Full News

Court upholds Tribunal's order on rental value assessment, allowing AO flexibility in determination

Court upholds Tribunal's order on rental value assessment, allowing AO flexibility in determination

The case involves Madras Application Software Development Export Company Private Limited appealing against the Income Tax Appellate Tribunal's order regarding the assessment of rental income from a property leased to a subsidiary. The High Court dismissed the appeal, affirming the Tribunal's decision to allow the Assessing Officer (AO) flexibility in determining the fair rental value.

For a comprehensive understanding, check out the original judgement of the court order here."

Case Name:

Madras Application Software Development Export Company Private Limited Vs Assistant Missioner of Income Tax (High Court of Madras)

Tax Case Appeal Nos.727, 728, 729 and 730 of 2016 and C.M.P.Nos. 16058, 16059, 16060, 16061, 16062, 16063 and 16064 of 2016

Key Takeaways

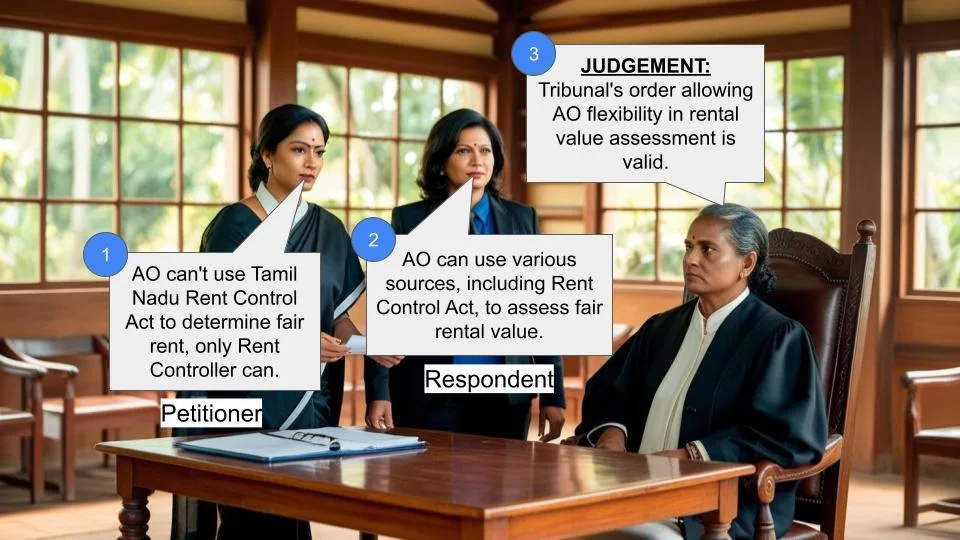

1. The court upheld the Tribunal's order, finding no legal infirmity.

2. The AO is allowed to use various sources, including state government and municipal corporation data, to determine fair rental value.

3. The Tribunal's reference to the Tamil Nadu Buildings (Lease and Rent Control) Act, 1960 for guidance in determining fair rent was deemed appropriate.

4. The Valuation Officer mentioned in the Tribunal's order is clarified to be the one appointed under the Income Tax Act.

Issue

Was the Income Tax Appellate Tribunal's order directing the Assessing Officer to determine the fair rental value of the property using various methods, including guidance from the Tamil Nadu Buildings (Lease and Rent Control) Act, 1960, legally valid?

Facts

1. The Assessee leased a property to a subsidiary company for Rs.7,500 per month.

2. The AO initially estimated the annual rental value at Rs.1,90,240.

3. After appeals and reassessment, the AO fixed the rental value at Rs.1,00,000 per month.

4. The Commissioner of Income Tax (Appeals) partly allowed the appeal, setting the annual rental income at Rs.3,00,000.

5. The Income Tax Appellate Tribunal set aside previous orders and directed the AO to examine the issue considering the Tamil Nadu Buildings (Lease and Rent Control) Act, 1960.

Arguments

The Assessee argued against the Tribunal's direction to use the Tamil Nadu Buildings (Lease and Rent Control) Act, 1960 for determining fair rent, stating that fair rent can only be fixed by the Rent Controller upon application under the Act.

Key Legal Precedents

No specific legal precedents were cited in the judgment.

Judgement

1. The High Court dismissed the Tax Case Appeals, finding no merit in them.

2. The court found no legal infirmity in the Tribunal's order.

3. The court clarified that the AO can seek information from the State Government or local Municipal Corporation regarding rental values of similar properties.

4. The Valuation Officer mentioned in the Tribunal's order was clarified to be the one appointed under the Income Tax Act.

FAQs

Q1: What was the main issue in this case?

A1: The main issue was the determination of fair rental value for a property leased by the Assessee to its subsidiary.

Q2: Why did the court uphold the Tribunal's order?

A2: The court found no legal infirmity in the Tribunal's order and deemed it appropriate to allow the AO flexibility in determining the fair rental value.

Q3: Can the Assessing Officer use the Tamil Nadu Buildings (Lease and Rent Control) Act, 1960 to determine fair rent?

A3: Yes, the court affirmed that the AO can use the Act as guidance for determining fair rent, even though it's not binding.

Q4: Who is the Valuation Officer mentioned in the judgment?

A4: The court clarified that the Valuation Officer is the one appointed under the Income Tax Act

Q5: What options does the Assessing Officer have in determining the fair rental value?

A5: The AO can seek information from the State Government, local Municipal Corporation, and obtain assistance from the Valuation Officer appointed under the Income Tax Act.

1. These Tax Case Appeals have been preferred by the Assessee under Section 260A (of Income Tax Act, 1961) mounting a challenge to the common order passed by the Income Tax Appellate Tribunal 'A' Bench, Chennai, in ITA No.139/Mds/2016, 140/Mds/2016, 141/Mds/2016, 142/Mds/2016 dated 22.04.2016, for Assessment years 2002-03, 2004-05, 2005-06 and 2006-07.

2. Since common issue arises for consideration in all these Appeals arising out of the common order passed by the Tribunal, conveniently, they can be dealt with by a common judgment.

3. The Assessee has let out a house property to one of its subsidiary companies on a monthly rent of Rs.7500/-. Initially the Assessing Officer has estimated its annual rental value at Rs.1,90,240/-. The matter was carried in appeal and the Commissioner of Income Tax (Appeals) allowed the appeal and remanded the matter back for consideration afresh. Thereafter, the matter once again was considered and based upon the report submitted by the Inspector of Income Tax who Conducted enquiries, the rental value has been fixed at Rs.1,00,000/- per month and after allowing deductions towards Municipal Tax and 30% towards repairs, the annual income has been assessed as Rs.8,32,728/-. The Assessment Order was passed on 17.12.2007. Aggrieved by that order of assessment, the Assessee preferred an appeal to the Commissioner of Income Tax (Appeals).

4. The Commissioner of Income Tax (Appeals) by an order dated 30.10.2015, has partly allowed the appeal as the Assessee is agreeable to an estimation of Rs.2,37,804/-. Based on the estimation made, the Commissioner of Income Tax (Appeals) has arrived at the annual rental income at Rs.3,00,000/- as reasonable and hence directed the Assessing Officer to adopt the said amount of Rs.3,00,000/- as the rental income of the Assessee for the Assessment Year 2002-03. Not satisfied with this order, the Assessee went before the Income Tax Appellate Tribunal by way of further appeal, which by its impugned order dated 22.04.2016, while setting aside the orders of both the Assessing Officer and the Appellate Authority, directed the Assessing Officer to examine the issue in the light of the provisions of the Tamil Nadu Buildings (Lease and Rent Control) Act, 1960 and estimated the annual rental income for the assessment year 2002-03 and thereafter the rent of the building so determined may be increased by 15% for every block of 3 years period. The Tribunal has given liberty to the Assessing Officer to refer the matter to the Valuation Officer to ascertain the rent of the building after applying the provisions of Tamil Nadu Buildings (Lease and Rent Control) Act, 1960.

5. Heard Mr.V.S.Jayakumar, learned counsel for the Appellant and Mr.T.R.Senthilkumar, learned Standing Counsel accepts notice on behalf of the Income Tax Department.

6. The undisputed fact is that an independent house with a built up area of 2584 sq. ft. in the ground floor and 1564 sq. ft. in the first floor situate on the land of 4 grounds and 210 sq. ft. was purchased by the Assessee and this property is situate at Crescent Street, Arch Bishop Mathias Avenue, Raja Annamalaipuram, in the city of Chennai, where the rental values are fairly high. Though a statement is made that the entire building has not been let out, we are not going into that issue inasmuch as the Assessee is at liberty to place the factual data relating to the extent of the building that has been leased out, before the Assessing Officer. But however, what the Tribunal has done now is to direct the Assessing Officer to take into account and consideration the provisions contained in the Tamil Nadu Buildings (Lease and Rent Control Act), 1960. That was objected to now.

7. The Rent Control Act contains certain provisions with regard to the reasonable method to determine the 'fair rent' payable by a tenant. Though a criticism has been mounted that fair rent can be fixed by the Rent Controller only upon an application made there under the provisions of the said Act, but however, we are not so much concerned with the issue of fixation of fair rent under the Rent Control Act in the present case. The formula contained for fixation of fair rent under the Rent Control Act is, what is now directed to be 'adopted' for the purpose of arriving at a reasonable rental value the property leased out by the assessee would fetch. Instead of leaving any discretion in the hands of the Assessing Officer in working out, all that the Tribunal did was to direct the Assessing Officer to get guided by the principles contained in the Rent Control Act in the matter of fixation of fair rent.

8. We do not find any legal infirmity in the order passed by the Tribunal warranting our interference. All that we need to clarify is that the Assessing Officer is at liberty to ascertain either from the State Government or from the local Municipal Corporation if there is any attempt made by them in the matter of fixation of rental values for similar accommodations in and around Raja Annamalaipuram, as the one which was leased out by the Assessee as a matter of guidance. Similarly, the Tribunal has also directed the Assessing Officer, to obtain the assistance of the Valuation Officer. We clarify that the Valuation Officer referred to by the Tribunal is the one who is obviously appointed as such under the Income Tax Act.

NOOTY. RAMAMOHANA RAO, J

AND

DR. ANITA SUMANTH, J

9. We find no merit in these Tax Case Appeals and accordingly, they stand dismissed. Consequently, C.M.P.Nos. 16058, 16059, 16060, 16061, 16062, 16063 and 16064 of 2016 are also dismissed.

(N.R.R.,J) (A.S.M., J) 24.10.2016

T.C.A.Nos.727 to 730 of 2016

×

Similar Ripples

Questions

Court upholds Tribunal's order on rental value assessment, allowing AO flexibility in determination

Write your CommentSimilar Posts

Generic

- Reportdata/11469-HC.pdf