Court Upholds Tax Deduction for Unified Housing Project Despite Multiple Plot A…

Full News

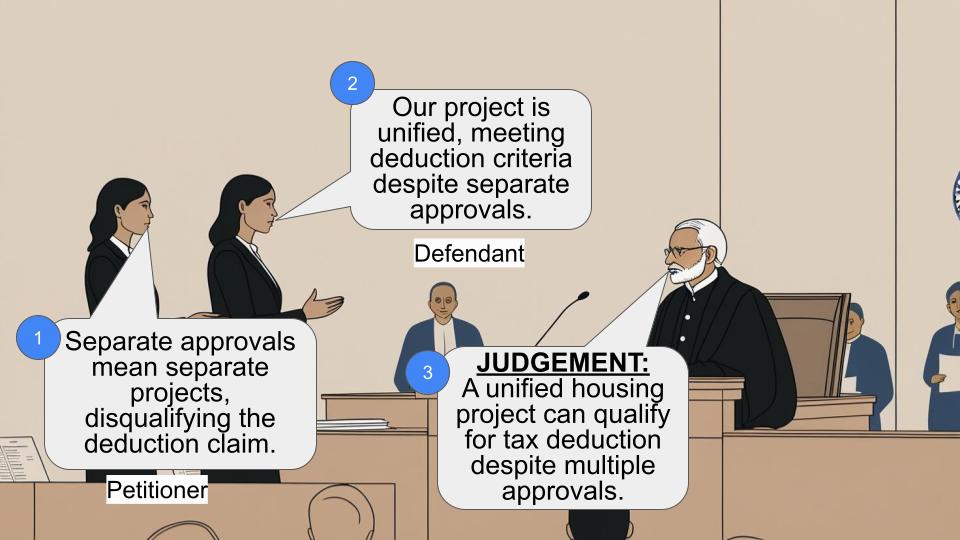

Court Upholds Tax Deduction for Unified Housing Project Despite Multiple Plot Approvals

Court Upholds Tax Deduction for Unified Housing Project Despite Multiple Plot Approvals

This case involves a dispute between the Commissioner of Income Tax (the Revenue) and Smt. A. Jagadeeswari (the Assessee) regarding the eligibility for tax deduction under Section 80IB(10) (of Income Tax Act, 1961). The Revenue challenged the Assessee's claim for deduction on a housing project, arguing that it consisted of separate projects on plots less than one acre each. The court ultimately ruled in favor of the Assessee, upholding the deduction claim.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Smt. A. Jagadeeswari (High Court of Madras)

TCA.No.377 of 2018

Date: 2nd March 2020

Key Takeaways:

1. For deduction under Section 80IB(10) (of Income Tax Act, 1961), the Assessee need not be engaged in developing and constructing the housing project, but must be the property owner.

2. A unified housing project can qualify for deduction even if approvals are obtained separately for individual plots.

3. The court's decision reinforces previous judgments favoring the Assessee in similar cases.

Issue:

Is the Assessee entitled to claim deduction under Section 80IB(10) (of Income Tax Act, 1961), for a housing project developed on multiple plots, each measuring less than one acre, but collectively forming a unified project?

Facts:

1. The Assessee filed an Income Tax Return for the Assessment Year 2007-08, claiming a deduction of Rs.4,99,11,555/- under Section 80IB(10) (of Income Tax Act, 1961).

2. The Assessing Officer noticed that the Assessee obtained separate plans for construction on plots measuring less than one acre each, although the entire project was slightly over one acre.

3. The Assessing Officer disallowed the deduction, treating each approval as a separate project extending less than one acre.

4. The case went through appeals, reaching the High Court.

Arguments:

Revenue's Arguments:

1. The project was developed on plots abutting two streets and should be considered separate projects.

2. The Assessee obtained separate approvals to circumvent Development Control Rules of CMDA.

Assessee's Arguments:

1. The project was a unified development on a site measuring over one acre.

2. Separate approvals were obtained only to take advantage of local Development Control Rules.

Key Legal Precedents:

1. TCA.No.257 of 2012: A Division Bench judgment that answered questions of law in favor of the Assessee.

2. TC(A) Nos.581 and 582 of 2011 and 314 and 315 of 2012: Earlier common judgment dated 01.11.2012 that ruled in favor of the Assessee.

Judgement:

The High Court dismissed the Revenue's appeal, confirming the order of the Income Tax Appellate Tribunal. The court held that:

1. The Assessee's project was a composite development on a site measuring over one acre.

2. Separate approvals were obtained only for the benefit of taking advantage of local Development Control Rules.

3. Previous judgments in similar cases had already ruled in favor of the Assessee.

4. No substantial questions of law arose for consideration in this appeal.

FAQs:

Q1: What is Section 80IB(10) (of Income Tax Act, 1961)?

A1: It's a provision that allows for tax deductions on profits derived from developing and building housing projects, subject to certain conditions.

Q2: Why did the Assessee obtain separate approvals for each plot?

A2: The Assessee obtained separate approvals to take advantage of the Development Control Rules of the local authority (CMDA).

Q3: Does the Assessee need to be involved in the construction to claim the deduction?

A3: No, the court clarified that for the purpose of deduction, the Assessee only needs to be the owner of the property, not necessarily involved in development and construction.

Q4: How did previous court decisions impact this case?

A4: Previous judgments in similar cases involving the same Assessee had already ruled in their favor, which strengthened the court's decision in this case.

Q5: What was the significance of the project being over one acre in total?

A5: The total area being over one acre was crucial in establishing that it was a unified project, despite having separate approvals for smaller plots.

(1)The Revenue is the appellant herein. Though the respondent / Assessee has been served and her name appears in the Cause List, there is no representation on her behalf.

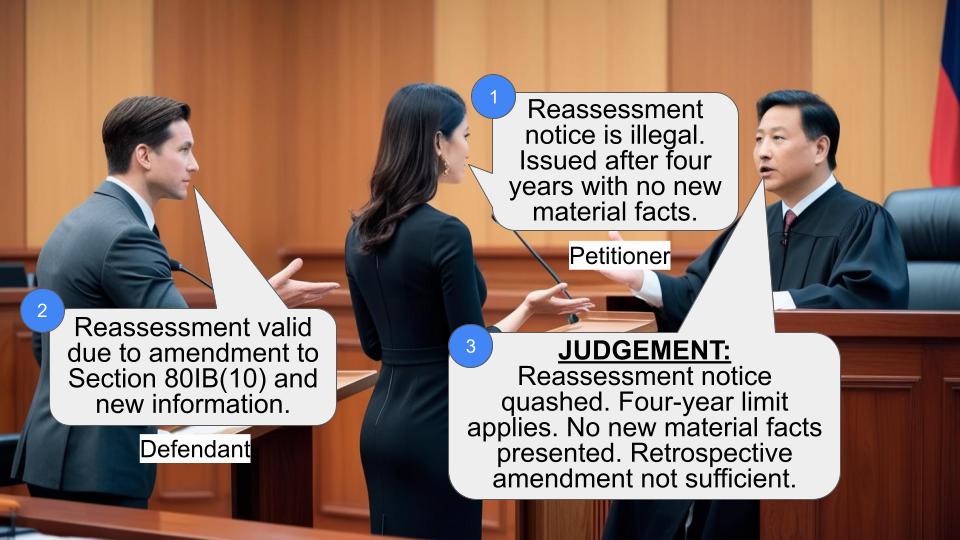

(2)The respondent/Assessee filed the Return of Income Tax for the Assessment Year 2007-08 on 29.09.2008, admitting the income of Rs.28,69,400/- after claiming deduction under Section 80IB (of Income Tax Act, 1961)[10] of the Income Tax Act, 1961, as amended from time to time, a sum of Rs.4,99,11,555/- and it was processed on 27.02.2010. The Assessing Officer, in the course of completing assessment for the Assessment Year 2009-10, noticed the fact that the Assessee did obtain plan for construction of the entire plot of measuring slightly over one acre, where blocks ranging from A to L were constructed. It was also noticed that each block of flat was constructed on a plot measuring less than one acre and therefore, the Assessing Officer held that the project was not an unified project in an extent of one acre and treated each approval as a separate project extending in an area less than one acre and therefore, not allowed the claim of deduction under the said Section. The Assessing Officer has also placed reliance upon the Board of Direct Taxes Instructions No.4 of 2009 dated 20.06.2009 and that apart, the deduction allowed in respect of earlier orders has to be withdrawn and therefore, a notice under Section 148 (of Income Tax Act, 1961), was issued on 01.03.2013 for the Assessment Year 2008-09.

(3)The Income Tax Officer, BW XV[1], Chennai, vide Assessment Order dated 08.03.2014, has concluded the assessment holding that similar view was taken for the year 2009-10, that is, each plan and approval is an independent project comprised in an area less than that specified in the Section and thus, not qualifying for the purported benefit of the deduction and accordingly, assessed the income at Rs.5,27,80,960/-.

(4)The Assessee, challenging the said order, filed an Appeal before the Commissioner of Income Tax [Appeals]-4, Chennai and the Appellate Authority, vide order dated 24.10.2016, found that the Assessing Officer was well within her jurisdiction in reopening the present case and therefore, confirmed the said action. The Appellate Authority, insofar as not allowing the deduction under Section 80-IB (of Income Tax Act, 1961)[10] of the Income Tax Act, 1961, found that in respect of the Assessment Year 2007-08, a Division Bench of this Court, in the judgment dated 12.11.2014 in Tax Case [Appeal] No.257 of 2012, filed by the Revenue, has considered the issues relating to the substantial questions of law 3 and 4 therein and found that the appeal filed by the Revenue lacks merit and accordingly, dismissed the appeal.

(5)The Commissioner of Income Tax [Appeals] had also considered the plea as to the development of composite project in the proposed site in S.Nos.486/1 and 482 and recorded a finding that at no point of time, the Assessee considered each plot as a separate project and it was considered as a single project and development was also on those lines. Thus, the Commissioner of Income Tax [Appeals], by taking into consideration, the facts and circumstances of the case, especially, the above cited judgment dated 12.11.2014 in TCA.No.257 of 2012, has allowed the appeal filed by the Assessee partly, vide order dated 24.10.2016.

(6)The Revenue, aggrieved by the same, filed a further appeal before the Income Tax Appellate Tribunal, [D Bench], at Chennai, [in short ''the ITAT''].

(7)The ITAT, vide order dated 20.11.2017, has taken note of the judgment in TCA.No.257 of 2012 and further found that the project of the assess was also in an area more than one acre and the approvals were obtained on unit basis only for the benefit of taking advantage of the Development Control Rules of the Local Authority, viz., the Chennai Metropolitan Development Authority [CMDA]. The ITAT, having recorded the said finding, found that the appeal filed by the Revenue is devoid of merits and insofar as the Assessee's Cross Objection is concerned, the ITAT, having found that it do not merit any consideration, had dismissed the appeal filed by the Revenue as well as the Cross Objection filed by the Assessee and challenging the legality of the dismissal of the appeal filed by the Revenue, the present Tax Case Appeal is filed.

(8)The appeal was admitted on the following substantial questions of law vide order dated 02.08.2018:-

1.Whether, claim of deduction u/s.80IB (of Income Tax Act, 1961)[10] is to be allowed even if there has been violation of condition of provisions of Section 80IB (of Income Tax Act, 1961)[10][c] since the area of two plots situated in two different streets, which the Assessee has considered as single project constituted an area of less than 1 acre each when considered individually?

2.Whether the Tribunal was right in allowing the claim of deduction under Section 80IB (of Income Tax Act, 1961)[10] especially, when the built up area of certain residential units exceeded the 1500 sq.ft. which was in violation of conditions specified in Section 80IB (of Income Tax Act, 1961)[10][c]?

(9)Mr.T.Ravikumar, learned counsel appearing for the appellant/Revenue would contend that the projects was developed in an area abutting two streets and therefore, it should be considered as separate projects and for the purpose of circumventing the Development Control Rules of CMDA, the project was developed separately and therefore, the Assessee was disentitled from availing the benefits of Section 80-IB (of Income Tax Act, 1961)[10] of the Income Tax Act, 1961 and also took a stand that challenging the legality of the judgment dated 12.11.2014 made in TCA.No.257 of 2012, the Revenue has preferred a Special Leave Petition before the Hon'ble Supreme Court of India and the same is pending and hence, prays for interference.

(10)This Court paid its best attention to the arguments advanced by the learned counsel for the appellant/Revenue and also carefully scrutinised the materials placed before it.

(11)In TCA.No.257 of 2012, the following substantial questions of law were raised:-

1.Whether on the facts and in the circumstances of the case, the Tribunal was right in holding that the assessee is entitled for deduction under Section 80IB (of Income Tax Act, 1961) when the assessee is not the owner of the property and had executed a contract with the purchasers of undivided share in the land to construct the building?

2.Whether on the facts and in the circumstances of the case, the Tribunal was right in holding that the completion certificate is not necessary in view of the letter dated 14.12.2009, issued by the Assistant Commissioner, Corporation, when the assessee itself had stated that the project is 'under construction in the form submitted to the Assessing Officer?

3.Whether on the facts and in the circumstances of the case, the Tribunal was right in holding that each of the unit of flats had a built up area of less than 1500 sq.ft., and is entitled to deduction under Section 80IB (of Income Tax Act, 1961)[10]?

4.Whether the assessee is entitled for deduction under Section 80IB (of Income Tax Act, 1961)[10] when the assessee had applied for sanction of building permission separately for each of the plots measuring less than 1 acre?

(12)The Division Bench, in the judgment dated 12.11.2014, in TCA.No.257 of 2012, had answered the questions of law and has taken note of the earlier common judgment dated 01.11.2012 made in TC[A] Nos.581 an 582 of 2011 and 314 and 315 of 2012, which came to be decided in favour of the Assessee, holding that for the purpose of considering deduction, it is not necessary that the Assessee, engaged in developing and construction of housing project and the only point is that he should be the owner of the property.

(13)It is also brought to the notice of this Court that so far, no challenge has been made to the common judgment dated 01.11.2012 in TCA.Nos.581 and 582 of 2011 and 314 and 315 of 2012.

(14)The ITAT, on facts also found that the Assessee has obtained approvals of the plan for the proposed projects and also planned the entire project regarding number of floors, number of apartments in each floor, cost of each apartment based on the square foot area of the apartment and it was done as a composite project at the proposed site in S.Nos.486/1 and 482.

(15)In the light of the factual findings coupled with the fact that the Assessee's own case, on the earlier occasions in TCA.Nos.581 & 582/2011 and 314 and 315/2012 vide common judgment dated 01.11.2012, was allowed and though a ground was raised before the ITAT as to the location of the plots in two different streets, but no arguments have been advanced, this Court is of the considered view that there are no substantial questions of law arise for consideration in this appeal.

(16)In the result, the Tax Case Appeal is dismissed, confirming the order of the Income Tax Appellate Tribunal dated 20.11.2017, made in ITA No.245/Mds/2017 relating to the Assessment Year 2008-09. No costs.

[M.S.N.,J] [A.Q., J]

02.03.2020

Internet : Yes

To

1.The Income Tax Appellate Tribunal ''D'' Bench, Chennai.

2.The Commissioner of Income Tax Chennai.

M.SATHYANARAYANAN, J.,

AND

ABDUL QUDDHOSE, J.,

TCA.No.377 of 2018

02.03.2020

×

Questions

Court Upholds Tax Deduction for Unified Housing Project Despite Multiple Plot Approvals

Write your CommentSimilar Posts

Generic

- Reportdata/6015.pdf