Court rules on tax liability for individuals claiming exemption under Section 1…

Full News

Court rules on tax liability for individuals claiming exemption under Section 194A(1) (of Income Tax Act, 1961).

Court rules on tax liability for individuals claiming exemption under Section 194A(1) (of Income Tax Act, 196…

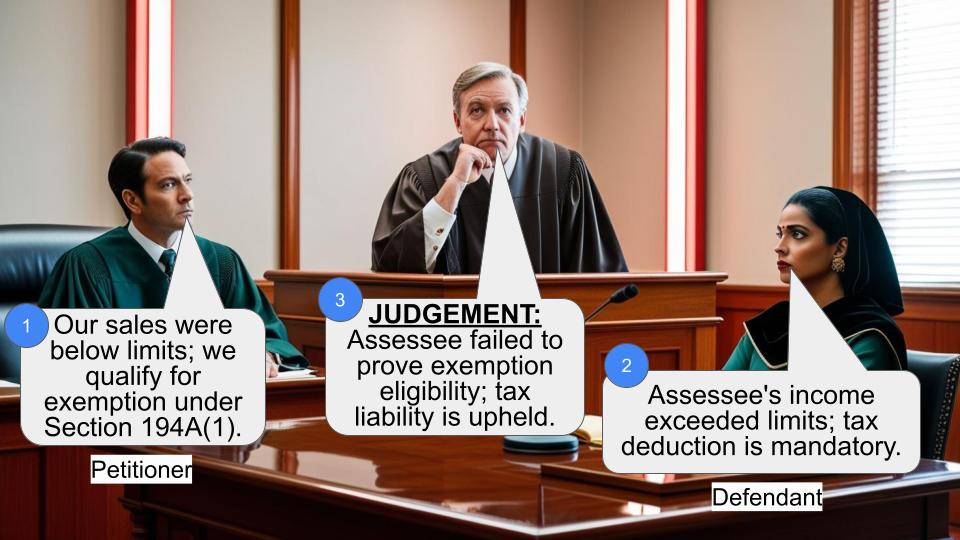

In the case of Thomas George Muthoot vs. Commissioner of Income Tax, the court addressed whether individuals and Hindu Undivided Families (HUFs) could claim exemption from tax deduction under Section 194A(1) (of Income Tax Act, 1961). The court found that the burden of proof lies with the assessee to demonstrate that they meet the conditions for exemption, which they failed to do. Consequently, the court upheld the tax liability.

Get the full picture - access the original judgement of the court order here

Case Name:

Thomas George Muthoot vs. Commissioner of Income Tax (High Court of Kerala)

ITA. No. 267 of 2014

Date: 3rd July 2015

Key Takeaways:

- The burden of proof for claiming tax exemptions under Section 194A(1) (of Income Tax Act, 1961) lies with the taxpayer.

- Individuals and HUFs are liable to deduct tax if their total sales or receipts exceed specified limits.

- The court emphasized the importance of compliance with tax laws and the consequences of non-compliance.

Issue

Did the assessee, an individual, satisfy the conditions for claiming exemption from tax deduction under Section 194A(1) (of Income Tax Act, 1961)?

Facts

- The assessee, Thomas George Muthoot, claimed exemption under Section 194A(1) (of Income Tax Act, 1961).

- The court noted that the exemption applies only if the total sales, gross receipts, or turnover from business do not exceed the limits specified under

Section 44AB (of Income Tax Act, 1961).

- The Income Tax Appellate Tribunal found that the assessee's business income exceeded these limits, thus making them liable to deduct tax.

Arguments

- Assessee's Argument: The assessee argued that they qualified for the exemption under Section 194A(1) (of Income Tax Act, 1961) as their total sales and receipts were below the specified limits.

- Revenue's Argument: The Revenue contended that the assessee's business income exceeded the limits set by Section 44AB (of Income Tax Act, 1961), and therefore, they were required to deduct tax.

Key Legal Precedents

- The court referenced Section 194A(1) (of Income Tax Act, 1961), which outlines the conditions under which individuals and HUFs are exempt from tax deduction.

- The court also cited Section 40(a)(ia) (of Income Tax Act, 1961), which states that if tax is deductible at source and not deducted, the amount is not allowable as a deduction.

Judgement

The court ruled against the assessee, confirming that they were liable to deduct tax under Section 194A(1) (of Income Tax Act, 1961) due to exceeding the specified limits of income. The court emphasized that the burden of proof was on the assessee to demonstrate eligibility for the exemption, which they failed to do. The appeals filed by the assessee were dismissed.

FAQs

Q1: What does Section 194A(1) (of Income Tax Act, 1961) entail?

A1: Section 194A(1) (of Income Tax Act, 1961) specifies the conditions under which individuals and HUFs can claim exemption from tax deduction on interest payments.

Q2: What happens if the tax is not deducted as required?

A2: If tax is not deducted when required, the amount is not allowable as a deduction under Section 40(a)(ia) (of Income Tax Act, 1961).

Q3: Can individuals and HUFs always claim exemption under Section 194A(1) (of Income Tax Act, 1961)?

A3: No, the exemption is only available if their total sales, gross receipts, or turnover do not exceed the limits specified under Section 44AB (of Income Tax Act, 1961).

Q4: What was the outcome for the assessee in this case?

A4: The court upheld the tax liability of the assessee, ruling that they did not meet the conditions for exemption under Section 194A(1) (of Income Tax Act, 1961).

1.These three appeals are filed by the assessee, who is aggrieved by the orders passed by the Income Tax Appellate Tribunal, Cochin Bench, upholding the assessment orders passed for the assessment years 2006-07, 2008-09 and 2010-11.

2.Assessee is a company engaged in portfolio management services having obtained necessary registration from the SEBI. The return of income for the assessment year 2008-09 was filed and assessment under section 143(3) (of Income Tax Act, 1961) was completed, treating the transactions in purchase and sale of shares as 'business income' instead of capital gains as shown by the assessee company. In so far as the assessment year 2006-07 is concerned, return of income was processed under section 143(1) (of Income Tax Act, 1961) and assessment was completed. After completing the assessment for the assessment year 2008-09, the assessment for 2006-07 was reopened by the Assessing

Officer invoking his power under section 147 (of Income Tax Act, 1961). Accordingly, assessment was completed under section 143(3) (of Income Tax Act, 1961), where also, the income of the

assessee from the purchase and sale of shares, which was originally treated as short term capital gains and taxed at the lower rate, was assessed as business income. The assessment for the year 2010-11 was also completed under section 143(3) (of Income Tax Act, 1961) as in the case of the assessment year 2008-09. These orders were confirmed by the Commissioner of Income Tax (appeals) and the

Tribunal, dismissing the appeals filed by the assessee. This is the background in which these appeals are filed.

3.The questions of law framed in ITA.267/14, which is common in these appeals, are the following:

“(1) Whether on the facts and circumstances of the case, the Appellate Tribunal is right in confirming the reopening of assessment under Section 147 (of Income Tax Act, 1961)?

(2) Whether on the facts and circumstances of the case, the Appellate Tribunal is right in confirming that the profit on sale of shares is to

be assessed under the head “income business” and not under the head “capital gains”?

(3) Whether there was any material or documents on record to justify the finding of the Appellate Tribunal that the Appellant is engaged in trading

activity and therefore profit on sale of shares should be assessed under the head “income from business”?

(4) Whether on the facts and circumstances of the case and in the light of the Department having accepted the assessment of similar income under the head “capital gains” for earlier Assessment Years and intervening Assessment

Years, the assessment under the head “income from business” for this Assessment Year is justified?

(5) Whether the Appellate Tribunal is right in law in disregarding the decisions of various High Courts including the jurisdictional High Court

which were relied on at the time of hearing, without a speaking order as to why they are not followed.”

4.We heard the senior counsel for the appellant and the learned senior standing counsel appearing for the Revenue.

5.According to the learned senior counsel, the re-opening of the assessment for the year 2006-07, invoking the power under section 147 (of Income Tax Act, 1961), is

illegal. He also contended that the grounds contemplated for re-opening an assessment under section 147 (of Income Tax Act, 1961) are not existing in this case. According to him, the assessee has been in the business since the assessment year 2002-03 and that till 2006-07, the income derived by the assessee from the sale and

purchase of shares was accepted by the Department as capital gains and that by treating such income for the aforesaid three assessment years as business

income, the Department has shown that it did not have consistency in the matter of assessment and treatment of income. It was also his case that even after re-opening the assessments for the year 2006-07 and completing the assessments for the years 2008-09 and 2010-11, the Department has left out assessments for the years 2007-08 and 2009-2010. According to the

counsel, such picking and choosing some of the years and leaving out the remaining years when the assessee had returned loss is impermissible.

6.These contentions were contradicted by the learned senior counsel appearing for the Revenue.

7.We have considered the submissions made. The first

issue that is required to be considered is the scope

of the power of the Assessing Officer under section

147 of the Act. Section 147 (of Income Tax Act, 1961) provides that

if the Assessing Officer has reason to believe that

any income chargeable to tax has escaped assessment

for any assessment year, he may, subject to the

provisions of sections 148 to 153, assess or re-

assess such income and also any other income

chargeable to tax which has escaped assessment and

which comes to his notice subsequently in the course

of the proceedings under this section, or recompute

the loss or the depreciation allowance or any other

allowance, as the case may be, for the assessment

year concerned. Under the first proviso, a time

limit of 4 years from the end of the relevant

assessment year has been fixed for taking action

under section 147 (of Income Tax Act, 1961), unless any income chargeable to

tax has escaped assessment by reason of the failure

on the part of the assessee to make a return under

section 139 (of Income Tax Act, 1961) or in response to a notice under section

142(1) or section 148 (of Income Tax Act, 1961) or to disclose fully and truly

all material facts necessary for his assessment for

that year. This provision, therefore, shows that the

power thereunder can be invoked by an Assessing

Officer if he has reason to believe that any income

chargeable to tax has escaped assessment for any

assessment year.

8.The expression 'reason to believe' incorporated in

Section 147 (of Income Tax Act, 1961) by Act 3 of 1989 with effect from

1.4.1989 came up for the consideration of courts on

various occasions. In Assistant Commissioner of

Income Tax v. Rajesh Jhaveri Stock Brokers P. Ltd

[(2007)291 ITR 500], the Apex Court examined this

expression and held thus:

“Section 147 (of Income Tax Act, 1961) authorises and permits the

Assessing Officer to assess or reassess income

chargeable to tax if he has reason to believe that

income for any assessment year has escaped

assessment. The word reason in the phrase

reason to believe would mean cause or

justification. If the Assessing Officer has cause

or justification to know or suppose that income

had escaped assessment, it can be said to have

reason to believe that an income had escaped

assessment. The expression cannot be read to

mean that the Assessing Officer should have

finally ascertained the fact by legal evidence or

conclusion. The function of the Assessing Officer

is to administer the statute with solicitude for

the public exchequer with an inbuilt idea of

fairness to taxpayers. As observed by the

Supreme Court in Central Provinces Manganese

Ore Co. Ltd. v. ITO [1991 (191) ITR 662], for

initiation of action under Section 147(a) (of Income Tax Act, 1961) (as the

provision stood at the relevant time) fulfilment of

the two requisite conditions in that regard is

essential. At that stage, the final outcome of the

proceeding is not relevant. In other words, at the

initiation stage, what is required is reason to

believe, but not the established fact of

escapement of income. At the stage of issue of

notice, the only question is whether there was

relevant material on which a reasonable person

could have formed a requisite belief. Whether

the materials would conclusively prove the

escapement is not the concern at that stage. This

is so because the formation of belief by the

Assessing Officer is within the realm of

subjective satisfaction (see ITO v. Selected

Dalurband Coal Co. Pvt. Ltd. [1996 (217) ITR 597

(SC)]; Raymond Woollen Mills Ltd. v. ITO [1999

(236) ITR 34 (SC)].

The scope and effect of Section 147 (of Income Tax Act, 1961) as

substituted with effect from April 1, 1989, as

also Sections 148 to 152 are substantially

different from the provisions as they stood prior

to such substitution. Under the old provisions of

Section 147 (of Income Tax Act, 1961), separate clauses (a) and (b) laid

down the circumstances under which income

escaping assessment for the past assessment

years could be assessed or reassessed. To confer

jurisdiction under Section 147(a) (of Income Tax Act, 1961) two conditions

were required to be satisfied firstly the

Assessing Officer must have reason to believe

that income profits or gains chargeable to income

tax have escaped assessment, and secondly he

must also have reason to believe that such

escapement has occurred by reason of either (i)

omission or failure on the part of the assessee to

disclose fully or truly all material facts necessary

for his assessment of that year. Both these

conditions were conditions precedent to be

satisfied before the Assessing Officer could

have jurisdiction to issue notice under Section

148 read with Section 147(a) (of Income Tax Act, 1961). But under the

substituted Section 147 (of Income Tax Act, 1961) existence of only the

first condition suffices. In other words if the

Assessing Officer for whatever reason has

reason to believe that income has escaped

assessment it confers jurisdiction to reopen the

assessment. It is however to be noted that both

the conditions must be fulfilled if the case falls

within the ambit of the proviso to Section 147 (of Income Tax Act, 1961).

The case at hand is covered by the main provision

and not the proviso.”

9. Commissioner of Income Tax v. Kelvinator of India

Ltd. [(2010) 228 CTR 488] is another case where the

Apex Court had again considered the scope of this

provision and it was held that one needs to give a

schematic interpretation to the words 'reason to

believe', failing which, section 147 (of Income Tax Act, 1961) would give

arbitrary powers to the Assessing Officer to re-open

assessments on the basis of 'mere change of opinion'

which may not be, per se, reason to re-open.

Accordingly, the Apex Court held thus:

“. . . . . However, one needs to give a schematic

interpretation to the words “reason to believe”

failing which, we are afraid, s.147 would give

arbitrary powers to the AO to reopen

assessments on the basis of “mere change of

opinion”, which cannot be per se reason to reopen.

We must also keep in mind the conceptual

difference between power to review and power to

reassess. The AO has no power to review; he has

the power to reassess. But reassessment has to

be based on fulfillment of certain pre-condition

and if the concept of “change of opinion” is

removed, as contended on behalf of the

Department, then, in the grab of reopening the

assessment, review would take place. One must

treat the concept of “change of opinion” as an

inbuilt test to check abuse of power by the AO.

Hence, after 1

st April, 1989, AO has power to

reopen, provided there is “tangible material” to

come to the conclusion that there is escapement

of income from assessment. Reasons must have a

live link with the formation of the belief. Our

view gets support from the changes made to

s.147 of the Act, as quoted hereinabove. Under

the Direct Tax Laws (Amendment) Act, 1987,

Parliament not only deleted the words “reason to

believe” but also inserted the word “opinion” in

s.147 of the Act. However, on receipt of

representations from the companies against

omission of the words “reason to believe”,

Parliament re-introduced the said expression and

deleted the word “opinion” on the ground that it

would vest arbitrary powers in the AO. . . . . . “

10.The Full Bench of Delhi High Court had occasion to

consider the above expression in its judgment in

Commissioner of Income Tax v. Usha International

Ltd. [(2012) 348 ITR 485] and after survey of all

relevant precedents on the subject, the position was

summarised thus:

“It is, therefore, clear from the aforesaid

position that:

(1) Reassessment proceedings can be validly

initiated in case return of income is processed

under Section 143(1) (of Income Tax Act, 1961) and no scrutiny assessment

is undertaken. In such cases there is no change

of opinion.

(2) Reassessment proceedings will be invalid

in case the assessment order itself records that

the issue was raised and is decided in favour of

the assessee. Reassessment proceedings in the

said cases will be hit by the principle of “change

of opinion”.

(3) Reassessment proceedings will be invalid

in case an issue or query is raised and answered

by the assessee in original assessment

proceedings but thereafter the Assessing

Officer does not make any addition in the

assessment order. In such situations it should be

accepted that the issue was examined but the

Assessing Officer did not find any ground or

reason to make addition or reject the stand of

the assessee. He forms an opinion. The

reassessment will be invalid because the

Assessing Officer had formed an opinion in the

original assessment, though he had not recorded

his reasons.

In the second and third situation, the

Revenue is not without remedy. In case the

assessment order is erroneous and prejudicial to

the interest of the Revenue, they are entitled to

and can invoke power under Section 263 (of Income Tax Act, 1961) of the

Act. This aspect and position has been

highlighted in CIT v. DLF Power Ltd. I.T.A.No.973

of 2011 decided on November 29, 2011 - since

reported in [2012] 345 ITR 446 (Delhi) and BLB

Ltd. v. Asst. CIT Writ Petition (Civil)No.6884 of

2010 decided on December 1, 2011 - since

reported in [2012] 343 ITR 129 (Delhi). In the

last decision it has been observed (page 135):

“The Revenue had the option, but did not

take recourse to section 263 (of Income Tax Act, 1961), in

spite of audit objection. Supervisory and

revisionary power under Section 263 (of Income Tax Act, 1961)

is available, if an order passed by the Assessing

Officer is erroneous and prejudicial to the

interest of the Revenue. An erroneous order

contrary to law that has caused prejudiced can

be correct, when jurisdiction under Section

263 is invoked.”

Thus, where an Assessing Officer incorrectly or

erroneously applies law or comes to a wrong

conclusion and income chargeable to tax has

escaped assessment, resort to section 263 (of Income Tax Act, 1961) of the

Act is available and should be resorted to. But

initiation of reassessment proceedings will be

invalid on the ground of change of opinion.”

11.From the principles laid down in the above

judgments, it can be seen that the power under

section 147 (of Income Tax Act, 1961) can be invoked by the

Assessing Officer, if, on the materials available

before him, he has reason to believe that any income

chargeable to tax has escaped assessment in any

assessment year, provided such proceedings are not

barred by the time limit prescribed in the first

proviso to the said section. The requirement that

the Assessing Officer must have 'reason to believe'

cannot be taken to mean that the Assessing Officer

must be satisfied that there exists grounds for

reopening the assessment or the Assessing Officer

should have formed an opinion about the nature of the

final order that is likely to be passed after re-

opening the assessment. The question is whether the

Assessing Officer was justified in re-opening the

assessment for the year 2006-07. For the assessment

year 2006-07, assessment was initially completed

under section 143(1) (of Income Tax Act, 1961). The scope of

enquiry that is permissible in an assessment

proceedings under section 143(1) (of Income Tax Act, 1961) is very limited as

is evident from the section itself, which reads thus:

“143. Assessment - (1) Where a return has been

made under section 139 (of Income Tax Act, 1961), or in response to a

notice under sub-section (1) of section 142 (of Income Tax Act, 1961), such

return shall be processed in the following manner,

namely:-

(a) the total income or loss shall be computed

after making the following adjustments,

namely:-

(i) any arithmetical error in the return; or

(ii) an incorrect claim, if such incorrect claim

is apparent from any information in the

return;

(b) the tax and interest, if any, shall be

computed on the basis of the total income

computed under clause (a);

(c) the sum payable by, or the amount of refund

due to, the assessee shall be determined

after adjustment of the tax and interest, if

any, computed under clause (b) by any tax

deducted at source, any tax collected at

source, any advance tax paid, any relief

allowable under an agreement under section

90 or section 90A (of Income Tax Act, 1961), or any relief allowable

under section 91 (of Income Tax Act, 1961), any rebate allowable under

Part A of Chapter VIII, any tax paid on self-

assessment and any amount paid otherwise

by way of tax or interest;

(d) an intimation shall be prepared or generated

and sent to the assessee specifying the sum

determined to be payable by, or the amount

of refund due to, the assessee under clause

(c); and

(e) the amount of refund due to the assessee in

pursuance of the determination under clause

(c) shall be granted to the assessee:

Provided that an intimation shall also be sent

to the assessee in a case where the loss declared

in the return by the assessee is adjusted but no

tax or interest is payable by, or no refund is due

to him;

provided further that no intimation under

this sub-section shall be sent after the expiry of

one year from the end of the financial year in

which the return is made.”

12.The scope of this provision was considered by the

Apex Court in its judgment in Assistant Commissioner

of Income Tax v. Rajesh Jhaveri Stock Brokers P. Ltd

(supra), where it was held thus:

“It is to be noted that substantial changes

have been made to Section 143(1) (of Income Tax Act, 1961) with effect

from June 1, 1999. Up to March 31, 1989, after a

return of income was filed the Assessing Officer

could make an assessment under Section 143(1) (of Income Tax Act, 1961)

without requiring the presence of the assessee or

the production by him of any evidence in support

of the return. Where the assessee objected to

such an assessment or where the officer was of

the opinion that the assessment was incorrect or

incomplete or the officer did not complete the

assessment under Section 143(1) (of Income Tax Act, 1961), but wanted to

make an inquiry, a notice under Section 143(2) (of Income Tax Act, 1961)

was required to be issued to the assessee

requiring him to produce evidence in support of

his return. After considering the material and

evidence produced and after making necessary

inquiries, the officer had power to make

assessment under Section 143(3) (of Income Tax Act, 1961). With effect

from April 1, 1989, the provisions underwent

substantial and material changes. A new scheme

was introduced and in the new substituted

Section 143(1) (of Income Tax Act, 1961) prior to the subsequent

substitution with effect from June 1, 1999, in

Clause (a), a provision was made that where a

return was filed under section 139 (of Income Tax Act, 1961) or in response

to a notice under section 142(1) (of Income Tax Act, 1961), and any tax or

refund was found due on the basis of such return

after adjustment of tax deducted at source, any

advance tax or any amount paid otherwise by way

of tax or interest, an intimation was to be sent

without prejudice to the provisions of Section

143(2) to the assessee specifying the sum so

payable and such intimation was deemed to be a

notice of demand issued under Section 156 (of Income Tax Act, 1961). The

first proviso to Section 143(1)(a) (of Income Tax Act, 1961) allowed the

Department to make certain adjustments in the

income or loss declared in the return. They were

as follows :

(a) any arithmetical errors in the return,

accounts and documents accompanying it were to

be rectified;

(b) any loss carried forward, deduction,

allowance or relief which on the basis of the

information available in such return, accounts or

documents, was prima facie admissible, but which

was not claimed in the return was to be allowed;

(c) any loss carried forward, relief claimed

in the return which on the basis of the

information as available in such returns accounts

or documents were prima facie inadmissible was

to be disallowed.

What were permissible under the first

proviso to Section 143(1)(a) (of Income Tax Act, 1961) to be adjusted were,

(i) only apparent arithmetical errors in the

return, accounts or documents accompanying the

return, (ii) loss carried forward, deduction

allowance or relief, which was prima facie

admissible on the basis of information available in

the return but not claimed in the return and

similarly (iii) those claims which were on the basis

of the information available in the return, prima

facie inadmissible, were to be rectified/

allowed/disallowed. What was permissible was

correction of errors apparent on the basis of the

documents accompanying the return. The

Assessing Officer had no authority to make

adjustments or adjudicate upon any debatable

issues. In other words, the Assessing Officer

had no power to go behind the return, accounts or

documents, either in allowing or in disallowing

deductions, allowance or relief.”

13.For the assessment year 2006-07, assessment under

section 143(1) (of Income Tax Act, 1961) was completed by order dated

23.12.2008. It was thereafter the Assessing Officer

completed the assessment under section 143(3) (of Income Tax Act, 1961) for the

year 2008-09 by his order dated 30.12.2010. In that

order, the income earned by the assessee in the

purchase and sale of shares as capital gains, was

treated as business income and was taxed. It was

thereafter that proceedings under section 147 (of Income Tax Act, 1961) were

initiated with respect to the assessment year 2006-07

and assessment was completed under section 143(3) (of Income Tax Act, 1961) by

order dated 15.12.2011. The question that is

required to be considered is whether the reopening of

assessment is based on the mere change of opinion of

the Assessing Officer as contended by the counsel for

the appellant.

14.In our view, the aforesaid contention cannot be

accepted. Law mandates that the Assessing Officer

should have reason to believe that income chargeable

to tax has escaped assessment for any assessment year

to invoke the power to re-open assessments under

section 147 (of Income Tax Act, 1961). Admittedly, assessments for the year

2006-07 were completed treating the income in

question as capital gains. Once the assessment for

the year 2008-09 was completed and the income for

that year was assessed as business income, the

Assessing Officer had sufficient materials to believe

that income chargeable to tax as business income for

the assessment year 2006-07 had escaped assessment.

It was on that basis, proceedings under section 147 (of Income Tax Act, 1961)

was initiated. The initiation of such proceedings

under section 147 (of Income Tax Act, 1961), according to us, is fully within

the four corners of section 147 (of Income Tax Act, 1961).

15.It is true that returns treating the income as

capital gains were accepted in the previous

assessment years also. It is on that factual basis

that contention was raised by the assessee that

Department should maintain consistency in the matter

of assessment. In support of this contention,

counsel for the appellant relied on the judgment of

the Bombay High Court in Commissioner of Income Tax

v. Gopal Purohit [(2011) 336 ITR 287]. This again is

an untenable argument for the reason that in the

matter of assessment of income tax, the decision

arrived at in the previous year cannot be regarded as

binding in the assessment for the subsequent years.

It has been so held by the Apex Court in Dwarakadas

Kesardeo Morarka v. Commissioner of Income Tax

[(1962) XLIV ITR 529], the relevant paragraph of

which is extracted herein:

“. . . . . It cannot be said that because in the

previous years the shares were held to be stock-

in-trade, they must be similarly treated for the

assessment year 1949-50. In the matter of

assessment of income-tax, each year's

assessment is complete and the decision arrived

at in a previous year on materials before the

taxing authorities cannot be regarded as binding

in the assessment for the subsequent years. . . . “

Therefore, though consistency is desirable, the

desirability of consistency cannot operate against

the Revenue in completing assessments for subsequent

years in accordance with law. This is all the more

so since the assessments for the previous years were

completed under section 143(1) (of Income Tax Act, 1961). In so far

as the judgment of the Bombay High Court in Gopal

Purohit (supra) is concerned, though the court has

highlighted the need for consistency, it has also

taken note of the fact that in that case, the Revenue

did not furnish any justification for adopting a

divergent approach for the assessment year in

question.

16. It is true, as contended by the learned counsel,

that assessments for the years 2007-08 and 2009-2010

were left out and according to the counsel, the

Revenue has, therefore, adopted a pick and choose

method, choosing the assessment years when the

assessee had returned profit. Though this contention

would appear to be attractive, a closer examination

thereof would show that there is no substance in it.

Admittedly, for the assessment years 2007-08 and

2009-2010, the assessee had returned loss. The

assessment for such years were also completed under

section 143(1) (of Income Tax Act, 1961). Re-opening of those assessments is

permissible only under section 147 (of Income Tax Act, 1961) and power under

that section could be invoked only if any income

chargeable to tax has escaped assessment. Here, in

the instant case, the assessee has returned loss and

therefore, no income chargeable to tax has escaped

assessment, permitting invocation of the power under

this provision.

17.Similar is the case with the revisional power of the

Commissioner under section 263 (of Income Tax Act, 1961), which also can be

invoked only if any order passed is prejudicial to

the interest of the Revenue. Such being the case,

the assessee cannot be heard to complain that the

Revenue has adopted a pick and choose method in the

matter of assessment for the years in question.

18.The main question that arises for consideration is

regarding the legality of assessment treating the

income for the years in question as 'business income'

instead of 'capital gains'.

19.Before we proceed to consider the relevant facts,

it would be appropriate to examine the legal

principles which govern the issue. Although both

sides have cited before us various precedents on the

subject, in our view, having regard to the principles

laid down by the Apex Court in its judgment in

Commissioner of Income Tax, Nagpur v. Sutlej Cotton

Mills Supply Agency Ltd. [(1975) 100 ITR 706], it is

unnecessary to refer to all those judgments. In this

judgment, after referring to various other

authorities, the Apex Court summarised the principles

thus:

“In the absence of any evidence of trading

activity in cases of purchase and resale of

shares, it has been held that profit arising from

the resale is an accretion to the capital. If a

transaction is in the assessee's ordinary line of

business there can be no difficulty in holding

that it is in the nature of trade. But the

difficulty arises where the transaction is outside

the assessee's line of business and then, it must

depend upon the facts and circumstances of each

case whether the transaction is in the nature of

trade.

It is not necessary to constitute trade that

there should be a series of transactions, both of

purchase and of sale. A single transaction of

purchase and sale outside the assessee's line of

business may constitute an adventure in the

nature trade. Neither repetition nor continuity

of similar transactions is necessary to constitute

a transaction an adventure in the nature of

trade. If there is repetition and continuity, the

assessee would be carrying on a business and the

question whether the activity is an adventure in

the nature of trade can hardly arise. A

transaction may be regarded as isolated although

a similar transaction may have taken place a

fairly long time before [see Commissioners of

Inland Revenue v. Reinhold (1953) 34 TC 389].

The principles underlying the distinction

between a capital sale and an adventure in the

nature of trade were examined by this court in

G.Venkataswami Naidu & Co. v. Commissioner of

Income-tax [(1959) 35 ITR 594 (SC)], where this

court said that the character of a transaction

cannot be determined solely on the application of

any abstract rule, principle or test but must

depend upon all the facts and circumstances of

the case. Ultimately, it is a matter of first

impression with the court whether a particular

transaction is in the nature of trade or not. It

has been said that a single plunge may be enough

provided it is shown to the satisfaction of the

court that the plunge is made in the waters of

the trade; but mere purchase/sale of shares-if

that is all that is involved in the plunge-may fall

short of anything in the nature of trade.

Whether it is in the nature of trade will depend

on the facts and circumstances.

Where the purchase of any article or of any

capital investment, for instance, shares, is made

without the intention to resell at a profit, a

resale under changed circumstances would only

be a realisation of capital and would not stamp

the transaction with a business character (see

Commissioner of Income-tax v. P.K.N.Co.Ltd

(1966) 60 ITR 65 (SC).

Where a purchase is made with the intention

of resale, it depends upon the conduct of the

assessee and the circumstances of the case

whether the venture is on capital account or in

the nature of trade. A transaction is not

necessarily in the nature of trade because the

purchase was made with the intention of resale

(see Jenkinson v. Freedland [(1961) 39 TC 636

(CA)], Radha Debi Jalan v. Commissioner of

Income-tax [(1951) 20 ITR 176 (Cal)], India Nut

Co. Ltd. v. Commissioner of Income-tax [(1960)

39 ITR 234 (Ker)], Mrs.Sooniram Poddar v.

Commissioner of Income-tax [(1939) 7 ITR 470,

478-9 (Rang)(FB)], Ajax Products Ltd. v.

Commissioner of Income-tax [(1961) 43 ITR 297,

310 (Mad)], Gustad Irani v. Commissioner of

Income-tax [(1957) 31 ITR 92 (Bom)] and

Mrs.Alexander v. Commissioner of Income-tax

[(1952) 22 ITR 379, 402 (Mad)].

A capital investment and resale do not lose

their capital nature merely because the resale

was foreseen and contemplated when the

investment was made and the possibility of

enhanced values motivated the investment (see

Leeming v. Jones [(1930) 15 TC 333 (HL)] and

also the decisions of this court in Saroj Kumar

Mazundar v. Commissioner of Income-tax [(1959)

37 ITR 242, 250-1(SC)] and Janki Ram Bahadur

Ram v. Commissioner of Income-tax [(1965) 57

ITR 21 (SC)].

In Commissioner of Inland Revenue v. Fraser

[(1942) 24 TC 498, 502] Lord Normand said:

“The individual who enters into a purchase of an

article or commodity may have in view the resale

of it at a profit, and yet it may be that that is

not the only purpose for which he purchased the

article or the commodity, nor the only purpose to

which he might turn it if favourable opportunity

for sale does not occurr.... An amateur may

purchase a picture with a view to its resale at a

profit and yet he may recognise at the time or

afterwards that the possession of the picture

will give him aesthetic enjoyment if he is unable

ultimately, or at his chosen time, to realise it at a

profit.....”

An accretion to capital does not become

income merely because the original capital was

invested in the hope and expectation that it

would rise in value; if it does so rise, its

realisation does not make it income. Lord

Dunedin said in Leeming v. Jones at page 360:

“The fact that a man does not mean to hold an

investment may be an item of evidence tending to

show whether he is carrying on a trade or

concern in the nature of trade in respect of his

investments but per se it leads to no conclusion

whatever.”

This court laid down in G.Venkataswami Naidu

& Co. v. Commissioner of Income-tax [(1959) 35

ITR 594, 610, 622(SC)] that the dominant or

even sole intention to resell is a relevant factor

and raises a strong presumption, but by itself is

not conclusive proof, of an adventure in the

nature of trade.

The intention to resell would, in conjunction

with the conduct of the assessee and other

circumstances, point to the business character of

the transaction.”

20.We may, in this context, also refer to the judgment

of the Apex Court in M/s.Rajputana Textiles

(Agencies) Ltd. v. Commissioner of Income tax,

Bombay City [42 ITR 743], where the contention that

buying and selling in shares was not one of the

objects of the company was rejected and the court

held that this was only one of the circumstances in

the totality of the circumstances which must be

considered, though this by itself is not

determinative of the question. Again, in its

judgment in Sutlej Cotton Mills Ltd. v. Commissioner

of Income Tax, West Bengal [(1979) 116 ITR 1], the

Apex Court held that the way in which entries are

made by the assessee in its books of accounts is not

determinative of the question whether the assessee

has earned any profit or suffered any loss.

Therefore, even if it is accepted that the objects

clause in the Memorandum of Association of the

assessee did not provide for trading in shares and

that in the accounts it was shown as investments,

that by itself would not be determinative of the

issue involved in these appeals.

21.While the precedents that we have referred to above

lead to the irresistible conclusion that it is the

totality of the circumstances which is determinative

of the question as to whether the profit earned by

the assessee is an accretion to the capital or is a

trading profit, it is also relevant that the Central

Board of Direct Taxes issued circular No.4/2007 dated

15.6.2007 indicating the tests to draw a distinction

between the shares held as stock-in-trade and shares

held as investment. This circular being relevant is

extracted below for reference:

C.B.D.T. Circulars

Circular No.4/2007, dated June 15, 2007

Sub: Distinction between shares held as stock-

in-trade and shares held as investment-Tests

for such a distinction.

The Income-tax Act, 1961 makes a

distinction between a capital asset and a trading

asset.

2. Capital asset is defined in section 2(14) (of Income Tax Act, 1961)

of the Act. Long-term capital assets and gains

are dealt with under section 2(29A) (of Income Tax Act, 1961) and section 2 (of Income Tax Act, 1961)

(29B). Short-term capital assets and gains are

dealt with under section 2(42A) (of Income Tax Act, 1961) and section 2 (of Income Tax Act, 1961)

(42B).

3. Trading asset is dealt with under section 28 (of Income Tax Act, 1961)

of the Act.

4. The Central Board of Direct Taxes (CBDT)

through Instruction No.1827 dated August 31,

1989, had brought to the notice of the Assessing

Officers that there is a distinction between

shares held as investment (capital asset) and

shares held as stock-in-trade (trading asset). In

the light of a number of judicial decisions

pronounced after the issue of the above

instructions, it is proposed to update the above

instructions for the information of the assessees

as well as for guidance of the Assessing Officers.

5. In the case of CIT v. Associated Industrial

Development Company (P) Ltd. [1971] 82 ITR 586,

the Supreme Court observed that (headnote):

Whether a particular holding of shares is by

way of investment or forms part of the stock-in-

trade is a matter which is within the knowledge

of the assessee who holds the shares and he

should, in normal circumstances, be in a position

to produce evidence from his records as to

whether he has maintained any distinction

between those shares which are his stock-in-

trade and those which are held by way of

investment.

6. In the case of CIT v. H.Holck Larsen [1986]

160 ITR 67, the Supreme Court observed (page

87):

The High Court, in our opinion, made a

mistake in observing whether transactions of sale

and purchase of shares were trading transactions

or whether these were in the nature of

investment was a question of law. This is a mixed

question of law and fact.

7. The principles laid down by the Supreme

Court in the above two cases afford adequate

guidance to the Assessing Officers.

8. The Authority for Advance Rulings (AAR)

[2007] 288 ITR 641, referring to the decisions

of the Supreme Court in several cases, has culled

out the following principles (page 651):

(i) Where a company purchases and sells shares,

it must be shown that they were held as stock-in-

trade and that existence of the power to

purchase and sell shares in the memorandum of

association is not decisive of the nature of

transaction;

(ii) the substantial nature of transactions, the

manner of maintaining books of account, the

magnitude of purchases and sales and the ratio

between purchases and sales and the holding

would furnish a good guide to determine the

nature of transactions;

(iii) ordinarily the purchase and sale of shares

with the motive of earning a profit, would result

in the transaction being in the nature of

trade/adventure in the nature of trade; but

where the object of the investment in shares of

a company is to derive income by way of dividend

etc. then the profits accruing by change in such

investment (by sale of shares) will yield capital

gain and not revenue receipt.

9. Dealing with the above three principles, the

AAR has observed in the case of Fidelity group as

under (page 661):

We shall revert to the aforementioned

principles. The first principle requires us to

ascertain whether the purchase of shares by a

FII in exercise of the power in the memorandum

of association/trust deed was as stock-in-trade

as the mere existence of the power to purchase

and sell shares will not by itself be decisive of

the nature of transaction. We have to verify as

to how the shares were valued/held in the books

of account i.e., whether they were valued as

stock-in-trade at the end of the financial year

for the purpose of arriving at business income or

held as investment in capital assets. The second

principle furnishes a guide for determining the

nature of transaction by verifying whether there

are substantial transactions, their magnitude,

etc. maintenance of books of account and finding

the ratio between purchases and sales. It will

not be out of place to mention that regulation 18

of the SEBI Regulations enjoins upon every FII

to keep and maintain books of account containing

true and fair accounts relating to remittance of

initial corpus of buying and selling and realizing

capital gains on investments and accounts of

remittance to India for investment in India and

realising capital gains on investment from such

remittances. The third principle suggests that

ordinarily purchases and sales of shares with the

motive or realising profit would lead to inference

of trade/adventure in the nature of trade; where

the object of the investment in shares of

companies is to derive income by way of dividends

etc., the transactions of purchases and sales of

shares would yield capital gains and not business

profits.

10. The Central Board of Direct Taxes also

wishes to emphasis that it is possible for a tax

payer to have two portfolios, i.e., an investment

portfolio comprising of securities which are to be

treated as capital assets and a trading portfolio

comprising of stock-in-trade which are to be

treated as trading assets. Where an assessee

has two portfolios, the assessee may have income

under both heads i.e., capital gains as well as

business income.

11. The Assessing Officers are advised that

the above principles should guide them in

determining whether, in a given case, the shares

are held by the assessee as investment (and

therefore giving rise to capital gains) or as stock-

in-trade (and therefore giving rise to business

profits). The Assessing Officers are further

advised that no single principle would be decisive

and the total effect of all the principles should

be considered to determine whether, in a given

case, the shares are held by the assessee as

investment or stock-in-trade.

12. These instructions shall supplement the

earlier Instruction No.1827 dated August 31,

1989.

22.Bearing the above in mind, we may now proceed to

consider the facts that are available before us to

decide whether the authorities were right in treating

the sale of shares as business income as against

capital gains. The transactions during the

assessment year 2008-09, as reflected in the order of

the Tribunal, show that the assessee has traded in

the shares of 45 companies. Among the 45 companies,

the maximum weighted holding period is in respect of

219,641 shares held by the assessee in M/s.JK Investo

Trade and the minimum weighted holding period is in

respect of 30000 shares of KITEX Garments traded by

it. If the average holding period of the 45 scrips

held by the assessee is taken, in the case of 36

shares, it ranges from 91 days to 3 days. The

Tribunal has also referred to the frequency of

purchases and sales which show that during the

assessment years 2006-07, 2008-09 and 2010-11 the

assessee company had purchased and sold shares in 62

companies, 53 companies and 78 companies

respectively. It is also seen that the scrip wise

purchase to sales also indicate that in the

assessment year 2006-07, while the company purchased

shares in 55 companies, it had sold shares in 57

companies. In the assessment year 2008-09, the

company purchased 51 scrips and sold 45 scrips.

Similarly, during the assessment year 2010-11, while

it purchased scrips in 67 companies, it had sold

scrips in 72 companies.

23.The authorities have also taken note of the fact

that the assessee has all the infrastructure for

buying and selling shares and that it has incurred

establishment expenses and various establishment

expenses have been charged to Profit and Loss Account

which indicated an organised and systematic activity

carried on by the assessee. It was also found that

the income earned by the company in the form of

dividend was only in respect of very few scrips which

gave a very low rate of return as compared to the

value of shares held by it. Yet another finding that

has been entered into is that the involvement of the

assessee in the trading of shares was not an

occasional one but was carried on by it in a

systematic and organised manner. The authorities

have also found that the short period of holding of

shares reveal that the assessee had no intention to

hold the shares for longer term as an investment.

These findings of the authorities below are

absolutely unassailable and therefore, the fact that

trading in shares is not the main object of the

assessee or that the shares were shown as stock-in-

trade in the books of accounts of the assessee cannot

be of any consequence.

24.It is true as contended by the learned counsel for

the assessee that it is possible for an assessee to

have more than one portfolio, viz., that a part of

the shares could have been held by it as investment

and the remaining part, as stock-in-trade. Such a

distinction has been recognised by the Central

Government in circular No.4/07 (supra). This

submission was made mainly with reference to the

219,641 shares of M/s.JK Investo Trade held by the

assessee, which has the maximum weighted holding

period. In so far as these shares are concerned,

along with I.A.1518/15, the Revenue has produced

before us the details of acquisition of these shares

which show that the company acquired these shares

over a period of time from 8.12.2005 to 1.12.2006 and

sold these shares during the period from 4.4.2007 to

26.11.2007. This particular transaction has been

discussed in the assessment order for the year 2008-

09, where the Assessing Officer has found thus:

“16. In order to see whether the shares of JK

Investo Trade Ltd. was held by the assessee as

an investment or as a prudent step to earn more

income, the price value chart of the above said

share for the period 1.12.2005 to 30.11.2007 was

called for. The papers presented by the assessee

is annexed as Annexure B, C & D. The assessee

started purchasing the share on 8.12.2005 and

went on buying it continuously till 1.12.2006. It

started selling it off in 4.4.2007 and sold off the

entire shares by 26.11.2007. Now a look at the

price value chart show that except for a rise for

the period May, 2006 to August, 2006, the price

of the share was almost statue till June-July,

2007. It started shooting upon in August 2007

and assessee started selling it in Sept., 2007 and

the entire shares were sold off in Nov. 2007.

Thus, it can be seen that holding of this share is

not with an investors mind, but with a real

business man's mind to sell it off at the right

time. This instance itself shows that the

assessee was not a mere investor but a prudent

business man making the right calculation to see

when to buy and when to sell, which share. This

is definitely an adventure in the nature of trade.

It may also be seen that though the assessee had

held this share for a long period, it was engaged

in buying and selling all the time throughout the

year.”

25. The factual correctness of the findings of the

Assessing Officer was not disputed at any stage of

the proceedings. It was on the basis of the

assessment for the year 2008-09 that the assessment

for the year 2006-07 was re-opened and the same

standard has been applied in respect of the

assessment for 2010-11 also. These findings, the

factual correctness of which has been concurrently

confirmed by the first appellate authority and the

Tribunal, when appreciated in the light of the

principles laid down by the Apex Court in

Commissioner of Income Tax, Nagpur v. Sutlej Cotton

Mills Supply Agency Ltd. [(1975) 100 ITR 706],

only leads to the conclusion that the assessee was

engaged in trading in shares and was not holding the

shares as stock-in-trade to contend that the

accretions are only capital gains. In such

circumstances, the questions of law raised will have

to be answered in favour of the Revenue.

Appeals are dismissed.

Sd/-

ANTONY DOMINIC, Judge.

Sd/-

SHAJI P. CHALY, Judge.

×

Similar Ripples

Questions

Court rules on tax liability for individuals claiming exemption under Section 194A(1) (of Income Tax Act, 1961).

Write your CommentSimilar Posts

Generic

- Reportdata/3658.pdf