Court Upholds Charitable Trust's Right to Registration Despite Delayed Property…

Full News

Court Upholds Charitable Trust's Right to Registration Despite Delayed Property Possession

Court Upholds Charitable Trust's Right to Registration Despite Delayed Property Possession

This case involves the Commissioner of Income Tax (the Revenue) appealing against an order of the Income Tax Appellate Tribunal. The Tribunal had directed the Original Authority to grant registration under Section 12AA (of Income Tax Act, 1961) to a charitable trust (the respondent). The Revenue challenged this decision, but the High Court dismissed their appeal, affirming the Tribunal's order.

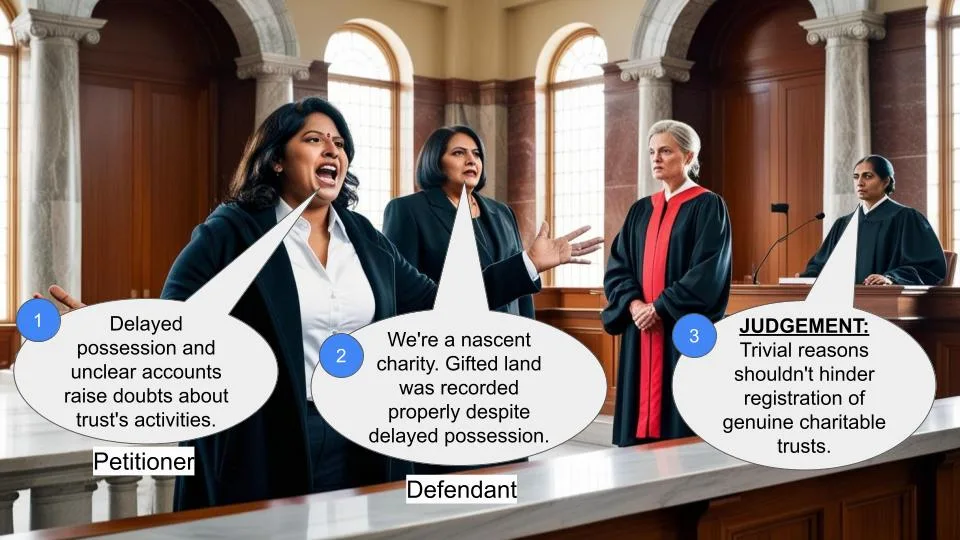

Case Name**: COMMISSIONER OF INCOME TAX VS HARE KRISHNA MOVEMENT **Key Takeaways**: 1. Trivial reasons should not prevent registration of genuine charitable trusts under Section 12AA (of Income Tax Act, 1961). 2. Delay in taking physical possession of a gifted property doesn't necessarily indicate lack of genuineness in a trust's activities. 3. Tax authorities should focus on the nature of a trust's activities rather than minor technical issues when considering registration. **Issue**: Was the Income Tax Appellate Tribunal correct in holding that the assessee (the trust) is entitled to registration under Section 12AA (of Income Tax Act, 1961)? **Facts**: 1. The respondent trust was formed by a trust deed executed on 18.01.2010. 2. The trust filed an application for registration under Section 12AA (of Income Tax Act, 1961) on 11.03.2013. 3. The trust received land as a gift, which was registered in its favor on 04.02.2010. 4. The gifted property was recorded in the trust's books of accounts for the year ending 31.3.2010. 5. Physical possession of the property was handed over to the trust on 26.5.2011. 6. The Original Authority rejected the application for registration, citing concerns about the delay in taking possession and lack of evidence of charitable activities. 7. The Income Tax Appellate Tribunal overturned this decision and directed the Original Authority to grant registration. **Arguments**: Revenue's Arguments: 1. The trust showed lack of diligence in taking over the gifted property. 2. Discrepancy between recording the asset in books (31.3.2010) and taking possession (26.5.2011) indicated unclear accounts and activities. 3. Lack of material evidence showing charitable activities. Trust's Arguments: 1. The property was duly registered and recorded in the books of accounts. 2. The delay in taking physical possession was not the trust's fault. 3. The trust was in its nascent stage and had the avowed object of conducting religious and charitable activities. **Key Legal Precedents**: The judgment doesn't explicitly cite any legal precedents. However, it refers to Section 12AA (of Income Tax Act, 1961), which governs the registration of charitable trusts. **Judgement**: 1. The High Court dismissed the Revenue's appeal, upholding the Tribunal's order. 2. The court found the Original Authority's reasons for declining registration to be trivial and not serving the cause of a charitable trust. 3. The court emphasized that a donee (the trust) cannot insist on how or when a donor delivers possession of a gifted property. 4. The delay in taking physical possession was not considered a fault of the trust. 5. The court deemed the Original Authority's inference about errors in maintaining accounts to be hyper-technical. 6. The court noted that Section 12AA (of Income Tax Act, 1961) provides for appropriate action if a trust's activities are not in consonance with the law, but that stage had not yet come. **FAQs**: 1. Q: Why did the court rule in favor of the trust? A: The court found the reasons for denying registration to be trivial and not reflective of the trust's genuine charitable nature. 2. Q: Does this case set a precedent for other charitable trusts? A: While not explicitly stated, this case suggests that tax authorities should focus on the substantive activities of a trust rather than minor technical issues when considering registration. 3. Q: What is the significance of Section 12AA (of Income Tax Act, 1961)? A: Section 12AA (of Income Tax Act, 1961) governs the registration of charitable trusts and provides for monitoring their activities to ensure compliance with the law. 4. Q: Can the tax department still monitor the trust's activities after registration? A: Yes, the court noted that Section 12AA (of Income Tax Act, 1961) allows for appropriate action if a trust's activities are found to be inconsistent with the law in the future. 5. Q: What lesson can other charitable trusts learn from this case? A: Trusts should ensure proper documentation of gifts and maintain clear accounts, but minor delays or technical issues shouldn't prevent registration if the trust's charitable intent is genuine.

This Tax Case (Appeal) is filed by the Revenue as against the order of the Income Tax Appellate Tribunal raising the following substantial question of law:

"Whether on the facts and in the circumstances of the case, the Tribunal was right in holding that the assessee is entitled for registration under Section 12AA (of Income Tax Act, 1961)?"

2. The respondent - trust, which was formed by a trust deed executed on 18.01.2010, filed an application under Section 10A (of Income Tax Act, 1961) for registration under Section 12AA (of Income Tax Act, 1961) on 11.03.2013. The application for registration was processed on the basis of the materials enclosed. On intimation by the Department by letter dated 01.04.2013, the applicant - trust filed a letter dated 25.6.2013 furnishing certain details. One of the details contained in the response is that the trust received a land as gift from donors, the property donated was registered in favour of the trust on 04.02.2010 and that is recorded in the books of accounts for the year ending 31.3.2010. It appears that the property has been actually handed over to the trust on 26.5.2011. On the subsequent hearing dates, the applicant - trust filed another letter dated 22.9.2013 filed on 25.9.2013 enclosing certain details of the property gifted to the trust along with the relevant particulars including income and expenditure statement,balance sheet etc.

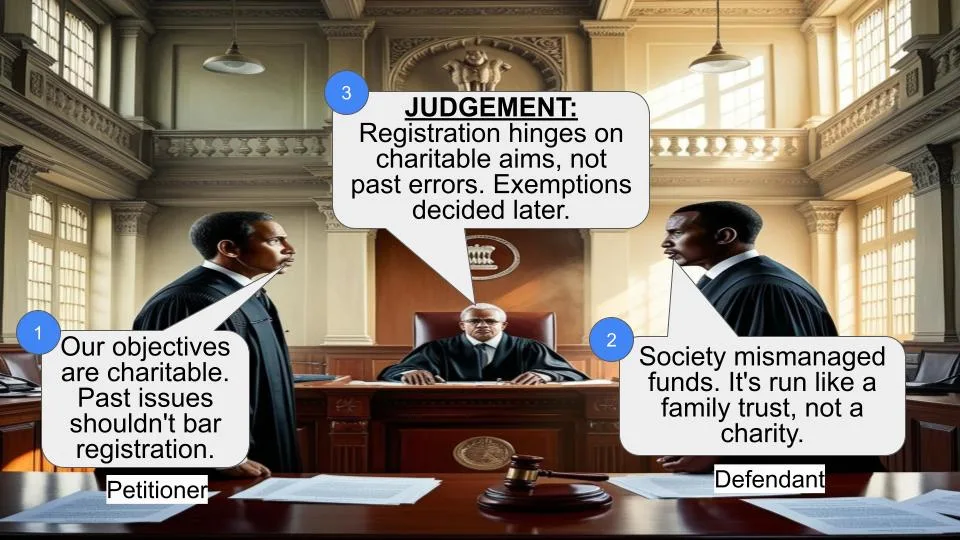

3. The Original Authority was of the view that though the gift deed was registered on 04.02.2010, the property was handed over to the corpus of the trust only on 26.5.2011 and the trust has not shown any diligence in taking over the property. Having brought the asset in the books of accounts of the trust for the year ending 31.3.2010 itself and taking over of the asset subsequently on 26.5.2011 would show that the accounts and the activities of the trust were not at all clear. The further ground is that the trust had not shown any material evidence to show that they are carrying on charitable activity. On this premise and on the basis of the report of the Inspector, who stated that except conducting pooja to the Presiding deity and distributing Prasadam to the devotees,no charitable activity has been effectively taken. Hence, the application was rejected. As against the said order of rejection, the assessee filed an appeal before the Income Tax Appellate Tribunal, which allowed the appeal directing the Original Authority to grant registration. Aggrieved by the same, the Revenue has filed the present Tax Case (Appeal).

4. Heard Mr.J.Narayanasamy, learned standing counsel appearing for the Revenue and perused the materials placed before this Court.

5. We find that the reasons given by the Original Authority to decline registration is trivial and does not sub-serve the cause of a charitable trust, which seeks registration under Section 12AA (of Income Tax Act, 1961). There is no doubt that the Trust got registered the property, which was gifted to it, on 04.02.2010 itself. On execution of the registered deed, they had primarily recorded in their books of accounts as on 31.3.2010. Hence, no fault could be attributed to the trust, when the donor does not physically handed over the possession of the property. A donee cannot insist the donor as to how his donation should be made. The Trust is started with an avowed object of conducting religious as well as charitable activities. It is in the nascent stage as we could see from the date of formation and seeking registration under Section 12AA (of Income Tax Act, 1961). Therefore, the Department was not correct in coming to the conclusion that the genuineness of the trust is in doubt. Primarily the reason as we could see from the order of the original authority is not on account of the nature of the activity of the trust, but on a ground that the property donated was registered on 04.2.2010, but taken over physical possession only on 26.5.2011. We find that such a reasoning is totally misconceived. As we have already observed, the donee cannot make conditions or call upon the donor that he should deliver possession immediately. What has been given as gift by a registered document has been entered into the books of accounts promptly. The delay in handing over possession cannot be attributed to the fault of the trust and as a consequence the interference drawn by the Original Authority that there is an error in maintaining the accounts appears to be hyper-technical. The Tribunal was correct in rectifying the error and allowing the appeal. It is not as if that the Original Authority did not have power to check the activities of the trust, as Section 12AA (of Income Tax Act, 1961) provides for appropriate action to be taken, if the objects of the trust and its activities are not in consonance with the provisions of law. That stage has not yet come and therefore, the Department is at error in declining to grant registration.

6. In the light of the above, we see no error in the order of the Tribunal. We find no question of law much less any substantial question of law arises for consideration in this appeal. Accordingly, the order of the Tribunal stands confirmed and this Tax Case (Appeal) stands dismissed. No costs.

Index :Yes/No (R.S.,J) (R.K.,J)

Internet:Yes/No 05.11.2014

To

1. The Income Tax Appellate Tribunal 'B' Bench, Chennai.

2. The Commissioner of Income Tax, Salem.

R.SUDHAKAR,J.

AND

R.KARUPPIAH,J.

×

Similar Ripples

Questions

Court Upholds Charitable Trust's Right to Registration Despite Delayed Property Possession

Write your CommentSimilar Posts

Generic

- Reportdata/4429.pdf