Court Rejects Income Tax Reassessment, Upholds 'Reason to Believe' Principle

Full News

Court Rejects Income Tax Reassessment, Upholds 'Reason to Believe' Principle

Court Rejects Income Tax Reassessment, Upholds 'Reason to Believe' Principle

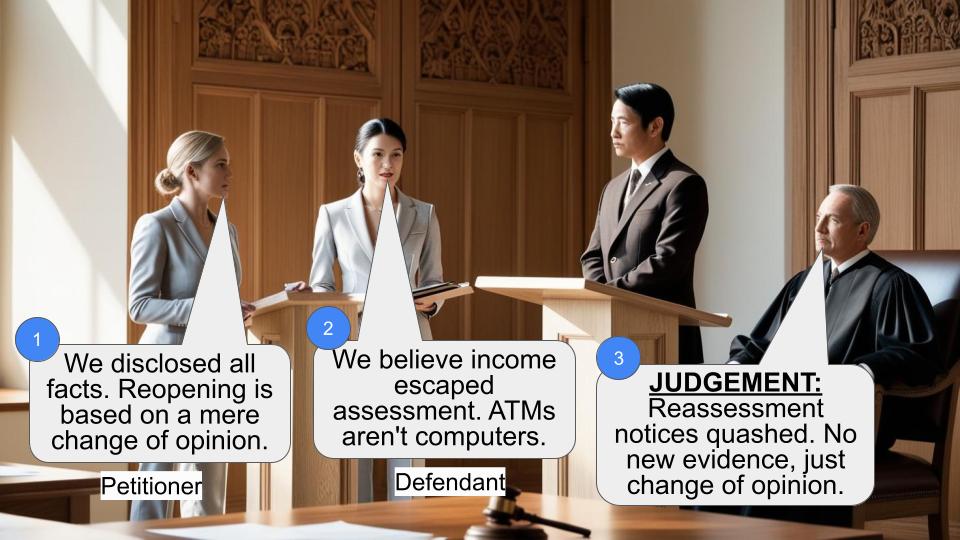

This case involves an appeal by the Principal Commissioner of Income Tax against M/s Swaraj Engines Ltd. The Income Tax Appellate Tribunal had ruled that the Income Tax Department wrongly issued a reassessment notice under Section 148 (of Income Tax Act, 1961). The High Court dismissed the appeal, affirming that a mere change of opinion does not constitute a valid reason for reassessment.

Get the full picture - access the original judgement of the court order here

Case Name:

Principal Commissioner of Income Tax vs M/s Swaraj Engines Ltd. (High Court of Punjab & Haryana)

ITA-266-2016 (O&M)

Date: 3rd February 2020

Key Takeaways:

1. Reassessment under Section 147 (of Income Tax Act, 1961) requires "reason to believe" and cannot be based on a mere change of opinion.

2. An explanation to a section in law is subordinate to the main provision and cannot override it.

3. The court emphasized the importance of maintaining the distinction between the power to review and the power to reassess.

Issue:

Can the Income Tax Department initiate reassessment proceedings under Section 147 (of Income Tax Act, 1961) based solely on a change of opinion regarding a previously scrutinized issue?

Facts:

1. The assessee, M/s Swaraj Engines Ltd., claimed a deduction under Section 80-I (of Income Tax Act, 1961) in the assessment year 1997-1998.

2. During the original assessment under Section 143(3) (of Income Tax Act, 1961), the Assessing Officer examined the deduction claim in detail and partially disallowed it.

3. Later, the Income Tax Department issued a notice under Section 148 (of Income Tax Act, 1961), claiming that the benefit of Section 80-I (of Income Tax Act, 1961) had been wrongly extended.

4. The Income Tax Appellate Tribunal set aside the reassessment order, stating that the primary condition of "reason to believe" under Section 147 (of Income Tax Act, 1961) was not met.

Arguments:

Appellant (Income Tax Department):

- Argued that sub-clause (c) of Explanation 2 to Section 147 (of Income Tax Act, 1961) permits reassessment in cases where income has been under-assessed or excessive relief has been given.

Respondent (M/s Swaraj Engines Ltd.):

- Contended that Explanation 2 must be read subject to the main provision of Section 147 (of Income Tax Act, 1961) and cannot be treated as an exception.

- Argued that a mere change of opinion cannot be considered as "reason to believe" for initiating reassessment.

Key Legal Precedents:

1. Commissioner of Income-Tax vs. Kelvinator of India Ltd and Another; 2010 (320) ITR 561 (SC):

- The Supreme Court held that the concept of "change of opinion" is an in-built test to check abuse of power by the Assessing Officer.

- Reassessment must be based on "tangible material" indicating escapement of income.

Judgement:

1. The High Court dismissed the appeal by the Income Tax Department.

2. The court agreed with the respondent's argument that Explanation 2 to Section 147 (of Income Tax Act, 1961) is subordinate to the main provision and cannot override it.

3. The court emphasized that a mere change of opinion cannot be considered within the ambit of "reason to believe" for initiating reassessment.

4. The court noted that if the revenue was aggrieved by the original assessment order, it should have pursued remedies under Section 263 (of Income Tax Act, 1961) rather than attempting a "short cut method" through reassessment.

FAQs:

Q1: What is the significance of "reason to believe" in income tax reassessment cases?

A1: "Reason to believe" is a crucial condition for initiating reassessment under Section 147 (of Income Tax Act, 1961). It requires the Assessing Officer to have tangible material indicating escapement of income, rather than merely changing their opinion on a previously scrutinized issue.

Q2: Can the Income Tax Department reassess a case based on a change of opinion?

A2: No, the court has clearly stated that a mere change of opinion cannot be the basis for reassessment. There must be new, tangible material that gives the Assessing Officer reason to believe income has escaped assessment.

Q3: What options does the Income Tax Department have if they disagree with an original assessment?

A3: If the Department is aggrieved by an original assessment order, they should pursue remedies under Section 263 (of Income Tax Act, 1961), which deals with revision of orders prejudicial to revenue, rather than attempting reassessment under Section 147 (of Income Tax Act, 1961).

Q4: How does this judgment impact future income tax reassessment cases?

A4: This judgment reinforces the principle that reassessment cannot be used as a tool to review past decisions. It emphasizes the need for new, tangible material to justify reopening an assessment, thereby providing greater certainty to taxpayers against arbitrary reassessments.

This appeal has been filed against the order of the Income Tax Appellate Tribunal Chandigarh Bench 'A' Chandigarh dated 22.03.2016 holding that the issue of allowance of Section 80-I (of Income Tax Act, 1961) (for short 'the Act') had wrongly been given to the assessee.

2. The brief facts are that assessee had claimed the deduction under Section 80-I (of Income Tax Act, 1961) in the year 1997-1998. In the final assessment under Section 143(3) (of Income Tax Act, 1961), the issue of this deduction was gone into detail by the A.O and a portion of it was disallowed. Thereafter notice under Section 148 (of Income Tax Act, 1961) was issued to the assessee claiming that the benefit of Section 80-I (of Income Tax Act, 1961) had wrongly been extended. Ultimately the Tribunal set aside this order holding that the primary condition of Section 147 (of Income Tax Act, 1961) viz 'reason to believe' (as defined by a plethora of judgments) did not exist and it was merely a case of change of opinion at best, which could not be permitted.

3. The argument of learned counsel for the appellant is that sub- clause-c of explanation 2 to Section 147 (of Income Tax Act, 1961) permits this. The said sub-clause is quoted here-in-below:

“147. Income escaping assessment 2 If the Assessing Officer has reason to believe] that any income chargeable to tax has escaped assessment for any assessment year, he may, subject to the provisions of sections 148 to 153, assess or reassess such income and also any other income chargeable to tax which has escaped assessment and which comes to his notice subsequently in the course of the proceedings under this section, or recompute the loss or the depreciation allowance or any other allowance, as the case may be, for the assessment year concerned (hereafter in this section and in sections 148 to 153 referred to as the relevant assessment year): Provided that where an assessment under sub- section (3) of section 143 (of Income Tax Act, 1961) or this section has been made for the relevant assessment year, no action shall be taken under this section after the expiry of four years from the end of relevant assessment year, unless any income chargeable to tax has escaped assessment for such assessment year by reason of the failure on the part of the assessee to make a return under section 139 (of Income Tax Act, 1961) or in response to a notice issued under sub- section (1) of section 142 (of Income Tax Act, 1961) or section 148 (of Income Tax Act, 1961) or to disclose fully and truly all material facts necessary for his assessment for that assessment year. Explanation 1-Production before the Assessing Officer of account books or other evidence from which material evidence could, with due diligence, have been discovered by the Assessing Officer will not necessarily amount to disclosure within the meaning of the foregoing proviso.

Explanation 2.- For the purposes of this section, the following shall also be deemed to be cases where income chargeable to tax has escaped assessment, namely:-

(c) where an assessment has been made, but-

(i) income chargeable to tax has been under- assessed; or

(ii) such income has been assessed at too low a rate; or

(iii) such income has been made the subject of excessive relief under this Act; or

(iv) excessive loss or depreciation allowance or any other allowance under this Act has been computed.”

4. On the other hand the stand of learned Senior Counsel appearing for the assessee is that explanation 2 can only be read subject to main provision of Section 147 (of Income Tax Act, 1961) and the interpretation which the learned counsel for the appellant is trying to give to it would give it an existence of an exception rather than an explanation.

5. We find this argument to be well merited. It is trite to say that an explanation is always subordinate to the main provision (as the name suggests, only to explain). In the present case we find that the powers under Section 147 (of Income Tax Act, 1961) have been now defined without any equivocation and without going to deep into it it is safe to say that a mere change of opinion cannot be considered within the ambit of phrase reason to believe.

6. Learned counsel for the petitioner has tried to take us to the merits of the case and to show how the deduction could not have been claimed but we are unable to into the merits of the case because she has not been able to deny that in the original order under Section 143(3) (of Income Tax Act, 1961), the issue of deduction did arise and after discussing the same a particular finding was given. Had the revenue been aggrieved of the assessment order passed under Section 143(3) (of Income Tax Act, 1961), it would had the recourse under Section 263 (of Income Tax Act, 1961) but the present short cut method cannot be allowed.

7. Learned counsel for the appellant has relied upon Commissioner of Income-Tax vs. Kelvinator of India Ltd and Another; 2010 (320) ITR 561 (SC) and particularly to the following part of the judgment:

“On going through the changes, quoted above, made to Section 147 (of Income Tax Act, 1961), we find that, prior to Direct Tax Laws (Amendment) Act, 1987, re-opening could be done under above two conditions and fulfillment of the said conditions alone conferred jurisdiction on the Assessing Officer to make a back assessment, but in section 147 (of Income Tax Act, 1961) [with effect from 1st April, 1989], they are given a go-by and only one condition has remained, viz., that where the Assessing Officer has reason to believe that income has escaped assessment, confers jurisdiction to re- open the assessment. Therefore, post-1st April, 1989, power to re-open is much wider. However, one needs to give a schematic interpretation to the words "reason to believe" failing which, we are afraid, Section 147 (of Income Tax Act, 1961) would give arbitrary powers to the Assessing Officer to re-open assessments on the basis of "mere change of opinion", which cannot be per se reason to re- open. We must also keep in mind the conceptual difference between power to review and power to re-assess. The Assessing Officer has no power to review; he has the power to re-assess. But re-assessment has to be based on fulfillment of certain pre- condition and if the concept of "change of opinion" is removed, as contended on behalf of the Department, then, in the garb of re-opening the assessment, review would take place. One must treat the concept of "change of opinion" as an in-built test to check abuse of power by the Assessing Officer. Hence, after 1st April, 1989, Assessing Officer has power to re-open, provided there is "tangible material" to come to the conclusion that there is escapement of income from assessment. Reasons must have a live link with the formation of the belief. Our view gets support from the changes made to Section 147 (of Income Tax Act, 1961), as quoted hereinabove. Under the Direct Tax Laws (Amendment) Act, 1987, Parliament not only deleted the words "reason to believe" but also inserted the word "opinion" in Section 147 (of Income Tax Act, 1961). However, on receipt of representations from the Companies against omission of the words "reason to believe", Parliament re-introduced the said expression and deleted the word "opinion" on the ground that it would vest arbitrary powers in the Assessing Officer. We quote hereinbelow the relevant portion of Circular No.549 dated 31st October, 1989, which reads as follows:

"7.2 Amendment made by the Amending Act, 1989, to reintroduce the expression `reason to believe' in Section 147 (of Income Tax Act, 1961).--A number of representations were received against the omission of the words `reason to believe' from Section 147 (of Income Tax Act, 1961) and their substitution by the `opinion' of the Assessing Officer. It was pointed out that the meaning of the expression, `reason to believe' had been explained in a number of court rulings in the past and was well settled and its omission from section 147 (of Income Tax Act, 1961) would give arbitrary powers to the Assessing Officer to reopen past assessments on mere change of opinion. To allay these fears, the Amending Act, 1989, has again amended section 147 (of Income Tax Act, 1961) to reintroduce the expression `has reason to believe' in place of the words `for reasons to be recorded by him in writing, is of the opinion'. Other provisions of the new section 147 (of Income Tax Act, 1961), however, remain the same." For the afore-stated reasons, we see no merit in these civil appeals filed by the Department, hence, dismissed with no order as to costs.”

8. The contention of learned counsel for the appellant is that the phrase 'conceptual difference' between power to review and power to reassess, some how changes the law. This argument is flawed because their Lordships' have merely reiterated that invocation of Section 147 (of Income Tax Act, 1961) can only be on the basis of tangible material which has come to the knowledge of the assessing officer after the assessment.

9. The question of law does not arise.

10. Dismissed.

[AJAY TEWARI]

JUDGE

[AVNEESH JHINGAN]

JUDGE

×

Similar Ripples

Questions

Court Rejects Income Tax Reassessment, Upholds 'Reason to Believe' Principle

Write your CommentSimilar Posts

Generic

- Reportdata/6079.pdf