No Incriminating Material, No Tax Addition: Court Upholds Tribunal’s Decision

Full News

No Incriminating Material, No Tax Addition: Court Upholds Tribunal’s Decision

No Incriminating Material, No Tax Addition: Court Upholds Tribunal’s Decision

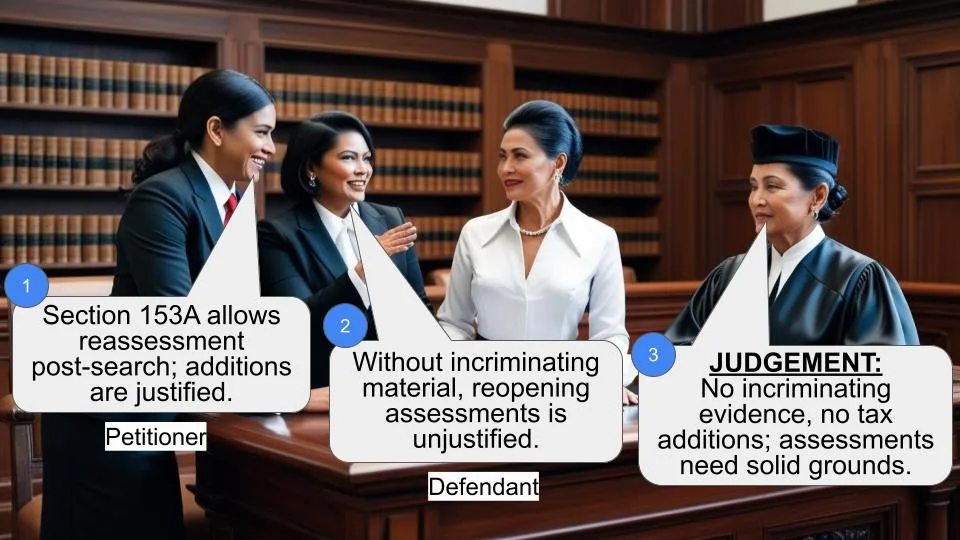

The case involves the Income Tax Department and an assessee, where the central issue was whether additions could be made under Section 153A (of Income Tax Act, 1961) when no incriminating material was found during a search. The court upheld the tribunal’s decision to delete the additions, emphasizing that without incriminating evidence, no additional tax assessments should be made.

Get the full picture - access the original judgement of the court order here

Case Name:

Principal Commissioner of Income Tax Vs. Dipak Jashvantlal Panchal (High Court of Gujarat)

Tax Appeal No. 110, 111, 115 & 116 of 2017

Date: 14th February 2017

Key Takeaways:

- Section 153A (of Income Tax Act, 1961): This section is triggered by a search or requisition and allows for the assessment of income for six preceding years.

- Incriminating Material: Additions to income can only be made if incriminating material is found during the search.

- Legal Precedent: The court relied on previous decisions, including those from the Delhi High Court and Rajasthan High Court, to support its ruling.

- Tribunal’s Role: The tribunal’s decision to delete the additions was upheld, reinforcing the principle that assessments must be based on evidence found during searches.

Issue

Can the Income Tax Department make additions to an assessee’s income under Section 153A (of Income Tax Act, 1961) if no incriminating material is found during a search?

Facts

The case arose from a search conducted on the assessee, Dipak Jashvantlal Panchal, under Section 132 (of Income Tax Act, 1961). The Assessing Officer made additions to the assessee’s income for the years 2000-2001 to 2004-2005 based on the search. However, the assessee argued that no incriminating material was found to justify these additions.

Arguments

- Income Tax Department: Argued that the additions were justified under Section 153A (of Income Tax Act, 1961), which allows for reassessment following a search.

- Assessee: Contended that without incriminating material, the completed assessments should not be reopened or altered.

Key Legal Precedents

- Kabul Chawla Case: The Delhi High Court decision emphasized that additions under Section 153A (of Income Tax Act, 1961) require incriminating material.

- Jai Steel (India), Jodhpur v. Assistant Commissioner of Income Tax: The Rajasthan High Court held that without incriminating material, earlier assessments should be reiterated.

Judgement

The court upheld the tribunal’s decision to delete the additions made by the Assessing Officer. It agreed with the tribunal that without incriminating material found during the search, no additions could be made under Section 153A (of Income Tax Act, 1961). The court emphasized that the purpose of Section 153A (of Income Tax Act, 1961) is to assess undisclosed income found during a search, not to reassess completed assessments without new evidence.

FAQs

Q1: What is Section 153A (of Income Tax Act, 1961)?

A1: It allows for the assessment of income for six years preceding a search or requisition, but additions can only be made based on incriminating material found during the search.

Q2: Why was the tribunal’s decision upheld?

A2: The tribunal’s decision was upheld because it correctly applied the legal principle that without incriminating material, no additions should be made under Section 153A (of Income Tax Act, 1961).

Q3: What does this decision mean for taxpayers?

A3: It reinforces the protection for taxpayers that completed assessments cannot be arbitrarily reopened without new evidence found during a search.

1.00. As common question of law and facts arise in this group of appeals and are between the same parties but with respect to different assessment years, all these appeals are decided and disposed of by this common order.

2.00. Feeling aggrieved and dissatisfied with the impugned common judgement and order passed by the learned Income Tax Appellate Tribunal, Ahmedabad

(hereinafter referred to as “the learned tribunal”) in I.T.A. Nos.371/AHD/2011, 372/AHD/2011 and 373/AHD/2011 and Cross Objection No.125 of 2011, by which the learned tribunal has partly allowed the said appeals preferred by the common assessee and has deleted the additions made by the A.O., made under section 153(A) (of Income Tax Act, 1961), 1961 for the A.Ys. 2000-2001 to 2004-2005, revenue has preferred present Tax Appeals with the following proposed questions of law :-

“[a] Whether on the facts and in the circumstances of

the case, the Appellate Tribunal is right in law in

narrowing down the scope of assessment u/s. 153(A) (of Income Tax Act, 1961) in

respect of completed assessment by holding that only

undisclosed income and undisclosed assets detected

during the search could be brought to tax ?

[b] Whether on the facts and in the circumstances of

the case, the Appellate Tribunal is correct in law in

holding the scope of section 153(A) (of Income Tax Act, 1961) is limited to

assessing only search releated income, thereby denying

Revenue the opportunity of taxing other escaped

income, that comes to the notice of the Assessing

Officer ?

[c] Whether on the facts and in the circumstances of

the case, the Appellate Tribunal was right in law in

limiting the scope of Section 153(A) (of Income Tax Act, 1961) only to undisclosed

income when as per the section the Assessing officer

has to assess the total income of the six assessment

years ?

[d] Whether the findings of the Tribunal that no

incriminating material is found is perverse inasmuch as

incriminating documents were found, though pertaining

to the other Assessment years which could be linked

with the present Assessment Year?”

3.00. Facts leading to the present appeals, in nutshell,

are as under :-

3.01. That a warrant of authorization under section

132(1) of the Act was issued and executed in the case of the

assessee on 10/2/2006. Thereafter, proceedings under section

153(A) of the Act were initiated and notice under section

153(A) of the Act was issued and served upon the assessee in

lieu of which returns were field.

3.02. The assessments were made under section 153(A) (of Income Tax Act, 1961)

read with section 143(3) (of Income Tax Act, 1961) for the A.Ys. 2000-2001 to

2004-2005.

3.03. That the A.O. made additions under section 153(A) (of Income Tax Act, 1961)

of the Act on the basis of incriminating materials found /

recovered at the time of search.

3.04. Feeling aggrieved and dissatisfied with the

additions made by the A.O. under section 153(A) (of Income Tax Act, 1961) on the basis

of incriminating material found during the search operation

conducted on 10/2/2006, the assessee preferred appeals

before the learned C.I.T.(A). And the learned C.I.T.(A).

dismissed the appeals preferred by the assessee and

confirmed the additions made by the A.O. under section

153(A) of the Act.

3.05. Feeling aggrieved and dissatisfied with the

impugned order passed by the learned C.I.T.(A). confirming

the additions made by the A.O. under section 153(A) (of Income Tax Act, 1961) of the

Act, the assessee preferred appeals before the learned

tribunal. It was contended before the learned tribunal that the

assessment for the A.Ys. 2000-2001 to 2004-2005 could not

have been made under section 153(A) (of Income Tax Act, 1961) as no

incriminating material was found at the time of search to

reopen the completed assessment.

3.06. Accepting the submissions made on behalf of the

assessee and relying upon the decision of the Delhi High Court

in the case of Commissioner of Income Tax Versus Kabul

Chawla reported in 380 ITR 573, the learned tribunal has

allowed the appeals preferred by the assessee and has deleted

the additions made under section153(A) (of Income Tax Act, 1961) for the

A.Ys. 2000-2001 to 2004-2005.

3.07. Feeling aggrieved and dissatisfied with the

impugned judgement and order passed by the learned tribunal

in directing to delete additions made by the A.O. under section

153(A) of the Act for the A.Ys. 2000-2001 to 2004-2005,

revenue has preferred present appeals with the aforesaid

proposed questions of law.

4.00. We have heard Mr.Varun Patel, learned counsel

appearing on behalf of the revenue. We have perused and

considered the assessment orders passed under section

153(A) of the Act as well as the order passed by the learned

CIT(A) as well as the impugned judgement and order passed by

the learned tribunal. The learned tribunal has deleted the

additions made under section 153(A) (of Income Tax Act, 1961), made on the

basis of incriminating material found during the search, on the

ground that under section 153(A) (of Income Tax Act, 1961) in respect of

undisclosed income and undisclosed assets detected during

the search could be brought to tax. In support of the above,

the learned tribunal has heavily relied upon the decision of the

Delhi High Court in the case of Kabul Chawla (supra).

4.01. Identical question came to be considered by the

Division Bench of this Court in the case of Principal

Commissioner of Income Tax-2 Versus Jay Infrastructure

and Properties Pvt. Ltd. rendered in Tax Appeal No. 740

of 2016 and considering the earlier decision of the Division

Bench in the case of Principal Commissioner of Income

Tax -4 vs. Saumya Construction Pvt. Ltd. rendered in Tax

Appeal No.24 of 2016 in which, it is specifically held that the

A.O. while framing the assessment under Section 153(A) (of Income Tax Act, 1961) of the

Act for the block period may make addition considering the

incriminating material found for the year under consideration

only which was collected during the search. The Division Bench

in the case of Saumya Construction Pvt. Ltd. (supra) in

paragraph Nos. 15, 16 and 19 has observed and held as under:

15. On a plain reading of section 153A (of Income Tax Act, 1961), it

is evident that the trigger point for exercise of powers

thereunder is a search under section 132 (of Income Tax Act, 1961) or a

requisition under section 132A (of Income Tax Act, 1961). Once a

search or requisition is made, a mandate is cast upon

the Assessing Officer to issue notice under section

153A of the Act to the person, requiring him to furnish

the return of income in respect of each assessment

year falling within six assessment years immediately

preceding the assessment year relevant to the

previous year in which such search is conducted or

requisition is made and assess or reassess the same.

Since the assessment under section 153A (of Income Tax Act, 1961) is

linked with search and requisition under sections 132 (of Income Tax Act, 1961)

and 132A of the Act, it is evident that the object of the

section is to bring to tax the undisclosed income which

is found during the course of or pursuant to the search

or requisition. However, instead of the earlier regime

of block assessment whereby, it was only the

undisclosed income of the block period that was

assessed, section 153A (of Income Tax Act, 1961) seeks to assess the

total income for the assessment year, which is clear

from the first proviso thereto which provides that the

Assessing Officer shall assess or reassess the total

income in respect of each assessment year falling

within such six assessment years. The second proviso

makes the intention of the legislature clear as the

same provides that assessment or reassessment, if

any, relating to the six assessment years referred to in

the sub-section pending on the date of initiation of

search under section 132 (of Income Tax Act, 1961) or requisition under section

132A, as the case may be, shall abate. Sub-section (2)

of section 153A (of Income Tax Act, 1961) provides that if any

proceeding or any order of assessment or

reassessment made under sub-section (1) is annulled

in appeal or any other legal provision, then the

assessment or reassessment relating to any

assessment year which had abated under the second

proviso would stand revived. The proviso thereto says

that such revival shall cease to have effect if such

order of annulment is set aside. Thus, any proceeding

of assessment or reassessment falling within the six

assessment years prior to the search or requisition

stands abated and the total income of the assessee is

required to be determined under section 153A (of Income Tax Act, 1961) of the

Act. Similarly, sub-section (2) provides for revival of

any assessment or reassessment which stood abated,

if any proceeding or any order of assessment or

reassessment made under section 153A (of Income Tax Act, 1961) is

annulled in appeal or any other proceeding.

16. Section 153A (of Income Tax Act, 1961) bears the heading Assessment in

case of search or requisition. It is well settled as held

by the Supreme Court in a catena of decisions that the

heading of the section can be regarded as a key to the

interpretation of the operative portion of the section

and if there is no ambiguity in the language or if it is

plain and clear, then the heading used in the section

strengthens that meaning. From the heading of

section 153 (of Income Tax Act, 1961), the intention of the legislature is clear

viz., to provide for assessment in case of search and

requisition. When the very purpose of the provision is

to make assessment in case of search or requisition, it

goes without saying that the assessment has to have

relation to the search or requisition. In other words,

the assessment should be connected with something

found during the search or requisition, viz.,

incriminating material which reveals undisclosed

income. Thus, while in view of the mandate of sub-

section (1) of section 153A (of Income Tax Act, 1961), in every case

where there is a search or requisition, the Assessing

Officer is obliged to issue notice to such person to

furnish returns of income for the six years preceding

the assessment year relevant to the previous year in

which the search is conducted or requisition is made,

any addition or disallowance can be made only on the

basis of material collected during the search or

requisition. In case no incriminating material is found,

as held by the Rajasthan High Court in the case of Jai

Steel (India), Jodhpur v. Assistant Commissioner

of Income Tax (supra), the earlier assessment would

have to be reiterated. In case where pending

assessments have abated, the Assessing Officer can

pass assessment orders for each of the six years

determining the total income of the assessee which

would include income declared in the returns, if any,

furnished by the assessee as well as undisclosed

income, if any, unearthed during the search or

requisition. In case where a pending reassessment

under section 147 (of Income Tax Act, 1961) has abated, needless to

state that the scope and ambit of the assessment

would include any order which the Assessing Officer

could have passed under section 147 (of Income Tax Act, 1961) as

well as under section 153A (of Income Tax Act, 1961).

19. On behalf of the appellant, it has been

contended that if any incriminating material is found,

notwithstanding that in relation to the year under

consideration, no incriminating material is found, it

would be permissible to make additions and

disallowance in respect of all the six assessment

years. In the opinion of this court, the said contention

does not merit acceptance, inasmuch as, the

assessment in respect of each of the six assessment

years is a separate and distinct assessment. Under

section 153A (of Income Tax Act, 1961), an assessment has to be

made in relation to the search or requisition, namely,

in relation to material disclosed during the search or

requisition. If in relation to any assessment year, no

incriminating material is found, no addition or

disallowance can be made in relation to that

assessment year in exercise of powers under section

153A of the Act and the earlier assessment shall have

to be reiterated. In this regard, this court is in

complete agreement with the view adopted by the

Rajasthan High Court in the case of Jai Steel (India),

Jodhpur v. Assistant Commissioner of Income

Tax (supra). Besides, as rightly pointed out by the

learned counsel for the respondent, the controversy

involved in the present case stands concluded by the

decision of this court in the case of Commissioner of

Income-tax-1 v. Jayaben Ratilal Sorathia (supra)

wherein it has been held that while it cannot be

disputed that considering section 153A (of Income Tax Act, 1961), the

Assessing Officer can reopen and/or assess the return

with respect to six preceding years; however, there

must be some incriminating material available with

the Assessing Officer with respect to the sale

transactions in the particular assessment year."

4.02. Similar view has been taken by this Court recently

in the case of The Principal Commissioner of Income Tax-

1 Versus Devangi Alias Rupa in Tax Appeal No.54 of

2017.

4.03. Considering the facts and circumstances of the

case, it cannot be said that the learned tribunal has

committed any error in deleting the additions made under

section 153(A) (of Income Tax Act, 1961) for the A.Ys. 2000-2001 to 2004-

2005 and/or any substantial question of law arise. In view of

the aforesaid binding decisions of this Court in Tax Appeal

Nos.749/2016 & 54/2017, we see no reason to interfere with

the impugned judgement and order passed by the learned

tribunal. No substantial question of law arise in this group of

appeals.

5.00. In view of the above and for the reasons stated

above and considering the binding decisions of this Court in

the case of Jay Infrastructure and Properties Pvt Ltd (supra)

and Saumya Construction Pvt. Ltd. (supra) and decision of the

Delhi High Court in the case of Kabul Chawla (supra), we see

no reason to interfere with the impugned judgment and order

passed by the learned Tribunal. No substantial question of law

arise in this group of appeals. Hence, all these appeals deserve

to be dismissed and are accordingly dismissed.

Sd/-

(M.R. SHAH, J.)

Sd/-

(B.N. KARIA, J.)

×

Questions

No Incriminating Material, No Tax Addition: Court Upholds Tribunal’s Decision

Write your CommentSimilar Posts

Generic

- Reportdata/2010.pdf