Court Upholds Deletion of Tax Addition, Citing Lack of Evidence on Higher Land …

Full News

Court Upholds Deletion of Tax Addition, Citing Lack of Evidence on Higher Land Sale Price

Court Upholds Deletion of Tax Addition, Citing Lack of Evidence on Higher Land Sale Price

This case involves appeals by the Revenue Department against the decision of the Income Tax Appellate Tribunal (ITAT) to uphold the deletion of additions made by the Assessing Officer (AO) in various assessees' income tax assessments. The additions were based on an alleged higher consideration for a land sale transaction. The High Court dismissed the Revenue's appeals, affirming the ITAT's decision.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Bhanwarlal Murwatiya (High Court of Rajasthan)

Income Tax Appeal No.68 of 2004

Date: 11th February 2008

Key Takeaways:

1. The question of whether a higher consideration was paid in a land sale transaction is a pure question of fact.

2. The Revenue Department must establish with evidence that the alleged higher consideration actually passed from the buyer to the seller.

3. Retracted statements and unexamined witness testimonies are not sufficient grounds for making additions to tax assessments.

4. The courts will not interfere with factual findings of lower authorities unless it's shown that relevant material was ignored or misread.

Issue:

Whether the Income Tax Appellate Tribunal (ITAT) was legally justified in dismissing the Revenue Department's appeal and upholding the deletion of additions made by the Assessing Officer based on an alleged higher consideration in a land purchase transaction?

Facts:

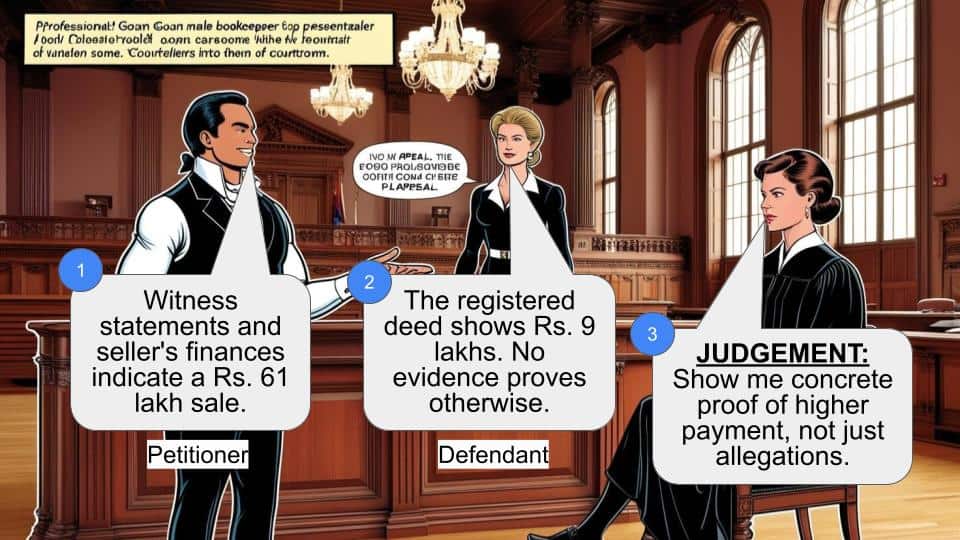

1. Bhanwarlal (the assessee) purchased land from Shri Suresh Soni through a registered sale deed for a consideration of Rs.9 lakhs.

2. The Revenue Department, based on its investigation, alleged that the actual sale price was Rs.61 lakhs.

3. The Assessing Officer made additions to the assessments of various assessees based on this alleged higher consideration.

4. The assessees appealed to the Commissioner of Income Tax (Appeals) [CIT(A)], who deleted the additions.

5. The Revenue Department then appealed to the ITAT, which dismissed all the appeals.

6. The Revenue Department filed appeals in the High Court against the ITAT's decision.

Arguments:

Revenue Department's Arguments:

1. The consideration of Rs.61 lakhs was clearly established on record.

2. Suresh Kumar Soni (the seller) had been assessed, and his balance sheets showed a disproportionate increase in resources during the relevant time.

3. Statements from witnesses Amar Chand, Bhanwarlal, and Radhey Shyam confirmed the higher sale price of Rs.61 lakhs.

Assessees' Arguments:

1. None of the witnesses were examined by the Assessing Officer.

2. Suresh Kumar Soni had given varying statements at different times and was not examined by the Assessing Officer.

3. The assessees had no opportunity to cross-examine the witnesses.

4. An independent enquiry by the Deputy Commissioner found that the land valuation was not above the amount shown in the sale deed.

Key Legal Precedents:

1. Fullangods Rubber Produce Co. Ltd. Vs. State of Kerala & Ors. (91 ITR 18):

This case established that an admission, while an important piece of evidence, is not conclusive and can be shown to be incorrect by the person who made it.

Judgement:

1. The High Court dismissed the Revenue Department's appeals.

2. The court held that the question of the land's price at the relevant time is a pure question of fact.

3. The court emphasized that unless the department establishes that the alleged higher consideration actually passed from the buyer to the seller, it has no right to make additions.

4. The court noted that the witnesses were not examined before the Assessing Officer, and the assessees had no opportunity to cross-examine them.

5. The court found that the department failed to show that any relevant material had been ignored or misread by the CIT(A) or the ITAT.

6. The questions framed by the Revenue Department were answered in favor of the assessees.

FAQs:

Q1: Why did the court dismiss the Revenue Department's appeals?

A1: The court found that the question of land price was a factual matter, and the department failed to prove that the alleged higher consideration actually passed between the parties.

Q2: What is the significance of witness statements in this case?

A2: The court gave little weight to the witness statements because they were not examined before the Assessing Officer, and the assessees had no opportunity to cross-examine them.

Q3: How does this judgment impact similar tax cases?

A3: It emphasizes the need for concrete evidence of actual payment in cases where the tax department alleges a higher consideration than what's stated in official documents.

Q4: What is the importance of the Fullangods Rubber Produce Co. Ltd. case in this judgment?

A4: It established that admissions, while important, are not conclusive evidence and can be retracted or shown to be incorrect.

Q5: Can the Revenue Department challenge factual findings of lower authorities?

A5: Yes, but they must show that relevant material was ignored or misread by the lower authorities, which wasn't done in this case.

All these nine appeals, arise out of the same judgment of the learned Tribunal dated 13.1.2004, passed with reference to different assessees, and for different assessment years. However, they have all been admitted, by framing common questions of law as under:

“1.Whether on the facts and in the circumstances of the case, the learned ITAT was legally justified in dismissing the appeal of the department and upholding the order of the learned CIT(A) deleting the additions made by the A.O. on account of unexplained investment in purchase of land by the assessee?

2.Whether the learned ITAT has erred in law in reversing the finding recorded by the learned A.O. that in the transaction of land in question, the sale consideration received was a sum of Rs.61,00,000/-, as against Rs.9,00,000/- on the basis of admission of the seller corroborated by independent witnesses and material on record?

3.Whether the findings recorded by the learned Tribunal are contrary to record and perverse?” Bereft of unnecessary details, the precise facts are that the assessing officer made the assessment, and while so making assessment, found that certain land was sold to Bhanwarlal by Shri Suresh Soni, by registered sale deed, which sale deed was registered for a consideration of Rs.9 lacs. However, the department on its own investigation, found that the sale was effected for a price of Rs.61 lacs and, therefore, relying on the material, collected during investigation, made additions of different amounts in the assessment of different assessees, while some assessments were made as protective assessments also.

The assessees filed appeals before the learned Commissioner, who partly allowed the appeals, and deleted the additions made. Against that, the Revenue filed appeals before the learned Tribunal, and the learned Tribunal dismissed all the appeals.

A look at the judgment of the learned Tribunal shows, that in para 13, it has been observed as under:

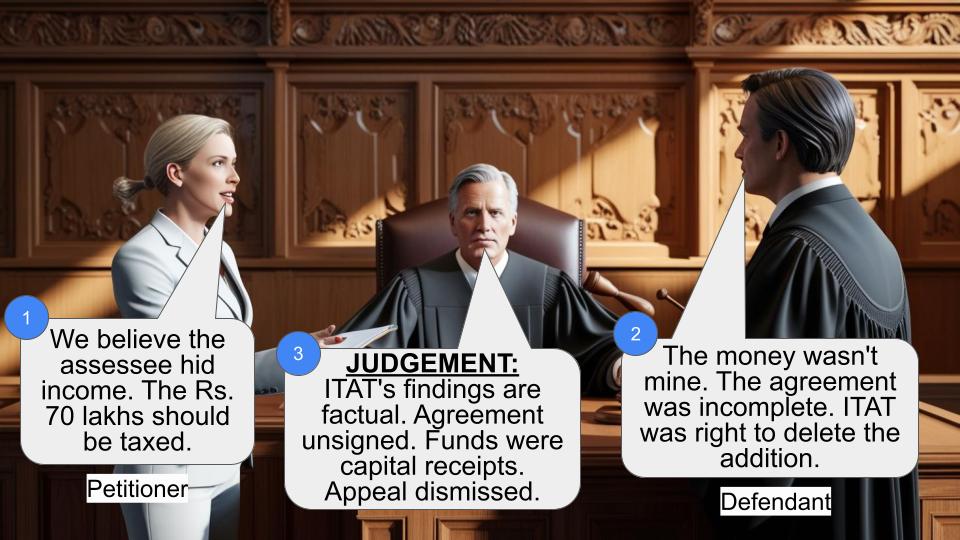

“13. These additions were made, admittedly, on the sole statement of Shri Suresh Kumar Soni, the vendor. The said Shri Suresh Kumar Soni retracted from the statement and almost tried to prove that these statements were extracted from him under duress and pressure. We also agree with the finding of the ld. CIT (A) in this regard because of the following reasons:

a) A retracted statement of any person cannot be made the sole basis for addition because an admission is an extremely important piece of evidence. But it cannot be stated that it is conclusive. It is open to the person who made the admission to show that it is incorrect. Needless to say that this is the law laid by the Highest Court of this country in the case of Fullangods Rubber Produce Co. Ltd. Vs. State of Kerala & Ors. reported in 91 ITR 18.

Then, even giving apart other reasons, reason (g) has again been given as under:

g) There is no evidence on record which can prove that any amount was paid to this appellant except the retracted statement of Shri Suresh Kumar Soni.

Thus, the entire case was sought to be hanged by the Revenue on the peg of statement of Shri Suresh Kumar Soni, said to have been recorded from time to time, who had given varying statements, at different times. Learned Assessing Officer also relied upon certain statements, said to have been recorded by the ADIT, of Amar Chand, Bhanwarlal and Radhey Shyam, but then, no reliance was placed on those statements by the learned Tribunal.

Assailing the impugned judgment, it is contended, with all vehemence, that it is more than clearly established on record, that a consideration of Rs.61 lacs did pass, so much so that Suresh Kumar Soni has been assessed, his balance sheets have been considered, and it is writ large, that during the relevant time, his resources had disproportionately increased, which obviously was on account of the above consideration. Likewise, the aforesaid three witnesses viz; Amar Chand, Bhanwarlal and Radhey Shyam, have also clearly given out, that the land was sold for Rs.61 lacs and, thus, there was no occasion for deleting the additions.

On the other hand, learned counsel for the assessees submitted that none of the witnesses were examined by the assessing officer, and even Suresh Kumar Soni had given varying statements at different occasions, apart from the fact that he was also not examined by the assessing officer, nor did the assessee have any opportunity to cross examine on the version of Suresh Kumar Soni, so as to test his veracity or reliability, and the statements of the said witnesses, recorded by the other authority, could not be looked into, as they are not even relevant, in view of the provisions of Section 32 of the Evidence Act. It was also contended that even an independent enquiry was got conducted, wherein the learned Dy.Commissioner had found, that the valuation of the land was not above the one, as shown in the sale deed, and thus, no interference is required to be made.

We have considered the submissions, and after going through the impugned orders, are of the view that all said and done, the question as to what was the price of the land at the relevant time, is a pure question of fact. Apart from the fact, that even if, it were to be assumed, that the price of the land was different than the one, recited in the sale deed, unless it is established on record by the department, that as a matter of fact, the consideration, as alleged by the department, did pass to the seller from the purchaser, it cannot be said, that the department had any right to make any additions. It is a different story as to, to what extent and how, the statement of Suresh Kumar Soni, as given before different authorities, at different times, can be used against the assessee. More so, when none of the witnesses were examined before the Assessing Officer, and the assessee did not have any opportunity to cross examine them.

In any case, the question as to whether the consideration of Rs.61 lacs, or any other higher consideration than the one, mentioned in the sale deed, did pass from the assessee to the seller or not, does nonetheless remain a question of fact, and it is not shown by the department, that any relevant material has been ignored, or misread by the learned Commissioner, or the learned Tribunal.

In that view of the matter, in our view, the questions, as framed, cannot be even said to be arising, and in any case, are required to be answered against the Revenue, and in favour of the assessee.

Accordingly, the questions are answered as above, and the appeals are dismissed.

( DEO NARAYAN THANVI ),J. ( N P GUPTA ),J.

×

Similar Ripples

Questions

Court Upholds Deletion of Tax Addition, Citing Lack of Evidence on Higher Land Sale Price

Write your CommentSimilar Posts

Generic

- Reportdata/4837.pdf