Court Voids Tax Assessment Order for Procedural Violation, Limits Revisional Po…

Full News

Court Voids Tax Assessment Order for Procedural Violation, Limits Revisional Powers

Court Voids Tax Assessment Order for Procedural Violation, Limits Revisional Powers

The case involves Gigaby Technology (India) Private Ltd. challenging a tax assessment order and subsequent revision by the Commissioner of Income Tax (CIT). The High Court ruled in favor of the company, declaring the original assessment order void for failing to follow mandatory procedures, and limiting the CIT's revisional powers.

Get the full picture - access the original judgement of the court order here

Case Name:

Gigaby Technology (India) Private Limited Vs Commissioner of Income Tax (High Court of Bombay)

Tax Appeal No.77 of 2015

Date: 19th October 2020

Key Takeaways:

1. Assessment orders made without following Section 144C (of Income Tax Act, 1961) procedures are void ab initio.

2. CIT's revisional powers under Section 263 (of Income Tax Act, 1961) cannot be invoked for void orders.

3. Both erroneous nature and prejudice to revenue must be established for Section 263 (of Income Tax Act, 1961) revision.

4. Revisional jurisdiction cannot extend time limits for assessment completion.

Issue:

Was the Income Tax Assessing Officer's final assessment order valid without first issuing a draft assessment order as required by Section 144C (of Income Tax Act, 1961), and could the Commissioner of Income Tax revise such an order under Section 263 (of Income Tax Act, 1961)?

Facts:

- Gigaby Technology filed a tax return for the 2006-07 assessment year.

- The Assessing Officer (AO) made a final assessment order on 18/12/2009 without issuing a draft order as required by Section 144C (of Income Tax Act, 1961).

- The company appealed to the Commissioner (Appeals).

- On 20/03/2012, the CIT issued a notice under Section 263 (of Income Tax Act, 1961) to revise the assessment order.

- The Income Tax Appellate Tribunal (ITAT) dismissed the company's appeals against both the CIT's revision and the Commissioner (Appeals)' dismissal.

Arguments:

Assessee (Gigaby Technology):

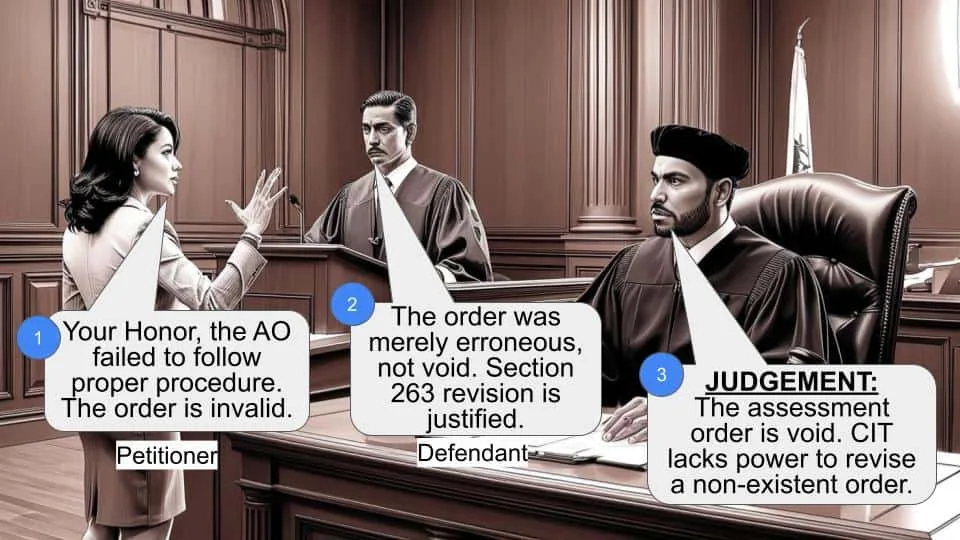

- The assessment order was void ab initio for not following Section 144C (of Income Tax Act, 1961) procedures.

- The CIT couldn't revise a void order under Section 263 (of Income Tax Act, 1961).

- The order wasn't prejudicial to the revenue's interests, a requirement for Section 263 (of Income Tax Act, 1961) revision.

Revenue:

- The assessment order was merely erroneous, not void.

- The order was prejudicial to revenue interests as it could be easily set aside on appeal.

Key Legal Precedents:

1. M/s. Zuari Cement Ltd. vs. The Assistant Commissioner of Income Tax

2. Control Risk India (P.) Ltd. vs. Deputy Commissioner of Income Tax

3. International Air Transport Association vs. Deputy Commissioner of Income-tax

4. Principal Commissioner of Income-tax-15 vs. Lionbridge Technologies (P.) Ltd.

5. Vijay Television (P.) Ltd. vs. Dispute Resolution Panel, Chennai

6. Malabar Industrial Co. Ltd. vs. Commissioner of Income Tax

These cases established that assessment orders made without following Section 144C (of Income Tax Act, 1961) are void or without jurisdiction.

Judgement:

The High Court ruled in favor of Gigaby Technology, holding that:

1. The assessment order dated 18/12/2009 was void ab initio for not following Section 144C (of Income Tax Act, 1961) procedures.

2. The CIT's revision under Section 263 (of Income Tax Act, 1961) was invalid as it lacked jurisdiction over a void order.

3. The CIT failed to establish that the order was prejudicial to revenue interests.

4. The ITAT erred in allowing the CIT to extend the assessment completion period.

The court set aside both the CIT's revision order and the ITAT's order confirming it.

FAQs:

Q1: What is Section 144C (of Income Tax Act, 1961)?

A1: It requires the Assessing Officer to issue a draft assessment order to eligible assessees before making a final order, allowing them to file objections with the Dispute Resolution Panel.

Q2: Can a void assessment order be revised under Section 263 (of Income Tax Act, 1961)?

A2: No, the court ruled that revisional powers under Section 263 (of Income Tax Act, 1961) cannot be invoked for orders that are void ab initio.

Q3: What are the requirements for invoking Section 263 (of Income Tax Act, 1961)?

A3: The Commissioner must be satisfied that the order is both erroneous and prejudicial to the interests of the revenue.

Q4: Does filing an appeal instead of a writ petition change the legal status of a void order?

A4: No, the court held that the legal status of the order being void remains the same regardless of the type of challenge.

Q5: Can revisional jurisdiction be used to extend assessment time limits?

A5: No, the court affirmed that Section 263 (of Income Tax Act, 1961) cannot be used to give a fresh lease of life for making an assessment order after the prescribed period has expired.

Heard the learned Counsel for the parties.

2. The learned Counsel for the parties submit that both these Tax Appeals can be disposed of by a common Judgment and Order, since, the decision in Tax Appeal No.77/2015 will govern the decision in Tax Appeal No.78/2015. The learned Counsel agree that in case Tax Appeal No.77/2015 is decided in favour of the Assessee, then, Tax Appeal No. 78/2015 will also have to be decided in favour of the Assessee. However, if Tax Appeal No.77/2015 is decided against the Assessee, then, Tax Appeal No.78/2015 will also have to be dismissed.

3. Tax Appeal No.77/2015 was admitted on 11/2/2016, on the following substantial questions of law :

1. Whether on the facts and circumstances of the case and in law, the Tribunal erred in holding that there was no infirmity in assuming revisionary jurisdiction by the CIT under section 263 (of Income Tax Act, 1961), without appreciating that the assessment order which was sought to be revised by such revisionary action was itself bad in law and void ab initio ?

2. Whether on the facts and circumstances of the case and in law, the Tribunal erred in upholding the action of the CIT under section 263 (of Income Tax Act, 1961), without appreciating that such action of the CIT directing the AO to frame de novo assessment would result in extending the period of limitation as provided in section 153 (of Income Tax Act, 1961), to complete the assessment proceedings, and thus, the action of the CIT was non-est, invalid and illegal?

4. In this case, the Appellant-Assessee is engaged in the trading of computer components and peripherals, including motherboards, AGP cards, and optical disk drives. On 27/11/2006, the Appellant filed a return of income for the Assessment Year 2006-07. Notices under Sections 143(2) (of Income Tax Act, 1961) and 142(1) (of Income Tax Act, 1961) (said Act) were issued to the Assessee on 25/10/2007. On 27/3/2008, the Assessee's return of income was processed under Section 143(1) of the Income Tax Act, 1961, since the Assessee had entered into international transactions during the subject assessment year. The matter was referred to Transfer Pricing Officer (TPO) for computing the arm's length price.

5. The TPO made an order dated 29/10/2009 under Section 92CA(3) of the Income Tax Act, 1961 proposing an addition of Rs.7,30,40,428/- in respect of the international transactions for the purchases made from the associated enterprises. On 18/12/2009, the Assessing Officer (AO) made the final assessment order under Section 143(3) of the Income Tax Act, 1961, assessing the total income of the Assessee at Rs.6,38,06,928/-.

6. The Assessee aggrieved by Assessment Order dated 18/12/2009, appealed to the Commissioner (Appeals) on 27/01/2010. One of the main grounds urged by the Assessee was that in this case, the AO was duty-bound to follow the provisions of Section 144C of the Income Tax Act, 1961 and, in terms thereof, to provide the Assessee with a draft assessment order before the assessment order would be made under Section 143(3) of the Income Tax Act, 1961.

7. The Commissioner (Appeals) called for a remand report from the AO, which was duly submitted by the AO on 2/2/2012. It is the case of the Assessee that the remand report form, with the provision of Section 144C of the Income Tax Act, 1961, was not complied with by the AO in this matter.

8. On 20/03/2012, the Commissioner of Income Tax (CIT) issued a notice under Section 263(1) of the Income Tax Act, 1961, purporting to exercise his revisional jurisdiction in the matter of the assessment order dated 18/12/2009 made by the AO. This notice states that the AO, by failing to provide the draft assessment order in terms of Section 144C(1) of the Income Tax Act, 1961 to the Assessee, had violated the principles of natural justice and, therefore, the assessment order dated 18/12/2009, was erroneous and deserved to be set aside.

9. The Assessee, on 19/3/2012, filed a detailed response to the notice dated 23/2/2012 objecting to the very initiation of the revisional proceedings. The Assessee pointed out that the assessment order dated 18/12/2009 was not merely illegal, but was void ab initio and, therefore, a nullity. In any case, the Assessee pointed out that the assessment order dated 18/12/2009 was certainly not prejudicial to the interest of the Revenue and, therefore, there was no question of exercise of the powers under Section 263 of the Income Tax Act, 1961.

10. On the very next day i.e. 20/3/2012, the CIT passed an order under Section 263 of the Income Tax Act, 1961, setting aside the assessment order dated 18/12/2009 and directing the AO to issue the Assessee draft assessment order as contemplated by Section 144C(1) of the Income Tax Act, 1961.

11. On 30/3/2012, the Commissioner (Appeals) dismissed the Assessee's appeal against the assessment order dated 18/12/2009 on the ground that the appeal was rendered infructuous because the CIT, in the exercise of powers under Section 263 of the Income Tax Act, 1961, had already set aside the assessment order dated 18/12/2009.

12. The Assessee appealed to the Income Tax Appellant Tribunal (ITAT), challenging both, the CIT's order dated 23/2/2012 purporting to exercise the revisional jurisdiction and the order of the Commissioner (Appeals) dated 30/03/2012, dismissing the Assessee's appeal. The ITAT, vide order dated 31/10/2014, dismissed both these appeals. Hence these two appeals under Section 260A of the Income Tax Act, 1961 by the Assessee.

13. Tax Appeal No.77/2015 concerns the order dated 30/3/2012 made by the CIT in the purported exercise of its revisional jurisdiction under section 263 of the Income Tax Act, 1961. If this order, as well as the order of the ITAT dated 31/10/2014 confirming this order, are set aside, then, obviously the assessment order dated 18/12/2009 and the order of the Commissioner (Appeals) dated 30/3/2012, will also have to be set aside.

14. Accordingly, it is only appropriate that both these Appeals are disposed of by a common Judgment and Order by treating Tax Appeal No.77/2015 as the lead matter.

15. Mr. Vishal Kalra, the learned Counsel for the Appellant- Assessee, at the outset, submitted that the AO was duty-bound to follow the provisions of Section 144C of the Income Tax Act, 1961 and since, admittedly, these provisions were not followed, the assessment order dated 18/12/2009 was void ab initio and a nullity. He submits that as against the order which was void ab initio, or a nullity, the revisional jurisdiction under Section 263 of the Income Tax Act, 1961 could never have been invoked. He submits that Section 263 of the Income Tax Act, 1961 presupposes the existence of an order which may be erroneous, but not an order which is void ab initio or a nullity. In support of this proposition, Mr. Kalra relies upon the following decisions :

(i) Keshab Narayan Banerjee vs. Commissioner of Income-tax

(ii) P. Abdulkadar Hamza vs. Commissioner of Income-tax

(iii) Commissioner of Income-tax

(iv) Westlife Development Ltd. vs. Principal Commissioner of Income

(v) Inder Kumar Bachani (HUF) vs. Income Tax Officer ; and

(vi) Paul John, Delicious Cashew Co. vs. The Income Tax Officer

16. Mr. Kalra also referred to some of the decisions which take the view that assessment orders made without following the provisions of Section 144C of the Income Tax Act, 1961 (wherever applicable) are a nullity and consequently unsustainable. These decisions are :

(a) M/s. Zuari Cement Ltd. vs. The Assistant Commissioner of Income Tax; Tirupathi

(b) Control Risk India (P.) Ltd. vs. Deputy Commissioner of Income Tax

(c) International Air Transport Association vs. Deputy Commissioner of Income-tax

(d) Principal Commissioner of Income-tax-15 vs. Lionbridge Technologies (P.) Ltd.; and

(e) Vijay Television (P.) Ltd. vs. Dispute Resolution Panel, Chennai 11

17. Mr. Kalra submits that in this case, even it were to be assumed that the assessment order dated 18/12/2009 was merely erroneous and not a nullity, the revisional jurisdiction could not have been exercised, because, the assessment order dated 18/12/2009 was, in no manner, prejudicial to the interest of the Revenue. He submits that unless and until the twin conditions i.e. the order being erroneous and the order being prejudicial to the interest of the Revenue, are established, there is no jurisdiction to exercise the revisional powers under Section 263 of the Income Tax Act, 1961.

18. Mr. Kalra submits that in any case, by incorrectly exercising the revisional jurisdiction of Section 263 of the Income Tax Act, 1961, the CIT has purported to extend the period of limitation for making the assessment order, which is impermissible. He relies upon the decision of the Full Bench of the ITAT (Chennai Bench) in case of V. Narayanan vs. ACIT12. He submits that the decision of the Full Bench in V. Narayanan (supra) was binding upon the ITAT in the present case, in view of the law laid down by the Hon'ble Supreme Court in Union of India & others vs. Kamlakshi Finance Corporation Limited ; the decision of the Bombay High Court in CIT vs. Goodlas Nerolac Paints Limited substantial questions of law, as framed in these matters, are required to be answered in favour of the Assessee and against the Revenue.

20. Ms. Linhares, the learned Standing Counsel for the Revenue, defends the order made by the ITAT based on the reasoning reflected therein. She submits that the assessment order dated 18/12/2009 was not a nullity, but it was merely an erroneous order made in breach of the procedure prescribed under Section 144C of the Income Tax Act, 1961. She points out that the assessment order dated 18/12/2009 was prejudicial to the interest of the Revenue because the said assessment order could have been easily set aside by the appellate authorities on the ground of breach of procedure. She submits that accordingly the two preconditions for the exercise of the revisional jurisdiction under Section 263 of the Income Tax Act, 1961 were fulfilled and there was nothing wrong in the exercise of the revisional jurisdiction by the CIT in these matters. On this basis, Ms. Linhares submits that the substantial questions of law are required to be answered against the Assessee and in favour of the Revenue.

21. The rival contentions now fall for our determination.

22. In this case, there is no dispute that the provisions of Section 144C of the Income Tax Act, 1961 were applicable and, further, such provisions were not complied with by the AO before passing the assessment order dated 18/12/2009.

23. Section 144C(1) of the Income Tax Act, 1961 provides that the Assessing Officer shall, notwithstanding anything to the contrary contained in the said Act, in the first instance, forward a draft of the proposed order of assessment (hereinafter in this section referred to as the draft order) to the eligible Assessee if he proposes to make, on or after the 1st day of October, 2009, any variation in the income or loss returned which is prejudicial to the interest of such Assessee.

24. Section 144C(2) (of Income Tax Act, 1961) then provides that on receipt of the draft order, the eligible Assessee shall, within thirty days of the receipt by him of the draft order, - file his acceptance of the variations to the AO;or - file his objections, if any, to such variation with,— (i) the Dispute Resolution Panel; and (ii) the Assessing Officer.

25. Section 144C(3) (of Income Tax Act, 1961) then provides that the AO shall complete the assessment based on the draft order, if the assessee intimates to the AO the acceptance of the variation; or no objections are received within the period specified in sub-section (2).

26. Section 144C(4) (of Income Tax Act, 1961) provides that the AO shall, notwithstanding anything contained in Section 153 (of Income Tax Act, 1961), pass the assessment order under sub-section (3) within one month from the end of the month in which, the acceptance is received, or the period of filing of objections under sub-section (2) expires.

27. Section 144C(5) (of Income Tax Act, 1961) provides that the DRP shall, in a case where any objection is received under sub-section (2), issue such directions, as it thinks fit, for the guidance of the AO to enable him to complete the assessment.

28. Section 144C(6) (of Income Tax Act, 1961) provides that the DRP shall issue the directions referred to in sub-section (5), after considering the following:

(a) draft order;

(b) objections filed by the assessee;

(c) the evidence furnished by the assessee;

(d) the report, if any, of the Assessing Officer, Valuation Officer or Transfer Pricing Officer or any other authority;

(e) records relating to the draft order;

(f) evidence collected by, or caused to be collected by, it; and

(g) result of any inquiry made by or caused to be made by, it.

29. Section 144C(7) (of Income Tax Act, 1961) provides that the DRP may, before issuing any directions referred to in sub-section (5), make such further inquiry, as it thinks fit; or cause any further inquiry to be made by any income-tax authority and report the result of the same to it.

30. Section 144C(8) (of Income Tax Act, 1961) provides that the DRP may confirm, reduce or enhance the variations proposed in the draft order so, however, that it shall not set aside any proposed variation or issue any direction under sub-section (5) for further enquiry and passing of the assessment order.

31. In this case, there is no dispute that the provisions of Section 144C (of Income Tax Act, 1961), read with Section 92CA of the Income Tax Act, 1961 were applicable. There is no dispute that in the present case, the AO before making the assessment order dated 18/12/2009 gave a complete go-by to the detailed provisions contained in Section 144C of the Income Tax Act, 1961. Therefore, the first question that arises for determination is, whether the assessment order dated 18/12/2009 made by the AO in clear breach of the mandatory provisions of Section 144C of the Income Tax Act, 1961, was merely erroneous, as contended by Ms. Linhares, or, whether the same was null and void as contended by Mr. Kalra, the learned Counsel for the Assessee.

32. In Zuari Cement Ltd. (supra), the Division Bench of the Andhra Pradesh High Court, in almost identical circumstances, held that the assessment order is contrary to the mandatory provisions of Section 144C of the Income Tax Act, 1961 and is 'one without jurisdiction, null and void and unenforceable'. In answer to the objection that no writ petition be entertained because the Assessee had a statutory appellate remedy, the Court held that since the impugned order was without jurisdiction, the objection about alternate remedy will not come in the way of the writ Court to grant relief. By order dated 21/2/2012, the Hon'ble Supreme Court dismissed the Special Leave to Appeal against the decision of the Division Bench of Andhra Pradesh High Court in M/s. Zuari Cement Ltd. (supra).

33. In Control Risk India (P.) Ltd. (supra), the Division Bench of Delhi High Court, held that consequent upon order of TPO under Section 92CA(3) of the Income Tax Act, 1961, it is incumbent upon the AO to pass a draft assessment order under Section 144C of the Income Tax Act, 1961 and this is a settled position as explained by the Court in its decision in Turner International India (P.) Ltd. vs. CIT [2017] 82 taxmann.com 125. In the said case the AO overlooked the above legal position and proceeded to pass the final order, thereby depriving the Assessee of an opportunity of questioning the draft assessment order under Section 144C of the Income Tax Act, 1961 before the DRP, the Court had no hesitation in setting aside the impugned assessment order and consequently the notice of demand. Again the Special Leave to Appeal against this decision was dismissed by the Hon'ble Supreme Court on 16/3/2018.

34. In International Air Transport Association (supra), the Division Bench of this Court has also taken a view that special rights are made available to an eligible Assessee under Section 144C of the Income Tax Act, 1961. These special rights contemplate the making of a draft assessment order under Section 144C (of Income Tax Act, 1961) by the AO before he makes a final assessment order under Section 143(3) of the Income Tax Act, 1961. Such a draft assessment order bestows certain rights upon an eligible Assessee, such as to approach the DRP with its objections to such a draft assessment order. This is for the reason that an eligible Assessee's grievance can be addressed before a final assessment order is passed and appellate proceedings invoked by it. However, these special rights were made available to eligible Assessee under Section 144C of the Income Tax Act, 1961 are rendered futile, if directly a final order under Section 143(3) of the Income Tax Act, 1961 is passed, without being preceded by a draft assessment order.

In such a situation, the assessment order made by the AO 'is completely without jurisdiction'. The Division Bench of this Court followed the decision of Andhra Pradesh High Court in M/s. Zuari Cement Ltd. (supra) and based on the same, not only set aside the assessment order but also consequential order on rectification application, as well as the penalty.

35. Again in Lionbridge Technologies (P.) Ltd. (supra), another Division Bench of this Court, following the decision in International Air Transport Association (supra) held that a draft assessment order is necessary in terms of Section 144C(1) of the Income Tax Act, 1961 before the AO can proceed to pass a final assessment order. In the absence thereof, the order is without jurisdiction. Non-issue of draft assessment order could not be corrected by issuing a corrigendum to a final assessment order. The Division Bench even rejected the contention that the Assessee was estopped from challenging the corrigendum, as it was expected by it that such a contention overlooked the fact that there can be no estoppel on the issue of law about jurisdiction. This Court held that if the corrigendum dated 16/4/2004 and the order dated 12/3/2014 of the AO were without jurisdiction, then, such an issue of jurisdiction can be raised at any time and the principles of estoppel will not apply. Mere consent of the parties does not bestow jurisdiction if the order is beyond jurisdiction.

36. To a similar effect is the law laid down by Madras High Court in Vijay Television (P.) Ltd. (supra). The Court held that the order passed by the AO lacked jurisdiction and when there is a statutory violation in not following the procedure prescribed and such an order cannot be cured by merely issuing a corrigendum. This decision has been approved by the Division Bench of this Court in Lionbridge Technologies (P.) Ltd. (supra).

36. Thus, from the conspectus of the aforesaid decisions, the legal position which emerges is that where a final assessment order is made by the AO without compliance with the mandate of section 144C of the Income Tax Act, 1961, the same is not merely an erroneous order as contended by Ms. Linhares, but such an order is without jurisdiction, as held by this Court or, null and void, as held by Andhra Pradesh High Court. The assessment order dated 18/12/2009 was therefore not merely an erroneous order but the same was an order without jurisdiction, null and void.

37. Even the CIT, in his order dated 20/3/2012 made in the purported exercise of revisional jurisdiction, held that the AO could not have passed the final assessment order dated 18/12/2009, without providing a draft assessment order in terms of Section 144C(1) of the Income Tax Act, 1961 to the Assessee in the present case. However, the CIT chose to style this final assessment order dated 18/12/2009 as merely 'erroneous'. Further, at least, in the notice dated 23/2/2012, by which the Commissioner purported to invoke the provisions of Section 263 of the Income Tax Act, 1961, there is no reference to the assessment order dated 18/12/2009 being prejudicial to the interest of the Revenue.

38. The Notice dated 23/2/2012, issued by the Commissioner invoking the revisional powers under Section 263 of the Income Tax Act, 1961, reads as follows :

39. Now, the legal position in so far as the invocation of the revisional powers under Section 263 of the Income Tax Act, 1961 is quite clear. Before such invocation, the Commissioner is required to be satisfied that the order which is proposed to be revised is erroneous, as well as prejudicial to the interest of the Revenue. Unless and until these conditions are satisfied, there is no question of invocation of powers under Section 263 of the Income Tax Act, 1961. There are several decisions, which have taken this view, the leading decision being Malabar Industrial Co. Ltd. vs. Commissioner of Income Tax.

40. In this case, the notice dated 23/2/2012, by which the Commissioner has purported to invoke his revisional powers, only points out that the assessment order dated 18/12/2009 which he proposed to revise, was erroneous because, the AO, in this case, failed to comply with the provisions under Section 144C of the Income Tax Act, 1961, though such provisions were clearly attracted in the facts and circumstances of the present case. However, there was absolutely no satisfaction recorded on the aspect of the assessment order dated 18/12/2009 being prejudicial to the interest of the Revenue. In absence of a record of any such satisfaction, there was no question of invoking the revisional powers under Section 263 of the Income Tax Act, 1961.

41. Some of the decisions relied upon by Mr. Kalra also support the view that revisional jurisdiction under Section 263 of the Income Tax Act, 1961 cannot be invoked in respect of an assessment order which is without jurisdiction or a nullity or void ab initio. However, according to us, it is not necessary to go into this issue, primarily because, the record, in this case, indicates that before the Commissioner invoked the revisional jurisdiction by the issuance of Notice dated 23/2/2012, the Commissioner nowhere recorded his satisfaction that the assessment order dated 18/12/2009 was prejudicial to the interest of the Revenue.

42. The ITAT, in this case, has not gone into the issue as to whether the Commissioner at all recorded any satisfaction that the assessment order dated 18/12/2009 was prejudicial to the interest of the Revenue. Instead, the ITAT has reasoned that since the assessment order dated 18/12/2009 was in breach of the provisions of Section 144C of the Income Tax Act, 1961, the assessment order would not have withstood the challenge in appeal, and in that sense the assessment order dated 18/12/2009 was prejudicial to the interest of the Revenue. Based on such reasoning, the ITAT virtually permitted the CIT to not only assume the revisional jurisdiction, in absence of satisfaction of one of the twin conditions, it further permitted the CIT to even extend the period for completion of the assessment in terms of Sections 143 and 144C of the said Act.

43. The Full Bench of the ITAT in the case of V. Narayanan (supra), has held that revisional jurisdiction under Section 263 of the Income Tax Act, 1961 cannot be invoked to give a fresh lease of life for making an assessment order where the period prescribed for making such an assessment order has already expired. This decision of the Full Bench was binding upon the ITAT in absence of any contrary decision of the Hon'ble Supreme Court or the jurisdictional High Court.

44. The ITAT has sought to distinguish the decisions in M/s. Zuari Cement Ltd. (supra), Control Risk India (P.) Ltd. (supra); International Air Transport Association; Lionbridge Technologies (P.) Ltd. (supra) and Vijay Television (P.) Ltd. (supra) on the basis that all these were decisions rendered in Writ Petitions where the High Courts held that the assessment orders without following the provisions under Section 144C of the Income Tax Act, 1961, is in excess of jurisdiction or null and void. The ITAT has reasoned that since in this case the Assessee had not instituted a Writ Petition and got the assessment order dated 18/12/2009 void ab initio or a nullity, such assessment order dated 18/12/2009 could always have been revised by the revisional authority.

45. According to us, the issue is whether the assessment order dated 18/12/2009 in this case, is void ab initio or not. Going by the decisions in M/s. Zuari Cement Ltd. (supra), Control Risk India (P.) Ltd. (supra); International Air Transport Association; Lionbridge Technologies (P.) Ltd. (supra) and Vijay Television (P.) Ltd. (supra), we have to hold that the assessment order dated 18/12/2009, in the present case, was clearly without jurisdiction and, therefore, null and void or void ab initio. The fact that the Assessee, in this case, may have not instituted a Writ Petition to challenge the same, but has instituted only an appeal challenging the same, can make no difference to the legal position which is otherwise quite clear. This was not a case where the assessee was merely throwing some collateral challenge to the assessment order dated 18/12/2009. The assessee had frontally challenged this order by instituting an appeal against the same. Therefore, all these decisions could not have been ignored by the ITAT by merely observing that these were the decisions in Writ Petitions instituted by the Assessees.

46. For all the aforesaid reasons, the two substantial questions of law will have to be answered in favour of the assessee and against the revenue. Further, the order dated 23/2/2012 made by the CIT in the purported exercise of jurisdiction under Section 263 of the Income Tax Act, 1961, is liable to be set aside. Since this order has merged into the order of the ITAT dated 31/10/2014, even this impugned order made by the ITAT is required to be set aside.

47. As a consequence, even the two substantial questions of law, as framed in Tax Appeal No.78/2015, will have to be answered in favour of the Assessee and against the Revenue. Further, the impugned orders in the said appeal will also have to be set aside.

48. Both the Appeals are disposed of in the aforesaid terms.

There shall be no order as to costs.

DAMA SESHADRI NAIDU, J. M. S. SONAK, J.

×

Similar Ripples

Questions

Court Voids Tax Assessment Order for Procedural Violation, Limits Revisional Powers

Write your CommentSimilar Posts

Generic

- Reportdata/6162.pdf