mere change of opinion inasmuch as during the course of the assessment proceedings under section 143(3) (of Income Tax Act, 1961), the petitioner had submitted detailed written submissions with supporting evidence explaining the loss by embezzlement of funds. The Assessing Officer after due application of mind upon being convinced that the petitioner was entitled to the said claim had given setoff for the loss of Rs.9,59,423/ incurred on account of embezzlement of fund by the Accountant. Thus, the reopening of assessment is clearly based upon a change of opinion inasmuch as there is no new material which has come on record to justify formation of opinion on the part of the Assessing Officer that income chargeable to tax has escaped assessment. Therefore, invocation of powers under section 147 (of Income Tax Act, 1961) is without jurisdiction, both on merits as well as on the ground that the same is beyond a period of four years from the end of the relevant assessment year without there being any failure on the part of the petitioner to disclose fully and truly all material facts necessary for its assessment.

4. On the other hand, Ms. Mauna Bhatt, learned Senior Standing Counsel, appearing on behalf of the respondent opposed the petition by placing reliance upon the averments made in the affidavit in reply filed on behalf of the respondents. The attention of the court was drawn to the Form of recording reasons for initiating proceedings under section 147 (of Income Tax Act, 1961), to submit that the Assessing Officer has rightly invoked power under section 147 (of Income Tax Act, 1961) for reopening the assessment as the claim for bad debts on account of embezzlement by the Accountant is not admissible in law in the light of the decisions of the Supreme Court in the case of Associated Banking Corporation of India Limited v. C.I.T. 56 ITR 1 (SC), as well as C.I.T. v. Navneet Lal Bank Ltd., 56 ITR 707 (SC). It was urged that the claim for bad debts having been erroneously allowed by the Assessing Officer at the relevant time on the basis of entries made in the profit and loss account, the Assessing Officer is justified in invoking powers under section 147 (of Income Tax Act, 1961).

5. Before adverting to the merits of the case, it may be germane to notice the legal position in this regard. It is by now well settled by a catena of decisions of the Supreme Court that in view of the proviso to section 147 (of Income Tax Act, 1961), an Assessing Officer acquires jurisdiction to reopen assessment under section 147 (of Income Tax Act, 1961) after the expiry of a period of four years from the end of the relevant assessment year only if he has reason to believe that income chargeable to tax has escaped assessment by reason of failure on the part of the assessee to (i) make a return under section 139 (of Income Tax Act, 1961) or in response to a notice under subsection (2) section 142 (of Income Tax Act, 1961) or section 148 (of Income Tax Act, 1961), or (ii) disclose fully and truly all material facts necessary for his assessment for that assessment year. Before initiating proceedings under section 147 (of Income Tax Act, 1961) by issuing notice under section 148 (of Income Tax Act, 1961), the Assessing Officer is required to record reasons for reopening the assessment recording satisfaction as regards compliance with provisions of section 147 (of Income Tax Act, 1961).

6. In the facts of the present case undisputedly the impugned notice has been issued after the expiry of a period of four years from the end of the relevant assessment year. Under the circumstances the requirements of the proviso to section 147 (of Income Tax Act, 1961) must be satisfied to vest in the Assessing Officer the jurisdiction to reopen the assessment. In the present case it is not the case of the Assessing Officer that there is any failure on the part of the petitioner to make a return under section 139 (of Income Tax Act, 1961) or in response to a notice under subsection (2) section 142 (of Income Tax Act, 1961) or section 148 (of Income Tax Act, 1961). Hence, for the purpose of assuming jurisdiction to reopen assessment the Assessing Officer is required to be satisfied that income chargeable to tax has escaped assessment by reason of failure on the part of the petitioner to make full and true disclosure of all material fact in respect of the assessment year under consideration and such satisfaction must be reflected in the reasons recorded by him as contemplated under subsection (2) of section 148 (of Income Tax Act, 1961). It would, therefore, be necessary to advert to the reasons recorded for reopening the assessment.

7. The record of the case indicates that the petitioner had by a letter dated 11.04.2003 requested the Assessing Officer to furnish a copy of the reasons recorded for reopening the assessment, pursuant to which the Assessing Officer had by a letter dated 29.05.2003 informed the petitioner that the reason for reopening the assessment is to scrutinise the assessee’s claim for the bad debts of Rs.9,59,423/ which had been claimed by it on account of embezzlement of funds by the accountant during the F.Y. 199394. This in sum and substance are the reasons communicated to the petitioner. However, along with the affidavitin- reply filed by the respondent a copy of the “From for recording reasons for initiating proceedings under section 147 (of Income Tax Act, 1961) for obtaining the approval of the Commissioner of Incometax” has been annexed which according to the learned counsel for the respondent contains detailed reasons. In the said form against the column “Reasons for the belief that income has escaped assessment” it has been stated thus: “While finalizing the regular asstt. for A.Y. 199697 u/s 143(3) (of Income Tax Act, 1961), the A.O. allowed assessee’s claim for bad debts of Rs.9,59,423/ on the basis of entries passed in the Profit & Loss A/c which was not allowable looking to the decision of the Supreme Court in the case of Associated Banking Corporation of India Limited v. C.I.T. 56 ITR 1 (SC)1 and C.I.T. v. Navneet Lal Bank Ltd., 56 ITR 707 (SC). The real fact was that the Assessee derived the Loss of Rs.9,59,423/ due to embezzlement made by Shri Bharat K. Shah an accountant of the firm in the financial year 199394. The assessee observed that there was no possibility of any recovery out of the said amount of Rs.9,59,423/ and accordingly written off the said amount as bad debts in the A.Y. 199697. As the claim was erroneously allowed by A.O. there was an under Assessment of income of Rs.9,59,423/ requiring reassessment within the meaning of section 147 (of Income Tax Act, 1961).”

8. From the reasons communicated to the petitioner it is apparent that all that is stated is that the Assessing Officer wants to scrutinise the petitioner’s claim for bad debt of Rs.9,59,423/ on account of embezzlement of funds by the accountant. Even if the detailed reasons are seen, it is evident that it is the case of the Assessing Officer that the claim of the petitioner which was not in consonance with the above referred decisions of the Supreme Court had been wrongly allowed by then Assessing Officer at the relevant time. In the entire reasons recorded there is not even a whisper as regards any failure on the part of the petitioner to make full and true disclosure of all material facts as contemplated under the proviso to section 147 (of Income Tax Act, 1961). Under the circumstances the conditions precedent for assumption of jurisdiction under section 147 (of Income Tax Act, 1961) beyond a period of four years from the end of the relevant assessment year are clearly not satisfied.

9. Another aspect of the matter is that as noticed earlier the sole reason for reopening the assessment is to scrutinize the assessee's claim of bad debts. In this regard a perusal of the record of the case shows that during the course of assessment proceedings, the petitioner had made detailed submissions in respect of its claim for setoff of the loss in respect of bad debt on account of embezzlement of funds by the accountant during the financial year 199394. The Assessing Officer after considering the submissions had accepted the same and had allowed the setoff of loss of Rs.9,59,423/ incurred on account on embezzlement of funds. Thus, it is apparent that all necessary particulars had been furnished by the petitioner during the course of assessment under section 143(3) (of Income Tax Act, 1961). Besides, as is apparent on a plain reading of the reasons as furnished to the petitioner, the Assessing Officer want to reopen the assessment to scrutinise the petitioner’s claim for bad debts of Rs.9,59,423/ . As noted hereinabove, assessment can be reopened under section 147 (of Income Tax Act, 1961), if the Assessing Officer is of the belief that income chargeable to tax has escaped assessment and not to carry out a fishing inquiry to ascertain as to whether or not income chargeable to tax has escaped assessment. The learned counsel for the petitioner is, therefore, justified in contending that even on merits the reopening of assessment is not valid.

10. Insofar as the applicability or otherwise of the decisions of the Supreme Court on which reliance has been placed by the Assessing Officer for the purpose of reopening the assessment, firstly the said decisions are old decision of the year 1965 and as such are deemed to have been within the knowledge of the Assessing Officer at the time when the original assessment came to be framed, and secondly, in the light of the fact that the conditions precedent for exercise of powers under section 147 (of Income Tax Act, 1961) after the expiry of a period of four years from the end of the relevant assessment year have not been satisfied, it is not necessary to enter into any discussion in respect thereof. Even if the submission of the Assessing Officer that the claim for bad debts had been erroneously allowed were to be accepted, even then in the absence of any failure on the part of the petitioner to disclose fully and truly all material facts the reopening of assessment under section 147 (of Income Tax Act, 1961) is without jurisdiction. Consequently, the impugned notice issued under section 148 (of Income Tax Act, 1961) cannot be sustained.

11. For the foregoing reasons, the petition succeeds and is, accordingly, allowed. The impugned notice dated 27th February 2003 issued by the respondent seeking to reopen the assessment of the petitioner for the assessment year 199697 is hereby quashed and set aside. Rule is made absolute accordingly with no order as to costs.

(Akil Kureshi, J.)

(Harsha Devani, J.)

×

Similar Ripples

Questions

Court Quashes Income Tax Reassessment Notice, Citing Lack of Jurisdiction

Write your CommentSimilar Posts

Generic

- Reportdata/5791.pdf