Court Upholds Capital Gains Exemption in Share Transfer Case, Citing Precedent

Full News

Court Upholds Capital Gains Exemption in Share Transfer Case, Citing Precedent

Court Upholds Capital Gains Exemption in Share Transfer Case, Citing Precedent

This case involves the Commissioner of Income Tax (CIT) challenging a decision made by the Income Tax Appellate Tribunal (ITAT) in favor of Shahibaug Enterprises (P) Ltd. The dispute centered around whether the transfer of shares to a subsidiary company should be exempt from capital gains tax under section 47(iv) (of Income Tax Act, 1961). The High Court ultimately ruled in favor of the assessee (Shahibaug Enterprises), upholding the ITAT's decision.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Shahibaug Enterprises (P) Ltd. (High Court of Gujarat)

Income Tax Reference No.257 of 1995

Date: 22nd January 2008

Key Takeaways:

1. The court emphasized the importance of consistency in tax rulings, especially when similar cases have been decided.

2. The decision reinforces the application of section 47(iv) (of Income Tax Act, 1961) for exempting capital gains in transfers to wholly-owned subsidiaries.

3. The court highlighted the significance of previous judgments in similar cases, even if they involve different assessees.

Issue:

Was the Income Tax Appellate Tribunal correct in law and on facts in deleting the addition of Rs.1,85,93,546 and holding that the amount represented capital gains exempt under section 47(iv) (of Income Tax Act, 1961)?

Facts:

1. The case pertains to the assessment year 1979-80.

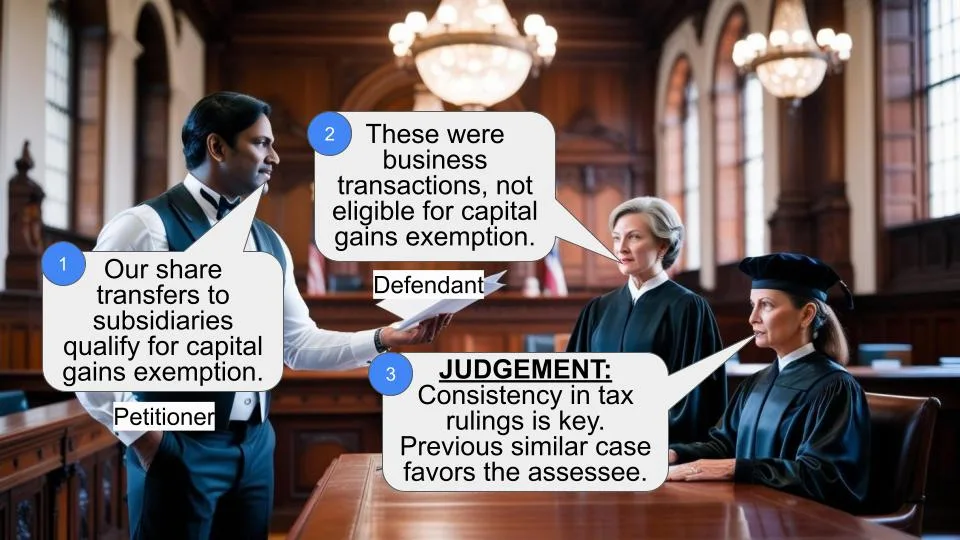

2. Shahibaug Enterprises (P) Ltd. sold shares of Suhrid Geigy Ltd. (acquired on 1.1.1974) to its wholly-owned subsidiary, Koshalya P. Ltd.

3. The assessee also sold shares of Wadi Chemicals P. Ltd. (acquired on 1.8.1977) to another wholly-owned subsidiary.

4. The assessee claimed the capital gains from these transactions were exempt under section 47(iv) (of Income Tax Act, 1961).

5. The Assessing Officer rejected this claim, arguing that the assessee was in the business of buying and selling shares.

Arguments:

Assessee's arguments:

1. The transactions resulted in capital gains, not business income.

2. The gains should be exempt under section 47(iv) (of Income Tax Act, 1961).

3. In previous years, similar transactions were treated as capital gains/losses, not business income/loss.

4. The shares were listed as investments in the company's balance sheet.

Revenue's arguments:

1. The assessee was in the business of buying and selling shares, so the gains should be treated as business income.

2. The exemption under section 47(iv) (of Income Tax Act, 1961) should not apply.

Key Legal Precedents:

1. Sercon P. Ltd. case (ITA No. 393/Ahd/1984):

The ITAT relied on this case, which had similar facts and was decided in favor of the assessee.

2. Union of India & Ors. vs. Kaumudini Narayan Dalal & Anr. (2001) 249 ITR 219:

The Supreme Court held that "it is not open to the Revenue to accept the judgment in case of one assessee and challenge its correctness in the case of other assessee without just cause."

Judgement:

The High Court ruled in favor of the assessee, Shahibaug Enterprises (P) Ltd. The court's reasoning was:

1. A similar issue had been concluded in favor of another assessee (Sercon P. Ltd.) in a previous case.

2. The Revenue had not challenged the earlier decision or pointed out any distinguishing features in the current case.

3. Following the principle laid down in the Kaumudini Narayan Dalal case, the court found no just cause to treat this case differently.

The court answered the referred question in the affirmative, upholding the ITAT's decision to exempt the capital gains under section 47(iv) (of Income Tax Act, 1961).

FAQs:

Q1: What is section 47(iv) (of Income Tax Act, 1961)?

A1: Section 47(iv) (of Income Tax Act, 1961) provides for exemption of capital gains in cases where assets are transferred from a holding company to its wholly-owned subsidiary.

Q2: Why did the court rely on the Sercon P. Ltd. case?

A2: The Sercon P. Ltd. case had similar facts and had been decided in favor of the assessee. The court emphasized the importance of consistency in tax rulings.

Q3: What is the significance of the Kaumudini Narayan Dalal case in this judgment?

A3: This Supreme Court case established that the Revenue cannot accept a judgment for one assessee and challenge it for another without just cause, which was a key principle applied in this case.

Q4: Does this judgment set a precedent for future cases?

A4: While it reinforces the application of section 47(iv) (of Income Tax Act, 1961) and the importance of consistency in rulings, each case would still be judged on its specific facts and circumstances.

Q5: What was the main point of contention between the assessee and the Revenue?

A5: The main dispute was whether the share transfers should be treated as capital gains (exempt under section 47(iv) (of Income Tax Act, 1961)) or as business income (taxable).

1. The Income Tax Appellate Tribunal, Ahmedabad Bench-C, has referred the following question at the instance of Revenue under section 256(2) (of Income Tax Act, 1961) (for short 'the Act'):

“Whether the Appellate Tribunal is right in law and on facts in deleting the addition of Rs.1,85,93,546/- holding that the amount in question represented capital gains and the said capital gains was exempt under section 47(iv) (of Income Tax Act, 1961)?”

2. The assessment year is 1979-80 and the relevant accounting period is financial year ended 31.3.1979. The assessee company sold certain shares of Suhrid Geigy Ltd., which had been acquired on 1.1.1974 to Koshalya P. Ltd. Which was a wholly owned subsidiary company of the assessee. Similarly, the assessee had also sold certain shares of Wadi Chemicals P. Ltd. Which had been acquired on 1.8.1977 to another wholly owned subsidiary company. The assessee worked out capital gains and claimed the said capital gains to be wholly exempt from tax under section 47(iv) (of Income Tax Act, 1961). The claim of the assessee was negatived by the Assessing Officer on the ground that the assessee had been carrying on the business of purchasing and selling shares. The assessee carried the matter in appeal before the Commissioner of Income Tax (Appeals) who dismissed the appeal on this count.

3. In the second appeal, the Tribunal accepted the stand of the assessee on the basis: (i) in assessment order for Assessment Year 1978-79 the Assessing Officer had taxed the profit on sale of investment as capital gains and not as business profit; (ii) the Assessing Officer rejected the claim of the assessee regarding investment being stock in trade; (iii) in earlier assessment year the profit or loss were treated as capital gains or capital loss and had never been treated as business income or business loss; (iv) the shares in question were reflected under the head of Investments in the balance sheet of the company.

4. The Tribunal also relied upon its own order in the case of one Sercon P. ltd. In ITA No. 393/Ahd/1984 for assessment year 1978-79 decided on 4.1.1988 involving identical facts. The Tribunal also relied upon assessee's own case where similar view had been taken.

5. Heard the learned Senior Standing Counsel for the applicant – Revenue as well as Shri R.K. Patel learned advocate for the assessee. It is an accepted fact between the parties that in case of Sercon P. Ltd., the order of Tribunal was carried before this Court by way of Income Tax Application No. 253/1988 under section 256(2) (of Income Tax Act, 1961) and vide order dated 16.4.1980 the application was rejected refusing to direct the Tribunal to raise and refer any question of law, either as proposed or otherwise. In the fact situation when on similar facts the issue stands concluded in favour of one assessee and there is nothing on record to suggest that the aforesaid order dated 16.4.1990 in case of Sercon P. Ltd. has been challenged further, the order made by the Apex Court in the case of Union of India & Ors. vs. Kaumudini Narayan Dalal & Anr., reported in (2001) 249 ITR 219, wherein, it is held that “it is not open to the Revenue to accept the judgment in case of one assessee and challenge its correctness in the case of other assessee without just cause” applies with full force. No distinguishing feature has been pointed out and hence in absence of any just cause the question referred to the Court requires to be answered in the affirmative upholding the view taken by the Tribunal considering the fact that in case of Sercon P. Ltd. similar issue stands concluded against the revenue. The question is, therefore, answered in the affirmative, that is, in favour of assessee and against the revenue.

6. The Reference stands disposed of accordingly. There shall be no order as to costs.

(D.A. MEHTA, J.)

(Z.K. SAIYED, J.)

×

Similar Ripples

Questions

Court Upholds Capital Gains Exemption in Share Transfer Case, Citing Precedent

Write your CommentSimilar Posts

Generic

- Reportdata/4976.pdf