Full News

Court Upholds Revenue Expense Deductions, Rejects Capital Expenses in Share Issue Case

Court Upholds Revenue Expense Deductions, Rejects Capital Expenses in Share Issue Case

This case involves a dispute between the Revenue (tax authorities) and Kreon Financial Services Ltd. regarding the classification of expenses related to share issuance. The court ultimately sided with the assessee (Kreon Financial Services Ltd.) on most points, allowing deductions for revenue expenses while upholding the rejection of certain capital expenses.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Kreon Financial Services Ltd. (High Court of Madras)

Tax Case (Appeal) No.2308 of 2006

Date: 3rd October 2012

Key Takeaways

1. Expenses related to day-to-day business operations can be classified as revenue expenditure and are eligible for tax deductions.

2. Certain expenses related to share issuance, such as printing, lead manager fees, and advertising, may be considered capital expenditure and not eligible for deduction.

3. Factual findings by lower authorities (CIT(A) and Tribunal) are given significant weight by higher courts if they are consistent and based on thorough examination.

Issue

The main question in this case was: Are expenses related to the issue of share capital eligible for deduction as revenue expenditure, or should they be considered capital expenditure?

Facts

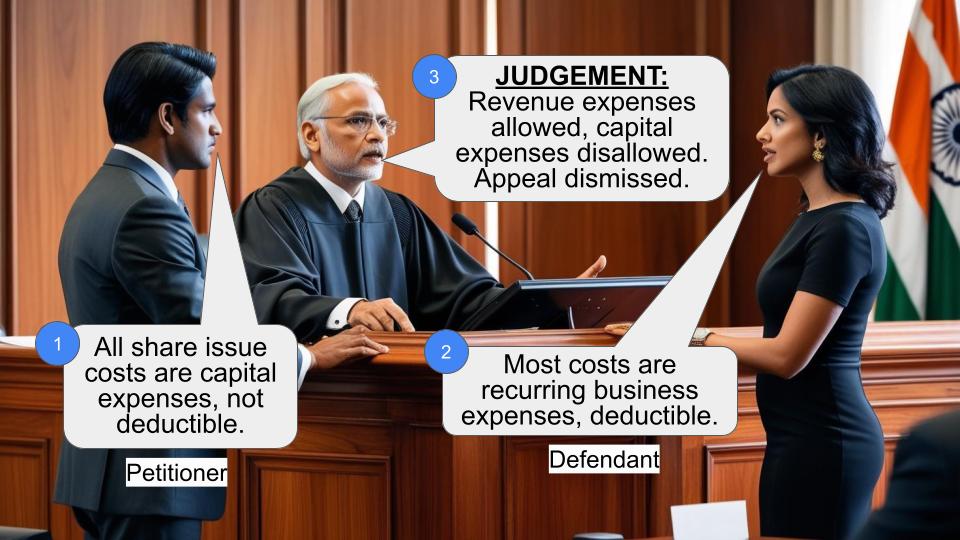

So, here's what happened. Kreon Financial Services Ltd. claimed a deduction of Rs.15,02,119 as revenue expenditure for share issue expenses in the assessment year 1996-97. The Assessing Officer said, "Hold on, these are capital expenses!" and disallowed the claim.

Kreon wasn't happy about this, so they appealed to the Commissioner of Income Tax (Appeals), or CIT(A) for short. They provided a detailed breakdown of their expenses, which included things like dispatch costs, registration fees, printing expenses, and even advertisement costs.

The CIT(A) looked at this list and said, "Okay, some of these are definitely revenue expenses, but others look more like capital expenses." They allowed most of the deductions but rejected three: printing expenses, lead manager fees, and advertisement expenses.

The Revenue folks weren't satisfied with this decision, so they took it to the next level - the Income Tax Appellate Tribunal. But the Tribunal agreed with the CIT(A)'s decision.

Arguments

On one side, we have the Revenue arguing that all these expenses related to share issuance should be considered capital expenditure. Their logic? These costs are associated with raising capital, which is a long-term benefit to the company.

On the other side, Kreon Financial Services Ltd. is saying, "Hey, most of these are just regular business expenses. We need to do these things to keep our day-to-day operations running smoothly."

Key Legal Precedents

Interestingly, this judgment doesn't explicitly mention any specific legal precedents. Instead, it focuses on the factual findings of the lower authorities and the principle that higher courts shouldn't interfere with these findings unless there's a clear contradiction or error.

Judgement

The High Court looked at all of this and basically said, "You know what? The CIT(A) and the Tribunal got it right." They agreed that most of the expenses were indeed revenue in nature and could be deducted. However, they also agreed that the printing expenses, lead manager fees, and advertisement expenses (totaling Rs.3,08,791) were capital expenses and shouldn't be deducted.

The court emphasized that the CIT(A) had done a thorough job, even getting a detailed report from the Assessing Officer about each expense. They felt there was no reason to mess with this well-reasoned decision.

In the end, they dismissed the Revenue's appeal and answered the questions of law in favor of Kreon Financial Services Ltd.

FAQs

1. Q: What's the difference between revenue and capital expenditure?

A: Revenue expenditure relates to day-to-day business operations, while capital expenditure is for long-term benefits or assets.

2. Q: Why were some expenses allowed and others disallowed?

A: Expenses that were seen as part of regular business operations were allowed. Those related to raising capital (like advertising for share issuance) were considered capital expenses and disallowed.

3. Q: Does this case set a precedent for future tax cases?

A: While it doesn't establish new legal principles, it reinforces the importance of properly categorizing expenses and the weight given to lower authorities' factual findings.

4. Q: Can companies now deduct all share issuance expenses?

A: No, this case shows that each expense needs to be examined individually. Some may be deductible, while others may not be.

5. Q: Why didn't the High Court interfere with the lower authorities' decisions?

A: The High Court found that the CIT(A) and Tribunal had done a thorough job in examining the facts and their findings were consistent. Courts typically don't interfere unless there's a clear error or contradiction.

1. The Revenue is on appeal in respect of assessment year 1996-97. The following are the substantial questions of law raised at the time of admitting the appeal.

"1. Whether in the facts and circumstances of the case, the Tribunal was right in holding that expenses relating to issue of share capital would be eligible for deduction as a revenue expenditure?

2. Whether in the facts and circumstances of the case, expenditure which might otherwise be allowable as regular business expenditure would be allowed as such when incurred in relation to issue of share capital?"

2. The assessee had claimed share issue expenses of Rs.15,02,119/- as revenue expenditure. The said claim of the assessee was disallowed by the Assessing Officer on the ground that those expenses are capital in nature. Aggrieved by the order of the assessment, the assessee filed an appeal before the first Appellate Authority. As the Assessing Officer has disallowed the claim of the assessee by pointing out that they have not given any details regarding the claim for deduction in respect of sum of Rs.15,02,119/-, the assessee, before the first Appellate Authority, had given a break up details with regard to the expenses meted out by the assessee in respect of the share issues, which are as follows:-

1. Despatch and out of pocket exp. Rs. 2,07,616.50

2. Registration Fees Rs. 50,000.00

3. Printing expenses Rs. 32,989.00

4. Listing Fees Rs. 39,250.00

5. Stationery Exp. Rs. 1,91,674.20

6. Travelling & Meeting exp. Rs. 26,635.85

7. Bank Charges & Commission Rs. 57,288.00

8. Lead Managers fees Rs. 1,13,000.00

9. Advertisement Rs. 7,74,665.30

10. Prof. Certificate Rs. 9,000.00

--------------------

Rs.15,02,118.65

3. Out of the above total ten heads of expenses, the first Appellate Authority disallowed the claim in respect of printing expenses, lead manager fees and advertisement expenses by holding that those expenses are capital in nature. In so far as the other expenses are concerned, the first Appellate Authority allowed the claim of the assessee by holding that those expenses are revenue in nature. Aggrieved by the said order of the first Appellate Authority, the Revenue went on appeal before the Income Tax Appellate Tribunal. The Tribunal rejected the appeal filed by the Revenue and confirmed the order of the first Appellate Authority by holding that the findings given by the Commissioner of Income Tax (Appeals) does not warrant any interference as the Commissioner of Income Tax (Appeals) has given categorical findings as to which are the expenses incurred in the regular course of the business and which are the expenses incurred in the capital field. The Tribunal has also noted that the Commissioner of Income Tax (Appeals) has passed the order only after getting remand report from the Assessing Officer with regard to each and every heads of expenses for which the deduction was sought for.

4. We have heard the learned counsel for respective parties and perused the orders of the authorities below and we find every justification in accepting the order of the Commissioner of Income Tax (Appeals) wherein and whereby the Commissioner has allowed the claim of deduction, except in the case of printing expenses, lead manager fees and advertisement expenses, totalling to Rs.3,08,791/-. As the said expenses are capital in nature, the same has been rightly rejected by the Commissioner of Income Tax (Appeals). Likewise, while considering the other expenses, the Commissioner has given categorical finding that the nature of the expenses is only revenue, as those expenses are to meet out the day today transactions of the business of the assessee.

5. In view of the factual finding rendered by the Commissioner of Income Tax (Appeals) based on the report received from the Assessing Authority, which has been accepted by the Tribunal and there being no contradiction in the finding of the Tribunal, we find no reason to interfere with the order. In the result, the appeal is dismissed and the questions of law raised are answered against the Revenue. No costs.

×

Similar Ripples

Questions

Court Upholds Revenue Expense Deductions, Rejects Capital Expenses in Share Issue Case

Write your CommentSimilar Posts

Generic

- Reportdata/5383.pdf