Full News

Court Rules Additional Interest for Interest-Tax Not Chargeable Under Interest-tax Act

Court Rules Additional Interest for Interest-Tax Not Chargeable Under Interest-tax Act

This case involves the Commissioner of Income Tax (CIT) challenging Canfin Homes Ltd., a financial institution, over the treatment of additional interest collected from borrowers to cover interest-tax liability. The court ruled in favor of Canfin Homes, stating that this additional amount was not "interest" under the Interest-tax Act and thus not chargeable.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax & Anr. Vs Canfin Homes Ltd. (High Court of Karnataka)

ITA No. 124 of 2003 C/w ITA No.125 of 2003

Date: 11th April 2008

Key Takeaways:

1. Additional interest collected to cover interest-tax is not considered "interest" under the Interest-tax Act.

2. Financial institutions can pass on the burden of interest-tax to borrowers through contractual agreements.

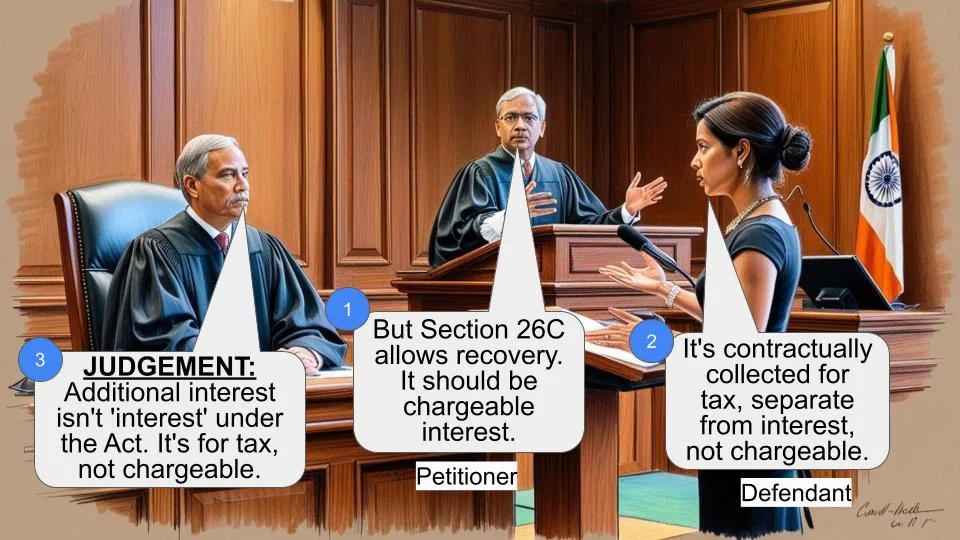

3. Section 26C of the Interest-tax Act is an enabling provision, not a charging provision.

Issue:

Is the additional interest collected by a financial institution from borrowers to cover interest-tax liability considered "chargeable interest" under the Interest-tax Act?

Facts:

- Canfin Homes Ltd. is a financial institution subject to the Interest-tax Act, 1974.

- The case covers assessment years 1996-97 and 1997-98.

- Canfin Homes collected additional interest from borrowers to cover its interest-tax liability.

- The company maintained separate accounts for this additional amount.

- The CIT argued that this additional amount should be treated as chargeable interest under the Act.

Arguments:

Revenue's Arguments:

- The additional interest collected under Section 26C (of Income Tax Act, 1961) should be treated as chargeable interest.

- Section 26C (of Income Tax Act, 1961) was introduced to facilitate credit institutions to vary agreements for pre-1991 loans only.

- There's no provision allowing the assessee to collect interest-tax separately.

Assessee's Arguments:

- The additional amount collected was specifically for covering interest-tax liability.

- Separate accounts were maintained for this amount.

- The collection was based on contractual obligations, not necessarily on Section 26C (of Income Tax Act, 1961).

Key Legal Precedents:

1. CIT vs. Bank of Madura Ltd. (1996) 130 CTR (Mad) 275 : (1995) 215 ITR 928 (Mad) - The court relied on this case, which held that amounts collected towards interest-tax were not "interest" under Section 2(7) (of Income Tax Act, 1961).

2. Indian Banks' Association & Ors. vs. Devkala Consultancy Service & Ors. (2004) 189 CTR (SC) 157 : (2004) 267 ITR 179 (SC) - The Supreme Court's observations on Section 26C (of Income Tax Act, 1961) were considered, but the court found that the Revenue's reliance on a single sentence from this judgment was out of context.

Judgement:

The court ruled in favor of Canfin Homes Ltd., holding that:

1. The additional amount collected was not "interest" within the meaning of Section 2(7) of the Interest-tax Act.

2. This amount could not be treated as chargeable interest for the purposes of the Act.

3. Section 26C (of Income Tax Act, 1961) is an enabling provision, allowing credit institutions to pass on the burden of interest-tax to borrowers.

4. The separate accounting of these amounts by the assessee was significant in determining their nature.

FAQs:

1. Q: Can financial institutions collect additional interest to cover interest-tax?

A: Yes, they can, based on contractual agreements with borrowers.

2. Q: Is this additional interest considered "chargeable interest" under the Interest-tax Act?

A: No, the court ruled that it is not considered "interest" under Section 2(7) (of Income Tax Act, 1961) and thus not chargeable.

3. Q: What is the significance of Section 26C of the Interest-tax Act?

A: It's an enabling provision that allows credit institutions to vary loan agreements to recover their interest-tax liability from borrowers.

4. Q: Does this ruling apply to all loans or only pre-1991 loans?

A: While Section 26C (of Income Tax Act, 1961) specifically mentions pre-1991 loans, the court's reasoning suggests it could apply more broadly based on contractual agreements.

5. Q: How important was the separate accounting of these amounts by Canfin Homes?

A: It was very significant, as it helped demonstrate that these amounts were specifically collected for interest-tax and not as general interest.

1. These appeals are heard and disposed of together, as they pertain to the same assessee—except that they are in respect of two different but consecutive assessment years namely 1996-97 and 1997-98, respectively. The controversy and the questions of law involved are identical.

2. The assessee is a financial institution. The assessee had filed its return of income under the provisions of the Interest-tax Act, 1974 (hereinafter referred to as ‘the Act’ for brevity). The assessment in respect of the year 1996-97 was completed by order dt. 19th March, 1999. The chargeable interest declared was accepted.

3. However, the CIT, in exercise of power under s. 19 of the Act, proceeded to hold, after hearing the assessee, by an order dt. 17th Aug., 2000 that a sum of Rs. 2,09,40,087 additional interest collected by the assessee from its customers in respect of loans advanced, was also subject-matter of levy under the Act. It was further held that as per Sch. 11 of the printed accounts of the assessee for the year ended 31st March, 1996, a sum of Rs. 3,76,41,023 was shown but the same was not examined by the AO. And accordingly he was directed to examine whether it would be chargeable as per the provisions of the Act after giving an opportunity to the assessee. The assessee had preferred an appeal to the Tribunal against the above order. The Tribunal having allowed the appeal, the Revenue has preferred the appeal in IT Appeal No. 125 of 2003.

4. In respect of the asst. yr. 1997-98, the AO held that amounts collected by the assessee from its debtors towards its liability to pay interest-tax forms part of the chargeable interest within the meaning of s. 2(5) r/w s. 5 of the Act. This was challenged by the assessee before the CIT(A), unsuccessfully. On a further appeal by the assessee, before the Tribunal, the Tribunal had held in favour of the assessee. It is this which is under challenge in the connected appeal No. IT Appeal 124 of 2003. The questions of law that are raised in these appeals are :

"(i) Whether the Tribunal is correct in law in holding that the order passed under s. 8(2) of the Act by the AO is not prejudicial to the interest of the Revenue and is not erroneous and therefore the CIT has no jurisdiction under s. 19 of the Act to bring the chargeable income to tax ?

(ii) Whether the Tribunal is correct in law in holding that interest of Rs. 2,09,40,087 collected from the debtors is not chargeable to tax under s. 26C of the Interest-tax Act ?"

5. It is contended on behalf of the Revenue that the assessee had collected additional interest by invoking s. 26C of the Act. This additional amount can only be treated as chargeable interest. It is contended that s. 26C was incorporated into the Act only w.e.f. 1st Oct., 1991, in order to facilitate credit institutions to vary the terms of agreements, in respect of term loan transactions entered into before 1st Oct., 1991, so as to increase the rate of interest stipulated therein to the extent to which such institution is liable to pay interest-tax under the Act. The said section cannot be pressed into service in respect of transactions entered into after 1st Oct., 1991.

6. There is no provision under the Act which enables the assessee to collect any amount as interest-tax and as the amounts collected are only by way of interest, the same is chargeable interest attracting the levy of interest-tax.

7. It is contended that the Tribunal could not have placed reliance on the decision in the case of CIT vs. Bank of Madura Ltd. (1996) 130 CTR (Mad) 275 : (1995) 215 ITR 928 (Mad) , as the said case pertained to the asst. yrs. 1975-76 and 1976-77 when there was no provision similar to s. 26C. Further, the facts are also different in that, the bank, in that case, was collecting interest-lax from its borrowers and paying the same to the Government. The Court held that there was no prohibition to do so. It was held that the amount of tax collected would not fall within the definition of "interest" under s. 2(7) of the Act. It is therefore, contended that there was clear evidence to show that the bank was collecting interest-tax from its borrowers. On the other hand, in the present case, the assessee has collected interest at a higher rate and that no deduction could be given in respect of such amounts while computing the chargeable interest.

8. It is further urged that the assessee could not realise by way of tax, or any amounts akin thereto, which has not been authorised by the Parliament. And seeks to draw sustenance from the decision of the Supreme Court in the case of Indian Banks’ Association & Ors. vs. Devkala Consultancy Service & Ors. (2004) 189 CTR (SC) 157 : (2004) 267 ITR 179 (SC) , in this regard while relying on that portion of the decision, dealing with s. 26C of the Act, at pp. 188-189 thereto. It is therefore, prayed that the appeals be allowed and the questions of law be answered in favour of the Revenue.

9. Per contra, Shri G. Sarangan, senior advocate, appearing for the respondents, contends that the decision of the Tribunal does not warrant interference and that appeals be dismissed. It is contended that a plain reading of s. 26C would indicate that was enacted only for a limited purpose of enabling institutions, such as the assessee, of passing on the burden of lax under the Act, to its borrowers. The counsel would submit that if for instance a sum of Rs. 100 lent was charged with a rate of interest of 10 per cent—the interest earned would come to Rs. 10. In terms of s. 26C the interest-tax payable thereon is at 3 per cent or 30 paise. Applying this to the amounts collected by the assessee, the accounts maintained by it, which have been scrutinized by the Revenue, would clearly disclose that out of Rs. 10.30 collected as interest on every Rs. 100, the sum of 30 paise has been passed on to the Revenue as interest-tax. The additional interest so collected is in accordance with the enabling provision namely s. 26C and the assessee having acted in terms of the same—the Revenue seeking to treat the total sum of Rs. 10.30 as chargeable interest is clearly illegal and the Tribunal has therefore, rightly allowed the appeal of the assessee.

10. It is also contended that the decision in Bank of Madura (supra) having been rendered with reference to a point of time when s. 26C was not even in existence, the ratio of that decision would apply with greater force to the case of the assessee. The reliance sought to be placed by the Revenue on a sentence in isolation, in the decision of Indian Bank’s Association is clearly untenable—the same is sought to be drawn out of context. It is hence prayed that the appeals be dismissed.

11. On these contentions—we may firstly, note that the Interest-tax Act was enacted by Parliament w.e.f. 1st Aug., 1974. The object of the Act was to impose tax on the total amount of interest received by scheduled banks and credit institutions on loans and advances. The Act was withdrawn in the year 1978, but re-introduced in the year 1980. It was again withdrawn in the year 1985. It was re-introduced yet again in the year 1991, by virtue of Finance (No. 2) Act, 1991 (hereinafter referred to as ‘the 1991 Act’ for brevity). Sec. 26C (of Income Tax Act, 1961) was inserted w.e.f. 1st Oct., 1991, under the 1991 Act. The same is reproduced here for ready reference : "26C. Notwithstanding anything contained in any agreement under which any term loan has been sanctioned by the credit institution before the 1st day of October, 1991, it shall be lawful for the credit institution to vary the agreement so as to increase the rate of interest stipulated therein to the extent to which such institution is liable to pay the interest-tax under this Act in relation to the amount of interest on the term loan which is due to the credit institution."

12. From a plain reading of s. 26C it is clear that the said provision vests a credit institution with power to vary an agreement, with a borrower in respect of a term loan sanctioned prior to 1991, to increase the rate of interest stipulated to the extent of recouping its liability of interest-tax. Thus passing on the burden of the tax on its borrowers.

13. The argument of the Revenue is that s. 26C cannot be construed as a charging provision and that the said section having been introduced merely to mitigate the hardship of the institutions with respect to pre 1st Oct., 1991 credit loan transactions so that such credit institutions can reimburse themselves on account of the lax liability ultimately from the borrowers.

14. In the light of a finding by the Tribunal that the assessee has, under agreements executed subsequent to the period 1st Oct., 1991, incorporated a term imposing an obligation on its borrowers to pay to it such amounts as are payable by the assessee to the Central or State Governments on account of any tax levied on interest on the loan by such Government, is significant. The circumstance that the assessee having collected the liability of interest-tax from its borrowers in terms of the contractual obligation and not necessarily on the strength of s. 26C is material. And the further circumstance that the assessee had maintained a separate account in respect of the amounts, though collected as additional interest was in fact towards payment of interest-tax, does compel us to hold that the amounts so collected were not "interest" within the meaning of s. 2(7) of the Act and hence could not be treated as chargeable interest for purposes of the Act.

15. The Tribunal has rightly held that the decision in the case of Bank of Madura (supra), would apply on all fours to the present case. The observation of the Supreme Court in the case of India Banks Association (supra), as to the scope of s. 26C is to the following effect : "Sec. 26C (of Income Tax Act, 1961) : Parliament by reason of the said Act imposed a tax on the banks and other financial institutions. By reason of the said Act, the appellants were not statutorily empowered to pass the burden thereof to the borrowers or realise the same on behalf of the Union of India. Concededly, in terms of the agreement of the term loan, the appellants were not entitled to charge interest at a higher rate than the agreed one. Sec. 26C (of Income Tax Act, 1961) was, therefore, enacted so as to enable the bankers to realise the amount of tax which they were liable to recover on the chargeable interest. The appellants have proceeded on the basis that having regard to the definition of "chargeable interest" as contained in s. 2(5) of the Act, the additional interest will have also to be calculated for the said purpose and the rate of tax must be calculated thereupon which, as noticed hereinbefore, resulted in adding of interest for the purpose of calculation of tax ad infinitum.

How Parliament thought of the matter is the question. The Union of India does not agree with the contentions of the appellants nor do we. The action on the part of the appellants suggests that they had put the cart before the horse. The action of taking recourse to s. 26C would arise only when the chargeable interest is calculated whereupon only the incidence of tax under the said Act is required to be passed on to the borrowers by way of additional interest. The entire approach of the appellants was based on a wrong premise. The said Act, is a taxing statute. The Union of India under the said Act cannot direct or permit the bankers or the financial institutions of raise interest. The Act must, therefore, receive purposive construction so as to give effect to the purport and object it seeks to achieve [see BBC Enterprise Ltd. vs. Hi-Tech Xtravision Ltd. (1990) 2 All ER 118 (CA) at 122-3 ; Mohan Kuniar Singhania vs. Union of India AIR 1992 SC 1; Murlidhar Meghraj Loya vs. State of Maharashtra (1976) 3 SCC 684; Superintendent and Remembrancer of Legal Affairs to Government of West Bengal vs. Abani Maity (1979) 4 SCC 85; Khet Singh vs. Union of India (2002) 4 SCC 380; Indian Handicrafts Emporium vs. Union of India (2003) JT 7 SC 446; Ashok Leyland Ltd. vs. State of Tamil Nadu (2004) 3 SCC 1 : (2004) 2 RC 249 and High Court of Gujarat vs. Gujarat Kishan Mazdoor Panchayat (2003) JT 3 SC 50 ]. In the event, the contention of the appellants is accepted, the same would give rise to incongruous results. Such an interpretation, as is well-known, must be avoided, if avoidable. Furthermore, a statutory impost must be definite. Having regard to Art. 265 r/w Art. 366(28) of the Constitution of India nothing is realisable as a tax or by way of recovery of tax or any action akin thereto which is not permitted by law.

It is neither in doubt nor in dispute that s. 26C is an enabling provision. It has to be so construed, having regard to the term "lawful" used therein.

It merely prevails over an agreement under which any term loan has been sanctioned by the credit institution before 1st Oct., 1991. It was "lawful" for the purpose of recovering the amount of tax which was payable by the appellants and a fortiori—nothing over and above the same. Such increase in the rate of interest would be (a) to the extent to which such institution is liable to pay the interest-tax; (b) in relation to the amount of interest on the term loan; and (c) which is due to the credit institution. Increase in the rate of interest in terms of s. 26C of the Act, thus, has a direct nexus with the statutory impost. The action on the part of the appellants in rounding off of the interest, thus, was wholly unjustified. Once it is held that increase in interest in a justifiable manner pertains to passing on the burden of tax, the contention that the same had been done by the bank in exercise of its contractual power must be rejected. A taxing statute must be construed reasonably. Nothing can be realised by way of tax or akin thereto which has not been authorised by Parliament." And the Revenue seeking to rely on the last sentence of the said passage is not tenable. The assessee has not collected any amount which were not authorised or expressly prohibited.

16. We, therefore, are of the firm opinion that the appellant has not made out any case on merits. The appeals are hence dismissed. The questions of law are answered in favour of the assessee and against the Revenue.

SD/-

JUDGE

SD/-

JUDGE

×

Similar Ripples

Questions

Court Rules Additional Interest for Interest-Tax Not Chargeable Under Interest-tax Act

Write your CommentSimilar Posts

Generic

- Reportdata/4652.pdf