Court Upholds Validity of Post-Assessment Satisfaction Note in Tax Case

Full News

Court Upholds Validity of Post-Assessment Satisfaction Note in Tax Case

Court Upholds Validity of Post-Assessment Satisfaction Note in Tax Case

This case involves an appeal by the Income Tax Department against a decision of the Income Tax Appellate Tribunal. The main issue was the timing of recording a "satisfaction note" under Section 158BD (of Income Tax Act, 1961). The High Court ruled in favor of the Revenue, overturning the Tribunal's decision and remitting the case back for consideration on merits.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs N. Ramakrishnan(High Court of Karnataka)

ITA No.234 of 2011

Date: 18th May 2020

Key Takeaways:

1. A satisfaction note under Section 158BD (of Income Tax Act, 1961) can be prepared even after completing assessment proceedings under Section 158BC (of Income Tax Act, 1961).

2. The Supreme Court's decision in CIT vs. CALCUTTA KNITWEARS is crucial in determining the timing of satisfaction notes.

3. The Tribunal's decision was overturned as it contradicted the Supreme Court's ruling.

Issue:

Is an assessment order under Section 158BD (of Income Tax Act, 1961) read with Section 158BC (of Income Tax Act, 1961) valid if the assessing officer records satisfaction after completing the block assessment proceedings under Section 158BC (of Income Tax Act, 1961)?

Facts:

1. A search was conducted at the residence of Mr. Syed Farahatullah, a partner of M/s Domicile Developers.

2. A memorandum of understanding between Farahatullah and N. Ramakrishnan for a land purchase was seized.

3. A survey at N. Ramakrishnan's premises revealed an undisclosed property sale to Akram Khan.

4. Notice under Section 158BD (of Income Tax Act, 1961) read with Section 158BC (of Income Tax Act, 1961) was issued to N. Ramakrishnan on 09.07.2003.

5. The Assessing Officer determined a tax liability on capital gains, which was upheld by the Commissioner of Income Tax (Appeals).

6. The Income Tax Appellate Tribunal quashed the assessment order, deeming it void ab initio.

Arguments:

Revenue's Argument:

- The satisfaction was recorded after completing proceedings under Section 158BC (of Income Tax Act, 1961) for Javed (Farahatullah).

- The Tribunal's decision to allow the appeal solely based on the timing of satisfaction recording was contrary to law.

Respondent's Argument:

- Not available as the respondent didn't appear despite notice.

Key Legal Precedents:

1. CIT vs. CALCUTTA KNITWEARS (2014) 362 ITR 673 (SC): This Supreme Court decision is crucial to the case. It held that a satisfaction note under Section 158BD (of Income Tax Act, 1961) could be prepared at various stages, including immediately after completing assessment proceedings under Section 158BC (of Income Tax Act, 1961).

Judgement:

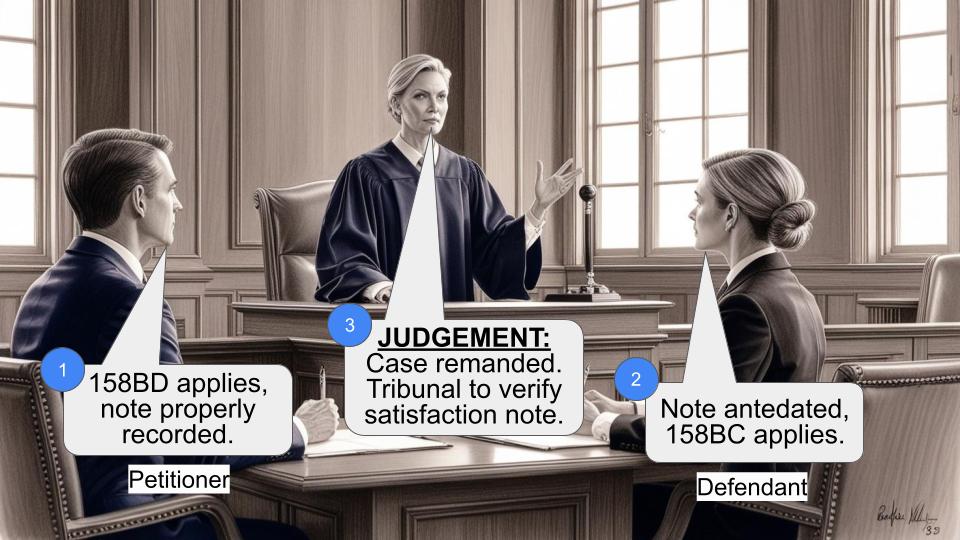

1. The High Court ruled in favor of the Revenue.

2. It held that the Tribunal's decision was contrary to the Supreme Court's ruling in CALCUTTA KNITWEARS.

3. The Court quashed the Tribunal's order and remitted the matter back to the Tribunal for consideration on merits.

FAQs:

1. Q: What is a "satisfaction note" in this context?

A: A satisfaction note is a document prepared by the Assessing Officer indicating their belief that undisclosed income belongs to a person other than the one searched.

2. Q: Why was the timing of the satisfaction note important?

A: The timing was crucial because it determined the validity of the assessment order under Section 158BD (of Income Tax Act, 1961).

3. Q: What did the Supreme Court say about the timing of satisfaction notes?

A: In the CALCUTTA KNITWEARS case, the Supreme Court held that satisfaction notes could be prepared even after completing assessment proceedings under Section 158BC (of Income Tax Act, 1961).

4. Q: What's the significance of this judgment?

A: It clarifies that assessment orders aren't automatically void if satisfaction is recorded after completing proceedings under Section 158BC (of Income Tax Act, 1961), aligning with the Supreme Court's interpretation.

5. Q: What happens next in this case?

A: The case goes back to the Income Tax Appellate Tribunal for consideration on its merits, rather than being dismissed on procedural grounds.

1. This appeal under Section 260A (of Income Tax Act, 1961) (hereinafter referred to as ‘the Act’) has been filed by the revenue. The subject matter of this appeal pertains to block period from 01.04.1981 to 29.05.2001.

The Appeal was admitted by a bench of this Court by an order dated 17.10.2019 on the following substantial question of law:

(i) Whether the Tribunal is justified in law on the facts and in the circumstances of the case in holding that the assessment order passed under Section 148BD (of Income Tax Act, 1961) read with Section 158BC (of Income Tax Act, 1961) is not valid and is void ab initio on the ground that the assessing officer of the person searched has not recorded satisfaction before the completion of block assessment proceedings under Section 158BC (of Income Tax Act, 1961) relying upon the decision of the Apex Court in case of Manish Maheswari (289 ITR 341) without appreciating the fact that the assessing officer in the case of the person searched as the assessing officer who initiated proceedings under Section 158BD (of Income Tax Act, 1961) in the case of the respondent – assessee is the same person and also that satisfaction was

recorded in the case of the respondent- assessee before the issue of notice

under Section 158BD (of Income Tax Act, 1961)?

2. Facts leading to filing of this appeal briefly stated

are that a search under Section 132 (of Income Tax Act, 1961) was carried

out in the residence of Mr.Syed Farahatullah alias Javed,

one of the partners of M/s Domicile Developers. During the

course of the search, a memorandum of understanding

entered by him with one Ramakrishnan for purchase of land

measuring 1 acre 11 guntas forming part of Sy.No.56/17,

Hongasandra Village, Begur Hobli, Bangalore South was

seized. As per memorandum of understanding dated

29.05.1995, total sale consideration was fixed at

Rs.1,92,00,000/- and out of the aforesaid amount, a sum of

Rs.1,12,00,000/- was paid to aforesaid N.Ramakrishnan the

payment of which was duly acknowledged. Thereafter, a

survey was conducted in the premises of N.Ramakrishnan

on 15.06.2001 and certain documents were impounded.

The impounded documents revealed that property was sold

to one Akram Khan and as per agreement dated

04.12.1998, total sale consideration was Rs.2,12,00,000/-,

out of which an amount of Rs.1,83,00,000/- was already

paid to Mr.N.Ramakrishnan. Mr.N.Ramakrishnan did not

disclose this transaction to the Income Tax department.

3. In order to bring the aforesaid amount to tax,

notice under Section 158BD (of Income Tax Act, 1961) read with Section 158BC (of Income Tax Act, 1961) of the

Act was issued on 09.07.2003 which was served on the

assessee on 14.07.2003. The assessee filed the return of

income for the block period on 06.11.2003 declaring

undisclosed income as ‘NIL’. The assessing officer by an

order dated 29.07.2005 inter alia held that assessee had

entered into an agreement for sale of the property in

question and had received the entire sale consideration as

on the date of the agreement and handed over the

possession. Therefore, the transfer of property had taken

place within the meaning of Section 2(47)(v) (of Income Tax Act, 1961) and

the capital gains arising out of transfer is chargeable to tax

for the block period. Accordingly, the Assessing Officer held

that a net sum of Rs.1,13,67,594/- is payable as tax on

capital gain. The interest and penalty under Section

158BFA(1) and 158BFA(2) (of Income Tax Act, 1961) were initiated separately. Being

aggrieved, the assessee filed an appeal before the

Commissioner of Income Tax (Appeals), who by an order

dated 28.09.2007 dismissed the appeal. Being aggrieved,

the assessee approached the Income Tax Appellate

Tribunal. The Tribunal by an order dated 04.03.2011 inter

alia held that before completion of block assessment

proceedings under Section 158BC (of Income Tax Act, 1961),

the assessing officer has to come to the conclusion whether

the undisclosed income belongs to the persons searched or

any other person. It was further held that even if the

Assessing Officer is the same person in the case of both the

person searched as well as other person, the recording of

satisfaction has to be before the completion of block

assessment proceeding in case of person searched. It was

also held that since, the Assessing Officer did not record

satisfaction before completion of proceeding under Section

158BC which should be reflected in notice under Section

158BD of the Act, the order of assessment is ab initio void.

Accordingly, the same was quashed and the appeal was

allowed. Being aggrieved, the Revenue is in appeal before

us.

4. Learned counsel for the revenue submitted that the

proceedings under Section 158BD (of Income Tax Act, 1961) were completed in case

of Javed on 30.05.2003 and thereafter, the satisfaction was

recorded by the Assessing Officer. However, the Income

Tax Appellate Tribunal, without examining the appeal on

merits, has allowed the appeal simply on the ground that

the satisfaction was not recorded in case of Javed before

completion of assessment proceedings. It is further

submitted that the aforesaid finding is contrary to law. In

this connection, reliance has been placed on the decision of

the Supreme Court in the case of ‘CIT Vs. CALCUTTA

KNITWEARS’ (2014) 362 ITR 673 (SC). None has

appeared on behalf of the respondents despite service of

notice.

5. We have considered the submissions made by the

learned counsel for the revenue and have perused the

record. The issue which arises for consideration before the

Supreme Court in the case of CALCUTTA KNITWEARS,

supra, was at what stage of proceedings under Chapter 14-

D, the Assessing Authority is required to record his

satisfaction for issuing a notice under Section 158BD (of Income Tax Act, 1961) of the

Act. The aforesaid issue has been answered in paragraph

44 of the judgment by the Supreme Court which is

reproduced below for the facility of reference:

“44. In the result, we hold that for the

purpose of section 158BD (of Income Tax Act, 1961) a

satisfaction note is sine qua non and must be

prepared by the Assessing Officer before he

transmits the records to the other Assessing

Officer who has jurisdiction over such other

person. The satisfaction note could be prepared

at either of the following stages: (a) at the time

of or along with the initiation of proceedings

against the searched person under Section

158BC of the Act; (b) along with the assessment

proceedings under Section 158BC (of Income Tax Act, 1961); and

(c) immediately after the assessment

proceedings are completed under Section 158BC (of Income Tax Act, 1961)

of the Act of the searched person.”

6. Thus, from perusal of the aforesaid paragraph, it is

evident that the satisfaction can even be recorded

immediately after completion of the assessment

proceedings under Section 158BC (of Income Tax Act, 1961). In the instant

case, admittedly, the satisfaction has been recorded after

completion of the proceedings under Section 158BC (of Income Tax Act, 1961) of the

Act. However, the order passed by the Assessing Officer as

well as the Commissioner of Income Tax (Appeals) has

been set aside by the Tribunal merely on the ground that

the satisfaction has not been recorded before completion of

the assessment proceedings. The aforesaid finding is

contrary to law laid down by the Supreme Court in the case

of CALCUTTA KNITWEARS, supra. Therefore, the same

cannot be sustained in the eye of law.

7. In view of the preceding analysis, the substantial

question of law framed by this Court is answered in the

negative. In the result, the impugned order passed by the

Tribunal dated 04.03.2011 is hereby quashed and the

matter is remitted to the Tribunal to deal with the appeal on

merits expeditiously in accordance with law.

In the result, the appeal is allowed.

Sd/-

JUDGE

Sd/-

JUDGE

×

Similar Ripples

Questions

Court Upholds Validity of Post-Assessment Satisfaction Note in Tax Case

Write your CommentSimilar Posts

Generic

- Reportdata/6245.pdf