"Cross-Examination Crucial in Tax Dispute: Assessee’s Burden to Prove"

Full News

"Cross-Examination Crucial in Tax Dispute: Assessee’s Burden to Prove"

"Cross-Examination Crucial in Tax Dispute: Assessee’s Burden to Prove"

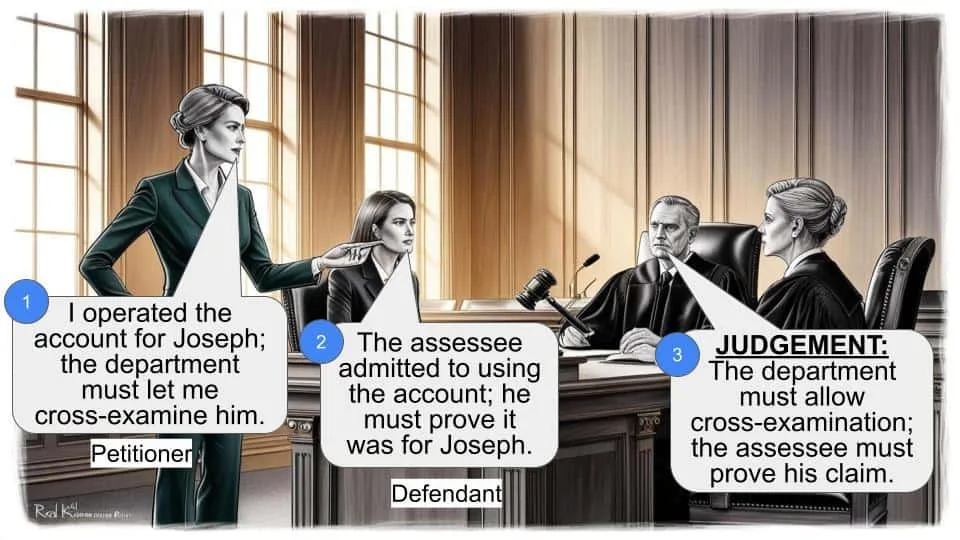

This case involves a dispute between an assessee and the tax department, where the department based its proceedings on a third-party statement. The court emphasized the necessity for the department to provide the third party for cross-examination and clarified the burden of proof lies with the department. However, the assessee admitted to operating a bank account, shifting the burden to him to prove he acted on behalf of the account holder.

Get the full picture - access the original judgement of the court order here

Case Name:

Jose Kuruvinakunnel Vs Commissioner of Income Tax (High Court of Kerala)

ITA. No. 149 of 2014

Date: 8th June 2015

Key Takeaways:

- The department must make third parties available for cross-examination when their statements are used against an assessee.

- The burden of proof initially lies with the department but can shift to the assessee if they admit to certain actions.

- The court highlighted the importance of not taxing the same income twice.

Issue

Does the tax department need to provide a third party for cross-examination when their statement is used against an assessee, and who bears the burden of proof?

Facts

The case revolves around the tax assessment of an individual who operated a bank account belonging to his brother-in-law, Sri Francis Joseph. The department initiated proceedings based on Joseph’s statement, which claimed the assessee used the account. The assessee admitted to operating the account but claimed it was on behalf of Joseph.

Arguments

- Assessee’s Argument: The department should have made Francis Joseph available for cross-examination. The same income was assessed in Joseph’s name, so it should not be taxed again in the assessee’s name.

- Department’s Argument: The addition to the assessee’s income was legal, as he admitted to operating the account. The burden to prove he acted on behalf of Joseph was on the assessee.

Key Legal Precedents

- P.S. Abdul Majeed v. Agricultural Income Tax and Sales Tax Officer and others [209 ITR 821]: Establishes the need for cross-examination of third parties in tax proceedings.

- Commissioner of Income Tax v. K.Chinnathamban [292 ITR 682] (SC): Discusses the depositor’s responsibility to explain bank deposits.

- Income Tax Officer, A Ward, Lucknow v. Bachu Lal Kapoor Kewal Ram [60 ITR 74]: Highlights that the same income cannot be taxed twice.

Judgement

The court ruled that while the department should provide third parties for cross-examination, the burden to prove the operation of the account on behalf of another lies with the assessee. The court directed the assessing officer to reconsider the Rs.3,00,000 addition, considering the final assessment order against Francis Joseph.

FAQs

Q1: Why is cross-examination important in this case?

A1: Cross-examination allows the assessee to challenge the credibility of the third-party statement used against them.

Q2: Who has the burden of proof in tax disputes?

A2: Initially, the department must prove allegations, but if the assessee admits to certain actions, the burden shifts to them to prove their claims.

Q3: Can the same income be taxed twice?

A3: No, the principle is that income should be assessed in the hands of the right person and not taxed twice.

1. These appeals are filed by the assessee challenging the order of the

Income Tax Appellate Tribunal, Cochin Bench in I.T.A.Nos.429, 431, 432 &

430 of 2005. Since issues raised are common, these appeals were heard

together and are disposed of by this common judgment treating ITA

149/14 as the leading case.

2. In these appeals, the relevant assessment years are 1996-1997 to

2000-2001, and in I.T.A.149/14 the assessee is challenging the additions

made on three counts. First one is deposit of Rs.3,00,000/- in the bank

account of one Sri.Francis Joseph, the brother-in-law of the assessee. The

second one is the unexplained credit of Rs.5,60,000/- in the capital account

of the firm Hotel Mayura of which the assessee is a partner and the third

one is relating to a loan of Rs.4,00,000/- taken by the assessee from one

Mr.George Joseph.

3. In so far as the addition of deposit of Rs.3,00,000/- in the bank

account of Mr.Francis Joseph is concerned, facts show that Sri.Francis

Joseph is the brother-in-law of the assessee. Sri.Francis Joseph had

given a statement to the DDIT (Inv) that he had opened S.B.Account

No.3075 in his name at the Federal Bank, Poovarani Branch and that he

had made initial deposits aggregating to Rs.2,00,000/-, which was

withdrawn by him. According to the Mr.Francis Joseph, thereafter all

other transactions in the account were operated by the assessee herein

using blank cheque leaves signed and given by him. On the basis of this

information, the assessment officer collected materials from the bank

and after considering the explanation offered by the assessee in

response to the notice issued to him, Rs.3,00,000/- was added to the

income of the assessee during the assessment year in question. This

addition was confirmed by the Commissioner of Income Tax Appeals

and the Tribunal.

4. Learned counsel for the assessee contended before us that

when the Department proceeded to initiate action on the basis of the

statement of Sri.Francis Joseph, Department should have made available

Sri.Francis Joseph for cross examination and that it was entirely upto

the Department to prove the allegations against him. Counsel also

referred us to Annexure G, an order of assessment in the name of

Sri.Francis Joseph, where according to him the very same amount was

assessed in the name of Sri.Francis Joseph himself. Therefore, according

to the counsel, the addition of this Rs.3,00,000/- to his income cannot

be sustained. This contention now raised by the counsel for the

assessee was refuted by the learned counsel for the Revenue and

according to him, the addition made was perfectly legal.

5. We have considered the rival submissions made. It is true that

as held in the judgment in P.S.Abdul Majeed v. Agricultural Income

Tax and Sales Tax Officer and others [209 ITR 821] when the

Department is proceeding against an assessee on the basis of the

statement of a third party, it is necessary that the Department should

make available that third party for cross examination and the burden to

prove the allegation is also on the Department. However, in so far as

this case is concerned, though the proceedings were originated on the

basis of the statement of Sri.Francis Joseph, after collecting the details

and records from the Bank, all such details were put to the assessee for

his explanation. The assessee thereupon admitted that he operated the

bank account of Sri.Francis Joseph, but according to him, such operation

of the bank account was on behalf of Sri.Francis Joseph and for his

benefit only. According to him, it was therefore that the bank

documents, such as cheque leaves and pay in slips, etc. contained his

signature.

6. This therefore shows that the fact that the assessee had

operated the bank account of Sri.Francis Joseph, was admitted by the

assessee himself. If that be so, the further question that remained was

whether he was acting for and on behalf of Sri.Francis Joseph as claimed

by him. The burden to prove a factual assertion made is upon the

person makes the assertion. Therefore, the burden to prove that he was

acting on behalf of Sri.Francis Joseph was not on the Department, but on

the assessee himself. When the burden is on the assessee to prove the

aforesaid factual question, it was the assessee's burden to make

available Sri.Francis Joseph for cross examination. In this context, we

should also record that the assessing officer had repeatedly issued

summons to Sri.Francis Joseph, and that though he stood by his

statement, he declined to appear for cross examination for one reason

or the other. This was despite the fact that the burden was that of the

assessee to produce him for examination. Therefore, in the facts of this

case, we are unable to find fault with the Department for not making

available Sri.Francis Joseph for cross examination.

7. In so far as the judgment of the Apex Court in Commissioner of

Income Tax v. K.Chinnathamban [292 ITR 682] (SC), relied on by the

counsel for the assessee is concerned, it is true that the principle laid

down in the judgment is that when proceedings are initiated based on

the bank deposit, it is for the depositor to explain the same. However,

that logic cannot be imported into the facts of this case for the simple

reason that the assessee himself has admitted of having operated the

bank account, though allegedly on behalf of the account holder. In such

a case, it is for the assessee who has operated the account to offer the

explanation and prove his case and not the deposit holder.

8. However, the contention of the assessee that by Annexure G

assessment order, Sri.Francis Joseph himself was assessed to income tax

for the year 1997-98, merits consideration. That assessment order also

makes reference to the aforesaid bank account in the name of

Sri.Francis Joseph and the amounts available therein. According to the

assessee, Annexure G assessment order has also become final.

9. Learned counsel for the assessee has placed reliance on the

judgment of the Apex Court in Income Tax Officer, A Ward, Lucknow v.

Bachu Lal Kapoor Kewal Ram [60 ITR 74] and submitted that the Act

does not envisage taxation on the same income twice over. The

principle that assessment should be in the hands of the right person and

that there cannot two assessments for the same income, are too well

settled. Therefore, if, as contended by the counsel for the assessee,

Annexure G assessment order has become final against Sri.Francis

Joseph, the very same amount cannot again be assessed in the name of

the assessee also.

10. We find that this issue was neither raised nor considered by

the assessing officer nor was this issue properly dealt with by the

Tribunal. Since, prima facie, there is force in what is argued, this is an

issue that needs to be considered by the Assessing Officer, who will

reconsider the liability of the assessee on this account, duly adverting to

Annexure G order in the name of Sri.Francis Joseph and with notice to

the assessee.

11. Second issue that arises for consideration is regarding the

deposit of Rs.5,60,000/- in the name of the assessee in the capital

account of the firm Hotel Mariya, of which he is a partner. Though this

addition was confirmed by the Appellate Commissioner and the

Tribunal, contention raised by the counsel for the appellant is that when

Rs.5,60,000/- was shown to the credit of the assessee in the accounts of

the firm, it is for the firm to explain such a credit and the assessee

cannot be called upon to explain the same. In support of this

contention, he placed reliance of a judgment in Commissioner of

Income Tax v. Shiv Shakti Timbers [229 ITR 505]. However, as rightly

contended by the learned Standing Counsel for the Department,

Rs.5,60,000/- was shown as the deposit made by the assessee in the

capital account of the firm and this amount was not reflected in the cash

flow statement filed by him before the assessing officer. This, therefore,

shows that Rs.5,60,000/- deposited by him in his capital account is an

unexplained investment made by the assessee attracting Section 69 (of Income Tax Act, 1961) of

the Income Tax Act. Facts being so, we do not find any illegality in the

order of the Tribunal confirming the said addition.

12. The third addition that is complained of is Rs.4,00,000/-

allegedly borrowed by the assessee from one George Joseph. According

to the learned counsel for the assessee, Sri.George Joseph in his

statement has explained source of this Rs.4,00,000/- by pointing out

that Rs.3,00,000/- was availed by him as loan from a bank and

Rs.1,00,000/- was from his personal savings. According to the learned

counsel, George Joseph is having substantial landed properties and

agricultural income and therefore, he having explained the source of the

amount advanced to the assessee, the addition ought not have been

made.

13. He also contended that the assessing officer himself and the

Tribunal having come to a conclusion that the assessee is not

maintaining books of accounts, the addition could not have been made

under Section 68 (of Income Tax Act, 1961). To support this contention,

counsel referred us to Commissioner of Income Tax v. Shiv Shakti

Timbers [229 ITR 505].

14. However, the statement of Sri.George Joseph itself show that a

part of the amount was borrowed by him from the bank and the

remaining part was from his personal savings. Despite this claim made,

he did not produce any evidence to substantiate it. Further, as rightly

indicated by the Tribunal, it is too improbable and against human

nature that a person who has borrowed money on interest, would lend

it without levying interest on the same. Therefore, we are unable to

accept the case of the counsel that the explanation of Sri.George Joseph

should have been accepted as the proof of source of the amount

advanced and that the addition should not have made.

15. It is true that Section 68 (of Income Tax Act, 1961) talks about books of accounts and it

is also true that in so far as this case is concerned, the assessee was not

maintaining books of accounts. It is on this basis that the counsel

contended that Section 68 (of Income Tax Act, 1961) could not have been invoked. We are unable

to agree. If this logic is accepted, it will be possible for any defaulting

assessee to escape from the payment of tax. In our view, Tribunal was

perfectly justified in its' finding that in case of this nature the cash flow

statement could be treated as the account of the assessee. Therefore, in

such circumstances, we cannot accept the case of the assessee. Issues

raised being common, the above findings would answer the contentions

raised in the remaining appeals also.

16. In the result, we dispose of these appeals setting aside the

addition made based on the deposit of Rs.3,00,000/- in the bank

account of Sri.Francis Joseph and direct that the assessing officer shall

reconsider that issue duly adverting to Annexure G order of assessment

issued to Sri.Francis Joseph for the assessment year 1997-98.

In all other respects, the orders will stand confirmed.

SD/-

ANTONY DOMINIC

JUDGE

SD/-

SHAJI P. CHALY

JUDGE

×

Similar Ripples

Questions

"Cross-Examination Crucial in Tax Dispute: Assessee’s Burden to Prove"

Write your CommentSimilar Posts

Generic

- Reportdata/3709.pdf