Court Upholds Tribunal's Decision, Rejects Revenue's Appeal on Income Tax Asses…

Full News

Court Upholds Tribunal's Decision, Rejects Revenue's Appeal on Income Tax Assessment

Court Upholds Tribunal's Decision, Rejects Revenue's Appeal on Income Tax Assessment

This case is about the Commissioner of Income Tax appealing against an order by the Income Tax Appellate Tribunal. The Tribunal had quashed a revision order made by the Commissioner under Section 263 (of Income Tax Act, 1961). The High Court dismissed the appeal, agreeing with the Tribunal that the Commissioner's use of Section 263 (of Income Tax Act, 1961) wasn't warranted in this case.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs. Narottam Mishra (High Court of Madhya Pradesh)

Income Tax Appeal No. 51 of 2015

Date: 3rd November 2016

Key Takeaways:

1. The court reinforced the principle that the Commissioner can't use Section 263 (of Income Tax Act, 1961) just because they disagree with the Assessing Officer's view.

2. For Section 263 (of Income Tax Act, 1961) to apply, an order must be both erroneous and prejudicial to the revenue's interests.

3. The court emphasized the importance of thorough investigation and proper appreciation of evidence by the Assessing Officer.

Issue:

Was the Income Tax Appellate Tribunal justified in quashing the Commissioner's order under Section 263 (of Income Tax Act, 1961)?

Facts:

1. The assessee (Narottam Mishra) filed a tax return for the assessment year in question on 28.07.2009.

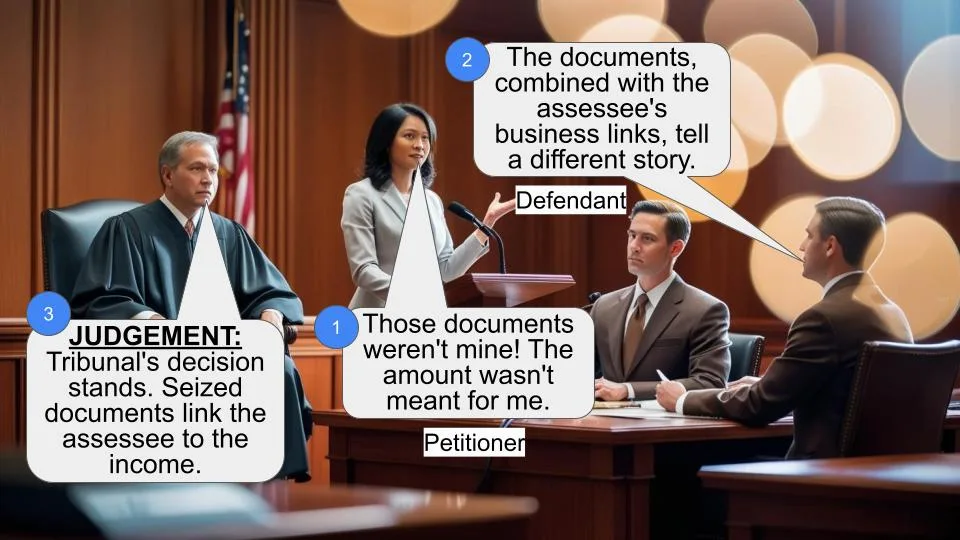

2. A search and seizure operation was conducted at the residence of one Shri Mukesh Sharma on 21.07.2008, where documents allegedly related to the assessee were found.

3. Based on these documents, the Assessing Officer made additions to the assessee's income.

4. The assessee appealed, and the CIT (Appeal) allowed the appeal on 12.12.2012.

5. The Commissioner then used Section 263 (of Income Tax Act, 1961) to revise the assessment, claiming the Assessing Officer's order was erroneous.

6. The assessee appealed to the Income Tax Appellate Tribunal, which quashed the Commissioner's order.

7. The revenue department then appealed to the High Court.

Arguments:

Revenue's side:

- The Assessing Officer's order was erroneous and prejudicial to the revenue's interests.

- The full amount received from certain companies should have been added to the assessee's income.

Assessee's side:

- The Assessing Officer had thoroughly investigated and made a reasoned decision.

- The Commissioner's revision under Section 263 (of Income Tax Act, 1961) wasn't justified as the order wasn't erroneous.

Key Legal Precedents:

1. Malabar Industrial Co. Ltd. vs. Commissioner of Income Tax (2000) 109 Taxman 66 (SC): This case defined when an order can be considered erroneous and prejudicial to revenue interests under Section 263 (of Income Tax Act, 1961).

2. Commissioner of Income Tax (Central) Ludhiana vs Max India Ltd. (2008) 166 Taxman 188 (SC): This case followed and clarified the Malabar Industrial Co. Ltd. judgment.

3. Commissioner of Income Tax vs. Shalimar Housing and Finance Ltd. (2010) 320 ITR 157 (M.P.): This case applied the principles from Malabar Industrial to a similar situation.

Judgement:

The High Court dismissed the revenue's appeal. They found that:

1. The Assessing Officer had thoroughly investigated and made a reasoned decision.

2. The Commissioner's use of Section 263 (of Income Tax Act, 1961) wasn't warranted as the Assessing Officer's order wasn't erroneous.

3. The Tribunal was correct in quashing the Commissioner's order.

FAQs:

1. Q: What is Section 263 (of Income Tax Act, 1961)?

A: It's a provision that allows the Commissioner to revise an Assessing Officer's order if it's erroneous and prejudicial to the revenue's interests.

2. Q: Can the Commissioner use Section 263 (of Income Tax Act, 1961) if they simply disagree with the Assessing Officer's view?

A: No, if two views are possible and the Assessing Officer has taken a reasonable view, the Commissioner can't use Section 263 (of Income Tax Act, 1961) just because they disagree.

3. Q: What does "erroneous and prejudicial to the interests of the revenue" mean?

A: It means the order must be both incorrect in law or fact AND cause a loss to the government's tax collection. Both conditions must be met for Section 263 (of Income Tax Act, 1961) to apply.

4. Q: Why did the court dismiss the revenue's appeal?

A: The court found that the Assessing Officer had made a thorough investigation and reached a reasonable conclusion. The Commissioner's disagreement alone wasn't enough to justify using Section 263 (of Income Tax Act, 1961).

1. This is revenue’s appeal under Section 260-A of the Income Act, 1961 challenging the order passed by the Income Tax Appellate Tribunal, Indore Bench, Indore on 25.11.2014.

2. While admitting the appeal on 10.02.2016 the following three questions were formulated for consideration.

“1. The purport of Section 263 (of Income Tax Act, 1961).

2. Whether there is perceptible distinction between the head “unaccounted income” and “unaccounted investment”, in accounting matters; and, if yes, whether the decision followed by the Appellate Tribunal applicable to head “unaccounted investment” can be the basis to hold that the Commissioner could not have exercised power under Section 263 (of Income Tax Act, 1961) in respect of inquiry relating to head “unaccounted income”.

3. Whether on the facts and in the circumstances of the case the ITAT was justified in law in quashing the order under Section 263 (of Income Tax Act, 1961) passed by the Commissioner of Income Tax, Bhopal when the Commissioner of Income Tax, Bhopal has rightly invoked the provisions of Section 263 (of Income Tax Act, 1961) only after examination of the record of assessment proceedings and after being fully satisfied that order passed by the A.O. is erroneous in so far as it is prejudicial to the interest of the Revenue and only after giving due opportunity to the Assessee of being heard and after making or causing to be made such inquiry as he deemed necessary.”

Respondent assessee filed a return for the assessment year in question on 28.07.2009 declaring a total income of Rs.3,55,440/- and an agricultural income of Rs.2,28,428/-. Prior to that on 21.07.2008, a search and seizure operation under Section 132 (of Income Tax Act, 1961) was conducted at the residence of one Shri Mukesh Sharma and certain documents were seized in the search and seizure purported to be relating to the present assessee. Based on these materials a detailed enquiry was carried out by the Assessing Officer and respondent/assessee was served with a specific questionnaire under Section 142(1) (of Income Tax Act, 1961). According to the revenue, these documents established receipt of certain amount by the assessee in his capacity as Minister of Urban Development and Administration, Government of Madhya Pradesh, from various companies to whom contracts were awarded. Based on the assessment undertaken, the Assessing Officer made an addition of Rs.14,24,60,600/- on account of proceeds said to have been received by the assessee through various channels from M/s. Nagarjuna Constructions Company Limited and similarly the Assessing Officer made an addition of Rs.1,53,41,000/- on account of proceed set to have been received through one Usman Khan, who said to have received the amount from another company M/s. Simplex Infrastructure Limited. Accordingly, these two additions were made to the income of the assessee and the assessment order Annexure A-1 passed on 30.12.2011.

3. Being aggrieved by this order of assessment, respondent assessee preferred an appeal before the CIT (Appeal) and the appellate authority vide order dated 12.12.2012 allowed the appeal, finding there to be an error in the order of assessment and by a detailed order held that the addition made are unsustainable. After the assessment was so finalized under Section 143(3) (of Income Tax Act, 1961), the Commissioner of Income Tax, Bhopal found that the Assessing Officer in his order has found receipt of income by the assessee to the tune of Rs.10,50,00,000/- from M/s. Simplex Infrastructure Ltd., but only made an addition of Rs.1,53,41,000/- instead of the entire amount of Rs.10,50,00,000/-. Similarly, the Commissioner found that in the matter of assessment of income said to have been received from M/s. Nagarjuna Constructions Company Ltd. against a receipt of Rs.16.02 crores an addition of only Rs.14,24,60,600/- was made. Holding that this amounts to erroneous assessment, prejudicial to the interest of revenue, notice under Section 263(1) (of Income Tax Act, 1961) was issued. Reply of the assessee being found to be unsatisfactorily, orders were passed by the Commissioner of Income Tax on 31.12.2012 vide Annexure A-3 and challenging this exercise of power under Section 263 (of Income Tax Act, 1961) by the Income Tax Commissioner, an appeal was filed by the respondent, assessee before the Income Tax Appellate Tribunal and vide order dated 25.11.2014 annexure A-4 the tribunal having allowed the appeal, this appeal under Section 260-A (of Income Tax Act, 1961) by the revenue.

4. The Commissioner appeal while exercising his jurisdiction of revision under Section 263 (of Income Tax Act, 1961) analyzed the entire order of assessment and came to the conclusion that, if the income received by the assessee from M/s. Nagarjuna Constructions Company Ltd. comes to Rs.16.02 crores and from M/s. Simplex Infrastructure Ltd. to Rs.10.50 crores then addition of only Rs.14,24,60,600/- and Rs.1,53,41,000/- was not proper, it amounts to erroneous assessment and, therefore, exercised jurisdiction under Section 263 (of Income Tax Act, 1961) and remanded the matter back to the Assessing Officer. However, while doing so, the Commissioner appeals failed to consider various aspects of the matter dealt with by both the Assessing Officer in its order of assessment and by the appellate authority in its order dated 12.12.2012, the Assessing officer while undertaking the appraisal of evidence took note of various documents and evidence that came on record, classified them as primary evidence and corroborative evidence and made the additions of Rs.14,24,60,600/- and 1,53,41,000/- respectively. The additions were made by the Assessing Officer because the primary evidence available were corroborated by certain other evidence i.e. no.1 to 6 and justified only an addition of Rs.14,24,60,600/-, similarly the primary evidence 1 to 5 read along with corroborative evidence No.7 justified an addition of Rs.1,53,41,000/- only, thereafter while dealing with the matter in its order dated 12.12.2012 the appellate authority went through various aspects of the matter and found that the legal position in the matter of making assessment based on the material available is well settled. The appellate authority found that the observations with regard to proceeds received from M/s. Nagarjuna Constructions Company Ltd. and M/s. Simplex Infrastructure Ltd. were based on inference only and not on direct or cogent evidence demonstrating the assessee’s nexus with the payment or investment. The alphabet “M” and the letter “Netaji” referred to in loose paper have been taken as basis to link them with the assessee. The Appellate Authority in its order dated 12.12.2012 found that this may refer to any class of person i.e. any Minister or Politician and there is no legal or admissible evidence to confirm that they refers to the assessee. Inference drawn by the Assessing Officer has been held to be based on the assumption that Shri Mukesh Sharma enjoyed substantial influence in the Urban Development Department. Various aspects have been examined by the appellate authority while dealing with the matter on 12.12.2012 and it was found that conclusion and inference drawn are not based on proper appreciation of the evidence, but are based on surmises, suspicion and conjecture. It was held by the appellate authority in its order passed on 12.12.2012 that the loose papers that were found from premises of Shri Mukesh Sharma were not in the handwriting of appellant assessee, the intermediaries in whose account the money was transferred did not belong to the appellant and an inference has drawn that appellant is recipient of the income only because the persons in whose account the amount was transferred were resident of ‘Dabra’, the constituency of the assessee. The appellate authority found that in order to hold a person as Benamidar of another person, it needs to be established that the latter is the ultimate beneficiary and was enjoining the fruits of transaction. It was held that this fundamental requirement of enjoying the fruits by someone other than the ostensible owner is missing. In this case it was after analyzing all these aspects of the matter in detail that the learned appellate authority interfered into the matter and now power is sought to be exercised under Section 263 (of Income Tax Act, 1961) to say that the assessing officer has committed an error in not adding the entire amount of income received and, therefore, an error is committed.

5. The appellate tribunal in para 5.1 and 5.2 records its finding with regard to the matter particularly with regard to the consideration made by the Assessing Officer in the following manner, which reads as under:

“5.1 On the basis of the portion reproduced from the assessment order it is evident that the AO was conscious about the importance of the evidences hence considering those evidences he has held that a sum of Rs.14,24,60,600/- was required to be added in the hands of the assessee on account of proceeds received from Nagarjuna Construction Company through a channel of persons. Likewise also he has held that a sum of Rs.1,53,41,000/- is required to be added on account of proceeds found in the possession of Shri Usman Khan alleged to be the proceeds received from Simplex Infrastructure Ltd. used for the purchase of property

5.2 If the AO has examined all those evidence from all angles that too after thorough investigation; as also after applying his mind; and came to the conclusion that a particular amount, in this case it was a substantial amount, was to be taxed in a particular manner in the hand of the assessee then in our humble opinion the said approach of the AO should not be held, a faulted approach specially to the extent of quashing the entire assessment order. We have noted that Ld. CIT has invoked the provisions of Section 263 (of Income Tax Act, 1961) mainly for the reason that the investigation was not properly conducted by the AO. But considering the facts of this case this allegation is not appreciable because there is a limit of an investigation. There should be a justifiable investigation. Side by side there should be a limit for a reasonable investigation. Otherwise also, the line of investigation depends upon the investigating authority and it may differ from officer to officer. There is no particular standard or line of direction prescribed for an investigation, therefore; if the investigation is reasonable through which a proper result can be achieved, then such an investigation can be termed as a reasonable or a thorough investigation. From the contents of the order passed u/s. 263 (of Income Tax Act, 1961), relevant portion already reproduced (supra), it appears that the Ld. CIT wants reinvestigation of the entire matter. But such a fishing or rowing inquiries have never been encouraged by the Hon’ble Courts. In the likewise manner, we are also of the view that Ld. CIT was not correct in asking the AO to conduct inquiries afresh on the basis of those from seized documents which were already appreciated during the assessment proceedings. Even this is not the case of Ld. CIT that certain evidences were overlooked which were very much on record or in the knowledge of the AO. Even this is not the case of Ld. CIT that certain new facts or evidences were brought to the notice of the Revenue Department which were having the direct impact on the income assessed by the AO. Neither there was an escapement of evidence nor there was any evidence now brought to the notice of the revenue department, therefore, if that was not the position, then we are not inclined to give our approval to such directions.”

and thereafter took note of the detailed order passed by the CIT Appeal on 12.12.2012 as we have indicated hereinabove and held that in this case exercise of jurisdiction under Section 263 (of Income Tax Act, 1961) was not warranted.

6. Having heard the submissions made by Shri Sanjay Lal, counsel for the revenue and Shri Sumit Nema, counsel for the respondent at length, we find after going through the records that the entire proceedings impugned for addition of the amount were based on the documents seized from the premises of Shri Mukesh Sharma. It has been found that these documents were not in the handwriting of the appellant, the accounts on which the amount were transferred did not belong to the assessee, only because the intermediaries in whose name benefit were transferred belonged to ‘Dabra’ an inference is drawn that they are benamidars of appellant, but while doing so, the principle of law discussed and upheld by the Commissioner appeals were not taken note of. Infact, this is a case where the assessing officer and the appellate authority when it dealt with the matter at the first instance on 12.12.2012 conducted proper proceedings and arrived at a conclusion based on cogent reasons that have been placed on record.

7. The import and meaning of Section 263 (of Income Tax Act, 1961) and the powers of revision available to a statutory authority under this Section has been discussed in detail by the Supreme Court in the case of Malabar Industrial Co. Ltd. vs. Commissioner of Income Tax (2000) 109 Taxman 66 (SC), it has been held by the Hon’ble Supreme Court that the pre-requisite for exercise of jurisdiction by the Commissioner, suo motu under this Section is that the order of the Income Tax Officer is erroneous in so far as it is prejudicial to the interest of the revenue. It is held that the twin conditions namely; (i) that the order of the Assessing Officer sought to be reviewed is erroneous and (ii) it is prejudicial to the interest of the revenue must exists together. If one of them is absent i.e. if the order of ITO is erroneous, but not prejudicial to the interest of revenue or if it is not erroneous but only prejudicial to the interest of revenue,recourse cannot be held to Section 263(1) (of Income Tax Act, 1961). It has been held in the aforesaid case by the Supreme Court that there can be no doubt that the provisions cannot be invoked to correct each and every type of mistake or error committed by the Assessing Officer. It is only when an order is erroneous that the section will be attracted and an incorrect assumption of fact or an incorrect application of law will satisfy the requirement of the order being erroneous. Various aspects of the matter has been considered, the phrase ‘prejudicial to the interests of the revenue’ is also considered and finally it has been held by the Supreme Court in the aforesaid case, that :

“The phrase ‘prejudicial to the interest of the revenue’ has to be read in conjunction with an erroneous order passed by the Assessing Officer. Every loss of revenue as a consequence of an order of the Assessing Officer cannot be treated as prejudicial to the interests of the revenue, for example, when an ITO adopts one of the courses permissible in law and it has resulted in loss of revenue; or where two views are possible and the ITO has taken one view with which the Commissioner does not agree, it cannot be treated as an erroneous order prejudicial to the interest of the revenue unless the view taken by the ITO is unsustainable in law. It has been held by the Supreme Court that where a sum not earned by a person is assessed as income in his hands on his so offering, the order passed by the Assessing Officer accepting the same as such will be erroneous and prejudicial to the interest of the revenue.”

8. It is clear from the aforesaid that if two views are possible and if the Assessing Officer has taken a view with which the commissioner does not agree, it cannot be treated as erroneous order, prejudicial to the interest of revenue. In this case also the Assessing Officer appreciated the entire aspect and came to one conclusion and merely because a different view was possible the exercise of power under Section 263 (of Income Tax Act, 1961) could not be made. The appellate tribunal has considered all these aspects of the matter and it is only after applying the law in the case of Malabar (supra) that the appeal has been allowed. This judgment of the Supreme Court in the case of Malabar Industrial (supra) has been followed in the case of Commissioner of Income Tax (Central) Ludhiana vs Max India Ltd. (2008) 166 Taxman 188 (SC) and in para 2 the following principles have been crystalized :

“At this stage we may clarify that under para 10 of the judgment in the case of Malabar Industrial Co. Ltd. (supra) this court has taken the view that the phrase ‘prejudicial to the interest of the revenue’ under Section 263 (of Income Tax Act, 1961) has to be read in conjunction with the expression “erroneous” order passed by the Assessing Officer. Every loss of revenue as a consequence of an order of the Assessing Officer cannot be treated as prejudicial to the interest of the revenue. For example, when the income-tax Officer adopted one of the courses permissible in law and it has resulted in loss of revenue; or where two views are possible and the Income tax Officer has taken one view with which the Commissioner does not agree, it cannot be treated as an erroneous order prejudicial to the interest of the revenue, unless the view taken by the Income Tax Officer is unsustainable in law.”

(Emphasis Supplied)

9. A Division Bench of this Court has followed the principle laid down in the case of Malabar Industrial (supra) and followed this principle in the case of Commissioner of Income Tax vs. Shalimar Housing and Finance Ltd. (2010) 320 ITR 157 (M.P.) and the tribunal after taking note of all these factors has found that exercise of power under Section 263 (of Income Tax Act, 1961) was not warranted in the present case and, therefore, the CIT’s revision order was quashed, we find no error in the same warranting reconsideration as we are also of the considered view that the exercise of power by the Commissioner under Section 263 (of Income Tax Act, 1961) was not proper.

10. In this case, if we go through a detailed order passed by the Commissioner Appeal exercising its power of revision on 31.12.2012 we find that the only reason given to hold the order of the Assessing Officer to be erroneous and prejudicial to the interest of revenue is that once the amount of proceed received from M/s. Nagarjuna Construction Company Ltd. and M/s. Simplex Infrastructure Ltd. is found to be 16.02 crores and 10.50 crores, then making an addition to the tune of only Rs.14,24,60,600/- and 1,53,41,000/- is not proper. This is the only reason for holding the order of the Assessing Officer to be erroneous. However while doing so, the authority namely the Commissioner of Income Tax exercising jurisdiction under Section 263 (of Income Tax Act, 1961) lost sight of the fact that the learned Assessing Officer in detail had gone into this aspect of the matter and has recorded a specific finding to say that appreciating the primary evidence from No.1 to 9 along with corroborative evidence 1 to 6 an addition of only Rs.14,24,60,600/- can be made and similarly by considering primary evidence 1 to 5 along with corroborated evidence no. 7 an addition of Rs.1,53,41,000/- only permissible, thus on a due analyses of the evidence, assessing officer arrived at a particular conclusion and if this is one of the views possible based on evidence that were appreciated by the Assessing Officer, merely because a different view was possible interference under section 263 (of Income Tax Act, 1961) on this count could not be made. Thereafter this addition is also analyzed by the appellate authority in detail while passing the order originally on 12.12.2012 and this addition is also found to be unsustainable for reasons as have been indicated in the said order and which is considered by us in the preceding paragraph.

11. Merely because in a given set of circumstances two different opinions can be formed, it is not appropriate to interfere with one of the opinion expressed until and unless the opinion is found to be perverse or based on no evidence or material. If this principle is applied to the present case, we find that the tribunal has not committed any error, it was a case where the exercise of jurisdiction under Section 263 (of Income Tax Act, 1961) by the Commissioner being unsustainable, the tribunal has rightly interfered into the matter, in view of the interpretation to Section 263 (of Income Tax Act, 1961) made by the Supreme Court, as detailed hereinabove, interference made by the Commissioner Appeal being unsustainable, we answer question No.1 and 3 by holding that the exercise of power under Section 263 (of Income Tax Act, 1961) by the appellate authority namely the Commissioner Appeal while passing the appellate order on 31.12.2012 was not proper and by interfering in a proceeding under Section 263 (of Income Tax Act, 1961) an error has been committed and if the tribunal has interfered on same, no illegality is committed by the tribunal. Once we hold that the exercise of power under Section 263 (of Income Tax Act, 1961) by the commissioner while passing order on 31.12.2012 was not warranted we have to dismiss this appeal and the other questions, i.e. question No.2 formulated need not to be gone into.

12. We accordingly hold that the power exercised by the Commissioner under Section 263 (of Income Tax Act, 1961) being unsustainable, the appeal is liable to be and is accordingly dismissed.

No order as to costs.

(RAJENDRA MENON) (Smt. ANJULI PALO)

ACTING CHIEF JUSTICE JUDGE

×

Similar Ripples

Questions

Court Upholds Tribunal's Decision, Rejects Revenue's Appeal on Income Tax Assessment

Write your CommentSimilar Posts

Generic

- Reportdata/HC-MP-51-2015.pdf