Court Upholds Multiple Flat Exemption Under Income Tax Act Section 54F (of Inco…

Full News

Court Upholds Multiple Flat Exemption Under Income Tax Act Section 54F (of Income Tax Act, 1961)

Court Upholds Multiple Flat Exemption Under Income Tax Act Section 54F (of Income Tax Act, 1961)

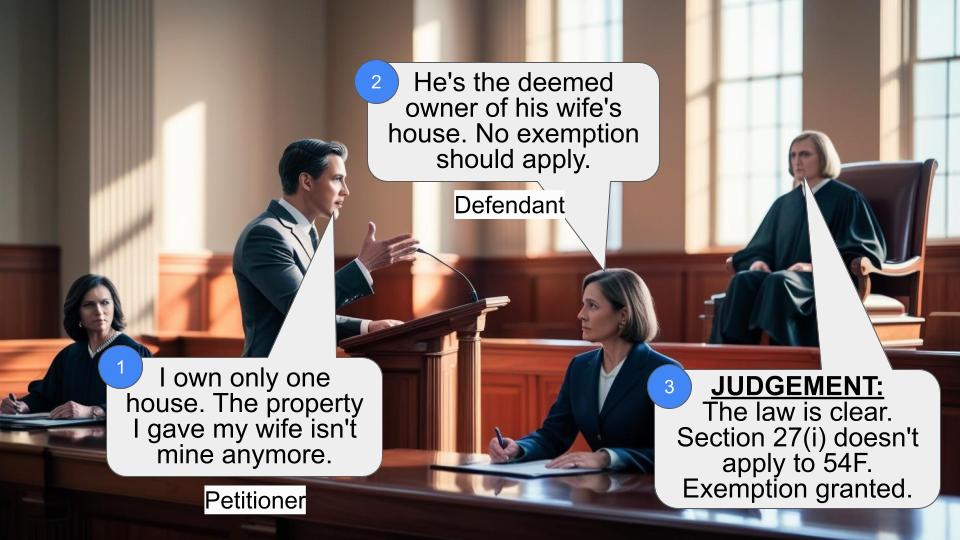

This case involves G. Chinnadurai (the petitioner) challenging the Income Tax Department’s decision to reopen his 2011-12 assessment. The dispute centered around whether the petitioner could claim exemption under Section 54F (of Income Tax Act, 1961) for multiple flats purchased with proceeds from a property sale. The court ruled in favor of the petitioner, allowing the exemption for all five flats.

Get the full picture - access the original judgement of the court order here

Case Name:

G. Chinnadurai Vs Income Tax Officer (High Court of Madras)

W.P.No.28409 of 2015 & M.P.Nos.1 to 3 of 2015

Date: 29th August 2016

Key Takeaways:

- The expression “a residential house” in Section 54F (of Income Tax Act, 1961) can include multiple flats.

- Investing in multiple flats doesn’t disqualify an assessee from claiming exemption under Section 54F (of Income Tax Act, 1961).

- The court’s interpretation favors a broader application of the tax exemption provision.

Issue:

Can an assessee claim exemption under Section 54F (of Income Tax Act, 1961) for investment in multiple residential flats from the proceeds of a single property sale?

Facts:

- The petitioner, G. Chinnadurai, filed a return for the assessment year 2011-12, claiming exemption under Section 54F (of Income Tax Act, 1961) for Rs. 3,12,50,000.

- He invested Rs.2,62,50,000 in five flats from the sale proceeds of a property owned by a partnership firm in which he was a partner.

- The Income Tax Department initiated reassessment proceedings, arguing that exemption should be limited to one residential property.

- The petitioner challenged this reopening of assessment.

Arguments:

Petitioner:

- Section 54F (of Income Tax Act, 1961) allows exemption for investment in residential property, even if spread across multiple flats.

- Relied on previous court decisions (Smt. V.R. Karpagam, Dr. Smt. P.K. Vasanthi Rangarajan, and G. Saroja cases) supporting this interpretation.

Revenue:

- Exemption under Section 54F (of Income Tax Act, 1961) should be limited to one residential house.

- The petitioner invested in five different flats in different blocks, which doesn’t fulfill the conditions for claiming exemption.

Key Legal Precedents:

- Smt. V.R. Karpagam vs. ITO (2013) 157 TTJ (Chennai) 887

- Dr. Smt. P.K. Vasanthi Rangarajan vs. CIT [2012] 23 299 (Mad)

- Commissioner of Income Tax-IX vs. G. Saroja in TC(Appeal) No. 656 of 2015

- CIT vs. Smt. K.G. Rukminiamma (2011) 331 ITR 211 (Kar)

These cases established that “a residential house” in Section 54F (of Income Tax Act, 1961) can include multiple flats or units.

Judgement:

The court ruled in favor of the petitioner, holding that:

- The expression “a residential house” in Section 54F (of Income Tax Act, 1961) should not be interpreted as a single residential house.

- If the legislature intended to limit it to one house, they would have used “one” instead of “a”.

- The petitioner is entitled to claim exemption under Section 54F (of Income Tax Act, 1961) for all five flats.

- The reasons for reopening the assessment were unsustainable.

The court quashed the reassessment proceedings and allowed the Writ Petition.

FAQs:

Q: Does this judgment apply to all cases of multiple flat purchases?

A: While it sets a precedent, each case may be judged on its specific facts and circumstances.

Q: Can I now freely invest in multiple flats and claim exemption under Section 54F (of Income Tax Act, 1961)?

A: It’s advisable to consult a tax professional, as the tax authorities may still scrutinize such claims.

Q: What if the flats are in different locations?

A: The judgment doesn’t specifically address this, but focuses on the interpretation of “a residential house” rather than location.

Q: Does this apply to other sections of the Income Tax Act?

A: This judgment specifically interprets Section 54F (of Income Tax Act, 1961). Its application to other sections would depend on their specific wording and context.

Q: How does this affect the Income Tax Department’s approach?

A: The Department may need to revise its interpretation of Section 54F (of Income Tax Act, 1961) in light of this judgment, potentially leading to fewer challenges of multiple flat exemptions.

1. The petitioner assails the order passed by the respondent dated 30.08.2015, containing the reasons for reopening the assessment for the year 2011-12, under Section 148 (of Income Tax Act, 1961), (Act).

2. For the purpose of adjudication of the present challenge the following facts are relevant. The petitioner filed his return of income for the assessment year 2011-12 admitting an income of Rs.1,71,470/- and claimed exemption under Section 54F (of Income Tax Act, 1961) for an amount of Rs.3,12,50,000/-. A survey under Section 133A (of Income Tax Act, 1961), was conducted in the premises of the petitioner on 31.10.2014, in the course of such survey verification of the genuineness of the claim for deduction as claimed by the petitioner under Section 54F (of Income Tax Act, 1961), which arose out of a sale transaction of the property owned by a partnership firm M/s. Karpagam Studios (hereinafter referred to as the 'firm') in which the petitioner was one of the partners and the petitioner had invested Rs.2,62,50,000/- in five flats at No.134, Arcot Road, Saligramam, Chennai, (subject property), out of the sale consideration of Rs.3,12,50,000/- was undertaken.

3. The firm and its partners (including the petitioner) entered into a deed of sale dated 29.10.2010, in terms of which the petitioner sold his share in the subject property for a sum of Rs.3,12,50,000/- and the consideration was invested towards purchase of constructed area of 9500 sq.ft., along with undivided share of land of an extent of 1807sq.ft., vide agreement dated 29.10.2010. Pursuant to a supplementary agreement, dated 05.09.2013, the allotable built up area was reduced to 8050 sq.ft. The sale proceeds having been fully utilised for the purchase of residential property, the petitioner claimed exemption under Section 54F (of Income Tax Act, 1961). While so, the petitioner received a notice dated 27.03.2015, under Section 148 (of Income Tax Act, 1961), stating that the respondent has reasons to believe that the income chargeable to tax had escaped assessment due to deliberate omission in the return of income of the petitioner as taxable income was not truly and fully disclosed to the department. The petitioner responded by letter dated 27.04.2015, and he filed a return claiming exemption to an extent of Rs.2,62,50,000/- and claiming Rs.50,00,000/- as allowable expenditure in computation of capital gains under Section 49 (of Income Tax Act, 1961), apart from seeking for the reasons for reopening the assessment. The respondent vide reply dated 16.06.2015, stated that the petitioner has invested into five flats out of the sale consideration received, the construction of which was not completed upto 70%. On the relevant date, the petitioner is entitled to claim exemption only for a residential property, construction of which should have been completed within three years from the date of transfer, reckoned as 29.10.2010. In this Writ Petition, the petitioner challenges the notice for reopening along with the reasons recorded by the respondent.

4. The learned counsel for the petitioner submitted that the respondent based on an erroneous assumption that investment in five flats does not satisfy the parameters of Section 54F (of Income Tax Act, 1961), has initiated proceedings for reassessment. That being a beneficial provision, without taking note of the provision, as it stood at the relevant point of time, investment in residential property is allowable, even though spread over multiple flats. In support of such contention, reliance was placed on the decision of the Hon'ble Division Bench of this Court in Smt.V.R.Karpagam vs. ITO, reported in (2013) 157 TTJ (Chennai) 887, and the decision in the case of Dr.Smt.P.K.Vasanthi Rangarajan vs. CIT reported in [2012] 23 Taxmann.com 299 (Mad), and the decision of the Hon'ble Division Bench in the case of Commissioner of Income Tax-IX, vs. G.Saroja in TC(Appeal) No.656 of 2015, dated 04.01.2012. The learned counsel referred to the circular of the CBDT, in circular No.1 of 2015, dated 21.01.2015, to submit that the amendments to Section 54F(1) (of Income Tax Act, 1961), will take effect from 1st, April, 2014 and will accordingly, apply in relation to assessment year 2015-16 and subsequent assessment years and would not apply to the petitioner's case pertaining to the assessment year 2011-12. Further, it is submitted that delay in handing over of the property by the seller to the petitioner is not materially relevant for grant of exemption under Section 54F (of Income Tax Act, 1961). Reliance was placed on the decisions of the ITAT in the case of Narasimha Raju Rudra Raju, vs. Asst., Commissioner of Income Tax, Hyderabad in ITA No.234/Hyd/12, dated 26.04.2013.

5. The learned Senior Standing counsel for the respondent Department submitted that the petitioner has invested in five different flats in different blocks, out of which one is under joint ownership and therefore, the petitioner has not fulfilled the condition for claiming exemption under Section 54F (of Income Tax Act, 1961), which states that within a period of three years, the assessee should have constructed a residential house, which has to be interpreted as one residential house and not more than one and this position was so even prior to the amendment of Section 54F(1) (of Income Tax Act, 1961). The learned counsel sought to factually distinguish the decisions in the case of Smt.V.R.Karpagam, and Dr.Smt.P.K.Vasanthi Rangarajan.

Further, it is submitted that as per the principles laid down by the Hon'ble Supreme Court in the case of GKN Driveshafts (India) Ltd Vs. Income Tax Officer, 259 [ITR] 19, the petitioner has to participate in the reassessment proceedings. The learned counsel placed reliance on the decision of the Punjab & Haryana High Court in the case of Pawan Arya vs. Commissioner of Income Tax reported in [2011] 11 Taxmann.com 312 (Punjab & Haryana), and the decision of the ITAT – Mumbai in Shri Narender Khubchandani vs. Income tax Officer in I.T.A.No.238/Mum/2011, dated 17.12.2014.

6. Heard Dr.Anita Sumanth, learned counsel for the petitioner and Mr.M.Swaminathan, learned Senior Standing counsel for the respondent and perused the materials placed on record.

7. Section 54F (of Income Tax Act, 1961) deals with 'Capital gain on transfer of certain capital assets not to be charged in case of investment in residential house'. The common condition both under Section 54E (of Income Tax Act, 1961) to 54ED and 54F, is that the assessee must purchase or construct a residential house before or after the transfer of the asset, which yields capital gains. If the assessee had invested the money in the construction of the house within the time limit, the exemption cannot be denied on the ground that construction has not been completed [see CIT vs. Praveen Kumar reported in 290 ITR 90 (Mad)]. However, the onus is on the assessee to produce sufficient material to establish the claim for exemption. In the instant case, the petitioner claimed exemption by stating that they have purchased flats with the built up area of 8050sq.ft., along with an extent of 1807 sq.ft of undivided share in land by a document, dated 29.10.2010. The reason for reopening the assessment is that the petitioner has invested an amount of Rs.2,62,50,000/-, into five flats and the construction of the flats were completed only upto 70% at the relevant point of time and therefore, the petitioner is eligible to claim exemption under Section 54F (of Income Tax Act, 1961) only for a residential property, apart from the fact that the only 70% of the construction has been completed. Thus, the question would be whether the petitioner can be denied exemption on the ground that he has invested in five flats and what would be the effect of the construction having been only partially completed.

8. The legal issue has been considered by the Hon'ble Division Benches of this Court as well as by the ITAT. As factual matrix in Smt.V.R.Karpagam is more or less similar to the case on hand, the same is referred at the first instance. In Smt.V.R.Karpagam (supra), (ITAT), the assessee challenged the order restricting the claim for exemption under Section 54F (of Income Tax Act, 1961) to a single flat. The assessee Smt.V.R.Karpagam entered into an agreement for development of a piece of land owned by her and as per the agreement, she was entitled to receive 43.75% of the built up area, which translated to five flats. The claim for exemption was restricted only to one flat. It was contended by the Revenue that the reliance placed on the decision in the case of Commissioner of Income Tax-IX, vs. G.Saroja, T.C.(A).No.656 of 2005, is distinguishable, since in the said case, High Court had granted relief to the assessee for four flats received by the assessee in exchange of ownership over part of the land with building and four flats, were assessed, as one unit with one door number, whereas in the case of Smt.V.R.Karpagam, it was five flats with different residential units with different door numbers. While considering the said factual issue, the Tribunal was called upon to examine as to whether “a residential house” should be treated as “one residential house” or whether “more than one residential house” can be considered eligible for deduction under Section 54 (of Income Tax Act, 1961). After referring to the said provision, the Tribunal took note of the various decisions of the Courts including the decision in the case of Dr.Smt.P.K.Vasanthi Rangarajan vs. CIT (supra) and held as follows:-

The proviso which disables the assessee from claiming exemption under Section 54F (of Income Tax Act, 1961) mentions at cl.(i) that assessee concerned should not own more than one residential house, other than the new asset. Other clauses also restrict a claim under Section 54F (of Income Tax Act, 1961), if an assessee purchased a house or sub-proviso (i) of proviso (a) i.e., owning more than one residential house on the date of transfer of the original asset will come into play only where assessee had within a period of one year before the date of transfer constructed a residential house as mentioned in substantive portion of sub-section (1). New asset is clearly defined in the substantive portion, to mean 'a residential house'.

Whether 'a residential house' can include only one flat or more than one flat was the issue considered by Hon'ble Karnataka High Court in the case of CIT vs. Smt.K.G.Rukminiamma (2010) 48 DTR (Kar) 377; (2011) 239 CTR (Kar) 435; (2011) 331 ITR 211 (Kar). Relying on Section 13 of the General Clauses Act, 1897, it was held as under by their Lordships at para 10 of the judgment:

“(2) words in the singular shall include the plural, and vice versa”

10. The context in which the expression 'a residential house' is used in Section 54 (of Income Tax Act, 1961) makes it clear that, it was not the intention of the legislation to convey the meaning that it refers to a single residential house. If that was the intention, they would have used the word 'one'. As in earlier part, the words used are buildings or lands which are plural in number and that is referred to as 'a residential house', the original asset. An asset newly acquired after the sale of the original asset also can be buildings or lands appurtenant thereto, which also should be 'a residential house'. Therefore, the letter 'a' in the context it is used should not be construed as meaning 'singular'. But being an indefinite article, the said expression should be read in consonance with the other words 'buildings and lands' and therefore, the singular 'a residential house' also permits use of plural by virtue of Section 13(2) of the General Clauses Act. This is the view which is taken by this Court in the aforesaid CIT vs. D.Ananda Basappa case in IT Appeal No.113 of 2004, disposed of on 20th Sept., 2008 (reported at (2009) 223 CTR (Kar) 186; (2009) 20 DTR (Kar) 266-Ed.]”

8. Their Lordships have clearly held in the above judgement that 'a residential house' in the context could not be construed as a singular. In the said case also, claim for exemption was with regard to four flats in lieu of share in land, but the claim was under Section 54 (of Income Tax Act, 1961) and not under Section 54F (of Income Tax Act, 1961).

However, in our opinion the meaning given to the expression 'a residential house' will apply pari passu to Section 54F (of Income Tax Act, 1961) also, since the expression used here is also 'a residential house'. New asset defined in Section 54F (of Income Tax Act, 1961), as 'a residential house' has also to be understood in the plural. It is not necessary that all residential units should have a single door number allotted to it as argued by the learned Departmental Representative No doubt Hon'ble jurisdictional High court in the case of G.Saroja (supra), did consider the fact that different flats were having one door number. However, this also was not the reason why assessee was held to be eligible for claiming of exemption under Section 54F (of Income Tax Act, 1961). Their Lordships took cue from the decision of Hon'ble Karnataka High Court in the case of Smt.K.G.Rukminiamma (supra). Similar exemption was given by the Hon'ble jurisdictional High Court again in the case of Dr.(Smt) P.K.Vasanthi Rangarajan (Supra), wherein there was no claim that flats allotted in lieu were having single number. We are therefore of the opinion that assessee was eligible for claiming exemption under Section 54F (of Income Tax Act, 1961) on the five flats received by her in lieu of the land she had parted with.

9. In the case of Dr.Smt.P.K.Vasanthi Rangarajan, the assessee entered into an agreement for joint development of eight apartments in another property owned by her individually. In terms of such agreement, she retained to herself undivided share in the land to an extent of 50% and the balance 50% was to be conveyed to the developer. The consideration for parting with 50% of the undivided land share was in lieu of four flats as well as a sum of Rs.10 lakhs payable by the developer. The claim for exemption under Section 54 (of Income Tax Act, 1961), was rejected, affirmed in appeal and further affirmed by the Tribunal and the correctness of these orders were tested by the Hon'ble Division Bench. The assessee contended before the Hon'ble Division Bench that investing in four flats would not disentitle the claim for exemption placing reliance on the decision in the case of G.Saroja, which in turn followed the decision of the Karnataka High Court in the case of CIT vs. Smt.K.G.Rukminiamma reported in [2011] 331 ITR 211 and CIT vs. Ananda Basappa reported in [2009] 309 ITR 329 and the Special Leave Petition filed against the decision in the case of Ananda Basappa having been dismissed, the assessee was entitled to claim exemption. The Hon'ble Division Bench agreed with the view expressed in the decision in the case of G.Saroja, and held that the purchase of four flats would not disentitle the assessee for exemption.

10. The learned counsel for the revenue relied on the decision of the Punjab and Haryana High Court in the case of Pawan Arya to sustain the impugned order. In the said case, the assessee claimed exemption on capital gains on sale of flat on the ground of acquisition of two houses. When the assessee placed reliance on the decision of the Tribunal in the case of D.Anand Basappa (supra), it was distinguished by the High Court stating that in the said case, two flats could be treated to be one house as both had been combined to make one residential unit.

11. In the decision of the Tribunal in the case of Shri Narender Khubchandani (supra), the assessee had purchased two residential flats under two different agreements from different sellers, they were adjacent units and they were combined into one unit having a common kitchen. In the said case, the property sold by the assessee consisted of two garages. However, the sale agreement did not refer to any garages. The Assessing Officer estimated the sale consideration of the garages and assessed the same as long term capital gain. While deciding the correctness of said order, the Tribunal took note of the other decisions and pointed out that in the case of CIT vs. Devdas Naik in ITA No.2483 of 2011, dated 10.06.2014, (Bombay High Court), wherein it was held that exemption under Section 54F (of Income Tax Act, 1961) will be applicable only when house purchased is a single unit and in the said case (Devdas Naik), the assessee purchased two residential flats under two different door numbers, from two different owners and combined it to one unit having common kitchen. On facts, the High Court held that the assessee was entitled to deduction. However, the Tribunal followed the decision of the jurisdictional High Court namely, the Bombay High Court in ITA No.238 of 2011 and on facts, in the said case, and held that the assessment order has computed the sale consideration relating to garages purely on surmises and conjuncture without bringing any material on record to show that the assessee had received any consideration separately for garages, over and above, the amount declared in the development agreement.

12. Before proceeding further, I would like to point out that the facts, which arose for consideration in Pawan Arya (supra), Shri Narender Khubchandani (supra), are different from that of the case on hand. In fact, the factual position is required to be carefully analysed to see as to whether the transaction done by the assessee would fall within the meaning of a residential unit. The Bombay High Court in Devdas Naik (supra), considered two flats purchased from two different owners with two different door numbers to be one because on purchase, it was converted into a single dwelling unit with one kitchen. Therefore, sans facts a decision cannot be taken. Therefore, we have to look into the type of transaction which had been entered into between the parties. The petitioner and other partners M/s.Karpagam Studio, entered into an agreement to execute a deed of an absolute sale dated 29.10.2010, in respect of the property in Saligramam and Virugambakkam villages and a separate agreement was entered into by the partners individually and the petitioner entered into such an agreement on 29.10.2010.

13. In terms of the said agreement, the developer has offered 9500sq.ft., of built up area along with proportionate undivided share of land in the proposed building complex. Therefore, the agreement is a composite agreement and it mentions that the petitioner is entitled to a total built up area of 9500sq.ft. Therefore, it would be immaterial, if whether 9500sq.ft., of built up area given to the petitioner is separate over in the same floor or in a different floor or in different blocks in the apartment complex, since the consideration which has passed on, was for agreeing to offer 9500sq.ft., of built up area along with proportionate undivided share. This agreement was followed by a supplementary agreement, dated 5th September 2013, where except for a small reduction in the super built up area by reducing it to 8050sq.ft., and giving the details of the flat numbers, there are no other changes to the principal agreement dated 29.10.2010.

14. Thus, by applying the legal principles enunciated in the case of Smt.V.R.Karpagam (supra), Dr.Smt.P.K.Vasanthi Rangarajan (supra), and G.Saroja, (supra), it is to be pointed out that the expression “a residential house” used in Section 54 (of Income Tax Act, 1961), should not be taken to convey the meaning that it refers to a 'single residential' house and if that was the intention of the legislature, the framers of the statute would have used the word “one” instead of “a”. In fact, the facts of the case in Smt.V.R.Karpagam (supra), is more or less identical to that of the case on hand, which also pertained to a development of a property, originally owned by the assessee and the consideration was that the owner/assessee was to receive 43.75% of built up area after development, which translated into five flats.

15. In the instant case, there is no doubt raised by the respondent with regard to the petitioner's eligibility to claim exemption under Section 54F (of Income Tax Act, 1961), but the dispute is as to whether the petitioner is entitled to claim such exemption for all the five flats or for only one flat.

16. In the light of the above discussion and taking note of the law laid down in the various decisions cited above, it is held that the petitioner is entitled to the benefit of exemption under Section 54F (of Income Tax Act, 1961) as claimed by him and the reasons for reopening the assessment for the relevant assessment year is unsustainable. Accordingly, the Writ Petition is allowed and the impugned proceedings are quashed. No costs. Consequently, connected Miscellaneous Petitions are closed.

29.08.2016

Index :Yes/No

Internet :Yes/No

To

The Income Tax Officer, Income Tax Department, Non Corporate Ward 13(2), Annexe Building, Room No.404, 4 th Floor,

121, Nungambakkam High Road, Chennai – 600 034.

T.S.SIVAGNANAM, J.

×

Similar Ripples

Questions

Court Upholds Multiple Flat Exemption Under Income Tax Act Section 54F (of Income Tax Act, 1961)

Write your CommentSimilar Posts

Generic

- Reportdata/HC-28409-2015.pdf