Its true that AO should corroborate section 133A (of Income Tax Act, 1961) oath…

Full News

Its true that AO should corroborate section 133A (of Income Tax Act, 1961) oaths, but in section 69 (of Income Tax Act, 1961) (unexplained investments) cases corroboration onus shifts on the assessee

Its true that AO should corroborate section 133A (of Income Tax Act, 1961) oaths, but in section 69 (of Incom…

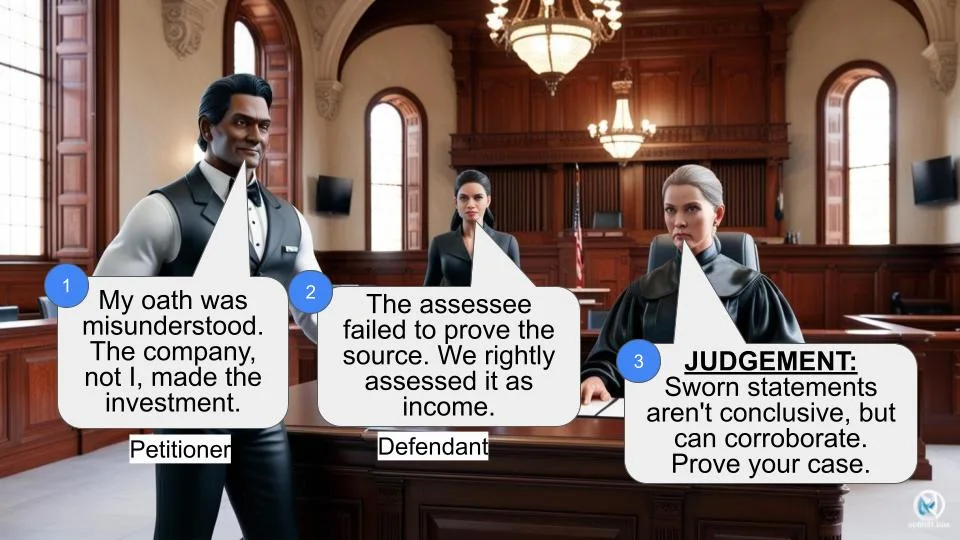

The Kerala High Court clarified that the statement made on oath by an assessee during survey proceedings is not conclusive and can be explained or withdrawn by the assessee. Assessment of tax cannot be solely based on the sworn statement made by the assessee under Section 133A(3)(iii) (of Income Tax Act, 1961). The burden of proving the source of a sum of money received by an assessee is on the assessee, and where an assessee fails to prove satisfactorily the source and nature of an investment, the Income Tax Officer is entitled to draw the inference that the amount is of an assessable nature. The discretion conferred on the Income Tax Officer under Section 69 (of Income Tax Act, 1961) to treat the source of investment as the income of the assessee must be exercised based on the facts and circumstances of the particular case.

Get the full picture - access the original judgement of the court order here

Case Name:

C.K. Abdul Azeez v. Commissioner of Income Tax, Central Circle, Calicut(High Court of Kerala)

ITA.No.19 of 2019

Date: 05 September 2019

Key Takeaways:

1. The income tax authority has the power to record the statement of any person, including an assessee, during survey proceedings under Section 133A (of Income Tax Act, 1961).

2. The statement made on oath by an assessee during survey proceedings is not conclusive and can be explained or withdrawn by the assessee.

3. Assessment of tax cannot be solely based on the sworn statement made by the assessee under Section 133A(3)(iii) (of Income Tax Act, 1961).

4. The burden of proving the source of a sum of money received by an assessee is on the assessee.

5. Where an assessee fails to prove satisfactorily the source and nature of an investment, the Income Tax Officer is entitled to draw the inference that the amount is of an assessable nature.

6. The discretion conferred on the Income Tax Officer under Section 69 (of Income Tax Act, 1961) to treat the source of investment as the income of the assessee must be exercised based on the facts and circumstances of the particular case.

Issue:

The central legal question in this case is whether a statement made on oath by an assessee (taxpayer) to the income tax authority during survey proceedings under Section 133A (of Income Tax Act, 1961) has any evidentiary value and can be used as the sole basis for making an assessment of tax.

Facts:

A search was conducted at the residential premises of Mr. Sainul Abdheen, a director of Parathode Granites Private Limited (the company).

During the search, an agreement executed by the appellant (assessee), who was the Managing Director of the company, for purchasing land worth Rs. 90 lakhs was found.

During subsequent survey proceedings under Section 133A (of Income Tax Act, 1961), the assessee gave a sworn statement on 11.03.2011 that he had paid Rs. 95 lakhs as advance for the property.

Later, the assessee claimed in a letter dated 04.03.2013 that the agreement was executed in his capacity as the Managing Director, the amount was invested from the company’s funds, and the deal was cancelled.

The company’s books did not reflect the investment of Rs. 95 lakhs.

Arguments:

Assessee’s argument:

The statement made on oath during the survey proceedings has no evidentiary value as the income tax authority has no power to examine on oath under Section 133A (of Income Tax Act, 1961). The assessment cannot be made solely based on this statement.

Revenue’s argument:

The assessee admitted in the sworn statement that he invested Rs. 95 lakhs. He failed to establish that the amount was invested by the company and not him personally.

Key Legal Precedents:

- Paul Mathews and Sons v. Commissioner of Income Tax (2003):

This case held that the income tax authority has no power to administer oath and record sworn statements under Section 133A (of Income Tax Act, 1961), and such statements have no evidentiary value.

- Commissioner of Income Tax v. Hotel Samrat (2010):

This case stated that the view in Paul Mathews does not lay down the correct law, and statements recorded under Section 133A(3)(iii) (of Income Tax Act, 1961) have corroborative value in assessments.

- Travancore Diagnostics (P) Limited v. Assistant Commissioner of Income Tax (2016):

This case clarified that the statement made under Section 133A (of Income Tax Act, 1961) is not conclusive, and the assessee can resile from it. However, it can be used to corroborate other materials.

- Govindarajulu Mudaliar v. Commissioner of Income Tax (1959):

The burden is on the assessee to prove the source of investments. If not satisfactorily explained, the Income Tax Officer can treat it as assessable income.

- Roshan Di-Hatti v. Commissioner of Income Tax (1977):

If the source of a receipt cannot be satisfactorily explained, the revenue can treat it as the assessee’s income.

Judgment:

The court harmonized the precedents and held that:

The income tax authority has the power to record statements under Section 133A(3)(iii) (of Income Tax Act, 1961), including sworn statements, though not specifically empowered to examine on oath.

A sworn statement made under Section 133A (of Income Tax Act, 1961) is not conclusive evidence and can be resiled from by the assessee.

However, such a statement can be used to corroborate other materials before the assessing authority.

The assessment in this case was not made solely based on the sworn statement but also on the agreement found during the search and the assessee’s failure to establish that the investment was made by the company.

The assessee, being the Managing Director, could have produced records to prove the company’s investment but failed to do so.

The Tribunal’s factual findings were not perverse, and there was no ground to interfere.

Therefore, the court dismissed the assessee’s appeal, upholding the Tribunal’s order treating the Rs. 95 lakhs as the assessee’s unexplained investment under Section 69 (of Income Tax Act, 1961).

FAQ

Q1: Does a statement made on oath during survey proceedings under Section 133A (of Income Tax Act, 1961) have any evidentiary value?

A1: A sworn statement made under Section 133A (of Income Tax Act, 1961) is not conclusive evidence and can be resiled from by the assessee. However, such a statement can be used to corroborate other materials before the assessing authority.

Q2: Can the income tax authority examine on oath under Section 133A (of Income Tax Act, 1961)?

A2: The income tax authority has the power to record statements under Section 133A(3)(iii) (of Income Tax Act, 1961), including sworn statements, though not specifically empowered to examine on oath.

Q3: Can the assessment be made solely based on the sworn statement made during survey proceedings under Section 133A (of Income Tax Act, 1961)?

A3: The assessment cannot be made solely based on the sworn statement made during survey proceedings under Section 133A (of Income Tax Act, 1961).

1. What is the evidentiary value of a statement made on oath by the assessee to the income tax authority in survey proceedings held under Section 133A (of Income Tax Act, 1961) (hereinafter referred to as 'the Act')? This is the core issue for consideration in this appeal.

2. A search under Section 132 (of Income Tax Act, 1961) was conducted at the residential premises of Mr.Sainul Abdheen, one of the Directors of the company by name 'Parathode Granites PrivateLimited' (hereinafter referred to as 'the company'). During the search, an agreement executed by the appellant/ assessee, who was the Managing Director of the company, for purchase of land having an extent of 28.75 acres, was found and seized. This document revealed that the appellant had given 90 lakhs rupees as advance for purchase of the property. Thereafter, survey proceedings under Section 133A (of Income Tax Act, 1961) were conducted at the premises of the company. During the survey proceedings, the assessee gave a statement on oath on 11.03.2011 to the income tax authority that he had given an amount of 95 lakhs rupees as advance for purchase of the property. Subsequently, the appellant sent a letter dated 04.03.2013 to the department. In that letter he took the plea that he had executed the agreement in the capacity as the Managing Director of the company and that the amount of 95 lakhs rupees was invested out of the funds of the company and that he had not made any personal investment in the deal and also that the deal was subsequently cancelled by the company.

3. The assessing officer did not accept the explanation given by the appellant regarding the nature and source of the amount. The assessing officer found that the books of accounts of the company did not reveal that the amount of 95 lakhs rupees was invested by the company in such a deal. Therefore, the aforesaid amount was brought to tax by the assessing authority as unexplained investment.

4. The appellant took up the matter in appeal before the Commissioner of Income Tax (Appeals). The appellate authority agreed with the view taken by the assessing officer and dismissed the appeal. The appellant filed further appeal before the Income Tax Appellate Tribunal. The Tribunal confirmed the findings made by the assessing officer and the appellate authority and dismissed the appeal. The aforesaid order of the Tribunal is under challenge in this appeal filed by the assessee.

5. We have heard Sri.Arun Raj.S, learned counsel for the appellant and also Sri.Jose Joseph, learned Standing Counsel for the department.

6. Learned counsel for the appellant contended that the agreement for purchase of property was executed by the appellant in his capacity as the Managing Director of the company and that the investment was made out of the funds of the company and that he had not made any personal investment. Learned counsel has also contended that no assessment could have been made based solely on the sworn statement given by the assessee before the income tax authority during the survey proceedings. Learned counsel has further contended that, during the survey proceedings, the income tax authority has no power to examine on oath any person and that such a statement made on oath by the assessee has got no evidentiary value.

7. Per contra, learned Standing Counsel for the department would contend that the appellant had admitted in the sworn statement given before the income tax authority that he had invested 95 lakhs rupees in the deal. Learned Standing Counsel for the department would also contend that the appellant/assessee failed to establish his plea that the amount was invested not by him but by the company and in such circumstances, the assessing authority was right in bringing the amount to tax as unexplained investment under Section 69 (of Income Tax Act, 1961).

8. No question regarding the evidentiary value of the statement made on oath by the assessee to the income tax authority during the survey proceedings under Section 133A (of Income Tax Act, 1961) was raised by the assessee before the assessing officer or the appellate authority or even before the Tribunal. No such question of law has been raised by the appelant/assessee in the memorandum of appeal filed in this Court also. However, in view of the submissions made by the learned counsel for the appellant/assessee, we are inclined to raise and consider the following substantial questions of law:

(1) Has the income tax authority got power to examine on oath any person during survey proceedings under Section 133A (of Income Tax Act, 1961)?

(2) Is it correct proposition of law that a statement made on oath by the assessee before the income tax authority during the survey proceedings under Section 133A (of Income Tax Act, 1961) has no evidentiary value at all?

(3) Is it permissible under law to make assessment of tax solely on the basis of the statement made on oath by an assessee before the income tax authority during the survey proceedings under Section 133A (of Income Tax Act, 1961)?

9. Section 133A (of Income Tax Act, 1961) deals with survey proceedings. Section 133A(3)(iii) (of Income Tax Act, 1961) provides that an income-tax authority acting under Section 133A (of Income Tax Act, 1961) may record the statement of any person which may be useful for, or relevant to, any proceeding under the Act. It is evident from this provision that, during survey proceedings, the income-tax authority has got power to record the statement of any person. The expression “any person” in this provision includes an assessee.

10. Learned counsel for the appellant relied upon the decision of a Division Bench of this Court in Paul Mathews and Sons v. Commissioner of Income Tax : (2003) 263 ITR 101 in support of his contention that the income tax authority has got no power to examine on oath any person or to record any sworn statement of a person. Learned counsel has also pointed out that the decision in Paul Mathews (supra) has been relied upon by the Madras High Court in Commissioner of Income Tax v. Khader Khan Son : (2008) 300 ITR 157.

11. In Paul Mathews (supra), the Division Bench has held as follows:

"Section 133A(3)(iii) (of Income Tax Act, 1961) enables the authority to record the statement of any person which may be useful for, or relevant to, any proceeding under the Act. Section 133A (of Income Tax Act, 1961), however, enables the income-tax authority only to record any statement of any person which may be useful, but does not authorize taking any sworn statement. On the other hand, we find that such a power to examine a person on oath is specifically conferred on the authorised officer only under Section 132(4) (of Income Tax Act, 1961) in the course of any search or seizure.

Thus, the Income Tax Act, whenever it thought fit and necessary to confer such power to examine a person on oath, the same has been expressly provided whereas Section 133A (of Income Tax Act, 1961) does not empower any Income Tax Officer to examine any person on oath. Thus, in contradistinction to the power under Section 133A (of Income Tax Act, 1961), Section 132(4) (of Income Tax Act, 1961) enables the authorised officer to examine a person on oath and any statement made by such person during such examination can also be used in evidence under the Income Tax Act.

On the other hand, whatever statement is recorded under Section 133A (of Income Tax Act, 1961) it is not given any evidentiary value obviously for the reason that the officer is not authorised to administer oath and to take any sworn statement which alone has evidentiary value as contemplated under law. Therefore, there is much force in the argument of learned counsel for the appellant that the statement elicited during the survey operation has no evidentiary value”.

12. It can be seen that in Paul Mathews (supra), the Division Bench had categorically held that, whatever statement is recorded under Section 133A (of Income Tax Act, 1961), it is not given any evidentiary value obviously for the reason that the officer is not authorised to administer oath and to take any sworn statement.

13. At this juncture, we may notice that another Division Bench of this Court in Commissioner of Income Tax v. Hotel Samrat : (2010) 323 ITR 353, stated that the view taken in Paul Mathews (supra) does not lay down the correct law. However, the issue was not referred to a Full Bench as it was not necessary to do so in that case. In Hotel Samrat (supra), it was observed as follows:

“During hearing, we felt that the decision of this Court in Paul Mathews and Sons reported in [2003] 263 ITR 101 above referred to does not lay down the correct position of law because, in our view, statement recorded under Section 133A(3)(iii) (of Income Tax Act, 1961) though cannot be treated as independent evidence like evidence recorded under Section 132(4) (of Income Tax Act, 1961), has corroboratory value in assessment and statement recorded under the said provision can be even relied on by the assessee. In other words, the decision of this Court that the statement recorded under the above provision does not have evidentiary value, in our view, does not lay down the correct law. However, since counsel for the respondent- assessee does not rely on the above decision, we proceed to consider these cases on the merits without referring the matter for consideration to a Full Bench because by the operation of the latter part of the section, such statement has relevance for assessment and other proceeding under the Act”.

14. Another Division Bench of this Court considered the issue in Travancore Diagnostics (P) Limited v. Assistant Commissioner of Income Tax: 2016 (5) KHC 580 : 2016 (4) KLT 350. In that case, the Division Bench clarified the dictum laid down in Paul Mathews (supra) as follows:

“For the purpose of this case, we do not think that it is necessary to venture into a question as to whether Paul Mathew and Sons lays down the right law. Even taking the dicta in Paul Mathew and Sons as the correct law, it is clear from the judgment that what this Court had said is that the statement made by the assessee under Section 133A (of Income Tax Act, 1961) is not conclusive and that it is open to the person who made the admission to resile from it and to state the same to be incorrect, in which event, the assessee should be given an opportunity to show that the books of account discloses the correct statement of facts. We draw support for our opinion from the judgment of the Hon'ble Supreme Court in Pullangode Rubber Produce Co. Ltd. v. State of Kerala, 1973 (91) ITR 18 (SC). The position appears to be clear that the person making the admission or the statement will be at liberty to withdraw from the statement or admission, since such statement had not been made under Section 132(4) (of Income Tax Act, 1961), which provides for a sworn statement, but one under Section 133A (of Income Tax Act, 1961)”.

(emphasis supplied).

15. Section 133A(3)(iii) (of Income Tax Act, 1961) empowers the income tax authority to record the statement of a person including an assessee. Section 133A (of Income Tax Act, 1961), unlike Section 132(4) (of Income Tax Act, 1961), does not specifically empower the income tax authority to examine a person on oath. There can be no quarrel with this proposition laid down in Paul Mathews (supra). However, Section 133A (of Income Tax Act, 1961) does not also prohibit the income tax authority to administer oath to a person. As in the case of an accused in a criminal proceedings, there is no specific prohibition as contained in Section 4(2) of the Oaths Act, 1969 against administering oath to an assessee in the proceedings under Section 133A (of Income Tax Act, 1961). The status of an assessee in the proceedings under Section 133A (of Income Tax Act, 1961) cannot be equated to the status of an accused in a criminal case. Therefore, merely by reason of the fact that the income tax authority has administered oath to an assessee and recorded his sworn statement during the survey proceedings under Section 133A (of Income Tax Act, 1961), it cannot be found that such statement has no evidentiary value at all and that it cannot be used in any manner against the assessee in any proceedings under the Act. As explained in Travancore Diagnostics (supra), the statement on oath made by an assessee to the income tax authority during the survey proceedings under Section 133A (of Income Tax Act, 1961) is not conclusive. The assessee can explain or withdraw the admission, if any, made by him in such statement.

Assessment of tax cannot be made solely on the basis of such sworn statement made by the assessee under Section 133A(3)(iii) (of Income Tax Act, 1961). At the same time, such statement can be used to corroborate other materials before the assessing authority, including the contents of any document. In our view, the dictum laid down in Paul Mathews (supra) and Hotel Samrat (supra) and Travancore Diagnostics (supra) can be harmonised in this manner without any conflict. Thus, the substantial questions of law raised as items (1) and (3) are answered in favour of the assessee and against the revenue. The substantial question of law raised as item No.(2) is answered in favour of the revenue and against the assessee.

16. Section 69 (of Income Tax Act, 1961) provides that, where in the financial year immediately preceding the assessment year, the assessee has made investments which are not recorded in the books of account, if any, maintained by him for any source of income, and the assessee offers no explanation about the nature and source of the investments or the explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, the value of the investments may be deemed to be the income of the assessee of such financial year.

17. The burden is on the assessee to prove or explain the source of the money or investment. Where an assessee fails to prove satisfactorily the source and nature of the investment, the Income Tax Officer is entitled to draw the inference that the amount is of an assessable nature (See Govindarajulu Mudaliar v. Commissioner of Income Tax : AIR 1959 SC 248). The law is well settled that the onus of proving the source of a sum of money received by an assessee is on him. Where the nature and source of a receipt, whether it be of money or of other property, cannot be satisfactorily explained by the assessee, it is open to the revenue to hold that it is the income of the assessee and no further burden lies on the revenue to show that income is from any particular source (See Roshan Di-Hatti v. Commissioner of Income Tax : AIR 1977 SC 1605). The question whether the source of the investment should be treated as income or not under Section 69 (of Income Tax Act, 1961) has to be considered in the light of the facts of each case. In other words, a discretion has been conferred on the Income tax Officer under Section 69 (of Income Tax Act, 1961) to treat the source of investment as the income of the assessee if the explanation offered by the assessee is not found satisfactory and the said discretion has to be exercised keeping in view the facts and circumstances of the particular case (See Commissioner of Income Tax v. P.K.Noorjahan : AIR 1999 SC 1600).

18. In the instant case, there is no dispute with regard to the fact that the appellant had paid 95 lakhs rupees as advance for purchasing a property. His plea is that the investment was made by him in his capacity as the Managing Director of the company and not in his personal capacity and that the amount came out of the funds of the company. The books of account of the company did not reveal any such transaction or investment made by the company. Therefore, the assessing officer was not satisfied about the explanation given by the appellant/assessee. The assessee is none other than the Managing Director of the company. He could have easily produced records or materials to show that the amount was actually invested by the company and not by him in his personal capacity. In the absence of any such materials produced, the assessing officer was justified in rejecting the explanation given by the appellant and in bringing the amount to tax as unexplained investment.

19. The assessment of tax made by the authority concerned is not solely based on the sworn statement of the appellant given to the income tax authority. The basis of the assessment is the agreement executed by the appellant for purchase of property and also the circumstance that the appellant failed to establish his plea regarding the investment made. The sworn statement of the appellant only corroborates those materials. The fact that the assessing authority gave emphasis to the sworn statement of the appellant while passing the order of assessment does not change this fact situation.

20. The Tribunal has adverted to the factual aspects and confirmed the findings made by the assessing authority and the appellate authority. The conclusion reached by the Tribunal on a finding of fact cannot be interfered with by this Court unless it is shown that it is perverse or that the Tribunal had acted without any materials. In the instant case, the factual findings made by the Tribunal do not suffer from any such error or illegality or perversity. In such circumstances, we find no sufficient ground to interfere with the findings of the Tribunal. The appeal is liable to be dismissed.

Consequently, the appeal is dismissed. No costs.

(sd/-)

C.K.ABDUL REHIM, JUDGE

(sd/-)

R.NARAYANA PISHARADI, JUDGE

×

Similar Ripples

Questions

Its true that AO should corroborate section 133A (of Income Tax Act, 1961) oaths, but in section 69 (of Income Tax Act, 1961) (unexplained investments) cases corroboration onus shifts on the assessee

Write your CommentSimilar Posts

Generic

- Reportdata/4794.pdf