Income under Section 44AE (of Income Tax Act, 1961) can't be taxed as 'other so…

Full News

Income under Section 44AE (of Income Tax Act, 1961) can't be taxed as 'other sources' under Section 56 (of Income Tax Act, 1961)

Income under Section 44AE (of Income Tax Act, 1961) can't be taxed as 'other sources' under Section 56 (of In…

This case involves a dispute between the Commissioner of Income Tax and Nitin Soni, a truck owner. The tax department tried to tax additional income under 'income from other sources', but the court ruled in favor of Soni, stating that income already covered under Section 44AE (of Income Tax Act, 1961) (presumptive taxation for goods carriers) cannot be taxed under Section 56 (of Income Tax Act, 1961) (income from other sources).

Case Name**: Commissioner of Income Tax vs. Nitin Soni

**Key Takeaways**:

1. Income taxable under Section 44AE (of Income Tax Act, 1961) cannot be additionally taxed under Section 56 (of Income Tax Act, 1961).

2. The purpose of Section 44AE (of Income Tax Act, 1961) is to provide hassle-free tax assessment for small transporters.

3. If income can be categorized under any specific head in Section 14 (of Income Tax Act, 1961), it cannot be taxed as 'income from other sources'.

**Issue**:

Whether the Income Tax Tribunal was justified in confirming the deletion of an addition of Rs. 29,21,738/- made by the Assessing Officer under Section 56(1) (of Income Tax Act, 1961), when the assessee failed to explain the source and nature of his capital generation?

**Facts**:

1. Nitin Soni is the proprietor of M/s Nitin Freight Carrier and a director of Northern Alkalies (P) Ltd.

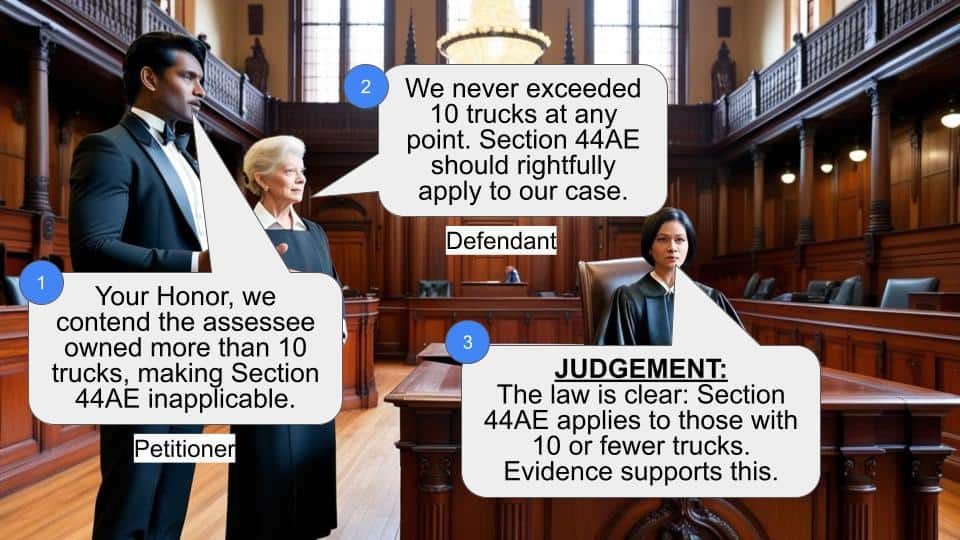

2. Soni disclosed income under Section 44AE (of Income Tax Act, 1961), claiming to possess only eight trucks.

3. The Assessing Officer made additions to Soni's income, arguing that he couldn't explain how he met his daily expenses.

4. The Commissioner of Income Tax (Appeals) partly allowed Soni's appeal.

5. The Income Tax Appellate Tribunal dismissed the department's appeal, leading to this case in the High Court.

**Arguments**:

Department's Argument:

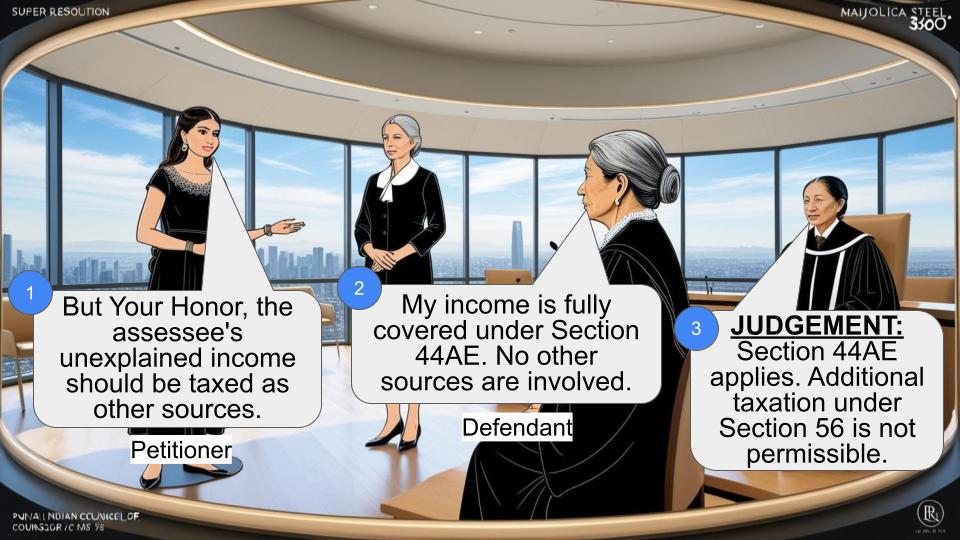

- The Assessing Officer found that the assessee had income from other sources.

- Even if Section 44AE (of Income Tax Act, 1961) applies, the assessee should explain excess income found.

Assessee's Argument:

- As the assessee owns eight trucks, there's no question of additional income from other sources.

- No other source of income was mentioned in the assessment order.

**Key Legal Precedents**:

1. S.G. Mercantile Corpn. (P) Ltd. v. Commissioner of Income-tax (1972) 83 ITR 700: The Supreme Court held that if income can appropriately fall under Section 28 (of Income Tax Act, 1961) as business income or any other specific head, Section 56 (of Income Tax Act, 1961) cannot be applied.

2. Commissioner of Income Tax v. Anil Kumar Arya (2009) 310 ITR 205: This case from the Punjab & Haryana High Court was cited by the assessee's counsel, though details weren't provided in the judgment.

**Judgement**:

1. The court dismissed the department's appeal, ruling in favor of Nitin Soni.

2. It held that Section 44AE (of Income Tax Act, 1961) applies in this case, which wasn't disputed by the department.

3. The court stated that the purpose of Section 44AE (of Income Tax Act, 1961) is to provide hassle-free proceedings for small transporters.

4. Even if actual income is more than calculated under Section 44AE (of Income Tax Act, 1961), it cannot be additionally taxed.

5. The court rejected the application of Section 56 (of Income Tax Act, 1961), stating that if income is chargeable under any heads specified in Section 14 (of Income Tax Act, 1961) (A to E), it cannot be charged as income from other sources.

**FAQs**:

1. Q: What is Section 44AE (of Income Tax Act, 1961)?

A: Section 44AE (of Income Tax Act, 1961) provides a special method for computing profits and gains for businesses involved in plying, hiring, or leasing goods carriages, applicable to owners of not more than ten trucks.

2. Q: Why couldn't the tax department tax the additional income under 'income from other sources'?

A: Because the income was already covered under Section 44AE (of Income Tax Act, 1961), and the law states that if income can be categorized under any specific head in Section 14 (of Income Tax Act, 1961), it cannot be taxed as 'income from other sources'.

3. Q: Does this mean that truck owners can never have income from other sources?

A: No, it doesn't mean that. It just means that income related to their trucking business, which is covered under Section 44AE (of Income Tax Act, 1961), cannot be additionally taxed under 'income from other sources'.

4. Q: What's the significance of this judgment for small transporters?

A: This judgment reinforces the purpose of Section 44AE (of Income Tax Act, 1961), which is to provide hassle-free tax assessment for small transporters. It protects them from additional taxation on income already covered under this section.

5. Q: Can the tax department challenge this decision further?

A: The judgment doesn't mention any further appeal. However, in principle, the department could appeal to the Supreme Court if they believe there's a substantial question of law involved.

Challenging the order dated 3rd September, 2008 passed by the Income Tax Appellate Tribunal, Lucknow Bench 'B', Lucknow (hereinafter referred to as 'the Tribunal') in I.T.A. No. 301/LUC/2007 for the assessment year 2001-02, the department has filed the present appeal.

In the memo of appeal, the following substantial question of law has been raised:

"1. Whether on the facts and in the circumstances of the case, the Hon'ble Tribunal was justified in law in confirming the order of the Ld. CIT(A)-I, Kanpur in deleting the addition of Rs.29,21,738/- made by the AO on a/c excess generation of income by invoking the provisions of section u/s 56(1) (of Income Tax Act, 1961) without appreciating that assessee failed to explain source and nature of generation of his capital."

Heard Sri Dhananjay Awasthi, learned counsel for the appellant and Sri Suyash Agrawal, learned counsel appearing for the assessee-opposite party.

The assessee is proprietor of M/s Nitin Freight Carrier. He is also one of the directors of Northern Alkalies (P) Ltd. In the return, he disclosed income under Section 44AE (of Income Tax Act, 1961) (hereinafter referred to as 'the Act') with the allegation that he possesses only eight trucks. Assessing Officer has made certain additions in the income of the assessee on the ground that the assessee has not been able to reply as to how he has been his meeting daily expenses. The plea raised under Section 44AE (of Income Tax Act, 1961) was rejected by him on the ground that the assessee has got income from other sources. The matter was carried in appeal before the CIT(A) by the assessee. The appeal was partly allowed vide order dated 08.02.2007 by the CIT(A). The matter was further carried in second appeal by the department before the Tribunal. The Tribunal has dismissed the appeal by order dated 03.09.2008, presently under appeal.

Sri Dhananjay Awasthi, learned counsel for the appellant submits that it was found by the Assessing Officer that the assessee has got income from other sources.Elaborating the argument, it was submitted that even if, Section 44AE (of Income Tax Act, 1961) is made applicable, it was for the assessee to explain the excess income found. He submits that the Assessing Officer was justified in making addition in the income at the hands of the assessee from other sources.

In reply, Sri Suyash Agrawal, learned counsel for the assessee submits that in view of the fact that the assessee has got eight trucks, there was no question of making any addition at the hands of the assessee from other sources. More so, no other source has been mentioned in the assessment order. He also placed reliance upon the judgment of Punjab & Haryana High Court in the case of Commissioner of Income Tax v. Anil Kumar Arya (2009) 310 ITR 205.

Considered the respective submissions of the learned counsel for the parties and perused the record.

Section 44AE (of Income Tax Act, 1961) inserted by Finance Act, 1994 provides special provision for computing profits and gains of business of plying, hiring or leasing goods carriages.It opens with an non obstanate clause by giving an overriding effect over sections 28 to 43C, in the case of an assessee who owns not more than ten goods carriages. Income of such assessee chargeable to the tax under the head “Profits and gains of business or profession” shall be deemed to be the aggregate of the profits and gains,from all the goods carriages owned by him in the previous year, computed in accordance with the provisions of sub-section (2). The words “shall be deemed” are the keys words and they are indicative of the legislative intent that the tax shall be chargeable on presumptive income, computed as per sub-section (2) of the Section 44AE (of Income Tax Act, 1961). The scope and effect of the above section has been explained in departmental circular No. 684 dated 10.06.1994. The relevant portion is extracted below:

“'Estimated Income Method for taxpayers engaged in the business of plying, leasing or hiring trucks owned by them.—32. A new section 44AE (of Income Tax Act, 1961) has been inserted in the Income-tax Act with a view to providing for a method of estimating income from the business of plying, hiring or leasing trucks owned by a taxpayer. The scheme applies to persons owning not more than ten trucks. It is not applicable to the persons who do not own any truck but operate trucks taken on hire. The income from each truck, being a heavy goods vehicle, will be estimated at Rs.2,000/- for every month or part of a month during which the truck is owned by the assessee. The income from each truck, other than a heavy goods vehicle, will be estimated at Rs.1,800/- for every month or part of a month during which the truck is owned by the assessee. In either case, the taxpayer can declare his income from trucks at a higher amount than that specified above.

32.2 The estimated income is comprehensive. All deductions under section 30 (of Income Tax Act, 1961) to 38 including depreciation, will be deemed to have been already allowed and no further deduction will be allowed under these sections. The written done value will be calculated, where necessary, as if depreciation as applicable has been allowed. In the case of firms, the normal deductions to the extent allowed under clause (b) of section 40 (of Income Tax Act, 1961) will be allowed. 32.3 An assessee who filed the return, estimating income on the basis of the specified amount per truck or estimating a higher income, will neither be required to maintain books of account under the provisions of section 44AA (of Income Tax Act, 1961), nor required to get accounts audited under the provisions of section 44AB (of Income Tax Act, 1961), in respect of his income from the business of plying, hiring or leasing trucks. However, even such an assessee has to comply with the requirements of both sections 44AA and 44AB in respect of his businesses which are not covered by this scheme.”

It is not in dispute that the assessee has got eight trucks. It was also not disputed by the learned standing counsel for the department that the provisions of Section 44AE (of Income Tax Act, 1961) are applicable. Emphasis was laid by him that the additions made in the hands of the assessee was justified as the assessee has income more than that which is calculated as per Section 44AE (of Income Tax Act, 1961). It is difficult to accept the aforesaid submission of the learned standing counsel. The very purpose and idea of enactment of such provision like Section 44AE (of Income Tax Act, 1961) is to provide hassle free proceedings. Such provisions are made just to complete the assessment without further probing provided the conditions laid down in such enactments are fulfilled. The presumptive income, which may be less or more, is taxable. Such an assessee is not required to maintain any account books. This being so, even if, its actual income in a given case, is more than income calculated as per sub-section (2) of Section 44AE (of Income Tax Act, 1961), cannot be taxed.

Thus, it follows the query of the Assessing Officer as to how the assessee met his daily expenses, there being no withdrawal and conclusion of additional income was uncalled for.

The Assessing Officer as well as the counsel for the revenue attempts to justify the addition with the aid of Section 56 (of Income Tax Act, 1961) i.e. income from other sources. It has no application here for the simple reason, as held by the Apex Court where an an income can appropriately fall under Section 28 (of Income Tax Act, 1961) as business income, or any other specific head of income, no resort can be made to Section 56 (of Income Tax Act, 1961) vide S.G. Mercantile Corpn. (P.) Ltd. v. Commissioner of Income-tax (1972) 83 ITR 700.

Income, if it is changeable to tax under any heads specified in Section 14 (of Income Tax Act, 1961),item A to E, it cannot be changed as income from other sources. Meaning thereby that if a particular income is referable to any one of the specified heads A to E, such income is not chargeable under Section 56 (of Income Tax Act, 1961), even if, it cannot be taxed under that head. Therefore, we reject the argument of the revenue.

In view of the fact that Section 44AE (of Income Tax Act, 1961) has been held to be applicable, which has not been disputed by the learned standing counsel for the department, we find that the CIT(A) and the Tribunal were justified in deleting the additions made holding that it cannot be treated as income from other sources. It may be stated here that the Assessing Officer has not given any other head of the income of the assessee. Only ground for making the addition is that the assessee was not able to explain the discrepancies in the account-books, which cannot be ground for making addition as income from other sources. Resultantly, the addition made by the Assessing Officer due to increase in the capital cannot be taxed under Section 56 (of Income Tax Act, 1961) as income from other sources as the accretion, if any, in the capital is relatable to profit from transport business of the assessee. A reading of the assessment order would show that the addition was made on account of excess generation of income of the assessee from the goods carriages business, under Section 56 (of Income Tax Act, 1961).

We do not find that any substantial question of law is involved in the appeal. It is dismissed summarily.

(Prakash Krishna,J) (Ashok Bhushan,J)

Order Date :- 26.4.2012

×

Similar Ripples

Questions

Income under Section 44AE (of Income Tax Act, 1961) can't be taxed as 'other sources' under Section 56 (of Income Tax Act, 1961)

Write your CommentSimilar Posts

Generic

- Reportdata/5885.pdf