Court Quashes Tax Reassessment Notice: Vague Reasons and Lack of Evidence Doom …

Full News

Court Quashes Tax Reassessment Notice: Vague Reasons and Lack of Evidence Doom Revenue's Case

Court Quashes Tax Reassessment Notice: Vague Reasons and Lack of Evidence Doom Revenue's Case

Jayesh Govindbhai Balar challenged a notice from the Income Tax Officer. The tax folks wanted to reopen his assessment for the 2008-09 year, but the High Court said, "Nope, not happening!" They quashed the notice because the tax officer's reasons were too vague and lacked solid evidence.

Get the full picture - access the original judgement of the court order here

Case Name:

Jayesh Govindbhai Balar vs Income Tax Officer (High Court of Gujarat)

Special Civil Application No. 994 of 2016

Date: 13th June 2016

Key Takeaways:

1. Tax authorities need solid, specific reasons to reopen assessments, especially after four years.

2. Vague assumptions about income based on property transactions aren't enough.

3. The court emphasized the importance of disclosing all material facts in tax returns.

4. Reopening assessments requires both evidence of escaped income and failure to disclose by the assessee.

Issue:

The main question here was: Did the Income Tax Officer have valid reasons to reopen Jayesh's tax assessment for 2008-09, especially when doing so after four years?

Facts:

1. Jayesh filed his 2008-09 tax return showing an income of about 2.44 lakh rupees.

2. The tax officer did a scrutiny assessment and finalized his income at 2.41 lakh rupees.

3. In his return, Jayesh disclosed buying two properties worth about 61.76 lakh and 54.59 lakh rupees (but he only owned part of these).

4. Jayesh also sold a property for 33.97 lakh rupees but didn't mention it in this return. He had actually reported it in his 2007-08 return.

5. On March 27, 2015 (more than four years later), the tax officer issued a notice to reopen the assessment.

Arguments:

Jayesh's side:

- He disclosed the property purchases in his return, and the tax officer knew about them.

- He reported the property sale in the previous year's return, which was already assessed.

- The tax officer's reasons for reopening were vague and illogical.

Tax Department's side:

- Jayesh didn't disclose the property sale in the 2008-09 return.

- The high-value transactions suggest he might have more income than reported.

Key Legal Precedents:

The judgment doesn't mention specific case laws, but it refers to some well-established principles:

1. Reasons for reopening must be in the recorded notes, not from outside material.

2. For reopening after four years, two conditions must be met:

a) Tangible material showing escaped income

b) Failure by the assessee to disclose all material facts fully and truly

Judgement:

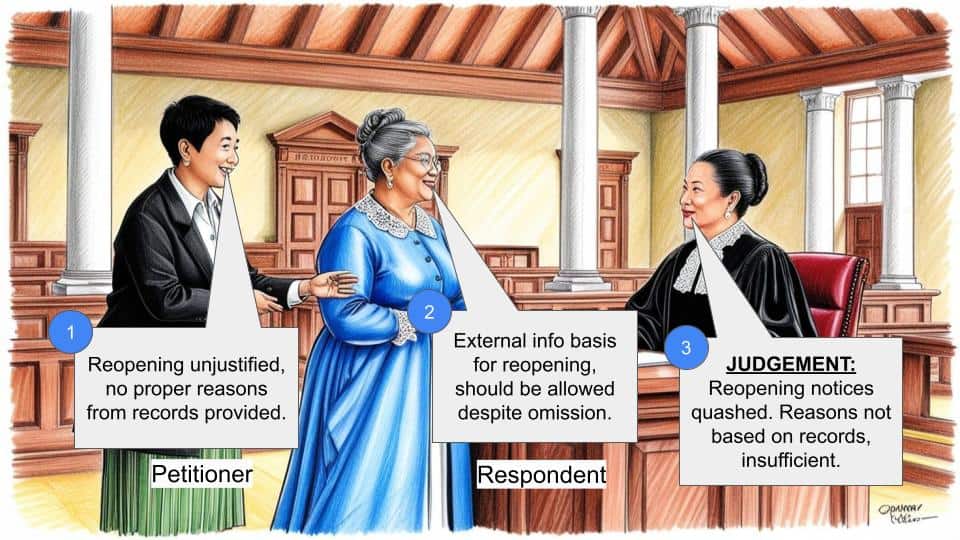

The court sided with Jayesh and quashed the reopening notice. Here's why:

1. The tax officer's reasons were vague and based on assumptions.

2. There's no direct link between property purchases and income disclosure.

3. The property sale, though not disclosed in 2008-09, was reported and taxed in 2007-08.

4. The tax officer didn't explain how he believed income had escaped assessment.

5. When the first condition (tangible evidence of escaped income) isn't met, the second condition (failure to disclose) doesn't matter.

FAQs:

1. Q: Can tax authorities reopen assessments after four years?

A: Yes, but they need strong reasons and evidence of income escaping assessment due to non-disclosure by the taxpayer.

2. Q: Does buying expensive property automatically mean higher taxable income?

A: No, the court said there's no direct correlation. Tax officers can't make such assumptions without evidence.

3. Q: What if I report a transaction in the wrong year's tax return?

A: While it's best to report in the correct year, the court considered that the transaction was disclosed and taxed, even if in a different year.

4. Q: What makes reasons for reopening an assessment "vague"?

A: In this case, the tax officer's assumptions without specific evidence of how income escaped assessment were considered vague.

5. Q: How important is it to disclose all transactions in tax returns?

A: It's crucial. Even though Jayesh won this case, the court emphasized the importance of full and true disclosure of all material facts.

1. The petitioner has challenged a notice dated 27.03.2015 issued by the respondent Assessing Officer by which he seeks to reopen the assessment of the petitioner for the assessment year 2008-09.

2. Brief facts are as under.

3. The petitioner is an individual. For the assessment year 200809, the petitioner had filed the return of income on 30.03.2009 declaring total income of Rs.2.44 lacs (rounded off). The return was taken in scrutiny. The Assessing Officer passed order of assessment on 22.12.2010 assessing income of the assessee at Rs.2.41 lacs (rounded off).

4. In the return of income, the assessee had disclosed purchases of two immovable properties made by him during the relevant previous year at a cost of Rs.61.76 lacs (rounded off) and Rs.54.59 lacs along with two other persons. The assessee however, had also sold an immovable property under a deed dated 19.07.2007 for sale consideration of Rs.33.97 lacs (rounded off). He had not disclosed this sale in the return for the assessment year 200809, but, had done so in the return filed for the assessment year 2007 08.

5. In order to reopen the assessment for the said assessment year 200809, the Assessing Officer issued impugned notice, which as can be seen, was done beyond the period of four years from the end of relevant assessment year. In order to do so, the Assessing Officer recorded reasons which read as under:

“As per AIR Information received in this office, in this case Shri. Jayeshbhai Govindbhai Balar having transaction of purchase of two immovable properties valued at Rs.61,76,500/ and Rs.54,59,000/ with two other personas. Shri Jayeshbhai Govindbhai Balar had also sold the immovable property valued at Rs.33,97,858/, it is also found that the assessee has filed his return of income for A.Y.200809 showing income Rs.2,44,120/ where as the assessee indulged in transaction of purchase of two immovable properties valued at Rs.61,76,500/ and Rs.54,59,000/ and also in transaction of sale of the immovable property valued as Rs.33,97,858/. In view of the above I have reason to believe that the assessee has filed his return of income Rs.2,44,120/ only, whereas the assessee has earned much more income from his transaction.

In view of the above I have reason to believe that income to the extent of huge transaction of Rs.1,16,35,500/ and transaction of sale property valued at Rs.33,97,858/ has escaped assessment for A.Y. 200809, by reason of failure on the part of the assessee to disclose fully and truly all the material facts necessary in the return of income. Hence, notice u/s. 148 (of Income Tax Act, 1961) r.w.s. 147 (of Income Tax Act, 1961) is to be issued for the A.Y. 200809.

I am therefore, Satisfied that this is a fit case for invoking the provisions of section 147 (of Income Tax Act, 1961) of the Income – Tax Act, 1961 for A.Y.200809.”

6. Learned counsel Shri Soparkar for the petitioner submitted that purchases of two immovable properties were duly reflected in the assesse's return. These transactions were noticed by the Assessing Officer in the original assessment proceedings. There was no failure on the part of the assessee to disclose material facts. He further pointed out that the assessee was not the sole purchaser and that the share of the assessee was of 49.65% of these two properties which was duly reflected in the return also.

7. With respect to the sale of the property by the petitioner, counsel submitted that though the sale deed was executed on 19.07.2007, on account of the transfer being an ongoing transaction, the petitioner had treated the effective sale falling within the assessment year 200708 and had accordingly declared the same in the return filed for the said year. The Assessing Officer had also examined the details of the sale.

8. On the other hand, learned counsel Shri Mehta for the department submitted that the assessee had not disclosed the sale of the immovable property made during the period relevant to the assessment year 200809 and had thus, not provided the correct information about the income. The Assessing Officer had therefore correctly reopened the assessment.

9. It is by now well settled that to support a notice for reopening of assessment, the justification must come from the reasons recorded by the Assessing Officer for issuing such notice. The Assessing Officer cannot rely on any material outside the reasons recorded in order to support his conclusion that income chargeable to tax had escaped assessment or that the same was on account of failure on the part of the assessee to disclose truly and fully all material facts.

10. In this context, if we revert to the reasons recorded, they contain two elements. The assessee had purchased two immovable properties valued at Rs.61.76 lacs and Rs.54.59 lacs respectively, whereas, he had filed return disclosing income of Rs.2.47 lacs only. The Assessing Officer was of the opinion that when assessee had purchased two properties at such sizable cost, he could not have shown income of only Rs.2.44 lacs. He therefore, concluded that 'income to the extent of huge transaction of Rs.1,16,35,500/ ... had escaped assessment for AY 200809 ...'. This reason completely lacks logic. There is no direct co- relation between the purchase of properties by the assessee and his disclosure of the income during a particular period. The reason is vague and relies on the presumptions on the part of the Assessing Officer. He seems to be presuming that when the assessee had made purchase worth such huge amounts, he must disclose sizable income. Additionally, these purchases had come up for discussion by the Assessing Officer in the original scrutiny.

11. With respect to the assessee's sale of land valued at Rs.33.97 lacs, it is true that the same was not disclosed in the returns filed. The assessee had however, shown the sale in the earlier assessment year 200708. Such transaction was examined and duly taxed during such period. Apart from this, with respect to this transaction also the Assessing Officer has not recorded any reasons pointing out as to in what manner he formed a belief that the income chargeable to tax had escaped assessment. He merely stated that the assessee had indulged in transaction of sale of immovable property valued at Rs.33.97 lacs, but shown income only of Rs.2.44 lacs and therefore, he had reason to believe that income concerning huge transaction cost had escaped assessment. Once again, the reasons are vague and imprecise and lack invalidity. If the Assessing Officer was primafacie of the opinion that sale transaction invited capital gain which the assessee had avoided by nondisclosure, the same has not come on record in the reasons.

12. When notice for reopening for scrutinized assessment is issued beyond the period of four years, twin conditions to be satisfied are that the Assessing Officer has some tangible material to form a belief that income chargeable to tax has escaped assessment and further that such escapement was due to failure on part of the assessee to disclose truly and fully all material facts. When first of these conditions is not satisfied, merely because the assessee failed to disclose the sale transaction would not by itself give authority to Assessing Officer to reopen the assessment.

13. In the result, petition is allowed. Impugned notice dated 27.03.2015 is quashed. Petition is disposed of.

(AKIL KURESHI, J.)

(A.J. SHASTRI, J.)

×

Similar Ripples

Questions

Court Quashes Tax Reassessment Notice: Vague Reasons and Lack of Evidence Doom Revenue's Case

Write your CommentSimilar Posts

Generic

- Reportdata/2773.pdf