Court Upholds Bona Fide Belief in TDS Exemption, Dismisses Revenue's Appeal

Full News

Court Upholds Bona Fide Belief in TDS Exemption, Dismisses Revenue's Appeal

Court Upholds Bona Fide Belief in TDS Exemption, Dismisses Revenue's Appeal

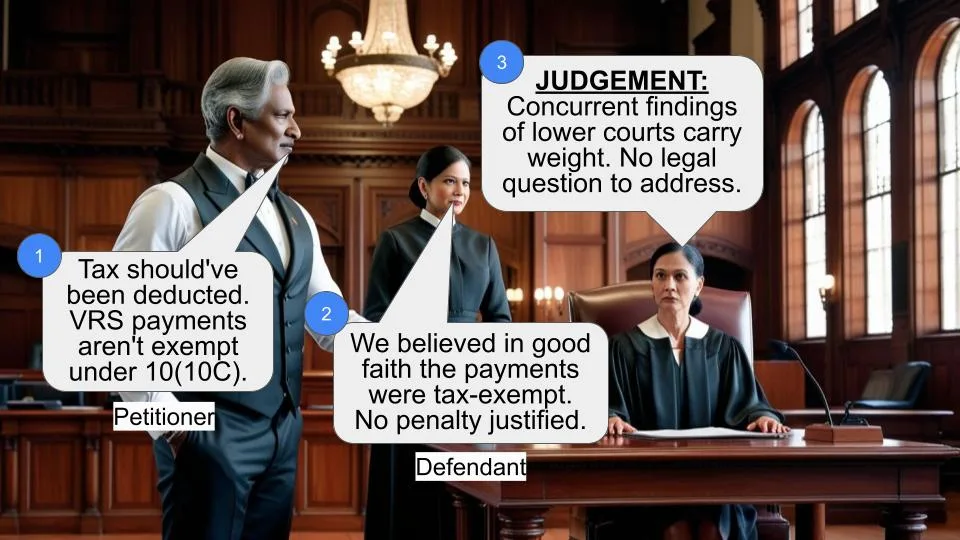

This case involves the Commissioner of Income Tax (appellant) challenging a decision made by the Income Tax Appellate Tribunal (ITAT) regarding Indokem Ltd. (assessee). The ITAT had upheld the CIT(Appeals) order, which found that Indokem Ltd. had a bona fide belief that payments made under a Voluntary Retirement Scheme were tax-exempt, justifying their failure to deduct tax at source. The High Court dismissed the appeal, agreeing with the concurrent findings of the lower authorities.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Indokem Ltd (High Court of Bombay)

Income Tax Appeal No.32 of 2001

Date: 15th January 2008

Key Takeaways:

1. Concurrent findings of fact by lower authorities carry significant weight in higher courts.

2. Bona fide belief can be a valid defense against penalties for non-deduction of tax at source.

3. The High Court's reluctance to interfere with factual findings emphasizes the importance of strong fact-building in lower tribunals.

Issue:

Was the Tribunal justified in confirming the CIT(A)'s order that the amount paid under the Voluntary Retirement Scheme was exempt under section 10(10C) (of Income Tax Act, 1961), and consequently, action under section 201(1) (of Income Tax Act, 1961) was not justified?

Facts:

1. Indokem Ltd. paid amounts to employees under a Voluntary Retirement Scheme.

2. The company did not deduct tax at source from these payments.

3. The Income Tax Department sought to take action under section 201(1) (of Income Tax Act, 1961).

4. Both the CIT(Appeals) and the ITAT found that Indokem Ltd. had a bona fide belief that the payments were tax-exempt.

5. The Revenue department appealed this decision to the High Court.

Arguments:

Revenue's Argument:

- The Tribunal erred in confirming the CIT(A)'s order.

- The amount paid under the Voluntary Retirement Scheme should not have been considered exempt under section 10(10C) (of Income Tax Act, 1961).

- Action under section 201(1) (of Income Tax Act, 1961) was justified due to non-deduction of tax at source.

Assessee's Argument:

- They had a bona fide belief that the amounts paid were exempt from tax in the hands of the employees.

- The default in deducting tax at source was for good and sufficient reasons.

- Action under section 201(1) (of Income Tax Act, 1961) was not justified due to their good faith belief.

Key Legal Precedents:

The judgment doesn't explicitly mention any specific legal precedents. However, it relies on the principle that concurrent findings of fact by lower authorities should not be disturbed unless a substantial question of law arises.

Judgement:

The High Court dismissed the appeal, stating:

1. The Tribunal and CIT(A) had recorded concurrent findings of fact regarding the assessee's bona fide belief.

2. These findings established that the default in deducting tax was for good and sufficient reasons.

3. Given these concurrent findings, no substantial question of law arises.

4. The court declined to interfere with the factual findings of the lower authorities.

FAQs:

Q1: What is a "substantial question of law"?

A1: It's a significant legal issue that needs to be addressed by a higher court, typically involving interpretation of statutes or legal principles, rather than mere appreciation of evidence.

Q2: What does "concurrent findings of fact" mean?

A2: It refers to similar factual conclusions reached by two or more lower courts or tribunals. Higher courts generally hesitate to interfere with such findings unless there's a clear error.

Q3: What is section 201(1) (of Income Tax Act, 1961)?

A3: This section deals with the consequences of failing to deduct tax at source or not paying the tax after deduction. It allows the tax authorities to treat the person responsible for deducting tax as an "assessee in default".

Q4: What is a Voluntary Retirement Scheme (VRS)?

A4: It's a scheme offered by companies to provide certain benefits to employees who opt to retire voluntarily before their normal retirement age.

Q5: Does this judgment set a precedent for all cases of non-deduction of tax at source?

A5: Not necessarily. The court's decision was based on the specific facts of this case, particularly the finding of bona fide belief. Each case would be judged on its own merits.

The appeal has been preferred on the following questions :

"Whether on the facts and circumstances of the case the Tribunal was justified in law in confirming the order of C.I.T. (A) by holding that the amount paid to the employees under the voluntary retirement Scheme was covered u.s. 10(19B) and hence, action u.s. S. 201(1) of the I.T. Act was not justified?"

The appellant before the tribunal was Revenue. The learned tribunal has considering the facts on record concurred with the findings on record by Commissioner (Appeals), that it was under the bona fide belief and consequently the default was for good and sufficient reasons. In our opinion considering that two concurrent findings of fact, the question of law as framed would not arise. Consequently appeal dismissed.

(R.S. MOHITE, J.) (F.I.REBELLO, J.)

×

Similar Ripples

Questions

Court Upholds Bona Fide Belief in TDS Exemption, Dismisses Revenue's Appeal

Write your CommentSimilar Posts

Generic

- Reportdata/5011.pdf