Court upholds ₹2 crore tax addition on unexplained cash found during CBI raid

Full News

Court upholds ₹2 crore tax addition on unexplained cash found during CBI raid

Court upholds ₹2 crore tax addition on unexplained cash found during CBI raid

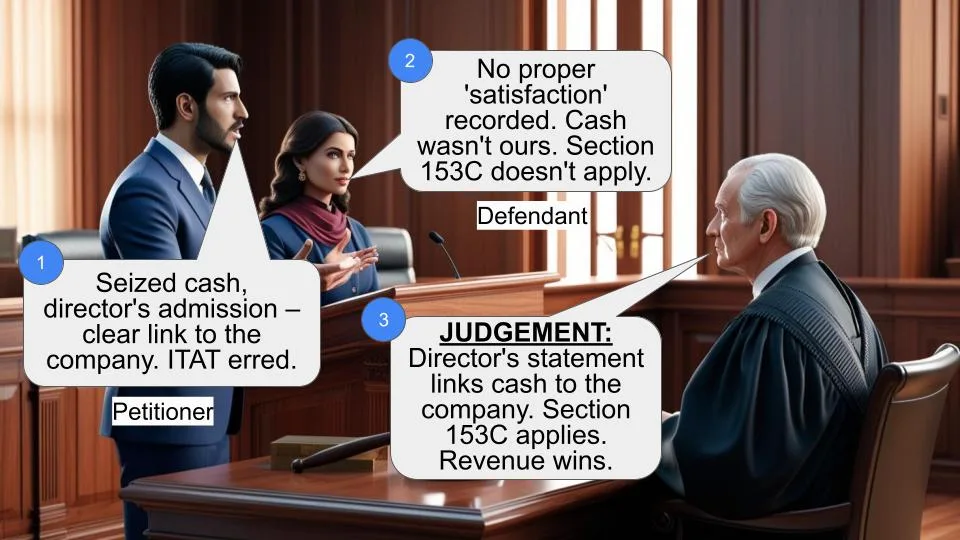

This case involves Jatinder Pal Singh, who was caught with ₹2 crores in cash during a CBI raid. The Income Tax Department added this amount to his taxable income under Section 69A (of Income Tax Act, 1961), treating it as “unexplained money.” Singh challenged this addition all the way up to the High Court, claiming the money was an advance payment for selling agricultural land. However, the court found his explanation unconvincing and upheld the tax addition.

Get the full picture - access the original judgement of the court order here

Case Name

Jatinder Pal Singh vs Deputy Commissioner of Income Tax (High Court of Delhi)

ITA 16/2021

Date: 8th February 2021

Key Takeaways

- Possession equals ownership: When cash is found in someone’s possession during a search, they’re presumed to be the owner unless they can prove otherwise

- Burden of proof: The person found with unexplained money must provide a satisfactory explanation for its source and nature

- Section 69A (of Income Tax Act, 1961) application: Courts will uphold additions under Section 69A (of Income Tax Act, 1961) when explanations are found to be fabricated or inconsistent

- Evidence scrutiny: Tax authorities can reject explanations based on contradictions and lack of supporting documentation

Issue

Whether the Income Tax Appellate Tribunal was correct in upholding the addition of ₹2 crores to the appellant’s income as unexplained money under Section 69A (of Income Tax Act, 1961).

Facts

In 2010, the CBI conducted a search operation at Jatinder Pal Singh’s premises and seized ₹2 crores in cash. On the same day, the Income Tax Department also conducted their own search under Section 132 (of Income Tax Act, 1961).

During questioning under Section 132(4) (of Income Tax Act, 1961), Singh initially claimed the money was an advance payment for selling 50 acres of agricultural land in Faridabad for ₹6 crores, received from someone named Mr. Sharma.

Later, during assessment proceedings for the 2011-12 tax year, Singh changed his story slightly, saying he received the ₹2 crores from Mr. Rahul Ahuja through a broker named Mr. Sanjeev Kumar Sharma.

The Assessing Officer conducted detailed inquiries, issued notices under Section 133(6) (of Income Tax Act, 1961), and recorded statements from all parties involved. However, the stories didn’t match up - there were contradictions about the land area (50 acres vs 30 acres), the total consideration (₹6 crores vs ₹4 crores), and other key details.

Arguments

Singh’s Arguments (through his lawyer Mr. Ajay Vohra):

- The cash was legitimately received as advance payment for land sale

- He had fully explained the nature and source of the money

- The Assessing Officer relied on mere suspicions and conjectures

- Since the authorities found it was bribe money, he was just a “conduit” and not the actual owner, so Section 69A (of Income Tax Act, 1961) shouldn’t apply

- The addition was made without specifying the exact legal provision

Income Tax Department’s Arguments (through Mr. Deepak Anand):

- Singh’s explanations were full of contradictions and discrepancies

- He couldn’t produce original documents like the MOU (Memorandum of Understanding)

- The entire story about land sale was fabricated to escape taxation

- The way the related court case was settled indicated the transaction was fake

Key Legal Precedents

The court relied on several important precedents:

- Section 69A (of Income Tax Act, 1961): This section deals with unexplained money and states that if someone is found to be the owner of money and either offers no explanation or an unsatisfactory explanation about its source, it can be deemed as income

- Section 110 of the Evidence Act: This establishes that when someone is found in possession of something, the burden is on them to prove they’re not the owner

- Durga Prasad More 82 ITR 540 (SC) and Sumati Dayal 214 ITR 80 (SC): The Supreme Court held that courts must judge evidence by applying the “test of human probability”

- Sukh Ram v. ACIT, [2007] 159 TAXMAN 385(Delhi): This case established that for Section 69A (of Income Tax Act, 1961) additions, possession is evidence of ownership, and the presumption is strongest for cash

- Chuharmal Vs. Commissioner of Income Tax (1988) 3 SCC 588: The Supreme Court approved that possession creates presumption of ownership, and the person must prove they’re not the owner

Judgement

The High Court dismissed Singh’s appeal completely. Here’s their reasoning:

Court’s Logic:

- Singh was found in physical possession of ₹2 crores and didn’t deny ownership initially

- His explanations were riddled with contradictions and inconsistencies

- The stories told by Singh, Mr. Sharma, and Mr. Ahuja didn’t match on basic facts

- No original documents were produced to support the land sale story

- The timing and circumstances made the explanation highly improbable

Key Findings:

- The purported land sale transaction was a “sham”

- The MOU and receipts were fabricated documents created as an “afterthought”

- Singh failed to discharge his burden of proving the legitimate source of the money

- The addition under Section 69A (of Income Tax Act, 1961) was legally justified

The court specifically noted that even if the money was bribe money (as the CBI alleged), Singh’s explanation to the tax authorities was about land sale, which was found to be false. Therefore, the addition was proper.

FAQs

Q1: What is Section 69A (of Income Tax Act, 1961) and when does it apply?

A: Section 69A (of Income Tax Act, 1961) deals with “unexplained money.” If you’re found with money that’s not recorded in your books and you can’t satisfactorily explain its source, the tax department can treat it as your income for that year.

Q2: Why couldn’t Singh argue he was just holding the money for someone else?

A: The court noted that Singh never made this argument to the tax authorities. Instead, he claimed it was advance payment for land sale. You can’t change your explanation later in court.

Q3: What made Singh’s explanation unbelievable?

A: Multiple factors: contradictory statements about land area and price, no original documents, suspicious timing of cash withdrawal vs. payment, and the fact that someone with banking facilities kept ₹2 crores in cash for months.

Q4: Does this mean anyone found with cash will be taxed?

A: No, but you need to provide a satisfactory explanation with proper documentation. The key is consistency and credibility of your explanation.

Q5: Can the tax department rely on CBI findings?

A: The court clarified that tax authorities make independent assessments. They can consider CBI findings but must evaluate the taxpayer’s explanation on its own merits.

1. For the reasons stated in the application, the delay of 25 days in re-

filing the present appeal is condoned.

2. The application stands disposed of.

ITA 16/2021

3. The present appeal under Section 260A (of Income Tax Act, 1961)

is directed against the order dated 1st November, 2019 passed under Section

254(1) of the Income Tax Act, 1961 [hereinafter referred to as „the Act‟], by the Income Tax Appellate Tribunal [hereinafter referred to as „ITAT‟] in

ITA No. 621/DEL/2015 for the Assessment Year 2011-12, whereby the

appeal of the Appellant-Assessee was dismissed and consequently the

addition to the extent of ₹ 2 crores to his income made by the Assessing

Officer has been upheld.

4. The brief factual matrix giving rise to the present appeal is that a

search operation was conducted by the Central Bureau of Investigation

[hereinafter referred to as „CBI‟] at the premises of the Appellant, during

which cash of Rs. 2 crores was seized. Subsequently, based on the

information provided by the CBI, the Director of Income Tax (Investigation)

conducted another search under Section 132 (of Income Tax Act, 1961) on the very same

day. In this search proceeding, the statement on oath of the Appellant was

recorded under Section 132(4) (of Income Tax Act, 1961), wherein he sought to contend that

the amount of Rs. 2 crores was received by him as advance for sale of

agricultural land at Faridabad. Total area of the land was stated to be 50

acres and agreed price for the sale was disclosed as ₹ 6 crores. He further

stated that the amount was received from one Mr. Sharma and receipt

against the advance of ₹ 2 crores was issued by the Assessee, although at the time of the search, the Appellant did not possess a copy of the same.

5. Subsequently, in the assessment proceeding for AY 2011-12, the

Appellant submitted that he had received the cash amounting to ₹ 2 crores as

advance from one Mr. Rahul Ahuja through the broker- Mr. Sanjeev Kumar

Sharma. Independent enquiries were conducted by the Assessing Officer,

notice under section 133(6) (of Income Tax Act, 1961) was issued to Mr. Ahuja, and

documents were obtained from him, which included a copy of a

Memorandum of Understanding dated 12th April, 2010 purported to be

executed between him and the Appellant for purchase of the said agricultural

land [hereinafter referred to as „MOU‟]. Mr. Ahuja submitted that the

payment of ₹ 2.01 crores was made to the appellant in cash, which was

withdrawn from the bank account maintained him. Later, the authorised

representative of Mr. Ahuja orally stated that the latter had filed a suit for recovery of the advance of ₹ 2.01 crores against the Appellant. In order to carry out further enquiry and verification in relation to the source of the cash found and seized from the premises of the Appellant, the Assessing Officer recorded the statements of Mr. Ahuja and Mr. Sharma, pursuant to summons issued under section 130 (of Income Tax Act, 1961). Ultimately, the Assessing Officer, after consideration of the testimonies and other evidence furnished by the Appellant, framed the assessment vide order dated 28th March, 2013 and added the amount of Rs. 2 crores to the income of the Appellant. Aggrieved with the aforesaid order, the Appellant preferred an appeal before the Commissioner of Income Tax (Appeals) [hereinafter referred to as

„CIT(A)‟]. The CIT(A), after considering the submissions of the Appellant,

directed the Assessing Officer to conduct further enquiry by summoning all

persons involved in the alleged transaction of sale and to confirm the status of the pending suit of recovery in the court at Faridabad. Pursuant thereto, the Assessing Officer, furnish a remand report, considering which, the CIT(A) rejected the submissions of the appellant and confirmed the addition.

The matter was then carried up in further appeal before the ITAT which

upheld the order passed by the Assessing Officer, as confirmed by the

CIT(A) and sustained the impugned addition of Rs. 2 crores in the hands of

the Appellant. Aggrieved, the Appellant has preferred the present appeal

under section 260A (of Income Tax Act, 1961), raising substantial questions of law as

follows:

(i) „Whether on the facts and in the circumstances of the case, the Tribunal

erred in law in upholding the addition of ₹ 2 crores made by the

Assessing Officer in the hands of the appellant representing cash found

and seized during the course of search?

(ii) Whether on the facts and in the circumstances of the case, the order passed by the Tribunal is perverse inasmuch as it relies upon various irrelevant facts and fails to consider the relevant/ material facts?‟

6. Mr. Ajay Vohra, learned Senior Counsel appearing for the Appellant,

submits that the CIT(A) and the Tribunal, while upholding the addition, have

been completely silent as to under which provision of the Act, the aforesaid

addition was sustainable. He presses that even if assuming the exercise of

the Assessing Officer to be in terms of the scheme of the Act, the only

provision which provides for bringing to tax the purported “unexplained

money” in the hands of an assessee is Section 69A (of Income Tax Act, 1961). He submits

that in order to qualify for addition under said provision, the conditions

specified therein are required to be fulfilled, which evidently is not in the present case. He puts forth that the appellant had duly and fully explained the “nature and source” of the amount of Rs. 2 crores found and seized by the CBI in the course of the search conducted by it, however, the Assessing Officer, on the basis of mere conjectures and suspicion, disregarded the explanation offered by the appellant by placing reliance on the enquiry conducted by the CBI. Mr. Vohra further submits that the addition under section 69A (of Income Tax Act, 1961) can only be made in respect of an assessee who is found to be the owner of the money. The findings of the Assessing Officer do not support the conclusion drawn by him for making the addition. The Assessing Officer has held, the amount recovered pertained to illegal gratification obtained for securing favour for Gyan Sagar Medical College and Hospital, Patiala. Thus, he submits that in view of the above finding, the Appellant can only be held to be acting merely as a conduit for the passage of money and cannot be deemed to be the „owner‟ of such cash, warranting additions in his hands under section 69A (of Income Tax Act, 1961). In these circumstances the cash cannot partake the character of income assessable in the hands of the appellant. Mr. Vohra also argues that there was sufficient explanation given by the Assessee during the course of the assessment proceedings to explain the nature and source of the amount of Rs. 2 crores recovered from his possession, and thus the findings of the Assessing Officer as well as the other tax authorities disregarding the same are perverse. In an attempt to demonstrate that the reasoning of the Assessing Officer is based on suspicion and conjectures, Mr. Vohra also drew our attention to a table wherein explanation/rebuttal is given to the findings of the Assessing Officer regarding the discrepancies in the statements of the appellant vis-à-vis those of Mr. Sharma and Mr. Ahuja.

7. Mr. Deepak Anand, learned Senior Standing Counsel appearing on an

advance notice, submits that in the instant case the Appellant should in fact be prosecuted for making false statements. He referred to several

contradictions and discrepancies in the stand taken by the Appellant and

urged that the Appellant has not been able to offer any satisfactory

explanation for the cash in question and thus, the conclusion drawn by the

Assessing Officer is justified. He argues that the material on record

demonstrates that the Appellant did not correctly disclose the area of the

land that sought to be sold under the purported MOU. The Appellant also

did not produce the original MOU and further the manner in which the suit

filed by the purchaser was compromised indicates that the entire version put

forth by him to explain the cash found in his possession was concocted and

contrived to escape taxation.

8. We have given our thoughtful consideration to the rival contentions of

the parties. The findings of the tax authorities and in particular the Assessing Officer, are based on the testimonies and evidence gathered during the course of the assessment. When the cash was found during the search

conducted at the premises of the Appellant and his statement was recorded

under section 132(4) (of Income Tax Act, 1961), he did not disclaim ownership over the

same. On the contrary, he sought to explain the „nature, purpose and source‟

of the said amount by contending that the amount was received by the

Appellant as an “advance for sale of agricultural land at Faridabad”. In the

course of the ensuing assessment proceedings, the Appellant submitted that

the amount of ₹ 2 crores was received in the form of cash advance from Mr.

Rahul Ahuja, through a broker. Appellant made full efforts to support this

contention and testimonies were recorded. The said explanation has not been

accepted since there were glaring discrepancies in the statement made by the

Appellant vis.-à-vis. the statements made by Sh. Sanjeev Sharma and Sh.

Rahul Ahuja. Their stand was divergent even on basic facts such as the area

of the land and the agreed price. The Assessee has deposed that no

agreement was signed, however Mr. Rahul Ahuja submitted a copy of MOU

dated 12th April, 2010 and in this view of the matter, the statement of Mr.

Rahul Ahuja was held to be unreliable. As rightly pointed out by Mr.

Deepak Anand, it is indeed strange that the original MOU was not produced

during the assessment proceedings. The Assessing Officer carefully and

meticulously examined the statements and arrived at a conclusion that the

purported transaction of sale was sham. He then observed that the appellant

had presented a story “to cover up the cash found and seized by the CBI at

his residence”. In this regard, he has referred to the findings of CBI and

observed that the “findings are further corroborated by the investigations

carried out by the CBI and the charge sheet”. In this background the AO

concluded “the amount of cash recovered was not any advance money

received by him for sale of so called land at Faridabad.” The ITAT has

agreed with the conclusions drawn by the AO while observing as under:

“7. (...) There is a discrepancy with regard to land agreed to be sold

was whether for 50 Acres or 30 Acres. The consideration also differ

whether it was for 6 Acre or 4 Acre. Nothing have been explained by

the assessee to the satisfaction of the authorities below. The assessee

has stated in his statement that no agreement was signed. However,

Shri Rahul Ahuja submitted copy of MOU Dated 12.04.2010.

Therefore, the statement of Shri Rahul Ahuja was not reliable. It

would not prove any genuine transaction entered into between the

assessee and Shri Rahul Ahuja. The assessee never produced original

of the MOU or receipt before the authorities below. The photo copies

of the MOU produced was not having back side to show stamping

done by the Stamp Vendor as to when the said papers were purchased

for preparing the MOU. It is also a fact that no copy of MOU or

receipt of amount were found from the possession of the assessee

during the course of search by the CBI or Income Tax Department.

Though the assessee claimed to have agreed to sale 50 Acres of land

for a consideration of Rs.6 crores, but, the MOU allegedly signed by

Shri Rahul Ahuja and assessee clearly mentioned the land under sale

to be 30 Acres and was sold for a consideration of Rs.4 crores only.

The Ld. CIT(A) on examination of the documents on record has given

a specific finding that share of the assessee comes to 30/130 share i.e.,

approximately 4 Acres of land. Learned Counsel for the Assessee

during the course of arguments did not explain any of the discrepancy

found in the statement of these persons and the calculation made by

the Ld. CIT(A) regarding area of the land to be approximately 4

Acres. There are contradictions in the statements of assessee and

others with regard to month of the first meeting, place of meeting,

area of land to be sold and sale consideration which is not explained

by the assessee through any reliable and cogent evidence. The figure

of the sale consideration is also differed as assessee has stated it to be

Rs. 2 crores received as advance, but, other 02 persons stated it to be

Rs. 2.01 crores. Shri Rahul Ahuja while explaining the source has

stated in his statement that he has withdrawn the cash from his Bank

account in January and February, 2010, but, did not explain why huge

cash was kept when he was having banking facility. There is a

significant gap between cash withdrawn from the Bank account of Shri

Rahul Ahuja in January and February, 2010 and allegedly paid to the

assessee in April, 2010. The assessee failed to explain this discrepancy

as well. Shri Rahul Ahuja filed suit against the assessee on 23.01.2013

after lapse of several years when the matter was going on at

assessment stage. The inconsistencies in the statements of these

persons have not been explained by assessee. Thus, there are serious

doubts about the alleged transaction of sale of land. It is highly

unbelievable that a person who is having banking facility kept

substantial amount of Rs.2 crores in cash with him for more than two

months. The assessee at the time of making statement has clearly

agreed that no Agreement to Sell pertaining to the sale of agricultural

land was executed between the parties. When there was a substantial

difference between the area of the land to be sold and consideration,

there was no reason to record lesser amount or lesser area in MOU

signed by the assessee. The assessee at the time of search by CBI did

not explain the details of persons who has given the amount in

question to the assessee. No mode of payment was also explained. It,

therefore, appears that entire story have been cooked-up by the

assessee later on and is clearly an afterthought. According to Section

110 of Evidence Act when assessee was found in possession of Rs. 2

crores at the time of search by CBI and assessee denied the ownership

of the same, the burden would be upon the assessee to prove as to who

was the owner of the cash found from his residence and possession.

However, the assessee failed to discharge onus upon him to prove as

to who is the lawful owner of the cash found during the course of

search. Therefore, it is the liability of the assessee to explain the

possession of the cash found during the course of search by CBI. It

may also be noted here that during the course of arguments, Learned

Counsel for the Assessee did not made any allegation against CBI who

have recovered Rs. 2 crores from the residence of the assessee during

the course of search. (...) There was specific information received by

CBI and conversation of all the persons have been recorded by the

CBI. Nothing have been explained in this regard with regard to

allegations made against the assessee and others in the charge-sheet

submitted by the CBI and reproduced by the Assessing Officer in the

assessment order. Considering the totality of the facts and

circumstances of the case and that there was substantial gap between

withdrawal of cash by Shri Rahul Ahuja and alleged payment to the

assessee. Therefore, assessee has failed to explain source of the cash

of Rs. 2 crores found from his possession during the course of search

by the CBI. The entire case set-up by the assessee is clearly an

afterthought. The MOU and receipt are sham documents and

fabricated by the assessee and others later on which fact is further

strengthened by the fact that no original of MOU and receipt have

been produced before the authorities below. Otherwise, the same

could have been subjected to verification by CFSL. Copy of the MOU

was produced, but, it was not having the back side which could have

throw light on the fact as to when the said stamp paper were

purchased and whether stamp papers were genuine or not. All these

facts and circumstances clearly prove that assessee has no

explanation whatsoever of the cash found from his possession during

the course of search by the CBI. The Hon‟ble Supreme Court in the

case of Durga Prasad More 82 ITR 540 (SC) and in the case of

Sumati Dayal 214 ITR 80 (SC) has held that “the Courts and

Tribunals have to judge the evidence before them by applying the test

of human probability”. If the said test is applied in this matter, it is

clearly established that the assessee has failed to prove source of Rs. 2

crores found during the course of search by the CBI at his residence.

Thus, appeal of assessee has no merit (...)”

9. The Appellant was found to be in possession of the amount in

question. Thus the onus lay on him to explain the „nature and source‟ and on

this account, the appellant has failed and therefore the amount is

unexplained/unaccounted for. The explanation offered by the appellant has

not been found to be satisfactory by the tax authorities in light of the

discrepancies and anomalies in the statements of the appellant vis-à-vis

those of Mr. Sharma and Mr. Ahuja. In terms of Section 69A (of Income Tax Act, 1961), in

case the assessee offers no explanation about the nature and source of the

acquisition of money, or in case the explanation offered by him is not

satisfactory in the opinion of the Assessing Officer, then the value of the

money may be deemed to be the income of the assessee. The concurrent and

consistent findings of fact recorded by the tax authorities rejecting the

explanation given by the assessee has resulted in adding the amount in

question to the income of the assessee under Section 69A (of Income Tax Act, 1961) and we do not find

any perversity in the same in order to entertain the present appeal. The test of human probabilities applied by the tax authorities buttresses the

conclusion drawn by them and justifies the denunciation of the incredulous

story portrayed by the Appellant. In Sukh Ram v. ACIT, [2007] 159

TAXMAN 385(Delhi), this Court has taken the view that for an addition

under Section 69A (of Income Tax Act, 1961), possession is evidence of ownership, and the

presumption of ownership is the strongest in case of cash, because its title

can be transferred by mere delivery of possession, and thus onus is on the

Assessee to prove that he is not the owner of the currency in his possession.

10. The aforesaid findings are purely findings of fact which have been

concurrently accepted by the CIT(A) as well as the ITAT. We cannot re-

appreciate the evidence, particularly when we see no perversity in the

findings of the ITAT. As regards the contention of Mr. Vohra, that the

finding recorded by the Assessing Officer that the amount of Rs. 2 crores

was for an illegal gratification, contradicts the conclusion drawn by him, we would say that firstly, we perceive no such contradiction. Secondly, on a

pointed query raised by the Court, Mr. Vohra refutes that the amount in

question was illegal gratification. Thus, the plea of being a conduit is a

pretext to evade tax. Thirdly, to our mind, the observations of the tax

authorities are on independent examination of the case and not entirely

resting on the case which has been set up by the CBI. As far as the Income

Tax proceedings are concerned, since the explanation offered by the

Appellant has not been found to be satisfactory, the addition is in accordance of law. In view of the consistent findings of the fact, no questions of law, much less any substantial question of law, arises for our consideration.

11. In view of the above, the present appeal is dismissed.

RAJIV SAHAI ENDLAW, J.

12. I have perused the order aforesaid dictated by Sanjeev Narula, J. and

though concur in entirety with the same but would like to address another

aspect.

13. The senior counsel for the appellant, being fully aware that from the

concurrent findings of fact, of the Assessing Officer, CIT and ITAT, no

substantial question of law arises, stressed on substantial question of law qua interpretation on Section 69A (of Income Tax Act, 1961), arising in the facts of the case. It is his contention that for addition to income to be made under Section 69A (of Income Tax Act, 1961), the assessee has to be found to be the owner of the money. It is argued that neither the Assessing Officer nor the CIT nor the ITAT have found the appellant in the present case to be the owner of the money found in cash in possession of the appellant and added to the income of the appellant. It is further argued that on the contrary there is a specific finding, of the appellant not being the owner of the said money.

14. Section 69A (of Income Tax Act, 1961) is as under:

“69A. Unexplained money, etc.—Where in any financial year the

assessee is found to be the owner of any money, bullion, jewellery or

other valuable article and such money, bullion, jewellery or valuable

article is not recorded in the books of account, if any, maintained by

him for any source of income, and the assessee offers no explanation

about the nature and source of acquisition of the money, bullion,

jewellery or other valuable article, or the explanation offered by him

is not, in the opinion of the Assessing Officer, satisfactory, the money

and the value of the bullion, jewellery or other valuable article may be

deemed to be the income of the assessee for such financial year.”

15. Attention is next drawn to the impugned order of the ITAT, recording

from the order of the Assessing Officer, as under:

“The above facts and discussion proves beyond doubt that the

transactions claimed to have been made by the assessee with Sh.

Ahuja is only a sham transaction. It was purportedly done to cover up

the cash found and seized by CBI at his residence which was illega

gratification meant to obtain favour from S. Ketan Desai, the then

President of Medical Council of India for obtaining recognition of

courses and grant of permission in respect of M/s Gyan Sagar

Medical College and Hospital, Patiala. The above findings are

further corroborated by the investigations carried out by the CBI and

the chargesheet (under Section 173 (of Income Tax Act, 1961) Cr.P.C.) .... against Dr. Ketan

Desai and others."

AND

recording the arguments of the Revenue before the ITAT as under:

“In this matter, the CBI received a source information, on the basis of

which, enquiry was conducted during which, mobile phones were

intercepted. The team was deployed at the residence of the assessee

who was coming to deliver the bribe amount of Rs.2 crores. The CBI

apprehended Dr. Kamaljeet Singh while coming out of the residence

of the assessee on 22.04.2010 at about 12:50 hours. On his

disclosure, Rs.2 crores was recovered from the office located at the

ground floor of the residential premises of the assessee at Vasant

Vihar, New Delhi. All these facts are mentioned in the bail order of

the assessee...... the transcript of the conversations between Dr. Ketan

Desai, Sukhwinder Singh and assessee, Sh. Kamaljeet Singh, Sh. K.A.

Paul and Sh. N.S. Bhango reveal that conversations were corelatable

to the dates on which the event took place. The conversation clearly

reveals that it was a bribe amount to be paid.... "

AND

to the findings of the ITAT itself, as under:

“Therefore, there is no reason to disbelieve the case set up by the CBI

and the Income Tax Department against the assessee. The Assessing

Officer has reproduced certain material based on chargesheet filed by

the CBI against the assessee and others, in which the CBI has clearly

mentioned that there was a criminal conspiracy between assessee, Dr.

Sukhwinder Singh and others to get a favour from Sh. Ketan Desai for

approval of MBBS course..... the entire case set up by the assessee is

clearly an afterthought. The MOU and receipt are sham documents

and fabricated by the assessee and others later on which fact is

further strengthened by the fact that no original MOU and receipt

have been produced before the authorities below.”

16. The senior counsel for the appellant, on the basis of the aforesaid

contended that since the Assessing Officer, CIT and ITAT have held

the said sum of Rs.2 crores to be bribe money, in possession of the

assessee, for payment to Dr. Ketan Desai, the assessee cannot be said to

have been found to be the owner thereof within the meaning of Section

69A.

17. We are however of the opinion that no substantial question of

law arises. A plain reading of Section 69A (of Income Tax Act, 1961) shows the expression

“found to be the owner”, to be meaning, found to be exercising any

right as owner. Possession and / or custody of money is a facet of

ownership and thus, during the raid by CBI and Revenue authorities,

the assessee was found to be the owner of the said money. Section 69A (of Income Tax Act, 1961)

thereafter permits the assessee to offer an explanation about the nature

and source of acquisition of money and empowers the Assessing

Officer to deem the said money to be the income of the assessee, only if

finds the explanation offered to be unsatisfactory. It is not as if the

explanation of the appellant with respect to the sum of Rs.2 crores

found in his possession / custody, was, of the same being with him in

transit, for onward delivery as bribe to Dr. Ketan Desai. On the

contrary, the assessee offered the explanation of the same being

advance received by him towards consideration for sale of agricultural

land and which explanation was not found satisfactory, neither by the

Assessing Officer nor by the CIT nor by the ITAT. It is for this reason

that the same was deemed to be the income of the assessee.

18. Had the explanation offered by the assessee with respect to the

money found in his possession / custody been, of the same being with

him in transit for onward delivery to Dr. Ketan Desai, the assessee

could have argued that since the case of the CBI was the same, the

explanation offered by the assessee was satisfactory. On the contrary,

the assessee offered some other explanation and with which he failed to

satisfy the Assessing Officer. We have rather, during the hearing also

enquired from the senior counsel for the appellant / assessee, whether

the appellant / assessee is even now willing to change the explanation

offered by him and to bring it in consonance with the case of the CBI.

The answer of the senior counsel for the appellant / assessee, on

instructions, is expectedly in the negative.

19. In this context, we may also notice that Section 69A (of Income Tax Act, 1961) empowers

the Assessing Officer to only adjudicate whether the explanation

offered by the assessee is satisfactory or not. The Assessing Officer is

not empowered to return a finding, of the sum of Rs.2 crores found in

possession / custody of the appellant being with the appellant in transit,

for onward payment as bribe. The Assessing Officer as well as the

ITAT referred to the same, only in the context of the chargesheet of the

CBI and to observe that the explanation offered by the assessee was an

afterthought. The assessee thus cannot argue that there is any finding of

the said money being bribe money. The jurisdiction to return a finding

in that respect is only of the Criminal Court and not of the authorities

under the Income Tax Act.

20. As far back as in Chuharmal Vs. Commissioner of Income Tax

(1988) 3 SCC 588 the Supreme Court approved the approach of the

High Court; the High Court held the assessee to be the owner of the

wrist watches found in his premises during a search and seizure

operation and relied on Section 110 of the Evidence Act, 1872

stipulating that when the question is whether any person is owner of

anything of which he is shown to be in possession, the onus of proving

that he is not the owner, is on the person who affirms that he is not the

owner; it follows, that normally unless contrary is established, title

always follows possession and since possession of the wrist watches

was found to be of the assessee in that case and the assessee did not

discharge the onus of proving that the wrist watches did not belong to

him, the High Court held the value of the wrist watches to be the

income of the assessee.

21. Thus no substantial question of law qua interpretation of Section

69A also arises.

22. Dismissed.

×

Similar Ripples

Questions

Court upholds ₹2 crore tax addition on unexplained cash found during CBI raid

Write your CommentSimilar Posts

Generic

- Reportdata/6501_compressed.pdf