High Court Upholds Tribunal's Deletion of Income Tax Additions

Full News

High Court Upholds Tribunal's Deletion of Income Tax Additions

High Court Upholds Tribunal's Deletion of Income Tax Additions

This case involves a dispute between the Commissioner of Income Tax and M/s Jeet Construction Company, a partnership firm engaged in civil construction. The Income Tax Department conducted a search and seizure operation at the firm's premises and made several additions to the firm's taxable income. The firm appealed these additions, and the matter went through multiple levels of the income tax appellate process. Ultimately, the High Court upheld the Income Tax Appellate Tribunal's decision to delete the additions made by the Assessing Officer, finding that the additions were based on mere assumptions rather than evidence from the search and seizure.

Case Name:** Commissioner of Income Tax vs M/s Jeet Construction Company **Key Takeaways:** 1. The High Court affirmed that additions to taxable income cannot be made merely on the presumption that the assessee had undisclosed income and expenses outside the books of account. 2. The Tribunal's findings of fact, such as the Assessing Officer's additions being based on assumptions rather than evidence, were upheld and not interfered with by the High Court. 3. The case emphasizes the importance of the Assessing Officer basing additions on material recovered during the search and seizure, rather than making presumptions. **Issue:** Whether the Income Tax Appellate Tribunal was correct in law in deleting the additions made by the Assessing Officer to the taxable income of M/s Jeet Construction Company. **Facts:** - M/s Jeet Construction Company is a partnership firm engaged in civil construction. - The Income Tax Department conducted a search and seizure operation at the firm's premises and seized various incriminating materials and books of account. - The Assessing Officer made additions to the firm's taxable income, including Rs. 3,82,66,276 for unexplained expenditure and Rs. 1,00,00,000 for suppression of receipts and inflation of expenses. - The firm appealed the additions before the Commissioner of Income Tax (Appeals), who confirmed the Assessing Officer's actions. - The firm then appealed to the Income Tax Appellate Tribunal, which allowed the firm's appeal and deleted the additions made by the Assessing Officer. - The Income Tax Department then appealed the Tribunal's decision to the High Court. **Arguments:** - The Income Tax Department argued that the Tribunal was incorrect in law in deleting the additions made by the Assessing Officer, as the additions were based on the seized material and documents. - The firm argued that the additions were made by the Assessing Officer without any evidence and were based on mere assumptions, which the Tribunal had rightly rejected. **Key Legal Precedents:** - The case was decided under the provisions of the Income Tax Act, 1961, specifically Sections 158BD and 158BFA. - The Tribunal relied on the legal principle that additions cannot be made merely on the presumption that the assessee had undisclosed income and expenses outside the books of account. **Judgment:** - The High Court upheld the Tribunal's decision to delete the additions made by the Assessing Officer. - The High Court found that the Tribunal's findings of fact, such as the additions being based on assumptions rather than evidence, were justified and did not require any interference. - The High Court concluded that the appeal by the Income Tax Department lacked merit and was dismissed. **FAQs:** 1. **Q:** Why did the High Court uphold the Tribunal's decision to delete the additions made by the Assessing Officer? **A:** The High Court found that the Tribunal's findings of fact, which stated that the additions were based on mere assumptions rather than evidence from the search and seizure, were justified and did not require any interference. 2. **Q:** What is the key legal principle established in this case? **A:** The case emphasizes that additions to taxable income cannot be made merely on the presumption that the assessee had undisclosed income and expenses outside the books of account. The Assessing Officer must base any additions on the material recovered during the search and seizure operation. 3. **Q:** What were the main additions made by the Assessing Officer that were ultimately deleted? **A:** The Assessing Officer had made additions of Rs. 3,82,66,276 for unexplained expenditure and Rs. 1,00,00,000 for suppression of receipts and inflation of expenses. These additions were deleted by the Tribunal and upheld by the High Court. 4. **Q:** What were the key legal provisions referenced in this case? **A:** The case was decided under the provisions of the Income Tax Act, 1961, specifically Sections 158BD and 158BFA.

1. These two connected appeals, under Section 260-A (of Income Tax Act, 1961) (hereinafter called as 'Act') arise out of judgment and order dated 31.10.2011 passed by Income Tax Appellate Tribunal, Delhi Bench “D” New Delhi (hereinafter called as 'ITAT') in ITA No. 26/Del/2011 and order dated 19.10.2012 passed in ITA No. 39/Del/2012 for the block assessment year 1997-98 to 2003-04.

2. Income Tax Appeal No. 604 of 2012 was admitted on 22.05.2012 on substantial question of law nos. 1 and 2, and on 11.02.2019 additional substantial question of law nos. 4 and 5 were added, which are hereasunder:

“(1) Whether the Ld. Income Tax Appellate Tribunal was correcting in law in deleting the Addition of Rs.3,82,66,276/- and Rs.1,00,00,000/- by holding that additions in fresh assessment cannot exceed the additions made in the set aside assessment ignoring that the assessment was completed according to the direction of Ld. ITAT itself to frame the assessment on the basis of seized material and documents u/S 158BB(1) (of Income Tax Act, 1961). Whether such findings of ITAT are according to the provisions of Income Tax Act, 1961.

(2) Whether Ld. Income Tax Tribunal has erred in law in deleting the addition made by the AO of Rs.6,38,500/- u/S 69 (of Income Tax Act, 1961) C of the IT Act 1961 ignoring that onus to prove legality and date of such expenditure lied upon assessee solely for which opportunities were given by the AO. Whether onus to prove the date of such expenditure was ever lying upon the department.

(4) Whether the ITAT is legally justified in reversing the concurrent finding of fact of the authorities below without appreciating the material on record?

(5) Whether the ITAT is legally justified in reversing the concurrent findings of fact of the authorities below in the absence of fresh material placed before it?”

3. Income Tax Appeal No. 81 of 2003 was admitted on 15.01.2014 on substantial question of law nos. 1 and 2, which are hereasunder:-

“(1) Whether on the facts and circumstances of the case, the Ld. ITAT, New Delhi was justified in law in deleting the penalty imposed by the A.O. for Rs.3,05,58,009/- u/s 158 (of Income Tax Act, 1961) BFA (2) of the Income Tax Act, 1961 ignoring that matter related to relevant additions made during assessment for the same block A.Ys. 1997 to 2003-04 was subjudice before Hon'ble High Court, Allahabad which has also been admitted by the Hon'ble High Court Allahabad vide order dated 22.05.2012 in Appeal No. 604 of 2012.

(2) Whether the ITAT has erred in law in deleting the penalty imposed under Section 158 (of Income Tax Act, 1961) BFA (2) when the assessee did not fulfill any of the conditions prescribed in the Section.”

4. Both the appeals are being heard together and decided by a common order.

5. The brief facts of the case are, that respondent-assessee being a partnership firm was engaged in business of civil construction. A search and seizure was conducted under Section 132 (of Income Tax Act, 1961) on 23.12.2002, in the residential premises of working partner of the firm, Baljeet Singh Bakshi, Arvind Puri and Baldev Singh Bakshi. Search was also carried on the business premises of the firm and another shared business premises situated at 187-A/ Abu Lane, Meerut. During the course of search, several incriminating materials, along with some books of accounts pertaining to the firm was seized. As the seized material needed verification, Assessing Officer issued notice on 16.09.2004 under Section 158 (of Income Tax Act, 1961) BD of the Act on the assessee, which was served on 20.09.2004. The Assessing Officer found that assessee could not produce books of accounts and vouchers and thus, he reached to the conclusion that expenses debited by the assessee in trading and profit and loss account for various years of the block period could not be verified, thus, the books of accounts were rejected. Assessing Officer applied rate of 8% in order to ascertain the income for the block period and estimated the same at Rs.51,44,968/-. This, however, was done by the Assessing Officer without giving credit to the income already returned by the assessee.

6. Against the assessment order an appeal was filed before CIT (Appeals), who on 13.08.2007 deleted the addition of Rs.51,44,968/- on the ground that provisions of Section 44 (of Income Tax Act, 1961) AD were not applicable to the facts of the case. However, one addition in respect of illegal payments of commission aggregating to Rs.5,88,500/- in addition to levy of surcharge, credit of pre-paid taxes etc. was confirmed.

7. Against the aforesaid order, the assessee as well as the Revenue preferred appeals before the ITAT against the confirmation of addition of Rs.5,88,500/- as well as on the deletion of the addition made by the AO.

8. On 11.11.2008, the ITAT dismissed the appeal of the Revenue for block period 1997-98 to 2003-04 in respect of all additions except estimation of income of Rs.51,44,968/-, while the ITAT remanded back the matter to the Assessing Officer for re-examination and re-deciding the matter in the light of observation so made as regards the assessee's appeal. The ITAT remanded the matter to the AO with the direction to compute income under Section 158 (of Income Tax Act, 1961) BD (1) and decide the issue of unexplained expenditure of Rs.5,88,500/- with the specific direction.

9. Assessing Officer in remand proceeding completed the assessment on 31.12.2009 by making an addition on account of unexplained expenditure Rs.3,82,66,276/- suppression of receipts and inflation of expenses Rs.1,00,00,000/- and illegal payments of Rs.6,38,500/-. Thus, the assessing authority added Rs.4,89,476/- on account of undisclosed income while allowing credit for amount declared in block return at Rs.4,00,000/-.

10. Aggrieved by the said order an appeal was preferred before CIT (Appeals) by the assessee, the CIT (Appeals) on 16.03.2011 confirmed the action of the AO in initiating proceedings under Section 158 (of Income Tax Act, 1961) BD of the Act and completed the assessment at an income of Rs.4,85,04,776/-. Further, the CIT(Appeals) deleted the addition of Rs.6,38,500/- which was the commission paid by the assessee.

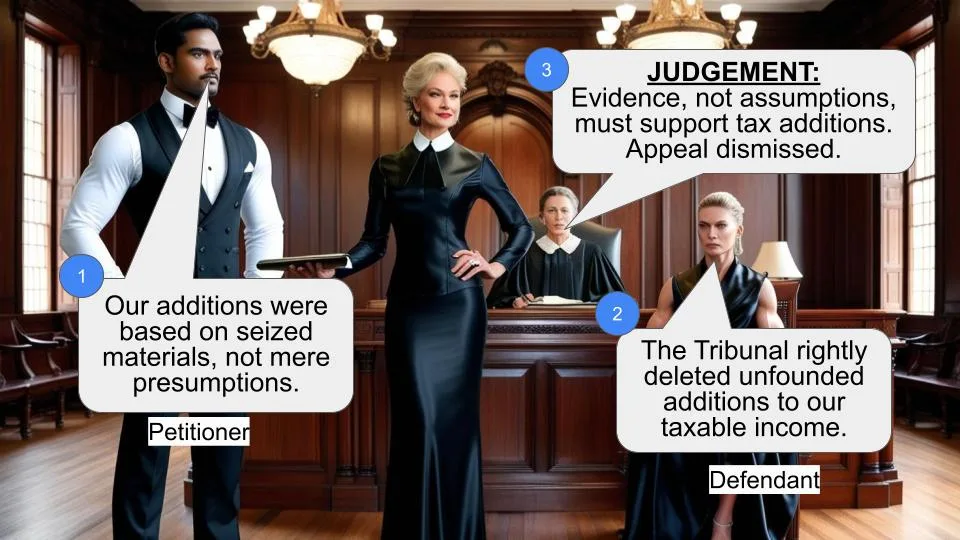

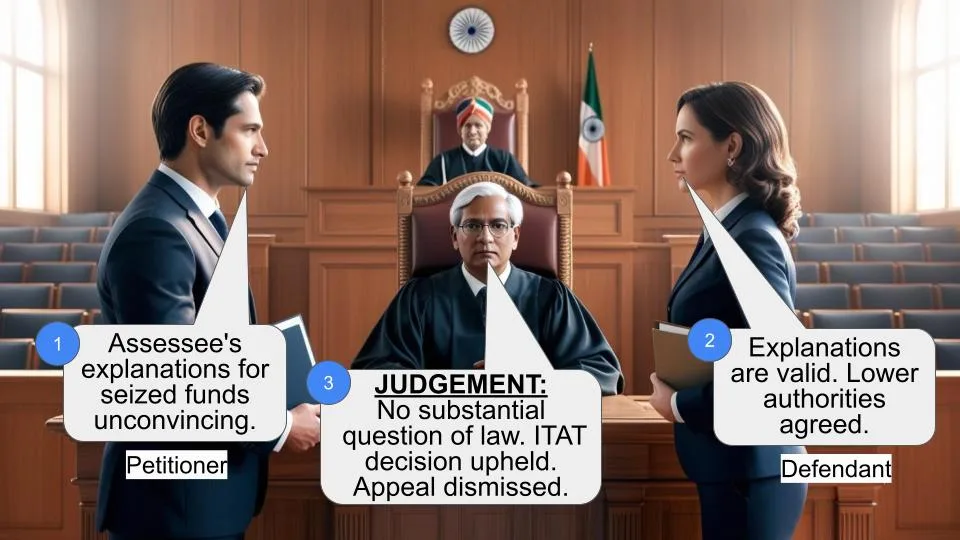

11. Against the said order, two appeals were filed before the ITAT, one by the assessee, ITA No. 26 (Del) of 2011 and the other ITA No. 28 (Del) of 2011 by the Department. The Tribunal on 31.10.2011 allowed the appeal of the assessee while dismissed the appeal of the Revenue on the ground that where the income had already been assessed or return of income has been filed, that income cannot be taken as undisclosed income. The Tribunal also recorded a categorical finding that Assessing Officer instead of working out undisclosed income, as per the provisions of Section 158 (of Income Tax Act, 1961) BD had totalled up amount mentioned in various annexures, which according to the assessee are part of the contract work done by him. No evidence was found to suggest that the assessee had been indulging in construction business outside books of account. Further, the Tribunal had recorded a finding that merely because ITAT remanded the matter to Assessing Officer, the total of all the entries whether recorded in regular books of accounts or without any date would constitute income of the assessee, that to undisclosed income. The Tribunal had remanded the matter with a direction to complete assessment under Section 158 (of Income Tax Act, 1961) BD based on seized material, but the Assessing Officer determined the taxable income of Rs.4,82,66,276/- as against addition of Rs.51,44,968/- has put the assessee in more adverse situation which is not permitted in law, and the addition cannot be made under Section 158 (of Income Tax Act, 1961) BD of the Act merely on presumption that assessee had earned undisclosed income and had incurred expenses outside the books of accounts.

12. We have heard learned counsel for the parties and perused the material on record.

13. We find that the Tribunal has recorded a finding in regard to the additions made by the Assessing Officer which was confirmed by the CIT (Appeals), which was based only on mere assumption and not on any material recovered during search and seizure. The Tribunal had recorded a categorical finding that addition cannot be made merely on presumption that assessee had earned undisclosed income and incurred expenses outside books of account, which need no interference being finding of fact, the appeal lacks merit and is hereby dismissed.

14. The question of law is, therefore, answered in favour of the assesseee and against the Revenue.

Order Date :- 16.10.2019

V.S.Singh

×

Similar Ripples

Questions

High Court Upholds Tribunal's Deletion of Income Tax Additions

Write your CommentSimilar Posts

Generic

- Reportdata/4780.pdf