Court Upholds Application of Section 44AE (of Income Tax Act, 1961) for Transpo…

Full News

Court Upholds Application of Section 44AE (of Income Tax Act, 1961) for Transport Contractor with 10 or Fewer Trucks

Court Upholds Application of Section 44AE (of Income Tax Act, 1961) for Transport Contractor with 10 or Fewer…

This case involves the Commissioner of Income Tax (the Revenue) appealing against an order by the Income Tax Appellate Tribunal (ITAT) regarding the assessment of a transport contractor's income. The main dispute centered around the applicability of Section 44AE (of Income Tax Act, 1961) to the assessee's business. The High Court dismissed the Revenue's appeal, affirming the ITAT's decision that Section 44AE (of Income Tax Act, 1961) was correctly applied to the assessee's case.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Anil Kumar Arya (High Court of Punjab and Haryana)

ITA No.508 of 2007

Date: 4th April 2008

Key Takeaways:

1. Section 44AE (of Income Tax Act, 1961) applies to assessees owning 10 or fewer goods carriages.

2. Factual findings by the Tribunal are given significant weight by higher courts.

3. The burden of proof lies with the Revenue to controvert factual findings.

Issue:

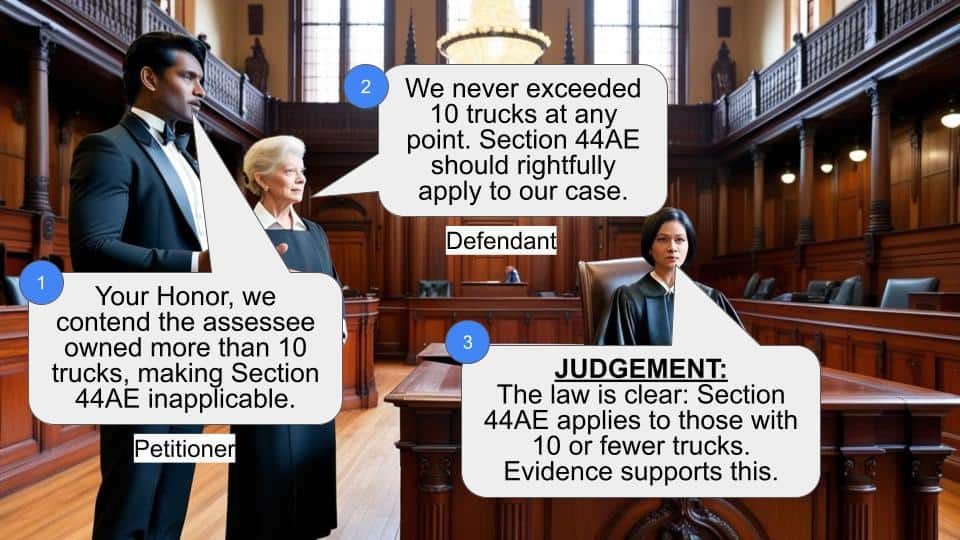

Was the Income Tax Appellate Tribunal correct in applying Section 44AE (of Income Tax Act, 1961) to the assessee's case, given that the assessee owned no more than 10 trucks at any point during the relevant assessment year?

Facts:

1. The assessee is a transport contractor supplying oil tankers on hire to various oil companies.

2. For the assessment year 2001-02, the assessee filed a return declaring a total income of Rs.1,96,590/-.

3. The case was selected for scrutiny, and the Assessing Officer concluded that Section 44AE (of Income Tax Act, 1961) was not applicable.

4. The Assessing Officer estimated the assessee's income by applying an 8% net profit on gross receipts.

5. The Commissioner of Income Tax (Appeals) partly allowed the assessee's appeal, holding that the assessee never owned more than 9 trucks during the accounting year.

6. The Revenue appealed to the Income Tax Appellate Tribunal, which upheld the CIT(A)'s order.

Arguments:

Revenue's Argument:

- The assessee failed to produce books of account or registration certificates to verify the number of trucks owned.

- Section 44AE (of Income Tax Act, 1961) should not apply as the assessee owned more than 10 trucks.

Assessee's Argument:

- The case falls under Section 44AE (of Income Tax Act, 1961), which applies to owners of 10 or fewer goods carriages.

- The total number of tankers owned never exceeded 10 at any point during the relevant year.

Key Legal Precedents:

The judgment doesn't cite specific case laws but heavily relies on the interpretation and application of Section 44AE (of Income Tax Act, 1961).

Judgement:

1. The High Court dismissed the Revenue's appeal.

2. The court affirmed that the Tribunal's finding was purely factual - the assessee did not own more than 10 trucks at any point during the assessment year.

3. The court held that Section 44AE (of Income Tax Act, 1961) was correctly applied to the assessee's case.

4. The Revenue failed to bring any material on record to controvert the Tribunal's factual finding.

5. No substantial question of law arose from the Tribunal's order.

FAQs:

Q1: What is Section 44AE (of Income Tax Act, 1961)?

A1: Section 44AE (of Income Tax Act, 1961) is a special provision for computing profits and gains from the business of plying, hiring, or leasing goods carriages. It applies to assessees who own 10 or fewer goods carriages and provides a simplified method of calculating income at a fixed rate per vehicle per month.

Q2: Why was the Revenue's appeal dismissed?

A2: The appeal was dismissed because the Tribunal had made a factual finding that the assessee owned 10 or fewer trucks, and the Revenue couldn't provide any evidence to contradict this finding. The High Court found no legal error in the Tribunal's decision.

Q3: What was the significance of the number of trucks owned by the assessee?

A3: The number of trucks was crucial because Section 44AE (of Income Tax Act, 1961) only applies to assessees owning 10 or fewer goods carriages. If the assessee had owned more than 10 trucks, a different method of income calculation would have been required.

Q4: What is the importance of factual findings by the Tribunal?

A4: Factual findings by the Tribunal carry significant weight in higher courts. Unless there's clear evidence to the contrary, higher courts typically don't interfere with these factual determinations.

Q5: What would have happened if the assessee owned more than 10 trucks?

A5: If the assessee owned more than 10 trucks, Section 44AE (of Income Tax Act, 1961) wouldn't apply. The assessee would likely have been required to maintain regular books of accounts and possibly have them audited under Sections 44AA (of Income Tax Act, 1961) and 44AB (of Income Tax Act, 1961).

1. The Revenue has filed the present Appeal under Section 260A (of Income Tax Act, 1961)(for short ‘the Act’) against the order dated 31.1.2007 passed by the Income Tax Appellate Tribunal, Delhi Bench(I), Delhi (for short ‘the Tribunal’), in ITA No.122/DEL/2005 for the assessment year 2001-02 raising the following proposed substantial questions of law: -

“1)Whether on the facts and in the circumstances of the case , the Hon'ble ITAT has erred in law and on facts in upholding the order of CIT(A) in deleting the addition of Rs.37,09,580/- computed on the basis of applying 8 % profit from contract receipts of 28 trucks because the case of the assessee falls outside the ambit of section 44AE (of Income Tax Act, 1961) as the amendments at any time during the previous year in section 44AE (of Income Tax Act, 1961) is effective from 1.4.2004. The assessee case is related to A.Y. 2001-02, hence clause at any time during the year in section 44AE (of Income Tax Act, 1961) is not applicable in the case of the assessee in the relevant assessment year i.e., A.Y.2001-02 ?

2) Whether on the facts and in the circumstances of the case , the Hon'ble ITAT has erred in law in upholding the order of learned CIT(A) deleting the addition of Rs.6,62,425/- on account of income of 5 trucks on the same basis which were owned by the assessee but not used in the tender of M/s Satpriya & Sons during the year under consideration ?

3)Whether on the facts and in the circumstances of the case , the Tribunal has erred in law in not adjudicating the ground of appeal of the revenue in respect of addition deleted by the CIT(A) at Rs.4,00,000/- on account of repair and renovation of flat and Rs.13,95,000/- on account of unexplained investment in shares?

4)Whether on the facts and in the circumstances of the case , the Tribunal has erred in law ignoring the facts that the TDS of the receipts on form No.16A from these 28 trucks were claimed by the assessee in his return of income and the refund was claimed by him and has been received by the assessee on all these 28 trucks ?

5)Whether on the facts and in the circumstances of the case , the Tribunal has erred in law in not taking into account the provision of section 199 (of Income Tax Act, 1961) which stipulate that any deduction made in accordance with section 194 (of Income Tax Act, 1961) C of the Act and paid to the Central Govt. shall be treated as a payment of tax on behalf of the person from whose income the deduction was made and credit shall be given to him on production of certificate u/s 203 (of Income Tax Act, 1961) on the assessment made under this Act for the A.Y. for such income is assessable provided that where the income is assessable to any other person the credit shall be given to such other persons in such circumstances as may be prescribed.?”

The assessee is a transport contractor and is engaged in the business of supplying oil tankers on hire to various oil companies. The return of income in this case was filed by the assessee on 25.9.2001 declaring total income of Rs.1,96,590/-. The said return was processed under Section 143(1)(a) (of Income Tax Act, 1961). Later on the case was selected for scrutiny. The assessee was issued notice under Section 143(2) (of Income Tax Act, 1961).

Reply was filed by the assessee. No books of account are stated to have been maintained by him on the plea that his case is covered under the provisions of Section 44 (of Income Tax Act, 1961) AE of the Act. The Assessing Officer reached the conclusion that provisions of Section 44 (of Income Tax Act, 1961) AE are not applicable in the case of the assessee and the assessee was required to maintain regular books of account and get these audited as per Section 44 (of Income Tax Act, 1961) AA and 44 AB of the Act. The Assessing Officer estimated the total income of the assessee on the basis of gross receipts earned by him by applying a net profit of 8 % and made additions vide his order dated 27.2.2004.

Aggrieved against this order, the assessee filed an appeal before the Commissioner of Income Tax(Appeals), Rohtak (for short 'the CIT(A)'). The CIT (A), Rohtak vide his order dated 28.10.2004 partly allowed the appeal and held that at no point of time, the assessee owned more than 9 trucks during the accounting year of appeal and directed the assessment of the income from business of trucks to be made at Rs.1,96,000/- as returned plus Rs.24000/-.

Not satisfied with the order of the CIT(A), Rohtak, the revenue filed the present appeal challenging the said order before the Tribunal. The main argument of the revenue before the Tribunal was that the assessee had failed to produce the books of account or the registration certificates of various tankers/trucks to verify as to whether or not the assessee was owning more than 10 trucks so as to verify the applicability of Section 44 (of Income Tax Act, 1961) AE of the Act. The Tribunal found that the dispute is essentially factual in nature and as per the computation of income filed by the assessee, the total number of tankers owned by the assessee does not exceed 10 at any time during the previous year relevant to the assessment year under consideration and there is no material brought on record by the Revenue to controvert the said finding and therefore, the provisions of Section 44 (of Income Tax Act, 1961) AE have been rightly held to be applicable to the assessee.

We have heard Mr.Yogesh Putney, Advocate learned counsel for the Revenue and perused the record. The Tribunal has given a pure finding of fact to the effect that total number of trucks owned by the assessee does not exceed 10 at any point of time during the assessment year under consideration and there is no material brought on record by the Revenue to controvert the said factual finding. Section 44 (of Income Tax Act, 1961) AE is a special provision for computing the profits and gains from the business of plying, hiring for lease of goods carriages. It provides that income from plying, hiring, leasing goods carriages shall be computed at Rs.2,000/- per month for every vehicle owned by an assessee. The provisions of Section 44 (of Income Tax Act, 1961) AE of the Act are applicable to only those assessees who do not own more than ten goods carriage.

Since the Tribunal has found as a fact that the total number of tankers owned by the assessee does not exceed 10 at any point of time during the relevant period. The provisions of Section 44 (of Income Tax Act, 1961) AE of the Act are applicable in the case of the assessee and therefore, the provisions of Section 44 (of Income Tax Act, 1961) AE have been rightly applicable to the case of the assessee. No other point has been argued by the learned counsel for the Revenue.

In view of the finding of fact, we find no infirmity in the order of the Tribunal. No substantial questions of law arises from the order of the Tribunal. Thus, the appeal filed by the Revenue being devoid of any merit is hereby dismissed.

(RAKESH KUMAR GARG)

JUDGE

April 4,2008 (SATISH KUMAR MITTAL)

JUDGE

×

Questions

Court Upholds Application of Section 44AE (of Income Tax Act, 1961) for Transport Contractor with 10 or Fewer Trucks

Write your CommentSimilar Posts

Generic

- Reportdata/4690.pdf