Full News

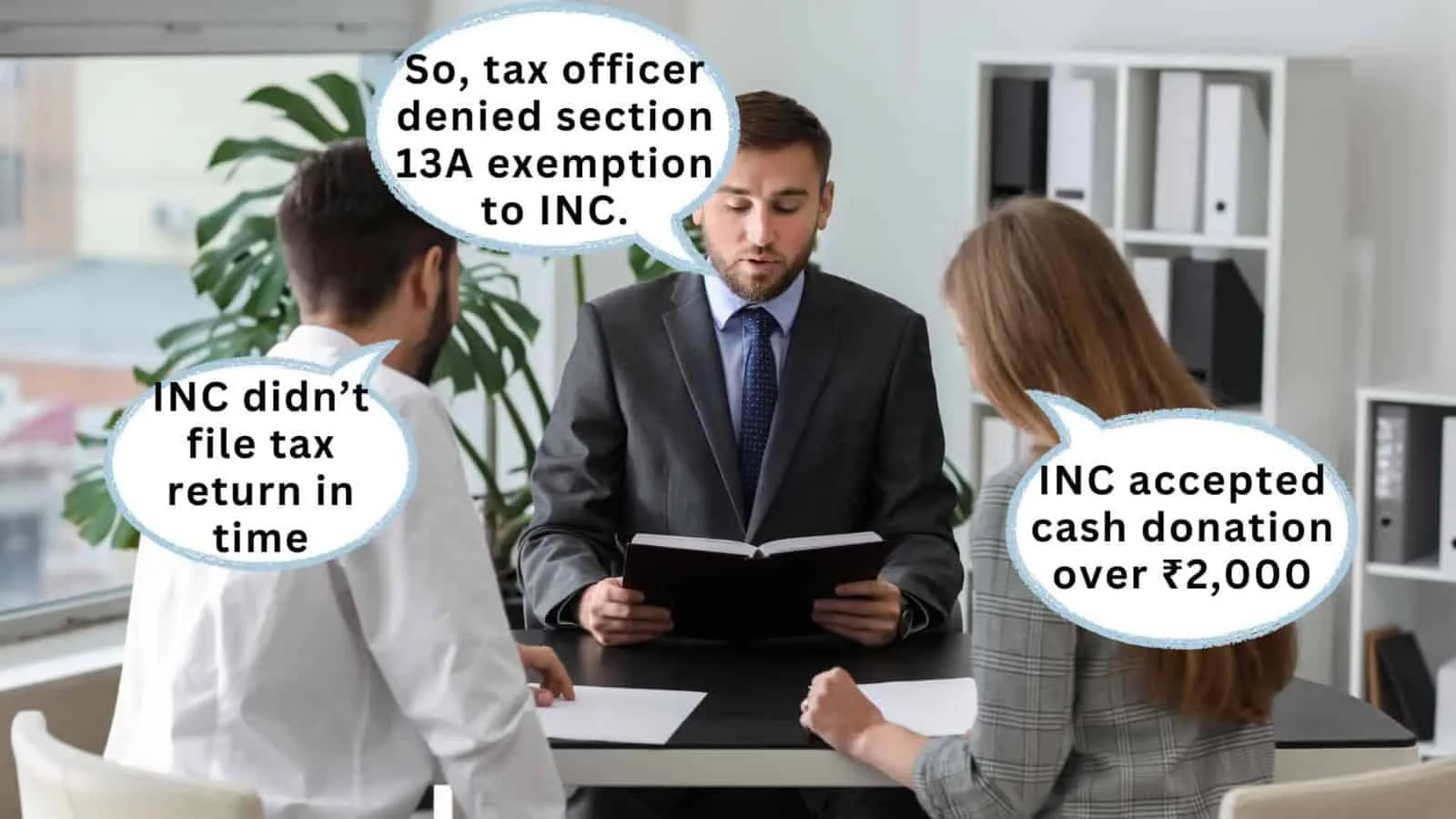

Indian National Congress denied tax exemption for 2018-19 due to violations of Section 13A (of Income Tax Act, 1961) rules on filing returns and cash donations.

Indian National Congress denied tax exemption for 2018-19 due to violations of Section 13A (of Income Tax Act…

The Income Tax Appellate Tribunal dismissed the stay application filed by the Indian National Congress (INC) against the recovery of tax demand of Rs. 105 crore for the assessment year 2018-19. The INC had claimed exemption under Section 13A (of Income Tax Act, 1961), but the assessing officer denied the exemption on two grounds: (1) the return was filed after the due date in violation of the third proviso to Section 13A (of Income Tax Act, 1961), and (2) the INC received cash donations exceeding Rs. 2,000 in violation of clause (d) of the first proviso to Section 13A (of Income Tax Act, 1961).

Case Name:

Indian National Congress All India Congress Committee Vs DCIT (ITAT Delhi)

Key Takeaways:

- Compliance with the conditions prescribed in Section 13A (of Income Tax Act, 1961) is mandatory for political parties to claim tax exemption.

- Filing the return of income by the due date under Section 139(1) (of Income Tax Act, 1961) is a prerequisite for claiming exemption under Section 13A (of Income Tax Act, 1961).

- Receiving cash donations exceeding Rs. 2,000 violates clause (d) of the first proviso to Section 13A (of Income Tax Act, 1961), leading to denial of exemption.

- The Tribunal found no merit in the INC’s arguments and dismissed the stay application.

Issue:

Whether the Indian National Congress (INC) is entitled to claim exemption under Section 13A (of Income Tax Act, 1961) for the assessment year 2018-19, given the alleged violations of the third proviso and clause (d) of the first proviso to Section 13A (of Income Tax Act, 1961).

Facts:

- The INC, a registered political party, filed its return of income for the assessment year 2018-19 on February 2, 2019, after the due date of December 31, 2018.

- The assessing officer denied the exemption claimed by the INC under Section 13A (of Income Tax Act, 1961) on two grounds:(1) violation of the third proviso by filing the return after the due date, and (2) violation of clause (d) of the first proviso by receiving cash donations exceeding Rs. 2,000.

- The assessing officer raised a tax demand of Rs. 105 crore on the INC’s income of Rs. 199 crore.

- The INC filed an appeal against the assessment order and sought a stay on the recovery of the demand during the pendency of the appeal.

Arguments:

INC’s Arguments:

- The return filed on February 2, 2019, was within the time allowed under Section 139(4) (of Income Tax Act, 1961) and should be considered compliant with the third proviso to Section 13A (of Income Tax Act, 1961).

- The cash receipts of Rs.14.49 lakh were voluntary contributions, not donations, and hence not violative of clause (d) of the first proviso.

- The entire income should not be taxed without allowing deductions for expenditure incurred in attaining the party’s aims and objects.

Revenue’s Arguments:

- The third proviso to Section 13A (of Income Tax Act, 1961) requires filing the return by the due date under Section 139(1) (of Income Tax Act, 1961), which was December 31, 2018, in this case.

- The INC’s account books and the report filed with the Election Commission treated the cash receipts as donations, violating clause (d) of the first proviso.

- No deduction for expenditure is allowable once exemption under Section 13A (of Income Tax Act, 1961) is denied, as per the Delhi High Court’s judgment in the INC’s case.

Key Legal Precedents:

Commissioner of Income-tax vs. Indian National Congress (I)/All India Congress Committee [2016] 383 ITR 99 (Delhi)

- Compliance with the conditions in Section 13A (of Income Tax Act, 1961) is mandatory for claiming exemption. No deduction for expenditure is allowed if exemption under Section 13A (of Income Tax Act, 1961) is denied.

Common Cause vs. Union of India and Ors. [1996] 2 SCC 752

- Statutory obligation on political parties to file returns of income.

Judgment:

The Tribunal dismissed the INC’s stay application, finding no merit in its arguments. The key reasons were:

1. The third proviso to Section 13A (of Income Tax Act, 1961) requires filing the return by the due date under Section 139(1) (of Income Tax Act, 1961), which the INC violated by filing the return on February 2, 2019.

2. The INC received cash donations exceeding Rs. 2,000, violating clause (d) of the first proviso to Section 13A (of Income Tax Act, 1961), as evident from its account books and the report filed with the Election Commission.

3. The Tribunal found no malafide intention in the assessing officer’s initiation of recovery proceedings under Section 226(3) (of Income Tax Act, 1961) on February 13, 2024.

4. The Tribunal upheld the assessing officer’s denial of exemption under Section 13A (of Income Tax Act, 1961) and the consequent tax demand.

FAQs:

Q1. What is the significance of the Tribunal’s decision?

A1. The decision upholds the strict interpretation of the conditions prescribed in Section 13A (of Income Tax Act, 1961) for political parties to claim tax exemption. It also affirms the Delhi High Court’s earlier ruling on the mandatory nature of these conditions and the disallowance of expenditure deductions if exemption is denied.

Q2. Can the INC challenge this decision?

A2. Yes, the INC can challenge the Tribunal’s decision by filing an appeal before the jurisdictional High Court.

Q3. What are the implications of the denial of exemption under Section 13A (of Income Tax Act, 1961)?A3. The INC’s entire income of Rs. 199 crore for the assessment year 2018-19, including voluntary contributions, will be taxable as income from other sources, without any deduction for expenditure.

Q4. What is the legal reasoning behind the Tribunal’s decision on the third proviso to Section 13A (of Income Tax Act, 1961)?

A4. The Tribunal held that the third proviso requires filing the return by the due date under Section 139(1) (of Income Tax Act, 1961), as defined in Explanation 2 to Section 139(1) (of Income Tax Act, 1961). The provision of Section 139(4) (of Income Tax Act, 1961), allowing belated filing, does not apply to the third proviso.

Q5. Why did the Tribunal reject the INC’s argument on cash donations?

A5. The Tribunal found that the INC’s account books and the report filed with the Election Commission treated the cash receipts as donations, not voluntary contributions. Hence, the cash donations exceeding Rs. 2,000 violated clause (d) of the first proviso to Section 13A (of Income Tax Act, 1961).

The Stay Application has been preferred by the assessee in terms of Rule 35A (of Income Tax Rules, 1962) of the Income-tax (Appellate Tribunal) Rules, 1963 seeking stay on the recovery of demand outstanding for Assessment year 2018-19.

2. Extensive arguments have been made by both the sides. Before we proceed to refer and deal with such arguments, it would be expedient to briefly touch upon the background, which has culminated in the present proceedings.

3. The Applicant before us is a Political Party registered under Section 29A of the Representation of the People Act, 1951. The Assessing Officer completed an assessment under Section 143(3) (of Income Tax Act, 1961) (hereinafter referred to as ‘the Act’) for the Assessment year 2018-19 vide an order dated 6th July, 2021 at an income of Rs.1,99,15,26,560/-, as against Nil income declared by the assessee in the return of income filed on 2nd February, 2019, thereby resulting in a demand of Rs.105,17,29,635/- (inclusive of interest under Section 234A (of Income Tax Act, 1961) at Rs.3,51,83,040/-, under Section 234B (of Income Tax Act, 1961) at Rs.28,14,64,320/-, under Section 234C (of Income Tax Act, 1961) at Rs.3,55,81,089/- and under Section 234F (of Income Tax Act, 1961) at Rs.10,000/-). The difference between the returned and assessed income is solely for the reason that assessee’s claim for exemption under section 13A (of Income Tax Act, 1961) has been denied by the Assessing Officer, and, accordingly, the entire income of Rs.1,99,15,26,560/- has been held to be taxable. The Assessing Officer has faulted the claim of exemption under Section 13A (of Income Tax Act, 1961) on two grounds viz., that the return of income filed by the assessee on 2nd February, 2019 under Section 139(4) (of Income Tax Act, 1961) contravenes the time limit prescribed in the third Proviso to Section 13A (of Income Tax Act, 1961); and, that clause (d) of the first Proviso to Section 13A (of Income Tax Act, 1961) has been violated since the assessee has received donations of Rs.14,49,000/- in cash from various persons, each donation being in excess of Rs.2,000/-.

4. The learned Senior Counsel for the Applicant opened his arguments by stressing upon the hardship created for the assessee, which is a National Political Party, in view of the forthcoming Parliamentary Elections, alleging that the initiation of the recovery proceedings under section 226(3) (of Income Tax Act, 1961) on 13th February, 2024 are so timed that the assessee would not be left with enough resources to contest the Parliamentary Elections. Attributing malice to the action of the Assessing Officer in exercising his power of recovery under Section 226(3) (of Income Tax Act, 1961), the learned Senior Counsel submitted that the intention is not merely to recover the outstanding demand, but to bring the activities of the assessee to a standstill, as it would not be able to meet out even the basic maintenance and establishment expenditure.

5. This was countered by learned Standing Counsel for the Revenue by asserting that the assessee was unnecessarily attributing motives to the action of the Assessing Officer, who has evidently proceeded in accordance with and as per the due process of law. According to him, the applicant-assessee was trying to take benefit of its own wrongs and delay, and has not approached this Court with clean hands. The chronology of events starting from the passing of assessment order on 6th July, 2021 has been referred in support.

6. It was pointed out that the impugned demand was raised by way of the Notice of demand under Section 156 (of Income Tax Act, 1961) which was issued along with the assessment order on 6th July, 2021; that the assessee approached the Assessing Officer on 20th October, 2021 seeking stay on the recovery of demand during the pendency of the appeal filed before the CIT(A) on 6th August, 2021; and, the said application was disposed-off by the Assessing Officer on 28th October, 2021, whereby, the Assessing Officer gave an option to the assessee to deposit 20% of the total demand and the balance of the demand would not to be enforced during the pendency of appeal before the CIT(A). The learned Senior Standing Counsel submitted that thereafter the assessee neither took the option of depositing 20% of the demand and nor challenged the rejection of its application before any higher authority. Having waited for almost two years, the Assessing Officer issued a letter on 9th January, 2023 seeking payment of the entire outstanding demand; the assessee by way of an e-mail dated 14th January, 2023 sought some time to reply and thereafter by letter dated 27th January, 2023 again sought stay on the recovery of demand under Section 220(6) (of Income Tax Act, 1961), because of the pendency of the appeal before the CIT(A). Learned Senior Standing Counsel submitted that the appeal of assessee was dismissed by the CIT(A) on 28th March, 2023; against which, an appeal has been preferred before this Tribunal on 24th May, 2023; and, even at that stage, no stay on the recovery of demand was sought till such time the Assessing Officer initiated the instant proceedings under Section 226(3) (of Income Tax Act, 1961) on 13th February, 2024. On the basis of the aforesaid sequence of events, it was submitted that the Assessing Officer has not shown any malice while initiating recovery proceedings by issuing notices under Section 226(3) (of Income Tax Act, 1961); rather, the assessee has been provided a reasonable time to organize its affairs. It was in October, 2021 that the assessee was given an option to pay 20% of the demand; however, assessee failed to pay and took no steps to challenge the rejection of its stay application as per law. It was thus submitted that the allegations of malice made against the action of the Revenue for initiating recovery proceedings were unfounded and baseless.

7. Next, in order to establish a prima facie case with regard to the issue in dispute, the learned Senior Counsel referred to various provisions of the Act regulating the filing of returns by the Political Parties, and submitted that the income-tax authorities below have failed to appreciate the scheme of Section 13A (of Income Tax Act, 1961) read with sub-section (4B) of Section 139 (of Income Tax Act, 1961) in its correct perspective. The learned Senior Counsel took us through the Memorandum explaining the provisions of Finance Bill, 2017, and pointed out that before the third Proviso was inserted below Section 13A (of Income Tax Act, 1961) with effect from 1st April, 2018, the filing of Return of income by a Political Party was not a condition precedent for availing the exemption under the said Section, and the purpose of the said Proviso was to mandate the Political Parties to henceforth file their returns of income for availing the exemption under Section 13A (of Income Tax Act, 1961); and, that such return of income was to be filed in terms of Section 139 (of Income Tax Act, 1961), which, according to him, meant that return of income could be filed within the due date as per sub-section (1) or as per the time allowed by subsection (4) of Section 139 (of Income Tax Act, 1961).

8. It was pointed out that similar amendment was also brought in Section 12 (of Income Tax Act, 1961), by the Finance Act, 2017, whereby the condition of filing return of income was introduced in order to claim the exemption under Sections 11 (of Income Tax Act, 1961) and 12 of the Act. The learned Senior Counsel referred to a CBDT clarification dated 23rd April, 2019, whereby it was clarified that for an entity registered under Section 12AA (of Income Tax Act, 1961), the requirement of filing of return in terms of sub-section (4A) of section 139 (of Income Tax Act, 1961) shall be fulfilled even if the return is filed within the time allowed as per sub-section (4) of Section 139 (of Income Tax Act, 1961). It was contended that on the same parity of reasoning, the time available to the Political Parties to file their return would be the time allowed as per sub-section (4) of Section 139 (of Income Tax Act, 1961), and it is not restricted to the due date prescribed in sub-section (1) of Section 139 (of Income Tax Act, 1961). Adverting to the import of subsection (4B) of Section 139 (of Income Tax Act, 1961), the learned Senior Counsel submitted that it merely prescribes the mode of filing of the return by the Political Parties, and the same does not prescribe that the time limit for furnishing the return is the due date as per Section 139(1) (of Income Tax Act, 1961) only, because it, inter alia, prescribes that “all the provisions of this Act, shall, so far as may be, apply as if it were a return required to be furnished under sub-section (1) of Section 139 (of Income Tax Act, 1961)”; and, that Section 139(4) (of Income Tax Act, 1961) being adjunct to Section 139(1) (of Income Tax Act, 1961) the period permissible in sub-section (4) would also be applicable; and, thus, the return filed by the assessee on 2nd February, 2019, though filed beyond the due date as per sub-section (1), is very much a return filed within the time allowed under Section 139 (of Income Tax Act, 1961), having been filed within the time allowed under sub-section (4) of Section 139 (of Income Tax Act, 1961). Learned Senior Counsel referred to certain other provisions of the Act to submit that wherever the law intended to deny a particular deduction/ exemption for non-filing of the return before the due date specified in Section 139(1) (of Income Tax Act, 1961), then explicit provision to that effect has been made under the Act, for instance, Sections 10A(1A), 10B and 80AC of the Act.

9. This has been countered by the learned Senior Standing Counsel for the Revenue by heavily relying on the judgment of the Hon’ble High Court of Delhi in the case of assessee itself reported as Commissioner of Income-tax Vs. Indian National Congress (I)/All India Congress Committee (and vice versa) - [2016] 383 ITR 99, to contend that the provisions of Section 13A (of Income Tax Act, 1961) and sub-section (4B) of Section 139 (of Income Tax Act, 1961) as amended by the Finance Act, 2017 have to be applied in letter and spirit. He also referred to the judgement of Hon’ble Supreme Court of India in Common Cause Vs. Union of India and Ors. - [1996] 2 SCC 752 to contend that a statutory obligation is cast on the Political parties to file their returns of income, and it is only as a fall out of the aforesaid Supreme Court judgment, that necessary amendments were brought in the Act. Section 13A (of Income Tax Act, 1961) was further amended by introduction of third Proviso by the Finance Act, 2017 with effect from 1st April, 2018, which was intended to fill the lacuna left out. He emphasized that the third Proviso specifically mandates that the return of income has to be filed on or before the ‘due date’ under Section 139(a) (of Income Tax Act, 1961), and by referring to Explanation 2 to Section 139(1) (of Income Tax Act, 1961), it was submitted that the ‘due date’ in the present case would mean 30th September, 2018, as extended up to 31st December, 2018 for the instant assessment year. According to him, the return of income filed by the assessee on 2nd February, 2019 is violative of the third Proviso to Section 13A (of Income Tax Act, 1961), thus, the exemption has been rightly denied by the Assessing Officer. He submitted that if the interpretation sought to be canvassed by learned Senior Counsel is to prevail, it would render the expression ‘due date’ in Section 13A (of Income Tax Act, 1961) as otiose.

10. Learned Senior Standing Counsel, relying on the fundamental principles of interpretation, contended that the provisions which are brought to counter a mischief should be given a literal interpretation, and accordingly, the third Proviso to Section 13A (of Income Tax Act, 1961) when read with Section 139(4B) (of Income Tax Act, 1961), makes it clear that the ‘due date’ is to be reckoned as per the definition in Explanation 2 of Section 139(1) (of Income Tax Act, 1961) only, thereby expressly making Section 139(4) (of Income Tax Act, 1961) inapplicable in the case of Political Parties seeking exemption under Section 13A (of Income Tax Act, 1961).

11. As regards the alleged violation of clause (d) of the Proviso of Section 13A (of Income Tax Act, 1961), the learned Senior Counsel submitted that indeed, no donation exceeding two thousand rupees has been received by the assessee otherwise than by account payee cheque/draft, and therefore, there is no violation of clause (d) of the Proviso to Section 13A (of Income Tax Act, 1961). It is submitted that assessee received Rs.14,49,000/- in cash as voluntary contributions, substantially from its own elected Members of Legislative Assemblies/Parliament/Office Bearers, etc. and that such sums do not constitute ‘Donations’ so as to attract clause (d) of the Proviso to Section 13A (of Income Tax Act, 1961). It was pointed out that complete details in this regard along with names, addresses and Permanent Account Number (PAN), etc. have been furnished and that such contributions fall for consideration in terms of clause (b) of the first Proviso to Section 13A (of Income Tax Act, 1961), for which no default attributed to the assessee.

12. The learned Senior Standing Counsel for the Revenue submitted that the Assessing Officer, after examining the account books of the assessee, has clearly recorded that assessee itself has described the impugned sums received as ‘Donations’ and that no distinction between a ‘Contribution’ and/or a ‘Donation’ has been maintained by the assessee in its account books. He also referred to a report dated 28th September, 2018, filed by the Treasurer of the assessee to the Election Commission of India under Section 29C(1) of The Representation of the People Act, 1951, which has also been relied by the Assessing Officer, to point out that the subject of the report itself makes it evident that the report is being filed in respect of Contributions/Donations received in excess of Rs.20,000/-. Thus, according to learned Senior Standing Counsel, it is clear that the assessee has received cash donations also in excess of Rs.2,000/- each as a part of Contributions and thus, the violation of clause (d) of the first Proviso stood established. He emphasized that so far as clause (d) of the first Proviso is concerned, there is an express bar on receipt of Donations in excess of Rs.2,000/- in cash.

13. Countering the distinction sought to be made by the learned Senior Counsel between clauses (b) and (d) of the first Proviso, the learned Senior Standing Counsel submitted that the presence of the word ‘and’ in between clauses (a) to (c) and (d) of the Proviso by the finance Act, 2017 shows that clauses (a) to (d) of the Proviso have to be applied in conjunction with clause (d) thereof. In support of the proposition that compliance with the clause (d) of the first Proviso is also mandatory, he has relied on the judgment of Hon'ble Delhi High Court in the case of the assessee itself dated 23rd March, 2016 (supra).

14. Lastly, the learned Senior Counsel submitted that even if for the sake of argument Section 13A (of Income Tax Act, 1961) is held to be inapplicable on the facts of the assessee, then too, the computation of income made by the Assessing Officer at Rs.119,15,16,560/- is unjust and arbitrary inasmuch as the expenditure incurred by the applicant for attaining the aims and objects of the Political Party has not been allowed. That taxing the entire receipts by treating the same as income was manifestly wrong. In this context, it was also pointed out that the income tax authorities have also not offset the deficit of Rs.96,30,18,572/- of the immediately preceding assessment year while determining the taxable income. In this context, he has relied upon the judgment of Hon'ble Supreme Court in the case of Commissioner of Income tax (Central), New Delhi Vs. Bijli Cotton Mills (P.) Ltd. – [1979] 116 ITR 60 (SC) as well as the judgment of Hon'ble Delhi High Court in the case of Deputy Director of Income-tax (Exemptions) Vs. Petroleum Sports Promotion Board – [2014] 362 ITR 235 (Delhi).

15. On the other hand, learned Senior Standing Counsel assailed the aforesaid by pointing out that in the return of income filed, assessee has not made any such claim of deduction for expenditure in terms of Section 57(iii) (of Income Tax Act, 1961). According to learned Senior Standing Counsel, only the expenses incurred wholly and exclusively for the purpose of earning income are allowable under the head “income from other sources” and that in the case of voluntary contributions of the nature in question, no expenses can be said to be attributable towards earning of voluntary contributions, and, in support, reference was made to the judgment of Hon'ble Delhi High Court in assessee’s own case dated 23rd March, 2016 (supra).

16. We have carefully put our mind to the rival contentions. Notably, the captioned proceedings are collateral to the substantive dispute of the assessee with the Revenue, which is the subject-matter of the appeal pending with the Tribunal vide ITA No.1609/Del/2023. The said appeal is listed for hearing before the regular Bench on 23rd April, 2024. In the instant proceedings, the limited issue relates to the plea of the Applicant that pending disposal of its appeal, the recovery of tax demand arising on account of the assessment order dated 6th July, 2021 (supra) be stayed.

17. So far as the power of the Tribunal to stay the recovery proceedings is concerned, the same has been judicially well-recognized, being an inherent power, and, it has also been impliedly imparted statutory acceptance by way of insertion of first and second Provisos below Section 254(2) (of Income Tax Act, 1961). The Hon'ble Supreme Court in the case of Income-tax Officer, Cannanore Vs. M.K. Mohammed Kunhi – [1969] 71 ITR 815 (SC) expressly opined that the Tribunal has power to grant stay, considering it to be a power which is incidental or ancillary to its appellate jurisdiction. In this context, we may refer to the following discussion by the Hon'ble Supreme Court :

“It could well be said that when section 254 (of Income Tax Act, 1961) confers appellate jurisdiction, it impliedly grants the power of doing all such acts, or employing such means, as are essentially necessary to its execution and that the statutory power carries with it the duty in proper cases to make such orders for staying proceeding as will prevent the appeal if successful from being rendered nugatory”.

18. However, the Hon'ble Supreme Court has also cautioned that such power should not be exercised in a routine way. The relevant discussion on this aspect is as under :-

“14. A certain apprehension may legitimately arise in the minds of the authorities administering the Act that if the Appellate Tribunals proceed to stay recovery of taxes or penalties payable by or imposed on the assessees as a matter of course the revenue will be put to great loss because of the inordinate delay in the disposal of appeals by the Appellate Tribunals. It is needless to point out that the power of stay by the Tribunal is not likely to be exercised in a routine way or as a matter of course in view of the special nature of taxation and revenue laws. It wilt only be when a strong prima facie case is made out that the Tribunal will consider whether to stay the recovery proceedings and on what conditions and the stay will be granted in most deserving and appropriate cases where the Tribunal is satisfied that the entire purpose of the appeal will be frustrated or rendered nugatory by allowing the recovery proceedings to continue during the pendency of the appeal.”

19. We may also refer to the judgment of Hon'ble Supreme Court in the case of Assistant Collector of Central Excise Vs. Dunlop India Ltd. And Ors. – 1985 AIR 330 wherein the Hon’ble Court has enunciated broad parameters to be applied while considering the pleas for grant of interim injunctions/stay on the recovery proceedings. The pertinent observations of the Hon'ble Supreme Court are as under :-

“There can be and there are no hard and fast rules. But prudence, discretion and circumspection are called for. There are several other vital considerations apart from the existence of a prima facie case. There is the question of balance of convenience. There is the question of irreparable injury. There is the question of the public interest. There are many such factors worthy of consideration.”

20. From the above, it is discernable that while exercising the power of stay, it is imperative for the Tribunal to not only consider factors, such as, existence of a prima facie case, balance of convenience and irreparable loss/hardship but also to be circumspect; and, that the stay on the recovery proceedings should not be granted as a matter of course or in a routine manner. Thus, each Application would have to be decided on its own merits, having regard to the facts and circumstances of the case.

21. We may also refer to the first Proviso below Section 254(2A) (of Income Tax Act, 1961), which reads as under :-

“Provided that the Appellate Tribunal may, after considering the merits of the application made by the assessee, pass an order of stay in any proceedings relating to an appeal filed under sub-section (1) of section 253 (of Income Tax Act, 1961), for a period not exceeding one hundred and eighty days from the date of such order and the Appellate Tribunal shall dispose of the appeal within the said period of stay specified in that order:”

22. Shorn of other details, for the purpose of the present controversy, it would suffice to note the words “……………after considering the merits of the application ………..” appearing above, reinforces our earlier premise that it is only in cases where the merits of the application have been made out, that the Tribunal would be justified in exercising its power of grant of stay on the recovery proceedings.

23. In this background, we may now proceed to examine as to whether or not the instant is a case which requires us to exercise power to stay the recovery of the impugned disputed demand. The basic dispute arises from the action of the Assessing Officer in denying the exemption claimed by the assessee under Section 13A (of Income Tax Act, 1961). The reasons for the denial, which are two-fold, have already been noted by us in the earlier part of this order. To recapitulate, the reasons are (i) violation of the third Proviso to Section 13A (of Income Tax Act, 1961); and, (ii) violation of clause (d) of the first Proviso to Section 13A (of Income Tax Act, 1961).

24. Before proceeding further, we reproduce hereinafter the relevant provisions of the Act, as applicable to the period under consideration and which have bearing on the issues before us :-

Section 13A (of Income Tax Act, 1961)

“13A. Any income of a political party which is chargeable under the head "Income from house property" or "Income from other sources" or "Capital gains" or any income by way of voluntary contributions received by a political party from any person shall not be included in the total income of the previous year of such political party :

Provided that—

(a) such political party keeps and maintains such books of account and other documents as would enable the Assessing Officer to properly deduce its income therefrom;

(b) in respect of each such voluntary contribution [other than contribution by way of electoral bond] in excess of [twenty] thousand rupees, such political party keeps and maintains a record of such contribution and the name and address of the person who has made such contribution.

(c) the accounts of such political party are audited by an accountant as defined in the Explanation below sub-section (2) of section 288 (of Income Tax Act, 1961) ; and

(d) no donation exceeding two thousand rupees is received by such political party otherwise than by an account payee cheque drawn on a bank or an account payee bank draft or use of electronic clearing system through a bank account or through electoral bond.

Explanation.—For the purposes of this proviso, "electoral bond" means a bond referred to in the Explanation to subsection (3) of section 31 of the Reserve Bank of India Act, 1934 (2 of 1934):

Provided further that if the treasurer of such political party or any other person authorised by that political party in this behalf fails to submit a report under sub-section (3) of section 29C of the Representation of the People Act, 1951 (43 of 1951) for a financial year, no exemption under this section shall be available for that political party for such financial year:

Provided also that such political party furnishes a return of income for the previous year in accordance with the provisions of sub-section (4B) of section 139 (of Income Tax Act, 1961) on or before the due date under that section.

Explanation.—For the purposes of this section, "political party" means a political party registered under section 29A of the Representation of the People Act, 1951 (43 of 1951).”

Relevant portion of Section 139(1) (of Income Tax Act, 1961)

“139. (1) Every person,—

(a) being a company or a firm; or

(b) being a person other than a company or a firm, if his total income or the total income of any other person in respect of which he is assessable under this Act during the previous year exceeded the maximum amount which is not chargeable to income-tax, shall, on or before the due date, furnish a return of his income or the income of such other person during the previous year, in the prescribed form and verified in the prescribed manner and setting forth such other particulars as may be prescribed:

Provided that ………”

Relevant portion of Explanation 2 below Section 139(1) (of Income Tax Act, 1961)

“Explanation 2. – In this sub-section, “due date” means, -

(a) where the assessee [other than an assessee referred to in clause (aa)] is -

(i) a company; or

(ii) a person (other than a company) whose accounts are required to be audited under this Act or under any other law for the time being in force; or

(iii) a working partner of a firm whose accounts are required to be audited under this Act or under any other law for the time being in force,

The [30th day of September] of the assessment year;

[(aa) in the case of an assessee who is required to furnish a report referred to in section 92E (of Income Tax Act, 1961), the 30th day of November of the assessment year;]

(b) in the case of a person other than a company, referred to in the first proviso to this sub-section, the 31st day of October of the assessment year

(c) in the case of any other assessee, the 31st day of July of the assessment year.”

Section 139(4B) (of Income Tax Act, 1961)

“139(4B) The chief executive officer (whether such chief executive officer is known as Secretary or by any other designation) of every political party shall, if the total income in respect of which the political party is assessable (the total income for this purpose being computed under this Act without giving effect to the provisions of section 13A (of Income Tax Act, 1961)) exceeds the maximum amount which is not chargeable to income-tax, furnish a return of such income of the previous year in the prescribed form and verified in the prescribed manner and setting forth such other particulars as may be prescribed and all the provisions of this Act, shall, so far as may be, apply as if it were a return required to be furnished under subsection (1).”

25. As the genesis of the dispute revolves around Section 13A (of Income Tax Act, 1961), we may briefly touch upon the same. Section 13A (of Income Tax Act, 1961) is a special provision relating to incomes of Political Parties. It prescribes that any income of a Political Party under the head – ‘income from house property’, ‘income from other sources or capital gains’ or ‘income by way of voluntary contributions received’ from any person shall not be included in the total income of such Political Party if it fulfils the conditions prescribed thereof. As Section 13A (of Income Tax Act, 1961) stands for the year under consideration, it prescribes that for a Political Party to be eligible for exemption, the following are to be complied with:-

(i) that such Political Party must keep and maintain such books of account and other documents as would enable the Assessing Officer to properly deduce its income therefrom;

(ii) that in respect of each such voluntary contribution other than by way of electrical bond in excess of Rs.20,000/-, such Political Party keeps and maintains a record of such contribution and the name and address of the person who has made such contribution;

(iii) that the accounts of such Political Party are audited by the Accountant as defined in Explanation below Section 288(2) (of Income Tax Act, 1961);

(iv) that it ought not to accept Donations exceeding Rs.2,000/- otherwise than by an account payee cheque or an account payee bank draft or by use of electronic clearing system through a bank or through electoral bond;

(v) that the Treasurer of such Political Party or any other person authorized in this behalf shall submit the report under Section 29C(3) of The Representation of the People Act, 1951; and,

(vi) that such Political Party furnishes a Return of income for the relevant year in accordance with the provisions of Section 139(4B) (of Income Tax Act, 1961) on or before the due date under that Section.

26. The phraseology of Section 13A (of Income Tax Act, 1961) shows that the conditions prescribed therein are pre-requisites for a Political Party claiming exemption under Section 13A (of Income Tax Act, 1961). In the instant case, the pre-requisites for the assessee-Political Party to exclude its voluntary contributions received and other incomes from the total income is subject to the fulfillment of the conditions prescribed therein. The scope and nature of the conditions prescribed in Section 13A (of Income Tax Act, 1961) has been a subject-matter of consideration by the Hon'ble Delhi High Court in assessee’s own case for Assessment year 1994-95 vide ITA Nos.145 and 180 of 2001 dated 23rd March, 2016 (supra).

The relevant discussion in the judgment of the Hon’ble High Court is as follows:-

“Given the context in which section 13A (of Income Tax Act, 1961) was introduced, it was critical from the point of view of the Legislature that political parties are made to disclose what their state of financial affairs is in any given financial year. It was felt necessary to make them account for the receipts and expenses in any financial year. After all, political parties do deal with monies contributed by the public. Political parties are purportedly incurring expenses for their political activities. It is with a view to placing a check on the financial transactions of political parties that the proviso to section 13A (of Income Tax Act, 1961) was enacted. In this context, the object of section 13A (of Income Tax Act, 1961) will be defeated if the compliance with the requirements of the proviso thereto are held not to be mandatory.

94. Section 13A (of Income Tax Act, 1961) has to be read as a whole. It is a provision beneficial to a political party. It exempts various items of income of a political party from tax. If it has to be strictly construed, so too should the conditionality attached to section 13A (of Income Tax Act, 1961). If a political party seeks exemption from paying Income-tax in a particular assessment year, it is incumbent on such political party to strictly comply with each of the requirements in the proviso to section 13A (of Income Tax Act, 1961) and to do so by the time the assessment is completed.”

27. Thus, as per the Hon’ble High Court, compliance with the conditions prescribed in Section 13A (of Income Tax Act, 1961) is mandatory for a Political Party in order to be eligible for the claim of exemption under Section 13A (of Income Tax Act, 1961).

28. Therefore, the assessee’s case for exemption under Section 13A (of Income Tax Act, 1961) has to be examined in the aforesaid light. The first case by the Assessing Officer is qua the third Proviso to Section 13A (of Income Tax Act, 1961). The compliance with the third Proviso can be understood as being two-fold. First, that a Political Party is required to furnish its return of income in accordance with the provisions of sub-section (4B) of Section 139 (of Income Tax Act, 1961); and, second that such return is to be furnished “on or before the due date under that Section”. So far as the first essential is concerned, the same has been complied with inasmuch as there is no dispute that assessee has filed its return of income; in order to examine the second essential of the Proviso, one has to decipher the meaning of ‘due date’ for furnishing of return as envisaged in the third Proviso to Section 13A (of Income Tax Act, 1961). For this purpose, we may go to sub-section (1) of Section 139 (of Income Tax Act, 1961), which requires an assessee to furnish its return of income on or before the ‘due date’.

Explanation 2 thereof enumerates the ‘due date’ applicable to the different category of assessees, and, insofar as the due date applicable in the instant case is concerned, there is no dispute between the parties that the same is 31st December, 2018 (since extended from 30th September, 2018). Ostensibly, the return of income has been filed on 2nd February, 2019, which is beyond the due date. Consequently, there is an apparent non-compliance with the requirements of the third Proviso to Section 13A (of Income Tax Act, 1961).

29. The defense of the assessee, which has been strenuously put forth by the learned Senior Counsel, is based on the provisions of sub-section (4) of Section 139 (of Income Tax Act, 1961), which read as under :-

“139(4) Any person who has not furnished a return within the time allowed to him under sub-section (1), may furnish the return for any previous year at any time before the end of the relevant assessment year or before the completion of the assessment, whichever is earlier.”

30. The aforesaid sub-section provides that any person who has not furnished return within the time allowed under sub-section (1), may furnish the return belatedly at any time before the end of the relevant assessment year or before the completion of the assessment, whichever is earlier. As per the learned Senior Counsel, sub-section (4) is a provision adjunct to sub-section (1), since both appear in Section 139 (of Income Tax Act, 1961) and, therefore, so long as a return of income is filed within the time allowed under sub-section (4) of Section 139 (of Income Tax Act, 1961), it should be considered as compliant with the requirements of the third Proviso to Section 13A (of Income Tax Act, 1961).

31. We have considered the above plea. The third Proviso, as reproduced by us in the earlier part of this order, was inserted in Section 13A (of Income Tax Act, 1961) by the Finance Act, 2017 with effect from 1st April, 2018. As per the Memorandum explaining the provisions introduced in the Parliament, it was noted that Political Parties were required to file their return of income in terms of Section 139(4B) (of Income Tax Act, 1961); So, however, the filing of the return was not a condition precedent for availing exemption under Section 13A (of Income Tax Act, 1961). The Proviso was introduced to make it mandatory for a Political Party seeking exemption under Section 13A (of Income Tax Act, 1961) to furnish its return of income for the relevant year on or before the due date under section 139 (of Income Tax Act, 1961).

32. In this context, the learned Senior Counsel submitted that since Section 139(4B) (of Income Tax Act, 1961) provides that “all the provisions of this Act” shall apply to a return filed by a political party “as if it were a return furnished under subsection (1) of Section 139 (of Income Tax Act, 1961)”, therefore, it would encompass sub-section (4) of Section 139 (of Income Tax Act, 1961) also.

33. In our view, the said argument is quite misplaced as it would negate the purpose for which the third Proviso has been inserted by the Finance Act, 2017. Moreover, the third Proviso contains the expression “the due date under section 139 (of Income Tax Act, 1961)” and a plain reading of the provisions shows that the due date for the purpose of Section 139 (of Income Tax Act, 1961) is defined in terms of Explanation 2 below Section 139(1) (of Income Tax Act, 1961) and that such ‘due date’ is not controlled by the provisions of sub-section (4) of Section 139 (of Income Tax Act, 1961), which merely permits filing of belated returns.

34. The above premise gets further strengthened by the following discussion. For that, we may advert to another plea of learned Senior Counsel, based on a CBDT Clarification dated 23rd April, 2019, which related to the assessees claiming exemption under Section 11 (of Income Tax Act, 1961) and 12 of the Act. In this context, it is to be noted that when the amendments were made in Section 13A (of Income Tax Act, 1961) by the Finance Act, 2017, simultaneously, clause (ba) was inserted in sub-section (1) of Section 12A (of Income Tax Act, 1961), which reads as under:-

“(ba) the person in receipt of the income has furnished the return of income for the previous year in accordance with the provisions of sub-section (4A) of section 139 (of Income Tax Act, 1961), within the time allowed under that section.”

35. In terms of the aforesaid, similar condition for filing of return of income in order to claim exemption under Section 11 (of Income Tax Act, 1961) and 12 was inserted, and which is canvassed to be pari materia with the third Proviso to Section 13A (of Income Tax Act, 1961).

In the context of the above amendment, a clarification was issued by the CBDT dated 23rd April, 2019 clarifying that the time allowed for filing of return of income as per the newly inserted clause (ba) for the trusts was the time allowed to file belated returns under Section 139(4) (of Income Tax Act, 1961). As per the CBDT, the trusts who have filed return under Section 139(4) (of Income Tax Act, 1961) need not be refused the exemption for the reason that the return of income filed was not within the due date of filing of the return. It has been canvassed by the learned Senior Counsel that the two provisions being pari materia, similar reasoning should govern the understanding of the condition prescribed in the third Proviso to Section 13A (of Income Tax Act, 1961) with regard to the due date of furnishing of the return.

36. In our view, the plea of the assessee to seek treatment on par with Trusts, is misplaced having regard to the pronouncement of Hon'ble Delhi High Court in assessee’s own case (supra). The following observations of Hon’ble High Court are worthy of notice in this regard:-

“69. Section 2(15) (of Income Tax Act, 1961) defines what is “charitable purpose”.

This is relevant for section 11 (of Income Tax Act, 1961). A political party cannot be said to be carrying on an activity that is comparable to that carried on by a “charitable trust”. Treating the income of a political party to be that of a Trust and using the same principle to test the treatment of its expenses is inconsistent with the very scheme of the Act.

70. It is clear, therefore, that for understanding and interpreting section 13A (of Income Tax Act, 1961), it would serve no purpose to compare it with section 11 (of Income Tax Act, 1961) which applies to trusts.”

37. Furthermore, there is also a subtle difference in the language used by the Legislature while inserting clause (ba) in Section 12A(1) (of Income Tax Act, 1961). In clause (ba), the language used is “within the time allowed under that Section”, whereas the language used in the third Proviso to Section 13A (of Income Tax Act, 1961) is “before the due date under that Section”. Ostensibly, the reference to the ‘due date’ in third Proviso to Section 13A (of Income Tax Act, 1961) has implications quite distinct than the provisions of clause (ba) of Section 12A(i) (of Income Tax Act, 1961). The “due date” for furnishing a return of income is prescribed in Section 139(1) (of Income Tax Act, 1961) read with Explanation (2) thereof, whereas the “time allowed” for furnishing a return of income is prescribed in Section 139(4) (of Income Tax Act, 1961), which permits filing of the belated returns. Thus, the difference in the phraseology clearly shows that in order to claim exemption under Section 13A (of Income Tax Act, 1961), it is necessary to furnish return of income by the ‘due date’ as per Section 139 (of Income Tax Act, 1961), whereas, in order to claim exemption under Section 11 (of Income Tax Act, 1961) and 12, the trusts are permitted to furnish their return of income within the time allowed under Section 139 (of Income Tax Act, 1961), which would include the extended period prescribed by sub-section (4) of Section 139 (of Income Tax Act, 1961). Therefore, the third Proviso to Section 13A (of Income Tax Act, 1961), though providing for a condition similar to that in clause (ba) of Section 12A(1) (of Income Tax Act, 1961) for the trusts, is more onerous. The reason for the same can be understood from the judgment of the Hon'ble Delhi High Court in assessee’s own case itself, which has explained the background, nature and scope of the conditions prescribed in Section 13A (of Income Tax Act, 1961), which we have already adverted to in earlier paragraphs.

38. With regard to the second reason for denial of exemption, namely, violation of clause (d) of the first Proviso to Section 13A (of Income Tax Act, 1961), we have considered the plea of the Applicant. Factually speaking, assessee has received certain sums in cash amounting to Rs.14,49,000/- from various persons, each exceeding Rs.2,000/-. There is no dispute that complete details in this regard viz., names, addresses and permanent account numbers of the contributors have been furnished by the assessee. The Assessing Officer treated the same as violative of clause (d) of the first Proviso inasmuch as Donations exceeding Rs.2,000/- have been received otherwise than by the modes prescribed therein. The assessee submitted that the aforesaid sum was in the nature of ‘voluntary contributions’ and not ‘Donations’ so as to be outside the purview of clause (d) of the first Proviso and falling for consideration only in clause (b) of the first Proviso.

39. After having perused the orders of the authorities below as well as other material, it is borne out that it is only during the assessment proceedings that the assessee has sought to make a distinction between ‘voluntary contributions’ and ‘Donations’. The Assessing Officer has recorded a finding, after examining the books of account that all the contributions have been recorded as ‘Donations’ and the distinction canvassed by the assessee is not supported by the account books maintained. The report filed by the assessee with the Election Commission of India in terms of Section 29C(1) of The Representation of the People Act, 1951 dated 29th September, 2014 also does not support any distinction between receipt of Voluntary Contributions and Donations. All these aspects, in our view, do not inspire any confidence in the plea of the assessee that there is a difference between Voluntary Contributions and Donations. No doubt the details of Rs.14,49,000/- maintained by the assessee is compliant with the requirements of clause (b) of the Proviso, so however, it does not distract from the fact that clause (d) of the first Proviso has been contravened inasmuch as Donations in excess of Rs.2,000/- have been received by the assessee in cash.

40. We may also analyze this aspect from another angle. Clause (b) of the first Proviso requires that in respect of each voluntary contribution in excess of twenty thousand rupees, a Political Party is required to keep and maintain a record of such contribution including the Name and address of the person who has made such contribution; whereas clause (d) of the first Proviso mandates that no Donation exceeding two thousand rupees ought to be received by the Political Party otherwise than by an account payee cheque or bank draft or through electronic clearing system or through electoral bond. Thus, while clause (b) obligates a Political Party to maintain the record and details of the voluntary contributions recorded in excess of twenty thousand rupees, clause (d) restricts a Political Party from receiving Donation in excess of two thousand rupees otherwise than by an account payee cheque or bank draft or through electronic clearing system or through electoral bond.

41. In our considered view, it is incongruent for a Political Party to canvass that inspite of accepting Donations in cash exceeding Rupees two thousand each, clause (d) is not violated merely because it has maintained the details as per clause (b) of the first Proviso. Each of the conditions laid down in clauses (a), (b), (c) and (d) of the first Proviso are to be mandatorily complied with in order to claim exemption under Section 13A (of Income Tax Act, 1961), as per the ratio of the judgment of the Hon'ble Delhi High Court in the case of the assessee (supra).

For a reference, the following discussion by the Hon’ble High Court is relevant:-

“77. …… While it is true that income by way of voluntary contributions is not identified as a separate head of income in Section 14 (of Income Tax Act, 1961), the legislative intent was not to exclude it altogether from the taxable income. It would be excluded only subject to fulfillment of the conditions stipulated under Section 13A (of Income Tax Act, 1961). It could never have been the legislative intention that voluntary contributions received by a political party that does not satisfy the requirement of Section 13A (of Income Tax Act, 1961) – viz., maintaining books of accounts, keeping a record of voluntary contributions in excess of Rs.10,000 and getting the accounts audited – would be exempt from tax. If the above conditions are not fulfilled, the income of a political party by way of voluntary contributions would be included in the taxable income.”

42. In the present case, the detail of Rs.14,49,000/- clearly show that each contribution is in cash in excess of Rs.2,000/-, thereby reflecting clear violation of clause (d) of the first Proviso. At this point, we are conscious of the statement made by the learned Senior Counsel at Bar that out of the sum of Rs.14,49,000/-, a sum of Rs.3,00,000/- has been received by transfer through RTGS. However, even after considering the same, violation of clause (d) to the first Proviso is palpable qua the balance of the amount.

43. Another aspect brought out by the learned Senior Counsel is that the component of Donations received in cash in excess of Rs.2,000/- each was merely 0.1% of the total contribution received and, therefore, the same should not invite wholesale denial of exemption under Section 13A (of Income Tax Act, 1961). In our view, the said plea is manifestly contrary to the understanding placed by the Hon’ble High Court on the provisions of Section 13A (of Income Tax Act, 1961). In fact, the following discussion by the Hon’ble High Court does not leave us in any doubt that once the mandatory requirements contained in Section 13A (of Income Tax Act, 1961) is violated, there is no discretion with the income tax authorities to give any relaxation in allowing the exemption envisaged in the said Section:-

“108. Since no attempt has been made by the Indian National Congress (I) to place before the Assessing Officer, or even before the Commissioner of Income-tax (Appeals), acceptable audited accounts, from which the Assessing Officer could deduce the taxable income of the assessee, the court has no hesitation to hold that the mandatory requirement of the proviso to section 13A (of Income Tax Act, 1961) was not fulfilled by the assessee. Such a failure could not have been condoned either by the Commissioner of Income-tax (Appeals) or the Assessing Officer.”

44. Therefore, the Revenue is justified in relying on the findings of the Assessing Officer to the effect that “the assessee has complied with the provisions of clause (b) but still violated the provisions of clause (d) of first proviso to section 13A (of Income Tax Act, 1961) which clearly prohibit receipt of donation in excess of Rs.2,000/- in cash”.

45. On the basis of the aforesaid discussion, and having regard to the legal position and the material on record, it is reasonable to conclude that the income tax authorities have not made any error in denying the exemption claimed by the assessee under Section 13A (of Income Tax Act, 1961) due to violation of clause (d) of the first Proviso as well as third Proviso to Section 13A (of Income Tax Act, 1961). Consequently, in our view, the Applicant has been unable to make out a strong prima facie case against the interpretation of Section 13A (of Income Tax Act, 1961) as adopted by the Revenue to deny the exemption, so far it is relevant for the purposes of examining the merits of the present Application.

46. Another aspect which has been argued by the learned Senior Counsel is that the total income has been computed without giving benefit of the expenditure incurred by the assessee for attaining its aims and objects and, therefore, the impugned tax demand has been unjustly raised. We find that this aspect does not require much indulgence from our side inasmuch as the same has been authoritatively negated by the Hon'ble Delhi High Court vide its Order dated 23rd March, 2016 (supra). As per the Hon'ble High Court, once the income by way of voluntary contributions is not excludible from total income on account of denial of exemption under Section 13A (of Income Tax Act, 1961), the same is liable to be treated as “income from other sources”. Thereafter, the question of allowability of expenditure incurred by a Political Party for attaining its aims and objects was declined by the Hon'ble Delhi High Court in the following words :-

“Expenditure of a political party

123. Here it is important to address another submission made on behalf of the Revenue which finds favour with the court. Under the head “Income from other sources”, no expenditure can be allowed as a deduction on the ground that the expenditure has been incurred by a political party for attaining the aims and objects of political party. As rightly pointed out, the only deduction is under section 57(iii) (of Income Tax Act, 1961) and this cannot be granted since the Indian National Congress (I) did not place on record the factual basis for such a claim.

124. The legal position is that no deduction can be allowed with respect to the expenditure incurred by the political party for any purpose whatsoever if it fails to comply with the basic requirements of section 13A (of Income Tax Act, 1961).

125. Therefore, the only way to proceed in the present matter is to wholly disallow the expenditure claimed by the Indian National Congress (I) as relatable to “income from other sources”. On the receipts side, the Revenue will simply have to go by whatever is disclosed by the Indian National Congress (I) as income by way of voluntary contributions in the return as originally filed and treat that as income from other sources.

126. Consequently, the court disagrees with the decision of the Commissioner of Income-tax (Appeals) restricting the expenditure of the assessee to 60 per cent. of the amount claimed and order of the Commissioner of Income-tax (Appeals) and the Income-tax Appellate Tribunal to that extent are set aside.”

(underlined for emphasis by us)

47. We may now refer to the opening argument made by the learned Senior Counsel for the Applicant on the issue of hardship created for the assessee by the recovery proceedings initiated under Section 226(3) (of Income Tax Act, 1961) on 13th February, 2024. According to him, the action of the Assessing Officer was lacking in bona fides as it had been initiated close to the ensuing Parliamentary Elections. This aspect of the matter is quite subjective, and we have considered the same only for the limited purpose of evaluating the merit of the extant interim Application before us. The chronology of events, which have been canvassed before us starting from the passing of the assessment order on 6th July, 2021 and culminating with the issuance of notice under section 226(3) (of Income Tax Act, 1961) on 13th February, 2024, in our view, does not justify an inference that the recovery proceedings have been done in an undue haste.

In the first point of time, when the assessee approached the Assessing Officer for stay during pendency of the Appeal with the CIT(Appeals), the Assessing Officer was willing to keep the recovery in abeyance requiring the assessee to pay 20% of the disputed demand. Even after the rejection of Appeal by the CIT(Appeals) on 28th March, 2023, no recovery action seems to have been initiated by the Assessing Officer to recover the demand till 13th February, 2024. On the other hand, the assessee has also not demonstrated its keenness to expeditiously settle the issue inasmuch as the Appeal of the assessee pending with the Tribunal had come up for hearing on three occasions, viz., 21st September, 2023, 28th November, 2023 and 5th February, 2024 and, on each of the occasion, the record of proceedings reveal that the appellant assessee was not prepared and sought adjournment. Now, the Appeal is fixed for hearing on 23rd April, 2024 before the regular Bench. Even in the course of hearing of the present petition, it was put across to the parties that since extensive arguments were being advanced, the Appeal pending before the Tribunal may be taken up for hearing on merits to facilitate an expeditious disposal of the same. The learned Standing Counsel had no objection to the same, while the learned Senior Counsel appearing for the Applicant did not opt for the same. Be that as it may, we are pointing out the aforesaid only to emphasize that the power to grant the stay is exercised inter alia, in cases where a delay can be expected in the determination of the pending Appeal in the due course. So however, in the instant case, the delay in determination of Appeal, if any, is not attributable to the Revenue.

48. In these circumstances, we do not find that the recovery notice under Section 226(3) (of Income Tax Act, 1961) issued by the Assessing Officer on 13th February, 2024 is lacking in bona fides, so as to require us to intervene.

49. At this stage, we may also refer to the reliance placed by the learned Senior Counsel on various judgments of the Coordinate Benches in order to support the proposition that it was an accepted practice at the level of the Tribunal that taxpayer is entitled to a stay on the recovery proceedings on payment of 20% of the demand during the pendency of the Appeal before the Tribunal. The aforesaid argument, in our view, is too general and does not merit acceptance. Moreover, as we have already discussed in the earlier paragraphs, each Application for stay has to be decided on its own facts and circumstances, and there can be no generalized approach.

50. The Stay Application is without merit and, it is dismissed accordingly.

51. Before parting, we may clarify that any observations made in the foregoing are only for the purpose of deciding this Stay Application and shall have no effect on the merits of the case, which shall be decided in the course of determination of the Appeal of the assessee pending with the Tribunal.

Decision pronounced in the open Court on 8th March, 2024.

Sd/- Sd/-

(ANUBHAV SHARMA) (G.S. PANNU)

JUDICIAL MEMBER VICE PRESIDENT

×