Court Quashes Tax Reassessment Notice, Upholds Long-Term Capital Gains Claim

Full News

Court Quashes Tax Reassessment Notice, Upholds Long-Term Capital Gains Claim

Court Quashes Tax Reassessment Notice, Upholds Long-Term Capital Gains Claim

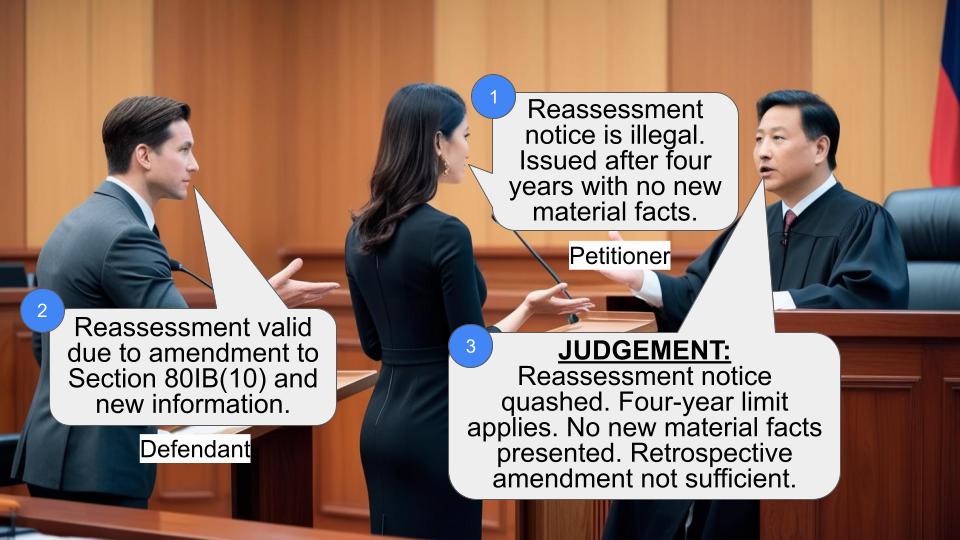

This case involves B. Kasi Viswanathan (the petitioner) challenging a notice issued by the Income Tax Officer (the respondent) to reopen his tax assessment for the year 2009-10. The court ruled in favor of the petitioner, quashing the reassessment notice and upholding the petitioner's claim for Long-Term Capital Gains deduction under Section 54 (of Income Tax Act, 1961).

Get the full picture - access the original judgement of the court order here

Case Name:

B. Kasi Viswanathan vs Income Tax Officer (High Court of Madras)

W.P.No.41441 of 2016 and W.M.P.Nos.35418 & 35419 of 2016

Date: 11th February 2020

Key Takeaways:

1. The Income Tax Department cannot reopen assessments beyond four years without evidence of failure to disclose material facts by the assessee.

2. A change of opinion by the tax authorities is not grounds for reopening an assessment under Section 147 (of Income Tax Act, 1961).

3. Full and true disclosure of all material facts by the assessee during the original assessment prevents reassessment under Section 147 (of Income Tax Act, 1961).

4. The court emphasized the importance of adhering to the proviso of Section 147 (of Income Tax Act, 1961) when conducting reassessment proceedings.

Issue:

Can the Income Tax Department reopen an assessment under Section 147 (of Income Tax Act, 1961) when the assessee has fully disclosed all material facts during the original assessment?

Facts:

1. The petitioner purchased a property in Mumbai in 2001 for Rs.54,32,000/-

2. He registered the property in 2008 and sold it for Rs.1.20 crores during the Assessment Year 2008-09

3. For the Assessment Year 2009-10, the petitioner filed returns declaring a total income of Rs.47,54,535/- and claimed deduction under Section 54 (of Income Tax Act, 1961)

4. The return was processed under Section 143(1) (of Income Tax Act, 1961) and later selected for scrutiny

5. An assessment order was passed on 29.10.2011

6. On 30.03.2016, the Income Tax Department issued a notice under Section 148 (of Income Tax Act, 1961) to reopen the assessment

Arguments:

Petitioner's Arguments:

1. The property was purchased in 2001 and sold in 2008, qualifying for Long-Term Capital Gains treatment

2. All material facts were fully disclosed during the original assessment

3. The reassessment notice is based on a change of opinion, which is not permissible as per the Supreme Court's decision in Kelvinator of India Ltd. case

Respondent's Arguments:

1. The department has the power to reopen assessments as long as the notice meets the criteria under Sections 149 (of Income Tax Act, 1961) to 153 of the Income Tax Act

2. The views expressed in the communication dated 10.11.2016 are only prima facie

Key Legal Precedents:

1. Commissioner of Income Tax vs. Kelvinator of India Ltd., (2010) 2 SCC 723:

Established that a mere change of opinion cannot be grounds for reopening an assessment

2. G.K.N. Driveshafts (India) Ltd. vs. Income Tax Officer and Others, (2003) 1 SCC 72:

Requires the department to furnish reasons for reopening an assessment when requested by the assessee

3. Calcutta Discount Private Limited vs. CIT, (1961) 41 ITR 191:

Reiterated in Jeans Knit Private Limited vs. Deputy Commissioner of Income Tax, (2018) 12 SCC 36, regarding the principles of reassessment

Judgement:

1. The court ruled in favor of the petitioner, stating that the Income Tax Department cannot reopen the assessment on the issue of Long-Term Capital Gains

2. The court directed the respondent to pass an appropriate order within 30 days without disturbing the petitioner's claim for Long-Term Capital Gains allowed under Section 54 (of Income Tax Act, 1961)

3. The court allowed the respondent to examine any other aspect of escaped assessment in light of Explanation 3 to Section 147 (of Income Tax Act, 1961)

FAQs:

Q1: What is the time limit for reopening a tax assessment?

A1: Generally, it's 4 years from the end of the relevant assessment year. However, in cases of income escaping assessment, it can be extended to 6 years.

Q2: Can the tax department reopen an assessment based on a change of opinion?

A2: No, as per the Supreme Court's decision in the Kelvinator of India Ltd. case, a mere change of opinion is not grounds for reopening an assessment.

Q3: What is the significance of Section 54 (of Income Tax Act, 1961) in this case?

A3: Section 54 (of Income Tax Act, 1961) allows for deduction on Long-Term Capital Gains from the sale of a residential property if certain conditions are met.

Q4: What should taxpayers learn from this case?

A4: It's crucial to fully and truly disclose all material facts during the original assessment to prevent future reassessments.

Q5: Does this judgment completely bar the tax department from reassessing the petitioner's case?

A5: No, the judgment allows the department to examine other aspects of escaped assessment, but they cannot disturb the Long-Term Capital Gains deduction already allowed.

1. In the Writ Petition, the petitioner has challenged the impugned communication dated 10.11.2016 bearing reference ITO/NCW15(2)/ADLPV3666R16-17.

2. By the impugned communication dated 10.11.2016, the respondent has overruled the objection of the petitioner against invocation of machinery prescribed for reopening of the assessment under Section 148 (of Income Tax Act, 1961) read with Section 147 (of Income Tax Act, 1961).

3. The impugned communication was issued to the petitioner in response to the objection of the petitioner vide letters/communications dated 05.04.2016 and 26.09.2016 against the notice dated 30.03.2016 bearing reference No. PAN:ADLPV3666R/ACIT/NCC-15/AY 09-10 issued under Section 148 (of Income Tax Act, 1961) read with Section 147 (of Income Tax Act, 1961).

4. The petitioner had purchased a property in the year 2001 in Mumbai for a sum of Rs.54,32,000/-. The petitioner registered the said property vide sale deed in the year 2008 and perfected the title. Later the petitioner sold the same for a total consideration of Rs.1.20 crores during Assessment Year 2008-09.

5. The petitioner filed income tax returns on 31.07.2009 for the Assessment Year 2009-10, wherein, the petitioner declared a total income of Rs.47,54,535/- and claimed deduction under Section 54 (of Income Tax Act, 1961).

6. The said return was processed under Section 143(1) (of Income Tax Act, 1961) and was later selected for scrutiny and a notice was issued under Section 143(2) (of Income Tax Act, 1961). Details were called for recording the same and explanations were offered on behalf of the petitioner on 03.10.2011 and on 20.10.2011. Thereafter, an assessment order was also passed by the then Asst. Commissioner of Income Tax on 29.10.2011.

7. The last date for reopening the assessment under Section 148 (of Income Tax Act, 1961) within a period of four years and six years would have expired on 31.03.2014 and 31.03.2016 respectively for the purpose of Section 147 (of Income Tax Act, 1961).

8. The impugned notice was issued on 30.03.2016 under Section 148 (of Income Tax Act, 1961). Under these circumstances, the petitioner called upon the respondent to furnish reasons for reopening the assessment as per the decision of the Hon’ble Supreme Court in G.K.N.Driveshafts (India) Ltd. Vs. Income Tax Officer and Others, (2003) 1 SCC 72. By a communication dated 08.08.2016 bearing reference No.ITO/NCW15(2)/ADLPV366R/16-17, the reasons were furnished to the petitioner.

9. It is stated that the petitioner has wrongly claimed Long- Term Capital Gain of Rs.41,39,650/- on transfer of house property for sale consideration of Rs.1.2 crores and had claimed an exemption under Section 54 (of Income Tax Act, 1961) by depositing a sum of Rs.50 lakhs under the Capital Gain Scheme the Corporation Bank on 13.07.2009 and that from the recital of the Agreement of Sale dated 18.03.2009, it was noticed that the petitioner had acquired the house property only on 30.01.2008 and transferred it within fourteen months of its purchase and therefore wrongly claimed the benefit of Long Term Capital Gains under Section 54 (of Income Tax Act, 1961).

10. The respondent concluded that the capital asset transferred was only a short-term capital asset as it was held for a period less than thirty six months ie. only for a period of fourteen months and therefore the petitioner was not entitled to Long-Term Capital Gain under Section 54 (of Income Tax Act, 1961),

11. The petitioner sent its objections to the above reasons stating that the property was indeed purchased in the year 2001 and sold only in the year 2008 on 30.01.2008 and that the petitioner has been holding the property for more than a period of thirty six months and therefore the petitioner was entitled to treat the asset is a Long-Term Capital is a claim exemption under Section 54 (of Income Tax Act, 1961). It was further stated that the petitioner has all along claimed deduction on the interest paid on housing loan under Section 24 (of Income Tax Act, 1961) from the Assessment Year 2001-2002, which was accepted by the Department.

12. The learned counsel for the petitioner submitted that the impugned notice dated 30.03.2016 and the impugned communication dated 10.11.2016 are liable to be quashed in the light of the decision of the Hon’ble Supreme Court in Commissioner of Income Tax Vs. Kelvinator of India Ltd., (2010) 2SCC 723, wherein the Hon’ble Supreme Court held that there is a conceptual difference between the power to review and the power to re-assess. An Assessing Officer has no power to review and re-assessment has to be based on fulfilment of certain pre- conditions and if concept of “change of opinion” was removed as was contended on behalf of the Department the said case, then in the garb of reopening of the assessment review would take place.

13. The learned counsel for the petitioner also submitted that the view of Division Bench of this court in the Joint Commissioner of Income Tax Vs. Kalanithi Maran, 2014 3 LW 846, was overruled by the Hon’ble Supreme Court.

14. The learned counsel for the petitioner also submitted that the Hon’ble Supreme Court in Jeans Knit Private Limited Vs. Deputy Commissioner of Income Tax, (2018) 12 SCC 36, has reiterated the principle laid down by the Hon’ble Supreme Court in Calcutta Discount Private Limited Vs. CIT, (1961) 41 ITR 191. The reliance was also placed on a recent decision of the learned Single Judge in the M/s.Asianet Star Communication Private Limited Vs. Asst Commissioner of Income Tax in W.P.Nos.25328, 25331 and 25336 of 2018 pronounced on 16.04.2019.

15. Opposing this Writ Petition, the learned Government Pleader (T) for the respondent submits that this writ petition is liable to be dismissed as the respondent is indeed empowered to reopen the assessment as long as the notice issued under Section 148 (of Income Tax Act, 1961) meet the criteria under Sections 149 (of Income Tax Act, 1961) to 153 of the Income Tax Act, 1961. It is submitted that the views expressed in the communication dated 10.11.2016 is only a prima facie view and therefore the petitioner should be directed to participate in the adjudicatory mechanism prescribed the Act.

16. The learned Government Pleader (T) for the respondent has relied on the decision of a learned Single Judge in Seshasayee Paper Boards Ltd. Vs. Union of India in W.P.Nos.12603 & 12604 of 2002 and W.P.No.33239 of 2002 dated 25.01.2019, wherein, in a somewhat identical case, the writ petitions were dismissed.

17. I have considered the arguments advanced on behalf of the petitioner and the learned Government Pleader (T) for the respondent. Vast powers have been vested with the officers under the provisions of the Income Tax Act, 1961 to reopen the assessment under Section 148 (of Income Tax Act, 1961) for the purpose of Section 147 (of Income Tax Act, 1961). The notice to be issued under Section 148 (of Income Tax Act, 1961), has to be within the period of limitation prescribed.

18. The Hon’ble Supreme Court has taken a view that if in absence of any material to conclude that there was failure on the part of assessee to either fully and/or truly disclose materials required for assessment, the machinery under Section 147 (of Income Tax Act, 1961) cannot be invoked beyond the period of four years. The Hon’ble Supreme Court has also held that if there is a change of opinion, the Department cannot resort to Section 147 (of Income Tax Act, 1961).

19. From the facts of the case, it is evident that petitioner had claimed Long-Term Capital Gains under Section 54 (of Income Tax Act, 1961), in his return filed for the Assessment Year 2009-10 on 30.07.2009. Before the assessment was completed, the petitioner was called upon to furnish evidence in support of his claim for deduction under Section 54 (of Income Tax Act, 1961) vide letter dated 09.09.2011.

20. By a reply dated 03.10.2011, the petitioner partly furnished certain informations followed by another letter dated 20.10.2011. In the reply/representation dated 20.10.2011 following documents were furnished:-

i. A sheet containing the workings for capital gains on sale of residential house is enclosed (Annexure 1). Kindly note that while computing the capital gains the cost inflation index for the financial year 2008-09 was inadvertently taken as 551 instead of 582. Hence the capital gains was shown as Rs.41,39,650 as against an amount of Rs.37,24,891.

ii. Copy of the deposit receipt evidencing deposit of Rs.50 lakhs in Capital Gains Account Scheme before the due date of filing of return is enclosed (Annexure 2).

iii. Copy of the sale deed evidencing sale of residential house is enclosed as Annexure 3.

iv. Copy of the sale agreement in connection with the purchase of the residential flat along with a copy of the registered deed is enclosed evidencing the cost of acquisition of the flat (Annexure 4).

21. Therefore, on this issue, the respondent cannot proceed to pass an order under Section 147 (of Income Tax Act, 1961) by treating the sale of house property in Mumbai was a short-term capital gains in the light of the decision of the Hon’ble Supreme Court in the Kelvinator of India’s case referred to supra.

22. The respondent will have to therefore pass an order dropping the proposal contained in the notice dated 13.03.2016 on this issue as it cannot be said that income chargeable to tax had escaped assessment by reason of the failure on the part of the petitioner to either make a return under Section 139 (of Income Tax Act, 1961) or in response to a notice issued under Section 142(1) (of Income Tax Act, 1961) or Section 148 (of Income Tax Act, 1961) to disclose fully and truly all material facts necessary for his assessment.

23. At the same time, while dropping the proposal contained in the notice invoking Section 148 (of Income Tax Act, 1961), the rights of the respondent to exercise the power in terms of Explanation 3 to Section 147 (of Income Tax Act, 1961) cannot be curtailed.

24. The issue of notice under Section 148 (of Income Tax Act, 1961) for the purpose of passing an order of re-assessment Section 147 (of Income Tax Act, 1961) has to merely satisfy the requirement of Section 149 (of Income Tax Act, 1961) to 151 of the Income Tax Act, 1961.

25. At the same time, while passing orders under Section 147 (of Income Tax Act, 1961), an Assessing Officer is required to keep in mind the settled principles of law on the subject. If there is a change of opinion which prompted the issue of the notice under Section 148 (of Income Tax Act, 1961), the officer while passing order under Section 147 (of Income Tax Act, 1961) can not proceed further. Proviso to Section 147 (of Income Tax Act, 1961) makes it clear that no action shall be taken under it, unless any income chargeable to tax has escaped assessment for such assessment year by reason of the failure on the part of the assessee to make a return under Section 139 (of Income Tax Act, 1961) or in response to a notice issued under sub-section (1) of Section 142 (of Income Tax Act, 1961) or Section 148 (of Income Tax Act, 1961) or to disclose fully and truly all material facts necessary for his assessment, for that assessment year.

26. While conducting proceedings, an Assessing Officer is bound by the proviso to Section 147 (of Income Tax Act, 1961). Therefore, while exercising the powers vested with an officer at the time of re-assessment under Section 147 (of Income Tax Act, 1961) pursuant to issue notice under Section 148 (of Income Tax Act, 1961), the officer concerned has to not only keep in mind the express language of the proviso to Section 147 (of Income Tax Act, 1961) but also well settled principles of law.

27. In the light of the above discussion the writ petition is disposed with the following directions / observations:-

i. The respondent cannot have a re-look into the issue arising out of the claim of the petitioner for Long-Term Capital Gains which was allowed in the assessment order passed on 29.10.2011 as there was true and full disclosure of all material required for assessment by the petitioner for claiming deduction;

ii. Therefore, the proposal to re-determine the taxable income and the tax payable by the petitioner for the reasons stated in the impugned communication is unsustainable.;

iii. At the same time, while passing final order under Section 147 (of Income Tax Act, 1961), the respondent can examine any other aspect for escaped assessment of tax in the light of Explanation 3 to Section 147 (of Income Tax Act, 1961).

iv. While passing such order, the respondent shall not disturb the deduction allowed under Section 54 (of Income Tax Act, 1961) in the assessment order dated 29.10.2011.

v. Since the dispute pertains to the assessment year 2009-10, the respondent is hereby directed to pass appropriate order within a period of thirty days from date of receipt of a copy of this order without disturbing the claim of the petitioner for Long-Term Capital Gains allowed under Section 54 (of Income Tax Act, 1961).

vi. No cost.

vii.Consequently, connected Miscellaneous Petitions are closed.

×

Similar Ripples

Questions

Court Quashes Tax Reassessment Notice, Upholds Long-Term Capital Gains Claim

Write your CommentSimilar Posts

Generic

- Reportdata/6054.pdf