Court Upholds Revenue Expenses for Business Expansion, Rejecting Capital Expend…

Full News

Court Upholds Revenue Expenses for Business Expansion, Rejecting Capital Expenditure Claim

Court Upholds Revenue Expenses for Business Expansion, Rejecting Capital Expenditure Claim

This case involves an appeal by the revenue department against a decision made by the Income Tax Appellate Tribunal (ITAT). The ITAT had ruled in favor of the assessee, Kayal Syntex Ltd, allowing certain expenses as revenue expenditure rather than capital expenditure. The High Court upheld the ITAT's decision, dismissing the revenue department's appeal.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Kayal Syntex Ltd. (High Court of Gujarat)

Tax Appeal No. 232 & 233 of 2006

Date: 14th June 2016

Key Takeaways:

1. Expenses related to business expansion can be considered revenue expenditure under certain circumstances.

2. The court emphasized that the nature of expenses, not their treatment in books of accounts, is crucial for tax purposes.

3. The decision reinforces the principle that expanding an existing business unit is different from setting up a new business for tax purposes.

Issue:

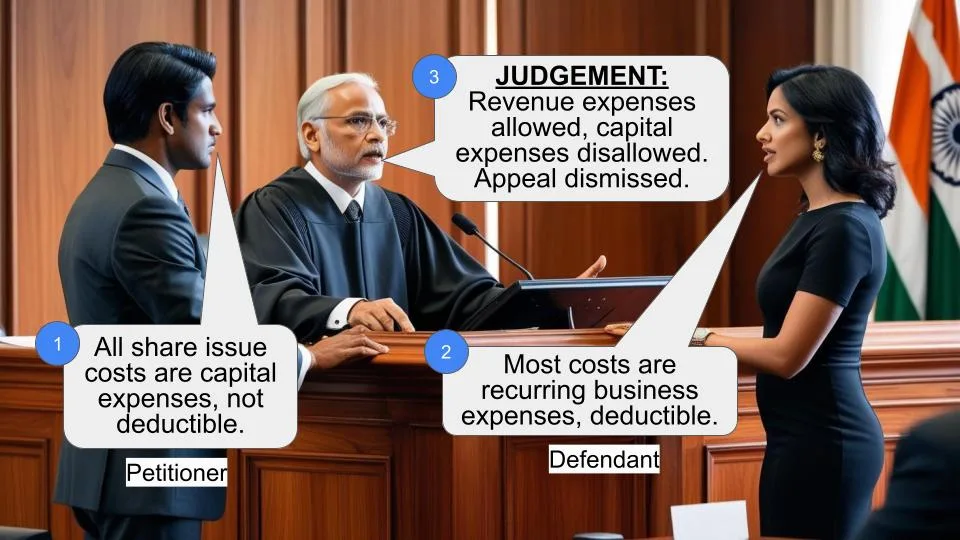

Was the Income Tax Appellate Tribunal correct in law and on facts in upholding the addition on account of revenue expenditure, which the revenue department claimed was capital in nature under Section 37 (of Income Tax Act, 1961)?

Facts:

1. The case pertains to assessment years 1996-97 and 1997-98.

2. The assessee, Kayal Syntex Ltd, claimed expenditure of Rs. 37,04,458 as revenue expenditure.

3. The Assessing Officer (A.O) initially observed that this expenditure was towards acquisition of capital expenditure and disallowed it as revenue expenditure.

4. On appeal, the Commissioner of Income Tax (Appeals) deleted the addition to the extent of Rs.37,04,458 and sustained the remaining addition.

5. The Income Tax Appellate Tribunal (ITAT) upheld the CIT(A)'s decision regarding the interest payment of Rs.37,04,458 and deleted the remaining addition.

6. The revenue department appealed against this decision in the High Court.

Arguments:

Revenue's Argument:

- The assessee had initially debited the expenses as capital expenditure in its books of accounts and shouldn't be allowed to change its stand later.

- The revenue cited the case of Commissioner of Income Tax, Central, Bombay vs. Jalan Trading Co. P. Ltd (1985) 155 ITR 536 (SC) to support their position.

Assessee's Argument:

- The expenses were for expansion of the existing business, not for setting up a new business.

- The assessee cited the case of Commissioner of Income Tax vs. Ghanshyam Steel work ltd (2010) 195 Taxman 180 (Guj) to support their position.

Key Legal Precedents:

1. Commissioner of Income Tax vs. Ghanshyam Steel work ltd (2010) 195 Taxman 180 (Guj): This case held that expenses incurred for expanding an existing business unit (not setting up a new business) were allowable as revenue expenses under Section 36(1)(iii) (of Income Tax Act, 1961) or Section 37 (of Income Tax Act, 1961).

2. The court also mentioned the case of United Phosphorus Ltd, where it was observed that the treatment of expenses in books of accounts is not final for tax proceedings unless these entries align with IT provisions.

Judgement:

The High Court dismissed the revenue's appeal and upheld the ITAT's decision. The court found that:

1. The case was similar to Ghanshyam Steel Work Ltd, where expenses for business expansion were allowed as revenue expenditure.

2. The new unit appeared to be an expansion of the existing business rather than a new business setup.

3. The court found no infirmity in the Tribunal's order that warranted interference.

FAQs:

1. Q: Why did the court allow the expenses as revenue expenditure?

A: The court determined that the expenses were for expanding an existing business, not setting up a new one, making them allowable as revenue expenditure.

2. Q: Does how a company records expenses in its books of accounts determine their tax treatment?

A: Not necessarily. The court emphasized that the nature of the expenses, not their treatment in books of accounts, is crucial for tax purposes.

3. Q: What sections of the Income Tax Act were relevant in this case?

A: The case primarily dealt with Sections 36(1)(iii) and 37 of the Income Tax Act, 1961, which relate to allowable deductions and general deductions respectively.

4. Q: How does this judgment impact businesses looking to expand?

A: This judgment suggests that expenses incurred for business expansion may be treated as revenue expenditure, potentially allowing for tax deductions in the year they're incurred.

5. Q: What was the significance of the Ghanshyam Steel Work Ltd case in this judgment?

A: The Ghanshyam Steel Work Ltd case set a precedent that expenses for business expansion could be considered revenue expenditure, which was directly applicable to this case.

1. By way of these appeals, the appellant-revenue has challenged the judgment and order dated 18.02.2005 passed by the Income-tax Appellate Tribunal, Ahmedabad Bench ‘B’ in ITA No. 2723/Ahd/2000 and 2724/Ahd/2000 for the assessment years 1996-97 and 1997-98.

2. These matters were admitted by this Court for consideration of the substantial question of law as to whether the Appellate Tribunal was right in law and on facts in upholding the addition on account of revenue expenditure capital in nature u/s 37 (of Income Tax Act, 1961).

3. The assessee had claimed expenditure of Rs. 37,04,458/- as revenue expenditure. During the course of assessment proceedings, the A.O observed that the said expenditure was towards acquisition of a capital expenditure and therefore not entitled to deducted as revenue expenditure. On appeal the CIT (Appeals) deleted the addition to the extent of the said amount and sustained the remaining addition. On further appeal, the Tribunal upheld the decision of CIT(A) with regard to interest payment to the tune of Rs. 37,04,458/- and deleted the remaining addition.

4. Being aggrieved and dissatisfied with the impugned orders passed by the Tribunal, the revenue has preferred the present Tax Appeals for consideration of the aforesaid substantial question of law.

5. Ms. Mauna Bhatt, learned advocate appearing for the revenue submitted that the Tribunal has erred in upholding the decision of CIT(A) with regard to deleting the addition on account of revenue expenditure being capital in nature. She submitted that the assessee itself had debited the same as capital expenditure in its books of accounts and therefore it cannot change its stand later on. Relying upon a decision of the Apex Court in the case of Commissioner of Income Tax, Central, Bombay vs. Jalan Trading Co. P. Ltd reported in (1985) 155 ITR 536 (SC) wherein it is held that since the assessee was a new company and it had no other business and it acquired under the assignment the right to carry on the business of sole selling agency on a long term basis subject to renewal of the agreement stipulating to pay 75 per cent of its annual net profits the expenditure was made for the initial outlay and a capital asset was acquired thereby, Ms. Bhatt submitted that the Tribunal has erred in upholding the order passed by CIT(A).

6. Mr. Hardik Vora, learned advocate appearing for the assessee supported the impugned order and submitted that the same having been passed in accordance with law does not call for any interference by this Court. He has submitted that in the assessment years 1996-97 and 1997-98 the assessee had claimed expenses to the tune of Rs. 99,18,607/- and Rs. 97,62,536/- respectively as revenue expenditure and that the assessee had initially capitalized these expenses in the books of account which was duly audited by the Chartered Accountant. He submitted that while filing return of income the assessee claimed the amounts as allowable expenditure.

He has relied upon the decision of this Court in the case of Commissioner of Income Tax vs. Ghanshyam Steel work ltd reported in (2010) 195 Taxman 180 (Guj) wherein it is held that in a case of new unit being merely an expansion of the existing business of the assessee and not setting up of a new business the expenses incurred in that regard were allowable as revenue expenses under Section 36(1)(iii) (of Income Tax Act, 1961) or Section 37 (of Income Tax Act, 1961).

7. Heard learned advocates for both the sides. The main ground for disallowance of the expenses by the Assessing Officer was that the said expenses were capitalized in the books of accounts of the assessee. The Tribunal has relied upon a decision of the Tribunal in the case of United Phosphorus Ltd. and observed that merely because the expenses have been capitalized in the books of account, the same cannot be a final wording in the tax proceedings unless these entries of books of account are in consonance with the IT provisions.

8. The facts in the case of Ghanshyam Steel Work Ltd (supra) are quite similar. This Court in the said case observed as under:

“7. Thus, both, the Tribunal as well as Commissioner (Appeals), have recorded concurrent findings of fact and come to the conclusion that the so called new unit was merely an expansion of the existing business of the assessee and was not setting up of a new business and as such the expenses incurred in this regard were allowable as revenue expenses. Considering the fact that the Assessing Officer had not considered the claims of each of the items of expenditure incurred by the assessee from the angle as to whether the same were in the nature of revenue or capital expenditure, the matter has been restored to the Assessing Officer to look into the nature of the expenses and consider as to whether the same are allowable under Section 36(1)(iii) (of Income Tax Act, 1961) or Section 37 (of Income Tax Act, 1961). In the circumstances, no infirmity can be found in the approach adopted by Commissioner (Appeals) as confirmed by the Tribunal so as to warrant interference. No question of law, much less any substantial question of law, can be stated to arise from the impugned order of the Tribunal. “

9. In the present case also there seems to be an expansion in the existing unit of business. The issue in the present case is squarely covered by the decision of this Court in the aforesaid case. We therefore do not find any infirmity in the order passed by the Tribunal so as to warrant interference.

10. In the premises aforesaid, the question raised in the present appeals are therefore answered in favour of the assessee and against the revenue. The impugned order passed by the Tribunal is confirmed. Appeals are dismissed accordingly.

(K.S.JHAVERI, J.)

(G.R.UDHWANI, J.)

×

Similar Ripples

Questions

Court Upholds Revenue Expenses for Business Expansion, Rejecting Capital Expenditure Claim

Write your CommentSimilar Posts

Generic

- Reportdata/2765.pdf