Court Upholds Tax Exemption for Software Company in Technology Park

Full News

Court Upholds Tax Exemption for Software Company in Technology Park

Court Upholds Tax Exemption for Software Company in Technology Park

This case involves an appeal by the Revenue (Income Tax Department) against Annik Technologies Ltd. regarding the company's eligibility for tax exemption under Section 10A (of Income Tax Act, 1961). The court dismissed the appeal, affirming the company's right to the tax benefit for its operations in a software technology park.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs. Annik Technologies Ltd. (High Court of Delhi)

ITA 122/2012

Date: 15th May 2012

Key Takeaways

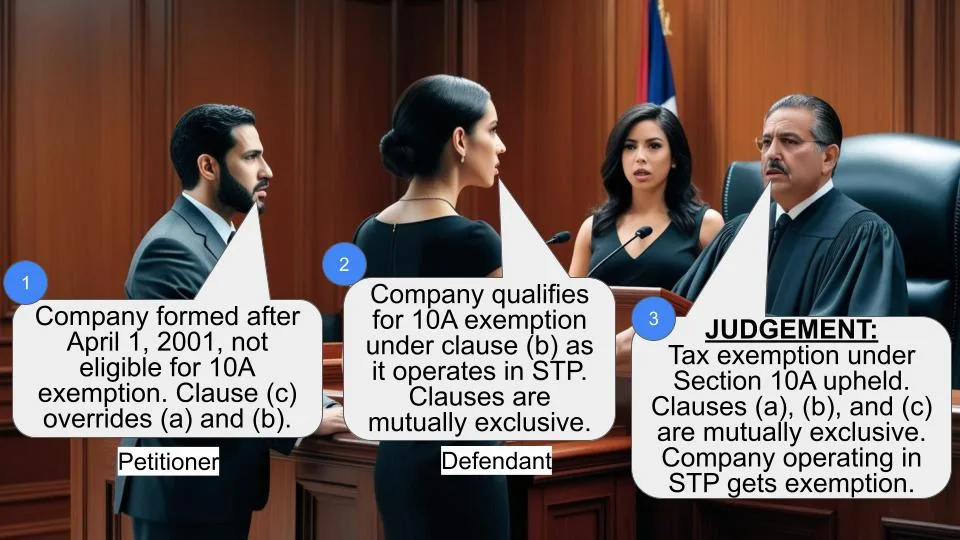

1. Clause (c) of Section 10A(2)(i) (of Income Tax Act, 1961) extends benefits to new undertakings without withdrawing benefits from those covered under clauses (a) and (b).

2. The three clauses of Section 10A(2)(i) (of Income Tax Act, 1961) are mutually exclusive and operate in their respective fields.

3. Companies operating in software technology parks can claim tax benefits under Section 10A(2)(i)(b) (of Income Tax Act, 1961), even if they were formed after April 1, 2001.

Issue

Is Annik Technologies Ltd. eligible for tax exemption under Section 10A (of Income Tax Act, 1961), despite being formed after April 1, 2001, and operating in a software technology park?

Facts

1. Annik Technologies was originally a partnership firm registered with the Directorate of Software Technologies Parks of India.

2. In September 2005, the entire business was transferred to Annik Technologies Ltd. (the respondent-company).

3. The company's name was substituted in the STP registration record.

4. The unit/undertaking of the respondent-assessee is located in a software technology park.

5. The case pertains to the assessment year 2007-08.

Arguments

Revenue's Arguments:

1. The respondent-assessee is not entitled to exemption under Section 10A (of Income Tax Act, 1961) because it was formed by splitting up or reconstruction of an existing business.

2. The company doesn't fulfill the conditions stipulated in clauses (a), (b), and (c) of Section 10A(2)(i) (of Income Tax Act, 1961).

3. Clause (c), applicable from April 1, 2001, overrides clauses (a) and (b).

Respondent's Arguments:

1. The company is covered under clause (b) of Section 10A(2)(i) (of Income Tax Act, 1961) as it operates in a software technology park.

2. The three clauses of Section 10A(2)(i) (of Income Tax Act, 1961) are mutually exclusive and operate in their own fields.

Key Legal Precedents

1. CBDT Circular No. 794 dated August 9, 2000, reported in (2000) 245 ITR (St.) 21: This circular clarifies that clause (c) extends the benefit to new undertakings in Special Economic Zones without withdrawing benefits available under clauses (a) and (b) .

Judgment

The court dismissed the appeal by the Revenue, ruling in favor of Annik Technologies Ltd. Key points of the judgment include:

1. The court rejected the Revenue's argument about Section 10A(2)(ii) (of Income Tax Act, 1961) violation, as it wasn't raised in the original grounds of appeal before the tribunal .

2. The court interpreted Section 10A(2)(i) (of Income Tax Act, 1961) to mean that clause (c) extends benefits without withdrawing those available under clauses (a) and (b) .

3. The three clauses of Section 10A(2)(i) (of Income Tax Act, 1961) were deemed mutually exclusive and operating in their own fields .

4. The court confirmed that Annik Technologies Ltd. is covered under clause (b) of Section 10A(2)(i) (of Income Tax Act, 1961) as it operates in a software technology park .

FAQs

Q1: What is Section 10A (of Income Tax Act, 1961) about?

A1: Section 10A (of Income Tax Act, 1961) provides special tax provisions for newly established undertakings in free trade zones, electronic hardware technology parks, software technology parks, and special economic zones .

Q2: Why was the Revenue's argument about Section 10A(2)(ii) (of Income Tax Act, 1961) rejected?

A2: The court rejected this argument because it wasn't raised in the original grounds of appeal before the tribunal. The court only considers issues that were properly raised in earlier proceedings .

Q3: How do the three clauses of Section 10A(2)(i) (of Income Tax Act, 1961) interact with each other?

A3: The court ruled that these clauses are mutually exclusive and operate in their own fields. Clause (c) extends benefits to new undertakings without affecting the benefits available under clauses (a) and (b) .

Q4: Does operating in a software technology park automatically qualify a company for tax benefits under Section 10A (of Income Tax Act, 1961)?

A4: While operating in a software technology park is a key criterion, companies must also meet other conditions specified in Section 10A (of Income Tax Act, 1961). In this case, the court found that Annik Technologies Ltd. met these conditions .

Q5: What impact does this judgment have on other companies in similar situations?

A5: This judgment clarifies that companies operating in software technology parks can claim tax benefits under Section 10A(2)(i)(b) (of Income Tax Act, 1961), even if they were formed after April 1, 2001. It reinforces the interpretation that the three clauses of Section 10A(2)(i) (of Income Tax Act, 1961) are independent and don't override each other.

1. This appeal by the Revenue under Section 260A (of Income Tax Act, 1961) impugns the order dated 28th July, 2011 passed by the Income Tax Appellate Tribunal (for short, the tribunal) in the case of Annik Technologies Pvt. Ltd. The appeal pertains to the assessment year 2007-08.

2. Learned counsel for the Revenue has raised two contentions before us. These have been dealt with separately.

3. It is submitted that the respondent-assessee is not entitled to exemption under Section 10A (of Income Tax Act, 1961), because it was formed by splitting up or reconstruction of business, which was already in existence. It is stated that Section 10A(2)(ii) (of Income Tax Act, 1961) has been violated. The aforesaid contention does not require adjudication in this appeal as this issue and contention was not raised by the Revenue in the grounds of appeal filed before the tribunal. Learned counsel for the respondent has produced before us the grounds of appeal filed and raised before the tribunal in which reference has been made to violation of Section 10A(2)(i)(a)(b) (of Income Tax Act, 1961) and (c) of the Act and no ground or contention was raised in respect of violation of Section 10A(2)(ii) (of Income Tax Act, 1961). The tribunal has not dealt with and examined the said contention. Therefore, on this aspect, no substantial question of law arises out of the impugned order dated 28th July, 2011.

4. The second contention raised by the learned counsel for the Revenue relates to interpretation of Section 10A(2)(i) (of Income Tax Act, 1961), which reads as under:-

10A. Special provision in respect of newly established undertakings in free trade zone, etc.?

(2) This section applies to any undertaking which fulfils all the following conditions, namely :?

(i) it has begun or begins to manufacture or produce articles or things or computer software during the previous year relevant to the assessment year?

(a) commencing on or after the 1st day of April, 1981, in any free trade zone ; or

(b) commencing on or after the 1st day of April, 1994, in any electronic hardware technology park or, as the case may be, software technology park ;

(c) commencing on or after the 1st day of April, 2001, in any special economic zone ;

5. In the grounds of appeal filed by the Revenue before the tribunal, it was contended that the respondent-assessee did not fulfill the conditions stipulated in clauses (a), (b) and (c) to Section 10A(2)(i) (of Income Tax Act, 1961). The grounds of appeal itself indicate that the respondent-assessee was entitled to benefit under Section 10A (of Income Tax Act, 1961) in case any of the clauses (a), (b) and (c) are applicable. What is contended and argued before us is that clause (c) applicable w.e.f. 1st April, 2001 had the effect of overriding clauses (a) and (b).

6. This is not correct as the CBDT had issued Circular No. 794 dated 9th August, 2000 reported in (2000) 245 ITR (St.) 21, in which in paragraph 5.4, it has been observed:-

?5.4 The conditions for the applicability of these provisions are that the undertaking:-

(a) Begins to manufacture or produce articles or things or computer software during the previous year relevant to the assessment year commencing on or after 1-4-1981 in any free trade zone or commencing on or after the first day of April, 1994 in any electronic hardware park or software technology park. The benefit has also been extended to new undertaking set up in any previous year relevant to an assessment year beginning on or after the first of April, 2001 in a Special Economic Zone.?

7. Thus, clause (c) extends the benefit and does not withdraw the benefit extended and available to undertakings covered by clauses (a) and (c). The three clauses are mutually exclusive and operate in their own field.

8. In the present case, STP registration was granted to the partnership firm-Annik Technologies by the Directorate of Software Technologies Parks of India. In September, 2005, pursuant to an agreement, the entire business was transferred to the respondent-company. The name of the respondent-company was substituted in the STP registration record. The unit/undertaking of the respondent-assessee is located in a software technology park and is accordingly covered by clause (b) to Section 10A(2)(i) (of Income Tax Act, 1961).

9. The appeal has no merit and the same is dismissed. No costs.

SANJIV KHANNA, J.

R.V.EASWAR, J.

MAY 15, 2012

×

Similar Ripples

Questions

Court Upholds Tax Exemption for Software Company in Technology Park

Write your CommentSimilar Posts

Generic

- Reportdata/5843.pdf