Court Quashes Reassessment Notice, Citing Lack of Tangible Evidence

Full News

Court Quashes Reassessment Notice, Citing Lack of Tangible Evidence

Court Quashes Reassessment Notice, Citing Lack of Tangible Evidence

This case involves a dispute between Woodward Governor India Ltd. (the assessee) and the Assistant Commissioner of Income Tax (the revenue). The revenue issued a reassessment notice under Section 147 (of Income Tax Act, 1961)-148 of the Income Tax Act for the Assessment Year 1997-98. The assessee challenged this notice, and the High Court ultimately quashed the reassessment notice, ruling in favor of the assessee.

Get the full picture - access the original judgement of the court order here

Case Name:

Woodward Governor India Ltd. Vs Assistant Commissioner of Income Tax (High Court of Delhi)

W.P.(C) 16902/2004

Date: 5th October 2016

Key Takeaways:

1. Reassessment notices must be based on tangible material or evidence outside of the concluded assessment.

2. The revenue cannot rely solely on a change in legal interpretation to reopen a concluded assessment.

3. Statutory orders must be judged based on their apparent reasons, not later explanations.

Issue:

Was the reassessment notice issued by the revenue valid and based on sufficient tangible evidence to reopen a concluded assessment?

Facts:

1. The case pertains to the Assessment Year 1997-98.

2. The assessee company claimed a deduction under Section 80IA (of Income Tax Act, 1961) on 30% of its taxable income.

3. The taxable income included income from services, sale commission, and interest on fixed deposits with banks, apart from trading income.

4. The revenue issued a reassessment notice under Section 147 (of Income Tax Act, 1961)-148 of the Income Tax Act to reopen the concluded assessment.

5. The revenue claimed that certain components of income were inadmissible for deduction under Section 80IA (of Income Tax Act, 1961).

Arguments:

Revenue's Arguments:

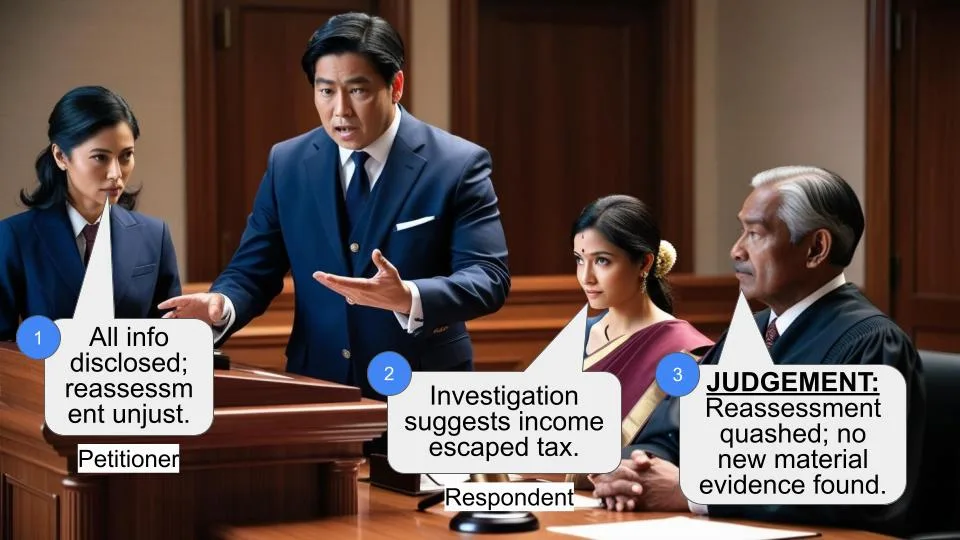

1. The assessee failed to provide a break-up of income from commission and interest on fixed deposits.

2. The Assessing Officer (AO) didn't make diligent enquiries during the original assessment.

3. Certain income components were not eligible for deduction under Section 80IA (of Income Tax Act, 1961) as per Supreme Court judgments.

Assessee's Arguments:

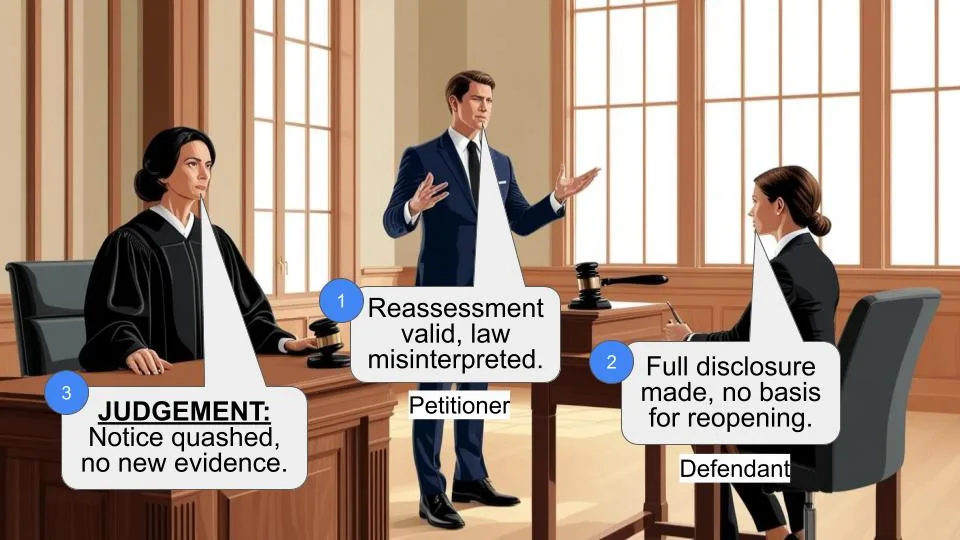

1. The reasons for reopening didn't indicate any objective or tangible material beyond the concluded assessment.

2. Full disclosure, including income break-up, was made during the original assessment proceedings.

Key Legal Precedents:

1. Commissioner of Income Tax vs. Kelvinator Ltd. (320 ITR 561): This Supreme Court ruling states that reassessment proceedings require tangible material or evidence outside the concluded assessment.

2. Pandian Chemicals Ltd. vs. CIT (262 ITR 278 SC) and Liberty India vs. CIT (2009) (317 ITR 218 SC): These cases were cited by the revenue regarding the admissibility of certain income under Section 80-IA (of Income Tax Act, 1961).

3. M.S. Gill and Anr. vs. Chief Election Commissioner (AIR 1978 SC 581): This case established that statutory orders should be judged based on apparent reasons, not later explanations.

Judgement:

The High Court ruled in favor of the assessee and quashed the reassessment notice. The court's reasoning was:

1. There was no reference to tangible material or objective documents outside the concluded assessment in the reasons furnished by the revenue.

2. As per the Supreme Court ruling in Kelvinator Ltd., without such tangible evidence, there cannot be a valid opinion leading to proper reassessment proceedings.

3. The revenue's rationale based on Supreme Court judgments (Liberty India and Pandian) was found unpersuasive, as it could have been the basis for a revision under Section 264 (of Income Tax Act, 1961), not reassessment.

4. The court emphasized that statutory orders must be judged on apparent reasons, not later explanations.

FAQs:

1. Q: What was the main reason for quashing the reassessment notice?

A: The main reason was the lack of tangible material or evidence outside the concluded assessment to justify reopening the case.

2. Q: Can the revenue reopen an assessment based solely on a change in legal interpretation?

A: No, according to this judgment, a mere change in legal interpretation without new tangible evidence is not sufficient for reopening an assessment.

3. Q: What is the significance of the Kelvinator Ltd. case in this judgment?

A: The Kelvinator Ltd. case established that reassessment proceedings require tangible material or evidence outside the concluded assessment, which was a key principle applied in this case.

4. Q: Could the revenue have taken a different approach instead of issuing a reassessment notice?

A: Yes, the court suggested that the revenue could have potentially used Section 264 (of Income Tax Act, 1961) for revision based on the Supreme Court judgments they cited.

5. Q: What lesson can tax authorities learn from this case?

A: Tax authorities should ensure they have tangible evidence or material outside the concluded assessment before issuing reassessment notices, and not rely solely on reinterpretation of existing information.

The asessee challenges reassessment notice under Section 147 (of Income Tax Act, 1961)-148 of the Act issued by the revenue seeking to re-open the concluded assessment for AY 97-98. The reasons furnished by the respondent/revenue to re-open the assessment are extracted below-Reasons for the belief that income has escaped assessment.

The assessee company has claimed deduction u/s 801A (of Income Tax Act, 1961) on 30% of taxable income (Rs.1,66,26,841). Taxable income includes income from services (Rs.31,53,009/-) income from sale commission (Rs.6,22,987/-) and interest on fixed deposits with bank (Rs. 24,746/-) apart from trading income, which is to be quantified. Deduction u/s 801A (of Income Tax Act, 1961) is only allowable on profits and gains ‘derived from’ the industrial undertaking setup. Income from sales After notice was issued this court admitted the petition and issued rule. The revenue in support of the reassessment notice urges that the failure of the petitioner to indicate the break-up of income that arose on account of commission and interest on fixed deposits empowers it to proceed under Section 147 (of Income Tax Act, 1961). It is submitted that in any event, the materials on record originally disclosed to the revenue at the time of completion of assessment, do not give the appropriate break up; more significantly the AO did not make diligent enquiries in that regard. It is urged that the two heads of Income sought to be passed off as deductions and clubbed with the receipts that are legitimately admissible under Section 80-IA (of Income Tax Act, 1961), are contrary to the declaration of law by the Supreme Court in Pandian Chemicals Ltd. Vs. CIT reported in 262 ITR 278 SC and Liberty India vs. CIT (2009) 317 ITR 218 SC.

The counsel for the petitioner urges that the so-called opinion or “reasons to believe” leading to the re-assessment, nowhere indicate any objective material much less tangible material in that impelled the AO to revisit a concluded issue. It is urged that the rationale for re-opening is utterly inaccurate because during the course of assessment proceedings, full disclosure including the break-up of income was in commission, income from services, trading income, bank interest cannot be said to be profits ‘derived from’ the industrial undertaking. I therefore have reason to believe that income in excess of Rs. 4,70,532/- has escaped assessment Notice u/s 148 (of Income Tax Act, 1961) may be issued, if approved.

fact made.

It is evident from a plain reading of the reasons furnished by the revenue that there is no allusion to tangible material in the form of objective documents, information etc outside of the concluded assessment and the documents pertaining to it. According to the binding ruling of the Supreme Court in Commissioner of Income Tax vs. Kelvinator Ltd. 320 ITR 561, sans such documents, evidence or tangible material, there cannot be valid opinion leading to proper re-assessment proceedings.

The rationale furnished by the revenue in its counter affidavit and reiterated in the court during the hearing was that a component of income which was otherwise inadmissible but escaped the notice of the AO, because of the ratio in Liberty India and Pandian (supra) is unpersuasive. Besides, the lack of any reference to objective material, cannot in any way improve the case of the revenue – much less its reference to otherwise binding judgments that could have been the basis of a valid revision by the revenue under Section 264 (of Income Tax Act, 1961). It goes without saying that statutory orders containing reasons are to be judged on the basis of what is apparent and not what is explained later, as the validity of those orders does not improve with time or on account of better explanations furnished in the course of legal proceedings (refer M.S. Gill and Anr. vs. Chief Election Commissioner AIR 1978 SC 581.

For the foregoing reasons, the petition has to succeed. The reassessment notice dated 31.03.2004 and all further proceedings emanating from it are hereby quashed.

The writ petition is allowed in the above terms.

S. RAVINDRA BHAT, J

DEEPA SHARMA, J

OCTOBER 05, 2016

×

Similar Ripples

Questions

Court Quashes Reassessment Notice, Citing Lack of Tangible Evidence

Write your CommentSimilar Posts

Generic

- Reportdata/2360_5iunzgL.pdf