Court Upholds Assessee's Property Valuation, Dismisses Revenue's Appeal

Full News

Court Upholds Assessee's Property Valuation, Dismisses Revenue's Appeal

Court Upholds Assessee's Property Valuation, Dismisses Revenue's Appeal

This case involves a dispute between the Income Tax Department (Revenue) and an assessee regarding the valuation of a property. The Income Tax Appellate Tribunal ruled in favor of the assessee, accepting their stated property value. The High Court dismissed the Revenue's appeal, finding no substantial question of law.

Get the full picture - access the original judgement of the court order here

Case Name

Commissioner of Income Tax Vs Rajiv Mehta (High Court of Delhi)

ITA 1456/2006

Date: 9th October 2007

Key Takeaways

1. Registered documents are considered reliable evidence of property value unless rebutted by contrary evidence.

2. Tribunal's findings based on evidence appreciation are generally not interfered with by higher courts.

3. Marital discord and unreliable testimonies can impact the credibility of evidence in tax disputes.

Issue

Was the Income Tax Appellate Tribunal justified in accepting the assessee's valuation of the property and deleting the addition made by the Assessing Officer?

Facts

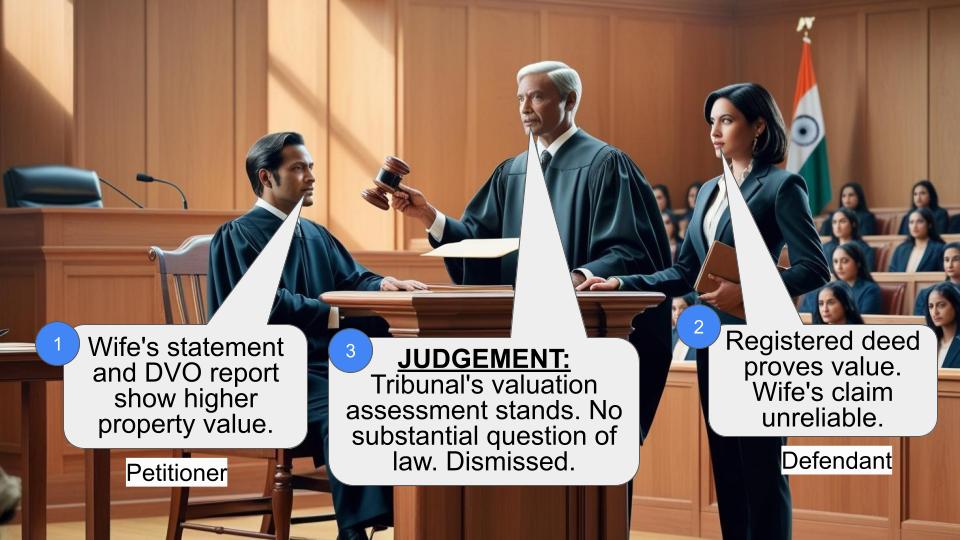

1. The assessee purchased a property (ground floor at E-16/12, Kalkaji, New Delhi) for Rs. 20 lakhs, as per a registered deed.

2. The assessee's wife stated that the property was actually purchased for Rs. 70 lakhs.

3. The Departmental Valuation Officer (DVO) valued the property at Rs. 31.44 lakhs.

4. The Assessing Officer (AO) preferred the wife's statement and valued the property at Rs. 70 lakhs.

5. On appeal, the Commissioner of Income Tax (Appeals) reduced the value to Rs. 25.15 lakhs.

6. The Income Tax Appellate Tribunal accepted the assessee's version and deleted the addition.

Arguments

Assessee's Arguments:

1. The property was purchased for Rs.20 lakhs, as evidenced by the registered document.

2. The wife's statement was unreliable due to marital discord and ongoing criminal proceedings.

3. The property dealer denied brokering the deal and stated that the Rs. 70 lakhs figure in his books didn't pertain to this property.

Revenue's Arguments:

1. The wife's statement indicating a higher purchase price of Rs. 70 lakhs should be considered.

2. The property dealer's books showed a higher transaction value.

3. The Departmental Valuation Officer's report supported a higher valuation.

Key Legal Precedents

The judgment doesn't explicitly cite any specific legal precedents. However, it mentions a well-settled principle:

"It is well-settled that a registered document indicates the value of the property, unless it is rebutted by reliable evidence to the contrary."

Judgement

1. The High Cpurt dismissed the Revenue's appeal.

2. The court found no infirmity in the Tribunal's view and stated that the case involved appreciation of evidence on record.

3. The court held that no substantial question of law arose from the case.

FAQs

Q1: Why did the court favor the assessee's valuation over the wife's statement?

A1: The court noted that there was marital discord between the assessee and his wife, including criminal proceedings. This cast doubt on the reliability of the wife's statement.

Q2: What was the significance of the property dealer's testimony?

A2: The property dealer's denial of brokering the deal and clarification that the Rs. 70 lakhs figure in his books didn't relate to this property weakened the Revenue's case.

Q3: Why wasn't the Departmental Valuation Officer's report given more weight?

A3: The Tribunal noted that the Valuation Officer hadn't called for comments from the assessee or allowed an opportunity to file objections, which affected the report's credibility.

Q4: What principle did the court emphasize regarding registered documents?

A4: The court reiterated that a registered document is considered indicative of a property's value unless rebutted by reliable contrary evidence.

Q5: Why didn't the High Court intervene in the Tribunal's decision?

A5: The High Court found that the case involved appreciation of evidence, which is typically the domain of the Tribunal. As no substantial question of law arose, the court didn't see grounds for intervention.

1. The Revenue is aggrieved by an order dt. 17th Feb., 2006 passed by the Income-tax Appellate Tribunal (‘Tribunal’), Delhi Bench ‘E’, in IT(SS)A No. 141/Del/2002 relevant for the block period 1st April, 1989 to 27th July, 1999 and IT(SS)A No. 155/Del/2002. The present appeal has been preferred in respect of ITA(SS)A No. 141/Del/2002.

2. The only question that has come up for consideration is with regard to the value of the property being the ground floor at E-16/12, Kalkaji, New Delhi.

3. According to the assessee he has purchased the property for a sum of Rs.20 laks under a registered document. However, the AO relied upon the statement given by the wife of the assessee to the effect that the property was actually purchased for Rs. 70 lakhs.

4. The matter was referred to the Valuation Cell of the IT Department. By his report dt. 13th Aug., 2001, the Valuation Officer valued the property at Rs. 31.44 lakhs. However, the AO did not go by the report of the Valuation Officer and chose to accept the value as stated by the wife of the assessee.

5. The CIT(A), while partly allowing the assessee’s appeal, reduced the value of the property to Rs. 25.15 lakhs.

6. In the further appeal by the assessee, the Tribunal set aside the findings of the authorities below and accepted the case put forth by the assessee. The Tribunal noted that there was marital discord between the assessee and his wife and that criminal proceedings had also been launched. In the circumstances, the Tribunal opined that the value of the property as indicated by the assessee’s wife was not reliable.

7. As regards the other piece of corroborative evidence, the AO had proceeded on the basis that the property dealer who brokered the deal had indicated in his books that the property had been sold for Rs. 70 lakhs. However, the Tribunal noted that on cross-examination the property dealer had denied that the property had been brokered by him. He further stated that the figure noted in his books did not pertain to the property in question.

8. As regards the valuation of the property by the Valuation Cell, the Tribunal noticed that the Valuation Officer had admitted that he had not called for any comments from the assessee nor allowed an opportunity to the assessee to file an objection. It also found that the Revenue had not produced any evidence to show why the value of the property, as indicated in the registered document should not be relied upon.

9. It is well-settled that a registered document indicates the value of the property, unless it is rebutted by reliable evidence to the contrary.

10. We do not find any infirmity in the view taken by the Tribunal. We find that this case involves the appreciation of evidence on record and does not raise any substantial question of law.

11. The appeal is dismissed.

MADAN B. LOKUR, J

OCTOBER 09, 2007 S. MURALIDHAR, J

×

Similar Ripples

Questions

Court Upholds Assessee's Property Valuation, Dismisses Revenue's Appeal

Write your CommentSimilar Posts

Generic

- Reportdata/5285.pdf