Court Rejects Taxpayer's Claim on Property Acquisition Date, Upholds Tax Assess…

Full News

Court Rejects Taxpayer's Claim on Property Acquisition Date, Upholds Tax Assessment

Court Rejects Taxpayer's Claim on Property Acquisition Date, Upholds Tax Assessment

This case involves Kewal Krishna Loroiya (the assessee) challenging the Income Tax Appellate Tribunal's decision regarding the calculation of capital gains tax on a property sale. The main dispute was about when the property legally became the assessee's, affecting the cost of acquisition calculation. The High Court upheld the Tribunal's decision, rejecting the assessee's arguments.

Get the full picture - access the original judgement of the court order here

Case Name:

Kewal Krishna Loroiya vs Income Tax Officer (High Court of Allahabad)

Income Tax Appeal No.95 of 2015

Date: 16th January 2017

Key Takeaways:

1. Mere registration fee payment doesn't constitute property ownership.

2. The date of allotment is crucial for determining when a property becomes an asset.

3. The court emphasized the importance of having superior interest and right to possess for property ownership.

4. Valuation reports from multiple sources can be considered for determining improvement costs.

Issue:

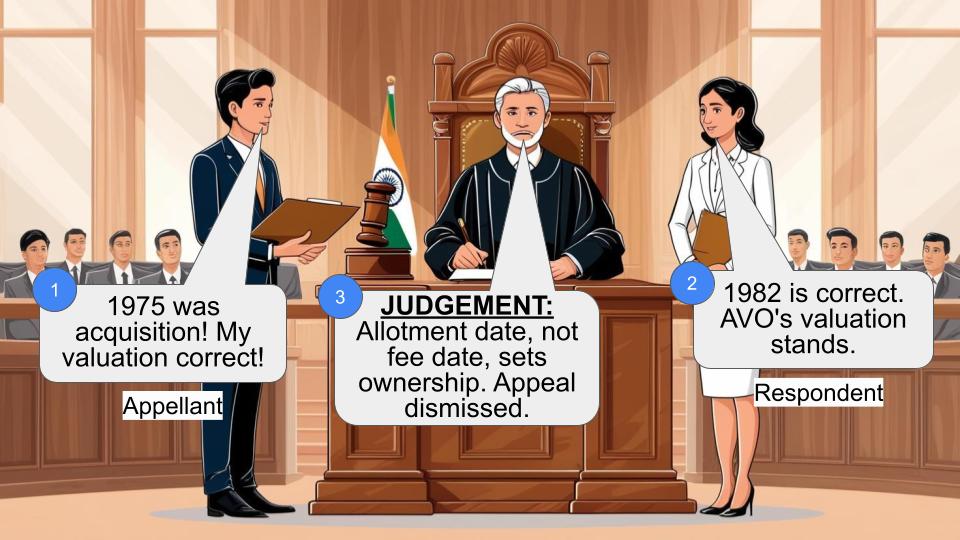

Did the property become the assessee's asset in 1975 when he paid the registration fee, or in 1982 when it was officially allotted to him by UP Awas Evam Vikas Parishad (UP AEVP)?

Facts:

1. In 1975, Loroiya paid a registration fee of Rs. 5,000 to UP AEVP for property allotment.

2. The property was officially allotted to him on 29.04.1982.

3. Loroiya sold the property on 28.03.2009 for Rs. 32,50,000, but the stamp value was Rs. 40,35,560.

4. The assessee claimed various improvements and additions to the property over the years.

5. The case went through multiple levels of appeal, including the Income Tax Appellate Tribunal.

Arguments:

Assessee's arguments:

1. The property became his asset in 1975 when he paid the registration fee.

2. This would allow him to use the fair market value as of 01.04.1981 for cost of acquisition under Section 55(2)(b) (of Income Tax Act, 1961).

3. The valuation of improvements by his private valuer should be accepted.

Tax Department's arguments:

1. The property only became the assessee's asset when it was allotted in 1982.

2. The Assistant Valuation Officer's (AVO) report should be considered for valuation of improvements.

Key Legal Precedents:

The judgment doesn't explicitly cite specific case laws, but it relies heavily on the interpretation of Section 55(2)(b) (of Income Tax Act, 1961).

Judgement:

1. The court ruled in favor of the Tax Department, upholding the Tribunal's decision.

2. It was determined that the property became the assessee's asset only on 29.04.1982 when it was allotted, not in 1975 when the registration fee was paid.

3. The court found no infirmity in the Tribunal's view on the date of acquisition.

4. Regarding the valuation of improvements, the court found no reason to interfere with the AVO's assessment, considering that even the assessee's new valuer provided a figure close to the AVO's valuation.

FAQs:

1. Q: Why didn't the court accept 1975 as the date of acquisition?

A: The court held that merely paying a registration fee doesn't constitute property ownership. There must be a superior interest and right to possess the property.

2. Q: How does this judgment affect the calculation of capital gains?

A: It means the assessee can't use the fair market value as of 01.04.1981 for cost of acquisition, potentially resulting in higher taxable capital gains.

3. Q: Why did the court prefer the AVO's valuation over the assessee's private valuer?

A: The court noted that even a second valuer hired by the assessee provided a figure closer to the AVO's valuation, lending credibility to the AVO's assessment.

4. Q: What's the significance of this judgment for other taxpayers?

A: It clarifies that for properties allotted by government agencies, the date of allotment, not the date of initial payment, is crucial for determining when the property becomes an asset for tax purposes.

5. Q: Can taxpayers still challenge property valuations by tax authorities?

A: Yes, but this case shows that courts may give weight to official valuations, especially if supported by multiple assessments.

1. Heard Sri Abhinav Mehrotra, learned Counsel for the appellant and Sri Ghanshyam Choudhary, learned Counsel for the respondent.

2. This appeal under Section 260-A (of Income Tax Act, 1961) (hereinafter referred to as the "Act, 1961") has arisen from judgment and order dated 16.04.2015 passed by Income Tax Appellate Tribunal, Lucknow (hereinafter referred to as “Tribunal”) in I.T.A. No. 521/Lkw./2013 relating to Assessment Year 2009-10 (hereinafter referred to as “AY 2009-10”).

3. Appeal was admitted on the following substantial questions of law :-

"(i) Whether on a true and correct interpretation of the expression "became the property of the assessee", as appearing in Section 55(2)(b) (of Income Tax Act, 1961), viz a viz the expression "ownership rights", the order of the Tribunal is in accordance with law, while determining the Cost of Acquisition of the Capital Asset?

(ii) Whether the order of the Ld. ITAT, in so far as the determination of the indexed cost of Acquisition of the Capital Asset is concerned, is in accordance with law?"

4. Brief facts necessary for proper appreciation of the aforesaid issues may be narrated as under :-

(i) For the AY 2009-10, Kewal Krishna Loroiya filed Return of income on 29.05.2009 showing total income of Rs. 1, 84,330/-. Case was selected for scrutiny through CASS under Section 143 (of Income Tax Act, 1961)

(3) of Act, 1961. A notice under Section 143(2) (of Income Tax Act, 1961) was issued on 23.09.2010. Subsequently notice under Section 142(1) (of Income Tax Act, 1961) also issued on 26.07.2011 and on non-compliance, a fresh notice on 05.08.2011 under Section 142(1) (of Income Tax Act, 1961) was issued.

(ii) Assessee through its Authorized Representative, appeared before Assessing Authority and besides other, explained the issue of ‘capital gain’ from sale of house stating that sale deed for House No. A-331, Indira Nagar, Lucknow was executed on 28.03.2009 for a sale consideration of Rs. 32,50,000/-. However, stamp value of property was taken in sale deed, as Rs. 40,35,560/-. The said house was allotted to Assessee by UP Awas Evam Vikas Parishad (hereinafter referred to as “UP AEVP”) on 29.04.1982 vide letter no. 4265. Assessee subsequently transferred the said house in the name of his wife Smt. Santosh Laroiya. A deed in favour of Assessee’s wife was executed on 22.11.1994. However, after the death of Assessee’s wife on 05.06.2002, the property again stood transferred to Assessee.

(iii) It was claimed that property was purchased on installments basis from UP AEVP and installments / payment was made from 01.07.1975 to 10.09.2008. Cost of acquisition of house was shown in the reply submitted by Assessee on 16.11.2011 at Rs. 2,82,265/-.

(iv) It appears that Assessee also got a letter dated 23.04.2009 from UP AEVP to furnish certain information and the same was submitted by Assessee before Assessing Authority along-with his reply dated 11.11.2011, which shows that a sum of Rs. 5000/- was paid by Assessee on 29.01.1975 and thereafter a lump-sum amount of Rs. 8858/- was deposited on 12.05.1982 and then installment of Rs. 1821/- were paid monthly. Some times, two months installments together were paid, therefore, payment had continued up to 29.04.1992 and thereafter three payments were made as under:

Rs. 5000/- on 28.12.1992, Rs. 15000/- on 27.05.1993 and Rs. 1000/- on 10.09.2008.

(v) UP AEVP also informed for stamp duty of Rs. 20,990/- which was paid in addition to the amount paid and thus total cost of acquisition including stamp duty and registry charges came to Rs. 10,03,449/-.

(vi) When the sale deed was executed by Assessee in Financial Year 1994-95 (hereinafter referred to as “FY 1994-95”), stamp duty of Rs. 15450/- and registry charges of Rs. 5000/- were paid. Assessing Authority for FY 2008-09 worked out index cost of acquisition of property at Rs. 10,03,449/-. Assessee also claimed certain further investments in the house in question in 1982-83 to the tune of Rs. 2,80,000/- and in support thereof a number of valuation reports were furnished in evidence. Assessing Authority sought valuation report from Official Valuation who, in report dated 28.11.2012, worked out indexed cost of improvement as Rs. 10,67,890/-. Thereafter for valuation of property in dispute Assessee furnished his objection on 21.12.2011 and requested that a reference be made to Assistant Valuation Officer of Department (hereinafter referred to as “AVO”) for ascertaining fair market value of property in question on the date of sale i.e. 28.03.2009. Consequently reference was made under Section 50-C(2) (of Income Tax Act, 1961),pursuant where to AVO in the report dated 28.12.2011, valued property as on 28.03.2009 as Rs. 47.70 lacs. Since valuation was more than the stamp value of property, Assessing Authority accepted market value at its stamp value i.e. Rs. 40,35,560/- and subscribing indexed cost of acquisition of Rs. 10,03,449 and indexed cost of improvement of Rs. 10,67,890/-, worked out long term ‘capital gain’ at Rs. 19,64,221. The final assessment order was passed by Assessing Authority on 30.12.2011 working out long term capital gain of Rs. 19,64,221/-, besides other items.

(vii) Assessee, being aggrieved, preferred appeal before Commissioner of Income Tax (Appeals)-I, Lucknow (hereinafter referred to as “CIT(A)”) being Appeal No. CIT(A)-I/Lko/11- 12/146. Commissioner confirmed sale consideration of disputed property by computing ‘capital gains’ at Rs. 40,35,560/- and rejected objection of Assessee with regard to the report of AVO.

(viii) Assessee then took the matter in appeal before Tribunal in ITA No. 521/Lkw/2013 but there also he has failed since Tribunal has dismissed appeal.

5. Sri Abhinav Mehrotra, learned Counsel for the appellant drew our attention to Section 55(2)(b) (of Income Tax Act, 1961) and contends that Clause – I which refers to ‘capital gains’ of assets before 01.04.1981, would mean the cost of acquisition of assets to Assessee on the fair market value on 01.04.1981. He submitted that words capital assets become the Assessee in the present case which must be applied to the case in hand by holding the property in question become Assessee property in 1975 when after allotment initially a sum of Rs. 5,000/- was paid.

6. No formal paper book of appeal has been filed but learned Counsel for appellant has placed before us paper book filed by Assessee before Tribunal containing report of private valuer of Assessee and that of AVO, letter of UP AEVP, copy of objections raised by approved valuer on 21.12.2011 and 27.12.2011.

7. Assessee submitted valuation report prepared by Er. Praval Pratap Singh, Chartered Civil Engineer, Fellow Member Institution of Valuer & Govt. Registered Valuer which shows that as per statement of Assessee himself, the entire building was renovated and additional construction work was carried out on ground and first floor during 1983-84 to make it fit for proper habital use. Thus believing contention of Assessee that addition and renovation was made in 1982-83, he assessed investment in construction at Rs. 2,79,064/-.

8. After report of AVO, Assessee requested another registered valuer Er. Khazan Chandra to inspect disputed house and submit report. The report dated 16.04.2013 submitted by Er. Khazan Chandra shows that he inspected disputed property on 16.04.2013 on representation of owner of property but submitted comments on the assessment made by AVO regarding investment cost. This report dated 16.04.2013, shows that there was no allotment of disputed house to Assessee in 1975 but in fact, while submitting application for allotment registration charges were paid by Assessee as Rs. 5,000/- on 29.01.1975.

9. Disputed house was admittedly allotted to him in 1982 i.e. 29.04.1982. Thereafter only process of installment commenced.

The registration amount already paid was adjusted against sale consideration of house, allotted by UP AEVP, therefore, the aforesaid allotment was obviously under hire purchase agreement.

10. In order to take advantage of Section 55(2)(b)(i) (of Income Tax Act, 1961), it was incumbent upon Assessee to show that ‘capital asset’ became property of assessee before 01.04.1981. Something can become property of a person only when he acquires an interest therein superior to interest of others and have a right to possess the same.

11. In the present case, as the facts discussed above shows the Assessee has no identification of his right with respect to property in question. In 1975 only a registration fee was deposited which means that Assessee was an applicant for allotment of property from UP AEVP and had agreed to pay sale consideration thereof, in case such property is allotted to him. It is not in dispute that allotment took place only on 29.04.1982. Therefore, prior thereto, Assessee had no interest, right or otherwise on the concerned property in dispute. Hence Section 55(2)(b) (of Income Tax Act, 1961)would have no application in the case in hand.

12. Tribunal has held that at the best Assesse could claim right of acquisition of property in dispute only on 29.04.1982 when UP AEVP allotted disputed house to the plaintiff. We find no infirmity or illegality in the aforesaid view. Question-1 is accordingly decided against Assessee.

13. Now coming to question no. 2, it is contended that index cost of acquisition of capital gain has not been rightly considered by Tribunal. Assessee tried to show report of his Valuer to suggest that the same ought to have been accepted by Assessing Authority who has accepted valuation of investment in addition and alteration of Rs. 2,00,000/-, worked out by AVO, without assigning any reason or discussion. It is submitted that the said valuation of Rs. 2,79,064/- worked out by Assessee’s private valuer has wrongly been rejected.

14. The assessment order shows that Assessee furnished objections on 21.12.2011 and requested that Reference be made to AVO, Income Tax Department for ascertaining fair market value of property where upon Reference was made and AVO submitted report on 28.12.2011.

15. In this regard, we find that even on the petitioner’s request another registered valuer Er. Khazan Chandra inspected property on 10.04.2013 and submitted report on 16.04.2013. As per his information, investment cost in the construction of additional accommodation and improvement of existing construction during 1982-84 worked out at Rs. 2,18,000/- giving a margin of 15%. In such a valuation / estimate it would not be seem that valuation of AVO was patently arbitrary and based on no material when for reinvestment, another registered valuer at the request of Assessee himself inspected premise but did find valuation of Rs. 2,79,064/- made by earlier registered valuer Er. Praval Pratap Singh which was relied by Assessee recorded his finding nearer to valuation made by AVO with regard to the investment for additional construction and renovation work. It thus cannot be said that the index cost of acquisition, worked out accordingly and it could not be shown that it is patently, fault or contrary to any provisions of law. In view thereof second question is also answered against Assessee and in favour of the revenue.

16. The appeal lacks merit and is dismissed with cost.

Order Date :- 16.1.2017

×

Similar Ripples

Questions

Court Rejects Taxpayer's Claim on Property Acquisition Date, Upholds Tax Assessment

Write your CommentSimilar Posts

Generic

- Reportdata/2116_lUJZYo4.pdf