Full News

Court Rules in Favor of Assessee on Taxability of Interest and Compensation in Land Acquisition Case

Court Rules in Favor of Assessee on Taxability of Interest and Compensation in Land Acquisition Case

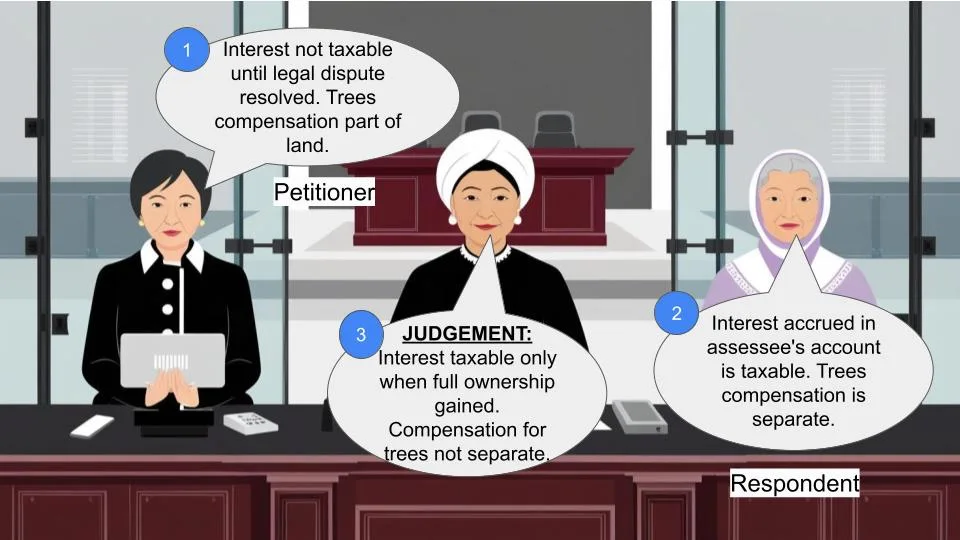

The Karnataka High Court ruled in favor of the assessee, B.M. Shivanna, in a case concerning the taxability of interest on compensation received for land acquisition and the treatment of compensation for trees on acquired agricultural land. The court held that the interest was not taxable until the legal dispute over land ownership was resolved, and the compensation for trees should not be treated separately from the agricultural land acquisition.

Get the full picture - access the original judgement of the court order here.

Case Name:

M. Shivanna Vs Assistant Commissioner of Income Tax (High Court of Karnataka)

ITA No.452 of 2009(IT)

Key Takeaways:

1. Interest on compensation is taxable only when the assessee gains full ownership without restrictions.

2. Compensation for trees on acquired agricultural land should not be treated separately for tax purposes.

3. Real income, not presumed income, is subject to taxation.

4. In land acquisition cases, the entire transaction should be considered as a single unit for tax purposes.

Issue:

1. Is interest on fixed deposits representing compensation, pledged against bank guarantee pending resolution of a land title dispute, taxable in the years when such interest was credited by the bank?

2. Is compensation for trees on acquired agricultural land taxable as capital gains separately from the land acquisition?

Facts:

1. The assessee's agricultural land was acquired by the Karnataka Industrial Area Development Board in 1997.

2. Compensation was awarded, but due to a legal dispute with cousins, it was kept in fixed deposits as security.

3. Interest accrued on these deposits, but the assessee couldn't access it due to the ongoing dispute.

4. The legal dispute was finally resolved in 2008 through a Regular Second Appeal.

5. The Income Tax Department conducted a search in 2001 and initiated assessment proceedings.

Arguments:

Assessee:

1. The interest was not taxable until the legal dispute was resolved in 2008, as the assessee didn't have full ownership before that.

2. The compensation for trees should not be treated separately from the agricultural land acquisition for tax purposes.

Revenue Department:

1. Interest was taxable as it accrued in the assessee's account, even if not accessible.

2. Compensation for trees should be treated separately and taxed as capital gains.

Key Legal Precedents:

1. COMMISSIONER OF INCOME TAX AND ANOTHER v/s SMT.SHANTAVVA (2004) 267 ITR 67 (Kar)

2. COMMISSIONER OF INCOME-TAX v/s A.B.V.GOWDA (DECD) (1986) 157 ITR 697 (Kar)

3. COMMISSIONER OF INCOME TAX v/s SRI. L. SAMBASHIVA REDDY in ITA No.347/2009

4. COMMISSIONER OF INCOME TAX, WEST BENGAL-II v/s HINDUSTAN HOUSING AND LAND DEVELOPMENT TRUST LTD. (1986) 161 ITR 524 (SC)

Judgement:

1. The court ruled in favor of the assessee on both questions of law.

2. Interest on compensation is taxable only when the assessee gains full ownership without restrictions, which occurred in 2008.

3. Compensation for trees should not be treated separately from the agricultural land acquisition for tax purposes, as it was a single transaction.

FAQs:

Q1: When does interest on compensation become taxable in such cases?

A1: Interest becomes taxable only when the assessee gains full and unrestricted ownership of the funds, typically after the resolution of any legal disputes.

Q2: Can compensation for trees on acquired agricultural land be taxed separately?

A2: No, the court ruled that in land acquisition cases, the entire transaction should be considered as a single unit for tax purposes.

Q3: What is the significance of "real income" in this case?

A3: The court emphasized that only real income, not presumed income, is subject to taxation. Income that the assessee cannot access due to legal restrictions is not considered real income.

Q4: How does this judgment impact similar land acquisition cases?

A4: This judgment sets a precedent for treating land acquisitions as single transactions and for determining the taxability of interest on compensation in cases with ongoing legal disputes.

Q5: What accounting method was applied in this case?

A5: The court applied the cash system of accounting, as the assessee did not maintain any books of accounts.

This is an appeal filed by the assessee, challenging the assessment order for the Block period from 01-04-1990 to 20-02-2001.

2. Briefly stated the facts of this case are:

The assessee-B.M.Shivanna, along with his brother B.M.Mariswamaiah, inherited certain agricultural lands which were acquired by the Karnataka Industrial Area Development Board (for short ‘the Board’) vide notification dated 17-07-1997. The total compensation for acquisition of such land, amounting to Rs.4,10,56,235/-, was awarded by the Board in favour of the assessee and his brother, out of which the assessee had 50% share. While awarding the compensation, the Board had calculated the value of the land so acquired at Rs.3,18,15,000/- and valued the trees, building, borewell and other assets on the said land at Rs.92,41,235/-. The compensation for the land portion was paid to the assessee and his brother vide cheque dated 28-11-1997, and the compensation for the standing trees, building, borewell, etc. was paid on 12-02-1999.

3. Since the cousins of the assessee and his brother had filed a civil suit, being O.S.No.141/1997, whereby the family partition arrived at in 1970 was under challenge, and a claim of share in the properties so acquired had been made, the compensation awarded to the assessee (and his brother) could not be actually received by the assessee, as the Board required the assessee to furnish adequate security for the same, to secure the interest of the Board in case the suit filed by the cousins of the assessee was decided in their favour. Consequently, though the cheques were deposited in Vysya Bank in the name of the assessee, but security in the form of Bank Guarantee was to be furnished by the assessee (as well as his brother), for which the Bank demanded 100% collateral security, and thus the amount so deposited in the name of the assessee was pledged as security, which he could not withdraw.

4. Consequently, a tripartite agreement was executed between the assessee (including his brother), Vysya Bank and the Board, which provided for Fixed Deposits of the amount credited in the account of assessee and his brother to be kept with the Bank as security on behalf of the Board, and would be payable either to the assessee (and his brother) or the cousins who had filed the suit, after dispute was resolved by the Court. On 09-03-2001, in exchange of Bank Guarantee, an Indemnity Bond was executed by the appellant-assessee in favour of the Board, according to which also the amount of compensation so deposited in the Bank, along with interest, was to remain as security in favour of the Board, till the suit/ appeal was finally decided.

5. The suit filed by the cousins of the assessee was dismissed on 31-10-2001, against which a regular appeal was filed before the Principal District and Sessions Judge, Bangalore, which also was dismissed on 26-10-2004. Challenging the said order passed in appeal, a Regular Second Appeal was filed in the High Court which was ultimately dismissed on 23-07-2008, and the dispute between the assessee and his brother on one side, and their cousins on the other side, came to rest.

6. During the pendency of the court proceedings, a search was conducted on 02-02-2001 by the Income Tax Department in the premises of the assessee and his brother, and the business premises of Vysya Bank, consequently, proceedings for assessment for the block period 1-4-1990 to 20-2-2001 was initiated.

7. With regard to compensation paid for acquisition of the agricultural land, amounting to Rs.3,18,15,000/-, no capital gains was leviable, since the land in question was agricultural land and was located within the limits of the village, not forming part of definition of ‘capital asset’. The question under consideration is whether the compensation received by the assessee, and his brother, in respect of the trees and other assets was to form part of the capital asset or not? The other question which arises is whether tax would be payable on interest which had accrued in the account of the assessee, and his brother, even when the assessee could not get full ownership on the interest amount?

8. All the authorities below, that is, the Assessing Officer, Appellate Commissioner and the Tribunal have held that the interest amount would be taxable in the year in which it was credited in the bank account of the assessee (as well as his brother), and since the same was not disclosed by the assessee as income in the years in question, it was to be treated as undisclosed income, on which tax at enhanced rate of 60% along with interest thereon would be payable by the assessee. The authorities below have also held that the compensation received by the assessee and his brother towards the trees, building, borewell and other assets amounting over Rs.92.41 lakhs would form part of the capital assets and would, thus, not be exempted from payment of tax.

9. Aggrieved by the orders of the authorities below, including the Tribunal, this appeal has been filed, which was admitted on 10-11-2009 with the following order:

“Appeal is admitted for examination, not only on the substantial question relating to the levy of tax on the value of the trees, which form part of agricultural lands, which were come to be acquired by the government for a public purpose, and in respect of which the government had compensated the owners and as to whether the value so apportioned to the trees standing on the lands could have been brought to tax as non-agricultural income, and the other substantial question of law, as raised in the memorandum of appeal, as, in our view, such questions do arise for examination”. However, at the time of arguments, learned counsel for the parties have formulated two substantial questions of law to be considered and decided by this Court, which are as follows:

“(1) Whether, in the facts and circumstances of the case, the Tribunal is right in law in holding that interest on fixed deposits representing compensation, pledged against bank guarantee given to KIADB pending resolution of dispute over title of land, is taxable in the respective years when such interest was credited by bank in its books?

(2) Whether, in the facts and circumstances of the case, the Tribunal is right in law in holding that part of compensation relating to trees in the agricultural land acquisition proceeding, is taxable as capital gains and if yes, the same is chargeable to tax in the block period and not in the year of unconditional receipt?”

10. We have heard Sri.K.K.Chythanya, learned counsel appearing for the appellant-assessee, as well as Sri.K.V.Aravind, learned counsel appearing for the respondent-Revenue and have also perused the records.

11. From the facts as narrated above, what is culled out is that payment of compensation for the acquisition of land was made through cheques in the name of the assessee and his brother, and the same were deposited in their names in the Bank. However, because of pendency of the suit filed by the cousins of the assessee, no amount was actually payable to the assessee or his brother, which remained in Fixed Deposit with the bank as security in favour of the Board. The interest did accrue on such deposit with the Bank, but the same was also to be kept as security and was subject to payment to such party as would be decided in the suit, or such orders as may be passed in the appeals. It was only after the decision in the Regular Second Appeal that by an order dated 23-07-2008, the assessee and his brother became entitled to receive the payment of compensation, as well as interest that had accrued on the said amount. Though the authorities below have held that the assessee could withdraw the interest which had accrued on the Fixed Deposits, but after having gone through the deed of Bank Guarantee, as well as the Indemnity Bond, we are of the opinion (and the same has also been very fairly accepted by Sri.K.V.Aravind, learned counsel for the respondent-Revenue) that at no point of time, before the final decision in the Regular Second Appeal, the assessee became entitled to withdraw even the interest, which had accrued on such compensation amount which was kept in deposit with the Bank.

12. In the light of the aforesaid facts, we may proceed to answer the two questions of law which have been framed:

Question No.1:

13. This question relates to taxability of the interest amount which accrued on the compensation deposited in the bank account of the assessee. The submission of the learned counsel for the assessee-appellant is that, the amount had never been in the hands of the assessee till the decision of the Regular Second Appeal, as it was a part of the legal dispute which was raised by the cousins of the assessee (and his brother) with regard to title of the land which was acquired by the Board. It is contended that the assessee does not maintain any books of account and, as such, mercantile method of accounting would not be applicable, and in the cash system of accounting, the income would be chargeable to tax only when the assessee becomes complete owner of the interest amount, without any dispute or restriction over the same. The submission, thus, is that till the title of the suit land was finalized in the Regular Second Appeal by the High Court on 23-07-2008, there was always some condition or impediment or restriction over the compensation amount, as well as on the interest that accrued on the same, and thus, the appellant-assessee never became the complete or real owner of the interest amount till 23-07-2008, which was only in the assessment year 2009-10 and not before, and the interest amount which accrued from the year 1997 till assessment year 2009-10, would be payable by the assessee only in such assessment year.

14. Per contra, Sri.K.V.Aravind, learned counsel for the respondent-Revenue has submitted that as per the definition and scope of ‘total income’ which would be taxable as per the provisions of the Act (more precisely Section 5 (of Income Tax Act, 1961) for short ‘the Act’), as per the cash system of accounting, the assessee would be liable to pay tax on such income received or deemed to be received and as per the mercantile system of accounting, the assessee would be liable to pay tax on such income which accrues or arise or deemed to accrue or arise to him. It is, thus, submitted that since the compensation for land, and standing trees, building, etc., was received by the assessee in the years 1997 and 1999 respectively, and the same was kept in deposit in the Bank in the name of the assessee, it would be the property of the assessee, and any interest which accrued on such amount would be treated as received by the assessee when it accrued in his account, and would thus be liable for payment of tax as on the date of its receipt or accrual, and by not having disclosed such interest income, the same has rightly been considered by the authorities as undisclosed income chargeable to tax at the rate of 60% plus interest.

15. Section 2(24) (of Income Tax Act, 1961) defines the ‘income’ and Section 5 (of Income Tax Act, 1961) give scope of ‘total income’. Sub- Section (1) of Section 5 (of Income Tax Act, 1961) is relevant, which is reproduced below:

5. Scope of total Income:

(1) Subject to the provisions of this Act, the total income of any previous year of a person who is a resident includes all income from whatever source derived which –

(a) is received or is deemed to be received in India in such year by or on behalf of such person; or

(b) accrues or arises or is deemed to accrue or arise to him in India during such year; or

(c) accrues or arises to him outside India during such year.

16. Admittedly, the assessee does not maintain any books of accounts. He is an agriculturist, who had never filed any returns of income prior to the acquisition of the land, and until the search operations were conducted in his premises on 2-2-2001, whereafter also the return was filed in response to the notice issued by the Department and then too, in the said returns, he had disclosed his taxable income as NIL, as by then the Regular Second Appeal had not been decided and he had not acquired full and complete right over the compensation amount, as well as the interest, which was acquired only after the decision in the Regular Second Appeal on 23-07-2008, and that income of the assessee became taxable only in the assessment year 2009-10.

17. In the absence of the assessee maintaining any books of accounts, and in the circumstances of the case, the accounting method which could be adopted in the case of the assessee would be nothing but cash system of accounting. In such a case, even as per Section 5 (of Income Tax Act, 1961), it would be income subjected to tax only when received or deemed to be received by the assessee. There can be tax imposed only on an income which is real, or in the hands of the assessee. In a case, where the assessee might have received some money in his account, but with certain impediment because of which the same cannot be used by the assessee till such impediment is overcome, which in the present case is of the decision in the suit/appeal filed by the cousins of the assessee, the same cannot be said to be actual receipt of money in the hands of or in favour of the assessee. If a right over certain money is dependent on contingency, condition or restriction, because of which the assessee cannot enjoy the money, though in his name in the bank, then the income will be in the hands of the assessee only when such condition, contingency or restriction is overcome. It is thus the real income of the assessee which could be taxed, and in a situation like the present, prior to the contingency, condition or restriction having been removed or overcome, the same could only be presumed income, and not real income.

18. The submission of the learned counsel for the respondent, that since the interest income had been received or accrued in the name of the assessee, the same would become taxable, is not worthy of acceptance. The interest income, in the present case, though may be in the name of the assessee, but was never in the hands of the assessee because of the pendency of the case and the furnishing of Bank Guarantee/Indemnity Bond by the assessee, due to which, neither capital nor interest could be withdrawn by the assessee. In whose favour such interest amount would actually go, was to depend on the outcome of the suit or appeal. It was only after the case was finalized, and the title of the assessee over the acquired property was confirmed on 23-07-2008, that the amount of compensation, along with interest, was finally found payable to the assessee, without any impediment. It was only then that amount (including interest) could be said to be real income of the assessee, and the same would then alone become liable for payment of tax.

19. A Division Bench of this Court, in the case of CHIEF COMMISSIONER OF INCOME-TAX AND ANOTHER v/s SMT.SHANTAVVA (2004) 267 ITR 67 (Kar), was dealing with a case under Section 45(5) (of Income Tax Act, 1961). Considering a case of awarding of compensation to a land owner, and thereafter enhancement by the Reference Court, which was challenged by the Acquiring Body in the High Court where a conditional deposit of the enhanced amount was directed by an interim order, and thereafter final amount of compensation was paid to the land owner (assessee therein), this Court held that part amount of the enhanced compensation paid in terms of the interim order would be subject to tax only when the appeal was finalized by the High Court, as the assessee therein (land owner) became complete owner of such compensation after finalization of the appeal, and the amount paid earlier was not to be taxable even when he may have actually received part of the enhanced compensation under the interim orders. Though the said case was under Section 45(5) (of Income Tax Act, 1961), the principle laid down in the said judgment, would squarely apply to the facts of the present case.

20. In another case, being COMMISSIONER OF INCOME-TAX v/s A.B.V.GOWDA (DECD) (1986) 157 ITR 697 (Kar), a Division Bench of this Court held that interest on the enhanced compensation, which was in dispute, would be taxable only after the dispute was over. The same view has been taken by the Madras High Court in the case of COMMISSIONER OF WEALTH TAX/INCOME-TAX v/s T.GIRIJA AMMAL (2006) 282 ITR 614 (Mad).

21. In a recent judgment rendered in the case of COMMISSIONER OF INCOME TAX v/s SRI. L. SAMBASHIVA REDDY in ITA No.347/2009 decided on 19-01-2015, a Division Bench of this Court, after relying on the decision of the Hon'ble Supreme Court in the case of the COMMISSIONER OF INCOME TAX, WEST BENGAL-II v/s HINDUSTAN HOUSING AND LAND DEVELOPMENT TRUST LTD. (1986) 161 ITR 524 (SC) has held that in the case of a private dispute between two parties, even if some payment is made to a party, the taxability of the same would arise only when the dispute is finally settled. It has been held that “Merely because by virtue of an interim order, with or without conditions, some payment is made for the purpose of Income tax Act, it would not constitute income and therefore there is no liability to pay tax on the day such interim payment is received”.

22. In our view it is thus clear, that if an amount is received by the assessee on certain conditions or by imposing any restrictions, such as of furnishing security, the assessee does not become the real owner of the money, though received in his name, or the interest that accrues thereon would not be chargeable to tax, till such dispute is resolved and the condition, or restriction, so imposed is removed or resolved.

23. For the foregoing reasons, we decide the first question of law in favour of the assessee and against the Revenue.

Question No.2:

24. Coming to the second question of law, which relates to whether the capital gains could be charged on the compensation for the standing mango and other fruit bearing trees, building, borewell and other assets on the agricultural land of the assessee, which was acquired under a notification for compulsory acquisition. What is to be noted in this regard is that it was acquisition of the land, along with structure, trees etc., which was made by a single transaction. It was only for the purpose of payment of compensation that valuation of the building, borewell, standing trees (which may be mango, tamarind and other fruit bearing trees) was made. While calculating the valuation of the trees, which was done by the Land Acquisition Officer of the Board, part relief had been granted by the Authorities with regard to certain kinds of trees and also the building and the borewell. But mango trees, which were approximately 12 years of age, were valued separately, and compensation on the same was treated as taxable. In this regard, since it is clear that the acquisition was for the entire land on “as is where is basis”, and the land in question is agricultural land, and the valuation of the trees and other assets, were made only for the purpose of calculating compensation, therefore the amount paid to the assessee was actually for acquisition of the agricultural land, which was exempted from tax. Hence, the question of payment of capital gains on the compensation only for the mango trees, etc., cannot be justified in law.

25. The Tribunal has wrongly relied on the decision in the case of COMMISSIONER OF INCOME TAX v/s M.RAMAIAH REDDY (1986) 158 ITR 611 (Kar), as the said case related to acquisition of urban land, where the assessee therein was claiming compensation for the trees to be treated as potential agricultural income and thus, be treated separately and exempted from tax. In the said case, though the Tribunal accepted the plea of the assessee, the High Court rejected the same, and held that the acquisition of the land, along with trees, was a single transaction which could not be split and thus, the benefit of trees being treated as separate transaction could not be given. The Division Bench of this Court, in paragraph 9, while deciding the said question held that “This legal formulation proceeded on the basis that there were two transactions in the acquisition, one pertaining to the land and the other to malkies thereon. This is wholly incorrect. The land was compulsorily acquired by the C.I.T.B., Bangalore. There were two transactions. While making the award the land and the tree growth were separately valued, but that does not mean that there were two transactions. The Tribunal, therefore, was not correct in drawing an inference that there were two transactions, one for acquiring the land and the other for the trees and malkies.”

26. In our view, the ratio of the said decision goes in favour of the assessee and not the Revenue. We are of the firm opinion that it was one transaction of acquisition, under which the land, as well as the trees, etc., had been acquired, and splitting the same into two for the purpose of taxation would be against the law.

27. Accordingly, we answer the second question also in favour of the assessee and against the Revenue. For the foregoing reasons, the two questions of law are answered in favour of the assessee and against the Revenue.

Accordingly, the appeal stands allowed. No costs.

Sd/- JUDGE

×

Similar Ripples

Questions

Court Rules in Favor of Assessee on Taxability of Interest and Compensation in Land Acquisition Case

Write your CommentSimilar Posts

Generic

- Reportdata/3447.pdf